I get locked down, but I get up again…

Despite the successful start to the UK's vaccination programme, new strains of the coronavirus pull at the British economy. More widely, global governments tackle their own Covid-19 challenges at a variety of rates. But promisingly, the global economy appears to have contracted less than initially predicted. Our economics team analyse this and more in the latest Global Economic Overview.

Amid the gloom of lockdown in a UK winter, it is easy to focus on the negatives. The near-term battle against Covid has become harder, as new, more infectious, virus strains have emerged adding pressure on healthcare systems, thus prompting a tightening of social restrictions. As a result, we have downgraded our Q1 GDP forecast and we now expect quarterly contractions in output in the UK, the Eurozone and Japan. Yet the global economy seems to have contracted less than we thought in 2020. World trade and Asian economies appear to be recovering, the vaccine rollout is underway and further fiscal stimulus is on its way in the US and Europe. So in fact, our global growth forecast has been revised up, from 5.8% to 6.2% for 2021.

Joe Biden is determined to unleash a material amount of fiscal stimulus. On the coattails of the $900bn package at the end of last year, the new President is planning to launch a $1.9trn programme next month. Furthermore, the Democrats aim to push their "Build Back Better" plan later in the year. Incoming Treasury Secretary Yellen has put forward a case to "act big." But narrow majorities in both houses of Congress are leading the Democrats to seek bipartisanship with Republicans, which may water down some of the proposals. Also, it is not clear how former President Trump’s second impeachment trial in the Senate will affect cross-party congressional dynamics.

In the Eurozone, Germany and the Netherlands have adopted stricter lockdown measures with curfews imposed in France. These measures will come at a cost to their economies, probably bringing about a double-dip recession again in Q4 and Q1 after the rebound last autumn. With vaccine rollout also lagging and fiscal support lacking strength – a coalition partner pulled out of Italy’s governing coalition, depriving the government of its majority. As the Dutch government resigned, we have lowered our growth forecast for the Eurozone and predict the bulk of the rebound to come later in the year, with carry-over effects into next year. We now predict growth of 3.4% in 2021 (down from 5.2% previously) and 4.9% in 2022.

A "two minutes to midnight" Brexit deal and an impressive start to the UK’s Covid vaccination programme have both supported economic prospects over 2021. But the surge in daily coronavirus cases, driven by the increased transmissibility of the so-called "Kent variant", has led to a third national lockdown and is set to result in a sharp fall in GDP in Q1. Accordingly, we have downgraded our GDP forecast to 6.2% from 7.0% for this year, although we expect the economy to continue to grow robustly next year, by 5.3%. Helped by a likely diminution of the Covid threat, plus a softer US dollar generally, our baseline case is for cable to rise to $1.40 by the end of this year and to $1.53 by end-2022.

Global

Across the world, vaccination programmes are well underway. In order to unlock a return to social normality and economic growth, countries are racing to inoculate their populations. Israel is leading the charge to become the first nation to immunise its citizens, having vaccinated 41.8% thus far. So far, over 80% of people over 60 have received their second jab, and 70% of those between 45 and 60 years of age. The spread of the virus will continue to put pressure on governments worldwide to suppress transmission until vaccinations are sufficiently widespread to alleviate social restrictions.

Of course, how Covid evolves will be the key determinant of the path of global GDP this year. We remain upbeat on prospects in this regard, despite the resurgence of the virus leading to lockdowns over Q1. We suspect this to be temporary and that ultimately vaccine roll-out will allow social restrictions to be abandoned, supporting a release of pent-up demand. In terms of our forecasts, we see global growth of 6.2% this year, upgraded from 5.8%, and against a 2020 figure of -3.6%. Upgrades to 2021 have been driven by fast-recovering Asian economies, such as China and India, as well as the US, where we are factoring in further fiscal stimulus. Beyond this year we suspect a degree of the Covid recovery will be factored into 2022, our forecast standing at 5.1%.

Signs of strengthening in global growth are evident in a number of areas. For example, the recovery in global trade has been gathering pace: the latest October figures showed a 1.6% y/y fall, up from -14% in June. If anything, more timely data from heavyweight Asian exporters such as China, S.Korea and Indonesia have pointed to further recovery, December export growth ranging from +4 to 17% (3m yoy). However, a shortage of freight containers emerged as an unexpected impediment to global trade. This was most notable on the China-EU shipping route and consequently pushed up the price of a container from $2k (Oct) to $12k. Leaving shipping containers in the wrong places is one hangover from the pandemic, but we believe this will subside over time.

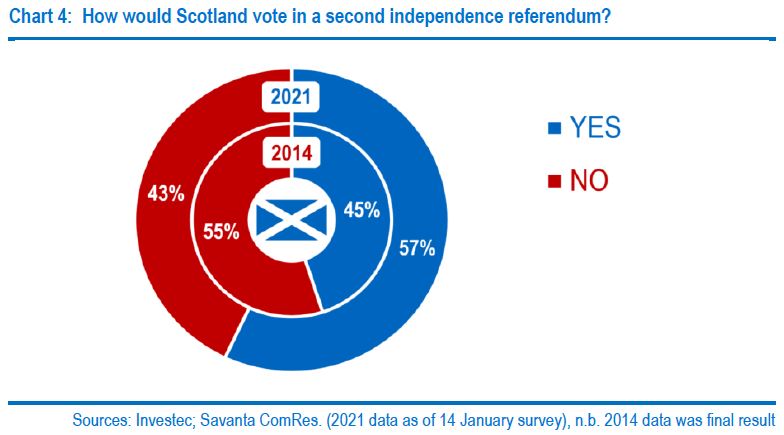

The global political scene makes for interesting viewing throughout 2021. The arrival of Joe Biden at the White House will help re-shape the face of global geopolitics. Relations between the US and China will need to be repaired, for example. In Europe, Merkel will step down in September after German Federal elections, raising questions of a power vacuum over the near and medium-term at the top of the EU. In the UK, a thorn in Boris Johnson’s side will be an SNP victory in the Scottish parliament elections in May (if they take place); and thus a call for IndyRef2. As Chart 4 shows, support for Scottish independence is close to a record high at 57% in favour, exc. people who said ‘I don’t know’.

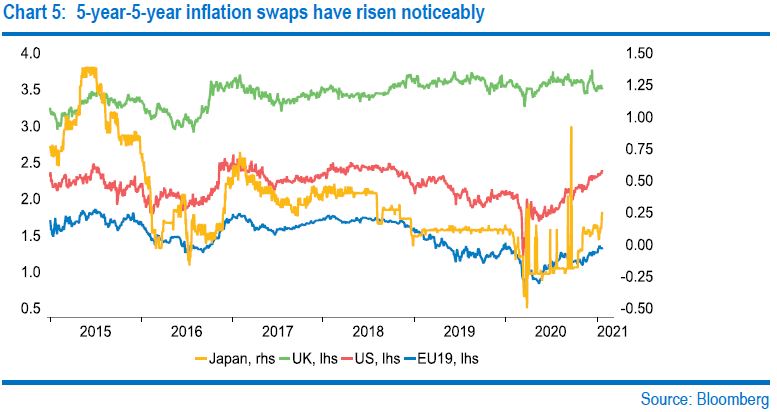

There has been a lot of talk about reflation. Market-based measures of inflation expectations, whether derived through breakeven inflation rates or from inflation swaps, have risen in the US and Europe, but are historically still low (Chart 5). Despite unquestionably huge monetary stimulus, central banks are battling deflationary forces from high spare capacity and what would be far higher unemployment still were it not for furlough. We hence remain sceptical that inflation will take off globally soon – mindful of the fact that bond yields have consistently confounded expectations of a rise since the ‘08/’09 recession, including when spare capacity was much lower.

Another important market question is over the path of the USD this year and next. Our central view is that it concedes further modest ground against major FX pairs. We judge a number of factors will be at play. Firstly, these include certain idiosyncratic country factors, such as an unwinding of negative sentiment surrounding GBP given the UK/EU trade deal. Secondly, an anticipated easing of the pandemic, a global economic recovery and positive risk sentiment should erode demand for safe-haven dollars. However, we are cognisant that one risk to the outlook is a faster reflation of the US economy. In that scenario, a new era under President Biden sees further stimulus, a more rapid recovery and market attention turning towards a possible earlier tightening of Fed policy.

United States

Georgia was on everyone’s minds in the 5 January US Senate runoffs. The Democrats narrowly won both, by 2.0% and 1.2% (Joe Biden carried the state by just 0.2% in November). The Senate is now split 50/50, with VP Kamala Harris’s casting vote giving the Democrats control. President Biden should now be reasonably able to pass legislation, but the wafer-thin majority means that centrist Democrats could constrain his agenda. The party’s majority in the House is also tight, at 10. Another potential limitation is time. Both Obama (2009) and Trump (2017) enjoyed clean sweeps for two years before losing one chamber of Congress at the subsequent midterms.

The Democrats’ Senate victory was kept off the top of the political news for a while by the storming of the Capitol and Donald Trump’s second impeachment. At the time of writing, it seems as though the former President’s Senate trial will commence on 9 February. A two-thirds majority is required for a conviction i.e. 17 Republicans need to vote with the 50 Democrats. Could this happen? We are doubtful, but it is not impossible, especially if senior GOP officials fear that Trump could lose the party the 2024 election. A conviction would enable the Senate to vote to prevent Trump from holding future office. Indeed outgoing Senate majority leader Mitch McConnell hinted he was open to voting to convict.

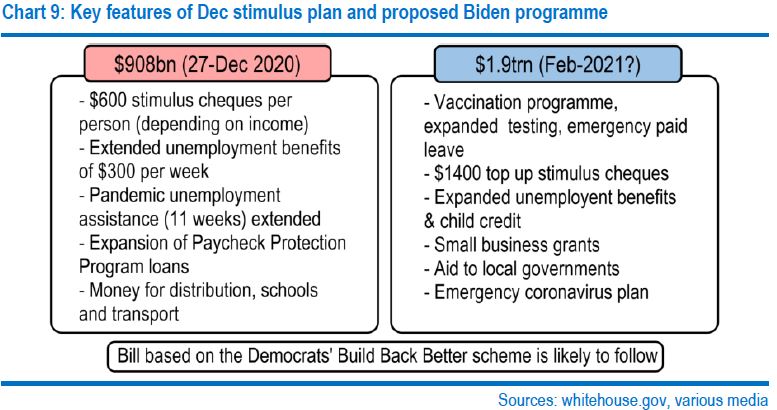

Hard on the heels of a $900bn stimulus deal passed late last year, Biden has lost little time outlining his own fiscal agenda. Proposals include spending amounting to $1.9trn and are shown (alongside those from December) in Chart 9. Senior Democrats hint that the plan is to pass this quickly before his "Build Back Better" programme (investment in infrastructure and "green" technology) is put together. The tight numbers in Congress could make this tricky and will require bi-partisanship, something in short supply in recent years. Hence, it could be halved to $1trn. But Democrats seem determined to force through material fiscal stimulus, with new Treasury Secretary Janet Yellen insisting on the need to "act big."

These events have ignited a new ‘reflation trade’, pushing the S&P500 index to repeated highs, shrugging off weak labour market and retail sales data. 10y Treasury yields rose to 1.19% at one stage. TIPS prices show that the trend so far this year is due to rising inflation expectations (rather than real yields), with breakeven yields hitting 2.11%, a 2½ year high. Fed officials have generally backed looser fiscal policy. Indeed a relentless rise in longer-term yields could well prompt the Fed to talk them down due to ‘an unwarranted tightening in monetary conditions’. We, therefore, see 10y Treasury yields rising modestly, to 1.25% at end-year and 1.75% end-next.

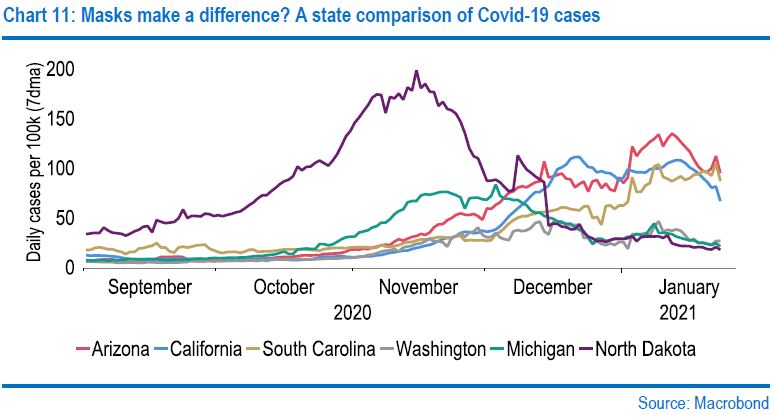

Priority number one for Biden will be tackling the pandemic. As Chart 11 reminds us, the spread of the virus has varied in different states. Cases rose late last year, leading to higher hospitalisation rates and greater fatalities (though daily infections have since come down). University of Washington estimates point to more than 566k deaths by May 1. Restrictions vary from state to state. As can be seen in North Dakota, cases have fallen sharply from Nov-20 as a result of compulsory mask-wearing. Biden is keen to hit the ground running and plans to vaccinate 100 million people in 100 days. His new executive order includes mask wearing for interstate travel.

In her recent Senate confirmation hearing, Janet Yellen conceded that how "Build Back Better" will be financed has not yet been decided. Tax hikes (including corporation and capital gains) may well be included. Even so, the emphasis will still be firmly on net stimulus. Overall we have pushed up our GDP forecast for this year to +5.3% (from +4.5%), with pre-pandemic (Q4 2019) levels of GDP hit in Q3 this year. We look for +4.2% in 2022. Whereas we do not see an upsurge in inflation, note the FOMC’s new mandate means that it has to compensate for periods of low inflation by aiming for inflation above 2% for a while. We still see the FOMC starting to shrink its balance sheet in H2 2023, but no hike until 2025.

Eurozone

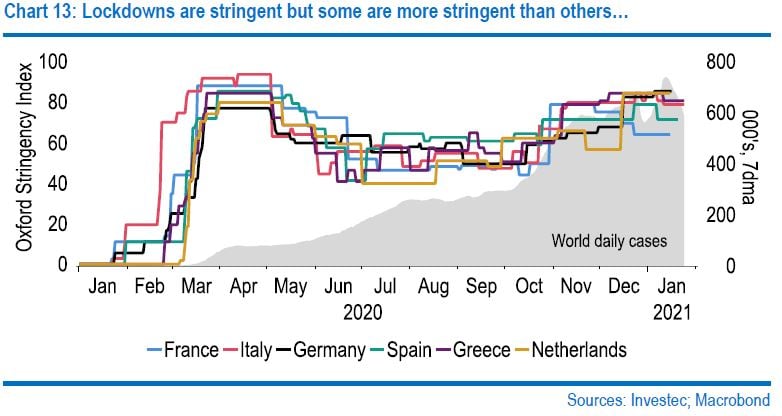

The pandemic continues to force the hand of European governments. As Chart 13 shows, as cases have risen, stringent lockdowns have been implemented. Moreover, these measures will continue well into February and March. In Germany, case numbers have eased back to November 2020 levels but concerns over the transmissibility of new variants, a rise in cases in other Euro area countries; coupled with a sporadic vaccination rollout across Europe, have kept lockdowns in place. As such, non-essential travel across much of the EU looks set to be banned. We see Q1 GDP of -1.6% (q/q) with Q2 GDP of 2.1%.

Whilst Covid developments will certainly be a driver of short-term macro-dynamics, in the medium term, prospects will in part be supported by fiscal stimulus stemming from the EU’s €750bn NextGenerationEU package. Crucial to this will be the early deployment of funds (this year), which in turn depends on national governments submitting their Recovery and Resilience Plans (RRP) by April, which will ultimately determine the disbursement of funds. To date, the European Commission has taken a less than enthusiastic view of some of the plans submitted so far. Nonetheless, given the funds on offer, we suspect this will be addressed, providing stimulus, which we believe will support annual growth of 3.4% in 2021 and 4.9% in 2022.

However, domestic political issues could potentially hamper the distribution of EU funds. In Italy, differences of opinion on spending plans almost caused the government to collapse in January when Matteo Renzi withdrew his party, Italia Viva, from the coalition. It survived a confidence vote, albeit with a loss of its majority in the Senate, undermining its ability to pursue its policy objectives. Political issues at the start of 2021 have been evident elsewhere too, with the Dutch government resigning over a child benefits scandal. It will continue to act in a caretaker capacity until March, but this too could disrupt spending plans. Indeed, political risks will be a feature of 2021 given the now fragile nature of Italy’s government, elections in the Netherlands as well as later in the year in Germany.

The ECB upped its stimulus measures in December to counter the disinflationary impulse of the pandemic, boosting the Pandemic Emergency Purchase Programme by €500bn to €1.85trn and extending liquidity operations that allow banks to borrow on favourable terms. As the economy has since developed broadly in line with its expectations – which importantly had assumed tight Covid restrictions throughout Q1 and only very gradual rollout of vaccines – no further measures were announced this month. The focus is on keeping financial conditions, in terms of lending rates, credit conditions and yields, favourable for households, firms and governments.

Eurozone inflation has held steady at -0.3% yoy for four months. Energy prices have exerted a key pull lower; excluding them, inflation would have been +½%. Germany’s temporary VAT cuts since July also weighed on inflation. Had they been passed on in full, this may have depressed inflation by 0.4-0.5pp; in practice, the impact was probably less. Still, base effects from both these factors clearly point to sharp temporary rises in Eurozone inflation in H1 2021. But the “underlying” rate of inflation is somewhere between ½% and 1%, and thus clearly depressed by spare capacity; without government support, importantly also for labour markets, it would be lower still.

The ECB upped its stimulus measures in December to counter the disinflationary impulse of the pandemic, boosting the Pandemic Emergency Purchase Programme by €500bn to €1.85trn and extending liquidity operations that allow banks to borrow on favourable terms. As the economy has since developed broadly in line with its expectations – which importantly had assumed tight Covid restrictions throughout Q1 and only very gradual rollout of vaccines – no further measures were announced this month. The focus is on keeping financial conditions, in terms of lending rates, credit conditions and yields, favourable for households, firms and governments.

Eurozone inflation has held steady at -0.3% yoy for four months. Energy prices have exerted a key pull lower; excluding them, inflation would have been +½%. Germany’s temporary VAT cuts since July also weighed on inflation. Had they been passed on in full, this may have depressed inflation by 0.4-0.5pp; in practice, the impact was probably less. Still, base effects from both these factors clearly point to sharp temporary rises in Eurozone inflation in H1 2021. But the “underlying” rate of inflation is somewhere between ½% and 1%, and thus clearly depressed by spare capacity; without government support, importantly also for labour markets, it would be lower still.

The euro has climbed in two steps last year, first from mid-February to early March and again through July. Since then, it has remained broadly steady, strengthening against the USD but weakening against the Yuan and GBP, which constitute its three largest trading partners. We expect most of these trends to persist, as the dollar loses more of its safe-haven allure in a post-pandemic recovery, and sterling, with the Brexit hurdle negotiated, moves towards closer towards long-term PPP estimates of “fair value”. In light of the shortfall of inflation vis-à-vis target, the ECB is likely to continue monitoring the currency closely.

United Kingdom

Averting the "no-deal" scenario, the UK and EU reached a Trade and Cooperation Agreement on Christmas Eve. Goods trade is free from tariffs and quotas, provided that rules of origin criteria, which set a minimum share of local content, are met. Extra paperwork and procedures have been introduced that make trade no longer frictionless and often add to business costs. For services trade, where the UK tends to run a sizeable trade surplus with the EU, the deal is much less comprehensive. And for financial services, in particular, there was effectively no deal. This leaves a number of areas yet to be ironed out. UK/EU trade negotiations, and dispute resolution, are likely to feature for years to come.

The UK vaccine rollout is well underway. All four nations have taken the same "top-down" approach - vaccinating those who are clinically vulnerable, frontline NHS staff and the elderly first. As new variants of Covid-19 are discovered, speed is everything. Whilst progress will differ across regions, the narrative remains on track that all adults will be offered the vaccine by the autumn. Overall, the pace of the UK rollout has been brisk. But UK governments will be wary about removing restrictions too soon. As such, we see Q1-21 GDP of 2.5% with a rebound in Q2-21 to 6.9%, pending any further restrictions.

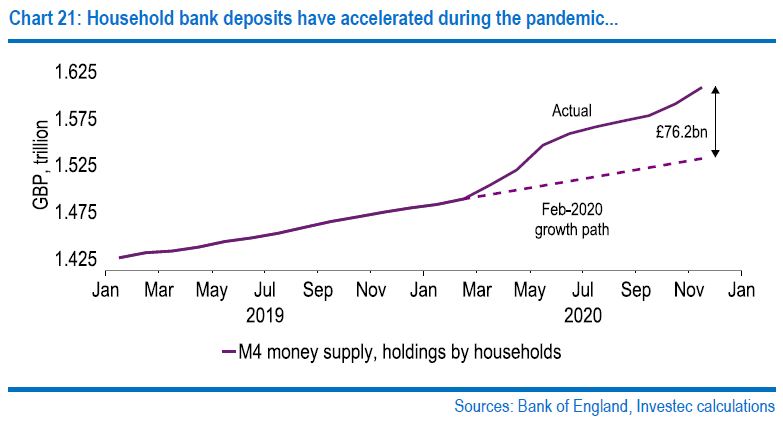

Social restrictions have supported spending on goods at the expense of services. Indeed in Q3, the annual growth of retail sales stood at +2.9%, while household consumption (which also includes services) was down 10.1%. Helped by government support, household incomes since the pandemic have remained close to Q1 2020 levels, while lower consumption pushed the saving ratio to record highs of 27.4% in Q2 and 16.9% in Q3. In turn, the stock of household bank deposits has accelerated (Chart 21). We estimate that such "excess savings" totalled £76bn in November, and if all of it were spent over 2021, this would add some 6% to consumer spending.

As in the US, UK government yields have risen, albeit less rapidly. 10y gilt yields are higher since the start of the year (now +0.29%), while equities have strengthened. This reflation trade has attracted much attention, but less noticed has been a softening in UK short-term interest rate expectations, as rumours of still tighter Covid restrictions has spawned renewed talk of a negative Bank rate. Indeed at the start of the year, the OIS curve was fully factoring a 25bp cut in the Bank rate to -0.10% by mid-2022. On 12 January, BoE Governor Andrew Bailey spoke of ‘issues’ with sub-zero rates, helping to dampen, though not extinguish, such speculation. Our base case remains that the MPC will avoid cutting rates again.

More likely is that it addresses short-term downside risks by stepping up the pace of its weekly QE purchases from the £4.4bn prevailing through much of H2 last year (the current rate of buying is clouded by the replacement of a large redemption). On fiscal policy, we still suspect Chancellor Sunak will signal limited tax hikes at the 3 March Budget, because he needs to show he is addressing the UK’s poor fiscal metrics. December’s data showed the cumulative deficit for 2020/21 so far to be £271bn, implying borrowing of some £340bn this year, below many estimates. But note that several pandemic schemes (e.g. CBILS) are not yet properly recorded in the data, which may give rise to upward revisions.

"Lockdown 3" is set to result in a contraction in the economy in Q1 and a delay in the UK’s recovery. Our GDP growth forecast for 2021 is now 6.2% from 7.6% previously. But we now see the rebound in activity following through into next year, clawing back a further 5.2% in 2022. Christmas Eve’s trade deal saw a muted reaction from the pound, with the expectation of a deal already priced in. That said, the possibility of negative rates continues to cap the currency. As vaccines are rolled out and confidence begins to spring back further into the year, we see the pound making up significant ground, with cable reaching $1.40 by end year and surpassing the $1.50 level in H2 next year.

Would you like to hear from our economists directly?

Sign up to receive invites to our fortnightly economic Q&A with a member of our team.

Browse articles in

Please note: the content on this page is provided for information purposes only and should not be construed as an offer, or a solicitation of an offer, to buy or sell financial instruments. This content does not constitute a personal recommendation and is not investment advice.