Desperately seeking stimulus for global recovery

With social distancing measures appearing to have brought the initial wave of the coronavirus pandemic under control in developed countries, many economies have now begun to ease their lockdowns. Data point to economic activity picking up. The Investec economics team set out their latest estimates in this month's Global Economic Overview.

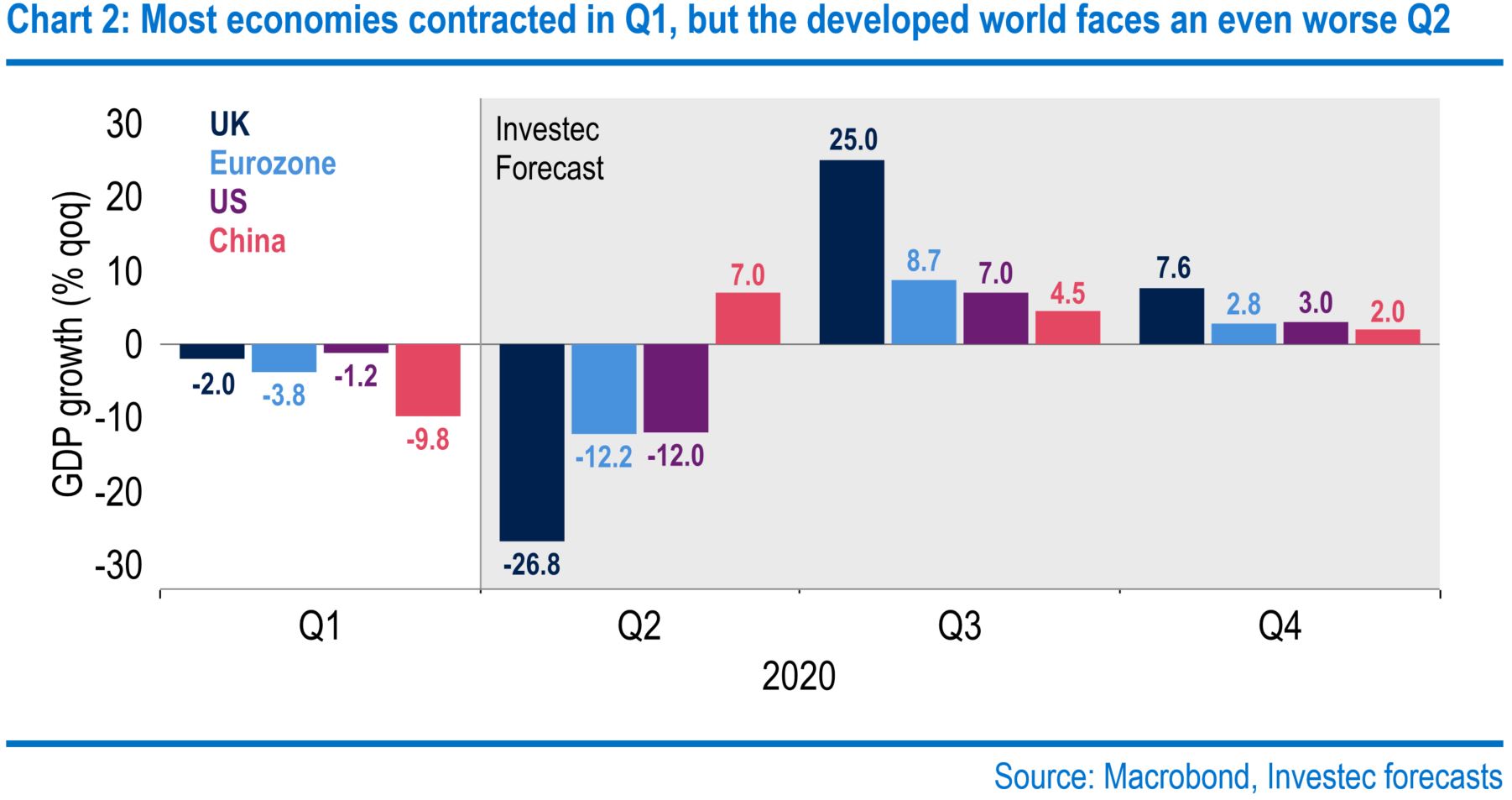

Evidence from the past month suggests that global activity has not only bottomed out but has gently risen off its lows. Providing that countries can continue to relax restrictions gradually without a spike in new cases, the recovery should take hold in the second half. In the absence of any significant surprising developments, we have made only modest tweaks to our forecasts - we still look for a contraction of 3.9% in world gross domestic product (GDP) in 2020, but we now see a rebound of 6.8% growth in 2021 (we previously estimated growth of 6.7%). Risks remain to the downside, with the rapid development and distribution of a vaccine being a critical factor if the global economy is to avoid significant "scarring".

Medical developments will be the key drivers for 2020 - our GDP forecast for this year remains at -5.6%. The impact is already evident in the labour market, with unemployment rising to 14.7% in April. However, states are beginning to reopen, with policy-aided businesses and consumers hoping to resume normal operations soon. US saving rates soared through lockdown, which could spur a mild spending boom through the third quarter. Still, economic risks remain and speculation of negative rates persists. However, the Federal Reserve has signalled it is not keen on this. President Donald Trump will look to reopen the economy to boost his approval rating ahead of this year’s presidential election, which history suggests he needs to do if he's going to win a second term.

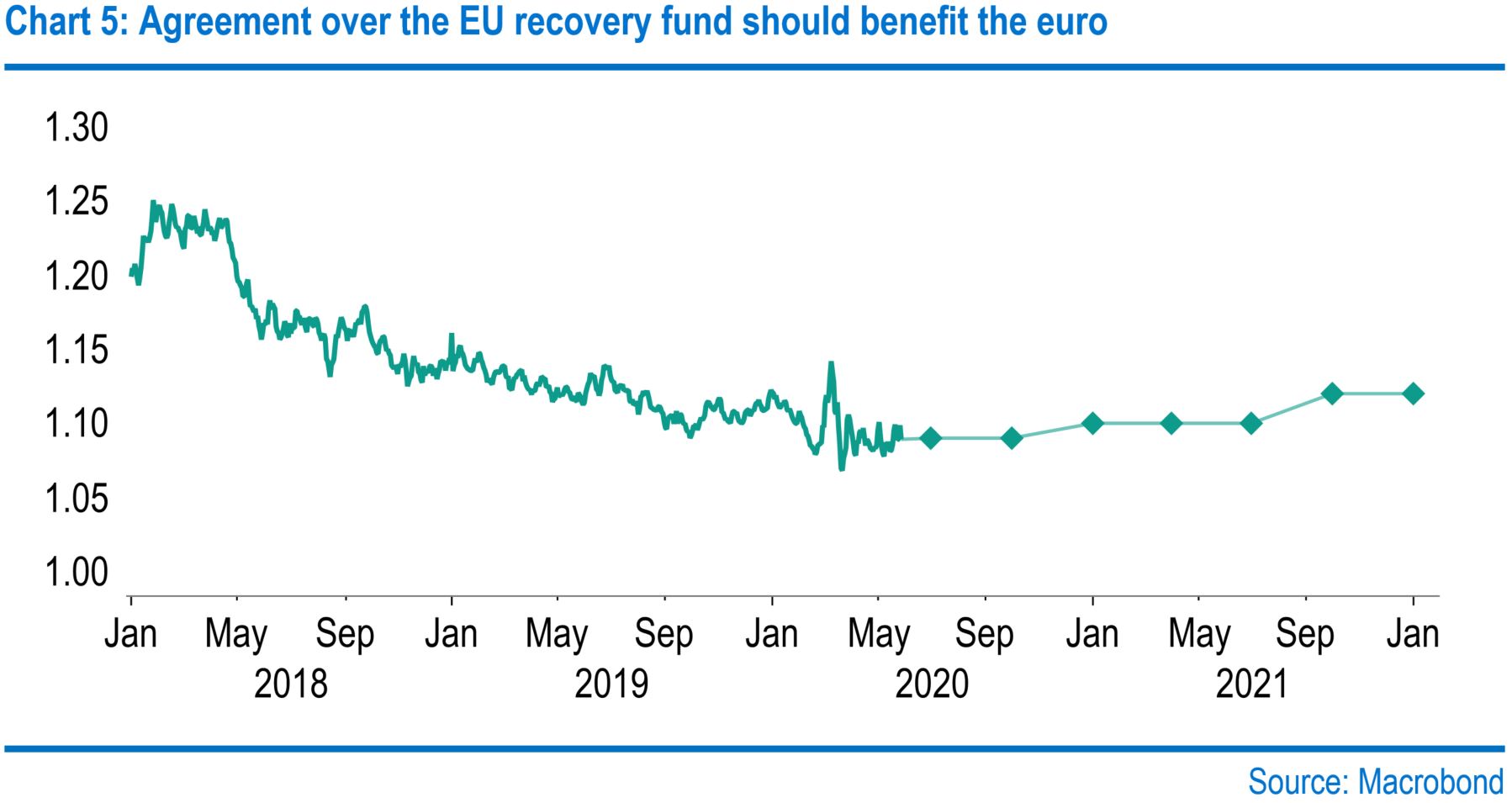

Eurozone GDP fell by 3.8% in the first quarter compared with the last three months of 2019. The second quarter will see a much sharper drop as shutdowns only took hold in March. We look for a decline of 8% in 2020 output, followed by a modest rebound of 5.5% in 2021. Looking forward, how social restrictions evolve and the public reaction to them will in the short-term be the key driver of any economic recovery. We expect European Central Bank policy to remain accommodative for some time. While we have dropped our forecast for a deposit rate cut in the second quarter, we see no change in rates until late 2023. We would not rule out additions to the ECB's quantitative easing programmes, despite the German Constitutional Court ruling seemingly casting doubts on this. The shift in our ECB view sees our near-term euro-dollar forecast revised to $1.09 in the second and third quarters, with our fourth quarter expectation remaining at $1.10.

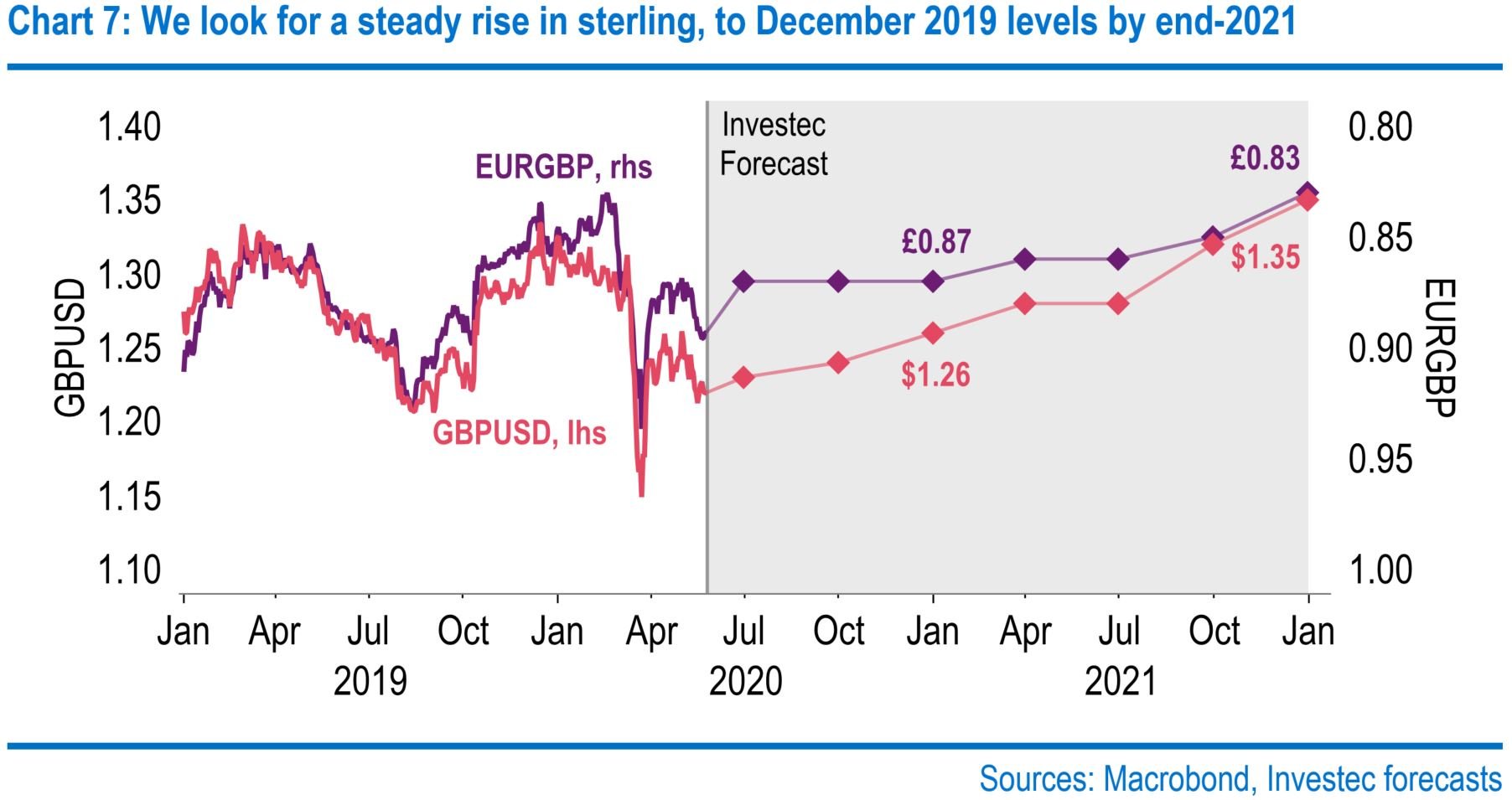

Our forecast for a drop of 10.8% in UK GDP in 2020 would probably be the largest contraction in output since 1709. Surveys point to an improving situation through the late-second quarter, though a sizeable contraction over the quarter as a whole is inevitable. The relevant coronavirus metrics are coming down, prompting the government to begin easing restrictions. It will look for this sooner rather than later, as public debt levels are set to soar following the mitigating policy decisions. Talk of negative rates is growing louder in the UK and is showing up in various bond yield curves, including negative short gilt yields, though we think the Bank of England will avoid this. There were huge increases in lending to corporates in March as firms moved to shore up their cashflow. In terms of a European Union trade deal, we suspect a zero-tariff goods arrangement will be agreed. Our end-year sterling forecast is unchanged at $1.26 and 87 pence against the euro.

Global

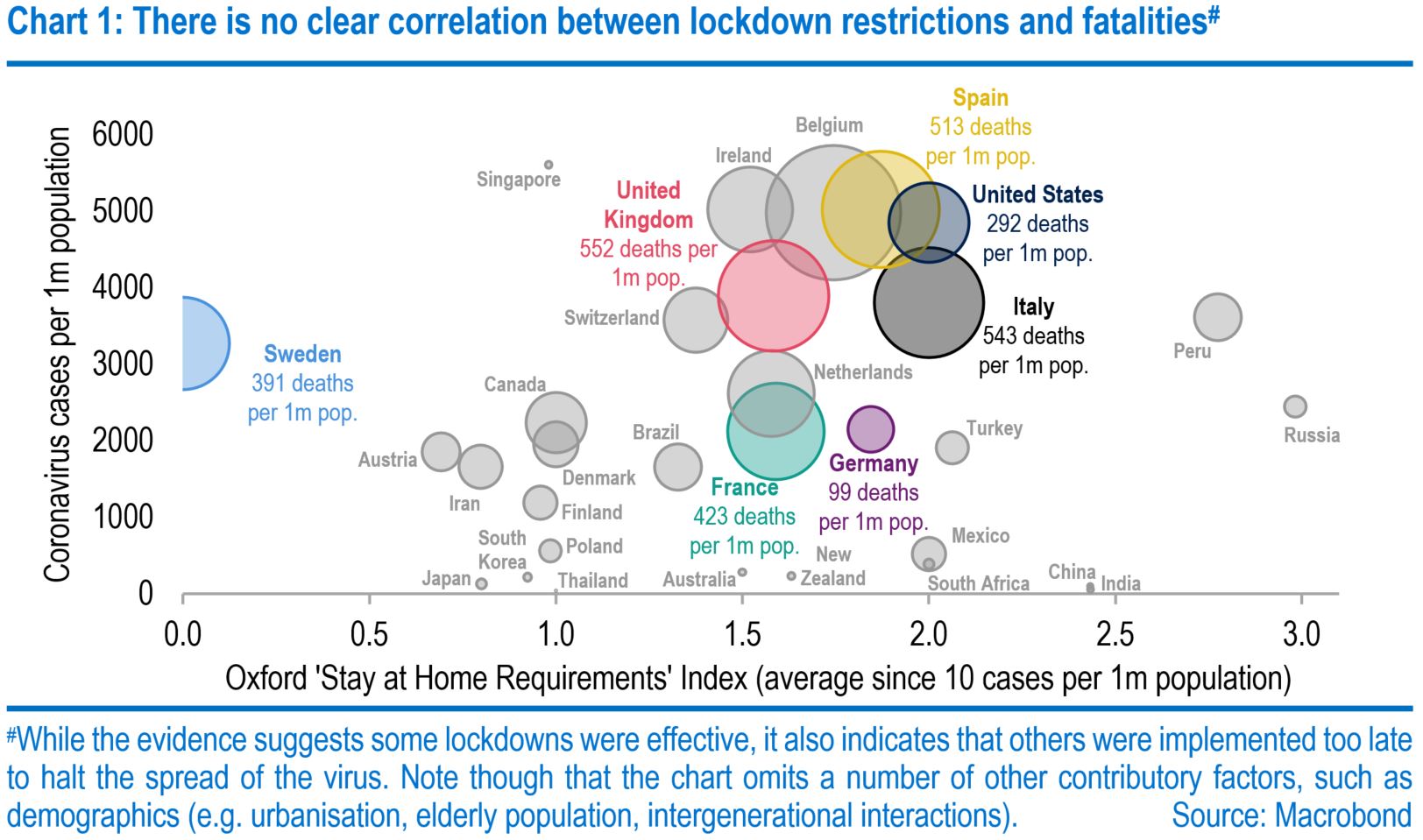

While the number of confirmed Covid-19 cases now stands at over 5 million, the initial wave appears to have been brought under control. To date, the daily infection rate has averaged just 2.2% in May, down from 4.8% in April and 8% in March. However, this improving pattern is not universal. Both Brazil and Russia look to be struggling, with the two countries accounting for one in four new cases globally despite comprising less than 5% of the world population. But this is the exception, with the majority of countries beginning to relax social distancing measures as their focus shifts from tackling a health crisis to preventing a prolonged economic slump.

Among the furthest down the path to normality is China, where the virus originated late last year. After a record 9.8% quarter-on-quarter (QoQ) decline in GDP in the first three months of the year, high-frequency data suggest that activity has risen off its lows. But the recovery may be hampered by a potential second wave, with lockdowns recently imposed in parts of Jilin province in the northeast of China. Consequently, Beijing has decided to not adopt a growth target for the first time since 1990. In fact, 2020 will likely be the first full-year contraction since the 1.6% decline at the end of the Cultural Revolution in 1976. It will also mean that China will fall short of its goal of doubling GDP between 2010 and 2020, which would require growth of 5.5% this year.

One headwind to China's recovery is set to be the subdued global trade backdrop, given that most other geographies are only just beginning to emerge from lockdown. As in China, the initial economic impact of these has been eye-watering - both the US and UK saw the sharpest declines in GDP since 2008, while the eurozone recorded the biggest drop since the common currency area was established. But the second quarter is set to be weaker still given that the first full lockdown in the Western hemisphere was not until 9 March in Italy. Still, we suspect that the worst has now passed, as suggested by the improvement in the flash Purchasing Manager Indexes (PMIs) in May. Providing that countries can continue to relax restrictions without a spike in new cases, the recovery should take hold in the second half.

But activity is unlikely to return to pre-virus levels until a vaccine can be developed and widely administered. Typically this process has taken a decade or even longer, with the current record being four years. Fast-tracked trials can shorten these timescales - Oxford researchers believe their vaccine may be available as soon as September, with the chances of success judged to be 50%. But accelerating the subsequent approval stage (usually one year) will be tricky - a 1950s polio vaccine rubber-stamped in a few hours caused several deaths. Generally, epidemiologists believe that a vaccine is 12 to 18 months away, meaning that social distancing will likely need to be maintained at least into 2021.

The uncertainty surrounding this is one of the many downside risks to our global growth forecasts, which is still for a contraction of 3.9% in 2020 but followed by a rebound of 6.8% in 2021 (previously +6.7%). Despite this, risk assets have rallied over the past two months. This has seen the MSCI ACWI Index recoup more than half of its peak-to-trough loss of 33.8%. Based on its current trajectory it would regain its pre-virus peak in the second half, although history suggests a full recovery may be some way off. But one reason why this rally might have legs is that policy looks set to remain highly accommodative for the foreseeable future, with expectations central banks will launch further stimulus.

There has even been growing speculation that more central banks will implement negative interest rates. While recent comments from policymakers have sought to quash any suggestion of this in the near-term, they have certainly not ruled them out at a later date. Though some market metrics have begun to price in the possibility of sub-zero rates, overnight index swaps (OIS) suggest that policy rates will remain close to current levels. We share this view: there is a high bar for negative rates in "virgin" countries given various side-effects elsewhere. But we would certainly not rule them out in the UK or even the US if the downturn becomes more profound and more prolonged than we currently anticipate.

United States

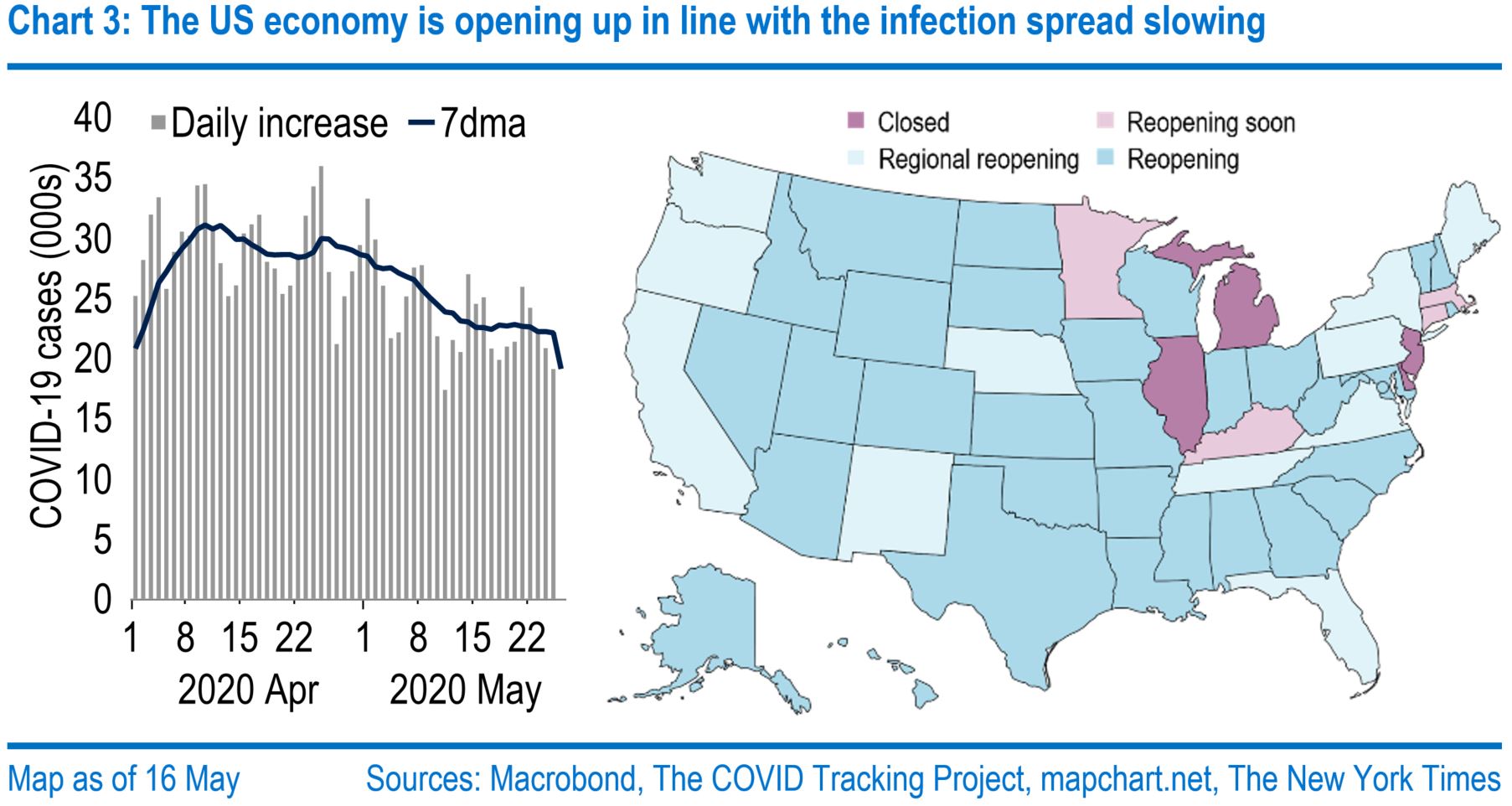

Federal Reserve Chair Jerome Powell has put it on the record that the medical metrics are the most important data for the US economy. Indeed, for as long as they remain the critical determinant of state-level restrictions on activity, they will underpin the economic path ahead. Across the US, the daily rise in cases is on a moderating trend, and this has paved the way for at least a partial re-opening in activity across a majority of states. Two other critical medical metrics are advances in the development of effective treatments and vaccines, with these set to determine whether a much bigger re-opening can take place spurring a more rapid economic recovery. One consideration is whether the reaction function of Donald Trump's administration to such data - and therefore its message to states on easing restrictions - will shift as the November Presidential election gets closer. The April labour market report laid bare the consequences for households of the restrictions in place, with unemployment at 14.7%. If there was one bit of the report to take heart from, it was that 78.3% of "job losers" were on temporary layoff.

With re-openings more amenable to outdoor sectors such as construction it seems likely we will see a recovery in these sectors first. Elsewhere, a slower recovery is expected and some unemployment may persist. Indeed, the persistently high levels of jobless claims provide a concerning message that many firms have not accessed schemes such as the Paycheck Protection Program, perhaps throwing in the towel. Hence, although policy support has been very sizeable, the Trump administration may need to do more to limit scarring. Small businesses remain a critical worry. The Economic Injury Disaster Loan program for small firms has been so overwhelmed by demand that it has significantly limited the size of loans, while blocking nearly all new applications. Congress is very likely to top up support again, but whether it provides enough and soon enough will influence long-term damage.

One feature of the restrictions has been the sharp rise in personal saving, with rates surging to Ronald Reagan-era highs, when higher saving was actively sought. In March, personal outlays fell by $1.2 trillion, with this reduction in consumption also evident in Fed data which put revolving consumer credit outstanding down 30.9% year-on-year (YoY) in the same period. We suspect that as restrictions are eased, some of those savings set aside will be spent, but perhaps moderately, with re-opening likely phased, confidence still shaky and unemployment elevated. Nevertheless, from such significant disruption, this should spur recovery over the second half overall. For now, we maintain our GDP forecasts at -5.6% for 2020 and +4.5% for 2021.

Doubts that the current overall stance of policy is sufficiently accommodative, even with further fiscal stimulus, have led to bets in markets that interest rates will fall further. Since April, the effective (traded) federal funds rate has averaged five basis points, within the 0%-0.25% target range. Fed funds futures are pricing in rates below this and have even strayed into negative territory on occasion. However, Fed officials, including Chair Powell, are not keen on negative rates. One argument against is that this would penalise banks, given they would have to pay to park the vast amount of liquidity at the Fed, the counterpart to massive amounts of quantitative easing (QE). Our main case view is that the Fed will keep the funds target at its current range until mid-2023.

Doubts that the current overall stance of policy is sufficiently accommodative, even with further fiscal stimulus, have led to bets in markets that interest rates will fall further.

Amid the enormous disruption that has come with the coronavirus, questions are being asked over what this means for the presidential race. If it is anything to go by, the outcome of the 12 May special election in California’s 25th Congressional District provides hope for Mr Trump. Here, a Republican newcomer, Mike Garcia, easily overturned 2018’s Democratic victory in a poll that was conducted primarily by mail. Mr Trump's net approval rate has held steady so far, even in recent days amid scrutiny over the high number of US Covid-19 cases. But at current levels (i.e. circa -9%), looking back at history, President Trump will want to improve this somehow to lift his hopes for re-election.

Eurozone

In the first official GDP figures that partially cover the coronavirus crisis, GDP was estimated to have fallen by 3.8% QoQ in the first quarter. There were material differences in performance over the quarter, predominantly linked to lockdown rules. Indeed, those countries introducing the most restrictive measures and at earlier dates witnessed the most significant GDP falls such as France (-5.8%), Italy (‑4.7%) and Spain (-5.2%). Meanwhile, at the other end of the spectrum, Finland saw a 0.1% rise.

However, with the coronavirus only really hitting the euro area during the last month of the quarter, and lockdown remaining in pace in the more recent months, the second figure is set to be far worse - we forecast a 12% drop on the quarter. Still, there are some modest signs of hope that the worst of the economic hit has been passed. For example, May's Composite PMI witnessed a rebound to 30.5 from April's record low of 13.6.

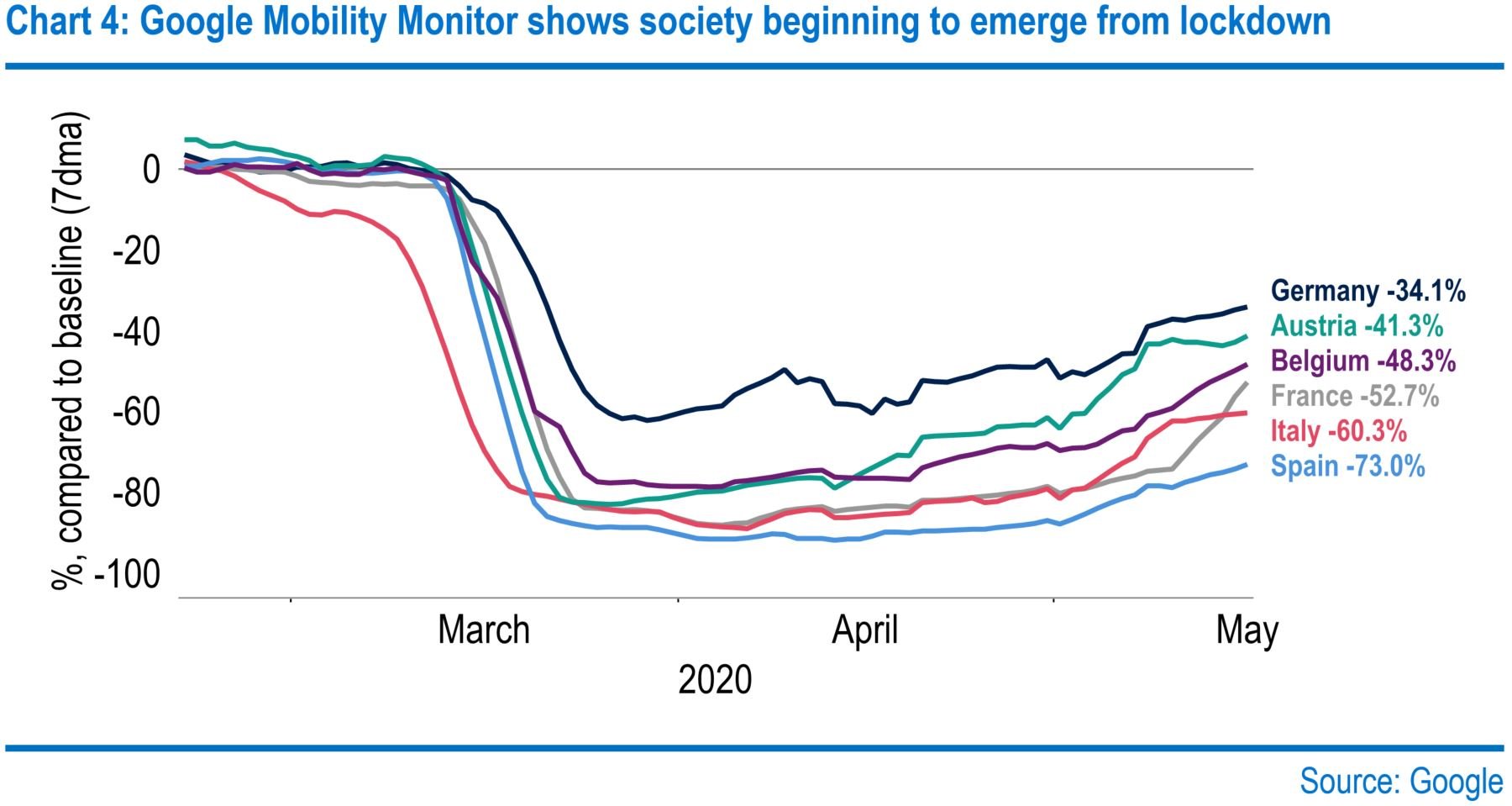

Other indicators such as business climate surveys in Germany and Belgium have echoed the signs of improvement in May too. Of course, the critical factor here is the gradual relaxation of containment measures being announced through the course of May. The University of Oxford's stringency index, which estimates the level of stay-at-home rules, highlights these developments following lockdown in April.

Looking forward, how social restrictions evolve and the public reaction to them will in the short-term be the key driver of any economic recovery. Google's activity monitor provides some fascinating insight on this front. Firstly, the mobility figures broadly tally with the first quarter GDP data in terms of relative country performance. Secondly, the numbers suggest a gradual but general strengthening in the pace of economic activity through the course of the second quarter so far. Our broad forecast continues to be for a material rebound in the third quarter, but one that is insufficient to overturn the contraction in the second quarter. Indeed, we do not see the level of fourth-quarter 2019 GDP being surpassed by the end of 2021. Following the first-quarter data, our GDP forecasts are unchanged at -8% in 2020 and +5.5% in 2021.

Despite positive effects from lifting the lockdown measures, there looks set to be some permanent economic scarring which will limit the scope of the recovery. Consequently, ECB policy will remain exceptionally accommodative for some time. However, we have dropped our forecast for a 10 basis-point deposit rate cut in June - our expectation is now that rates will remain at current levels until late 2023. Indeed, there have been two cuts in the borrowing rate for the ECB's new targeted longer-term refinancing operations (TLTRO III) - banks can now borrow at up to 50 basis points below the deposit rate (i.e. -1%). It could be argued that this has become the de facto benchmark policy rate and could see more adjustments.

Despite positive effects from lifting the lockdown measures, there looks set to be some permanent economic scarring which will limit the scope of the recovery. Consequently, ECB policy will remain exceptionally accommodative for some time.

We would also not rule out an increase in the ECB's €750-billion pandemic emergency purchase programme (PEPP). But changes here would come at a politically sensitive time following a German Constitutional Court ruling that raised doubts over the legality of the ECB's public-sector purchase programme (PSPP). Note that a European Court of Justice (ECJ) decision in 2018 ruled that purchases were within the ECB's mandate, while the Bundesbank has put forward a report aimed at answering the Court's questions. But the consequences of this disagreement could be far-reaching and undermine the European Union's legal framework should other national courts now challenge EU law. The European Commission has also become embroiled in the row, citing the supremacy of EU law and warning of infringement proceedings against Germany's court.

The questions over the ECB's QE programmes may well have been a factor in a historic agreement between German Chancellor Angela Merkel and French President Emmanuel Macron to create a €500 billion EU recovery fund. The groundbreaking part of this is that the European Commission will issue debt and provide grants rather than loans to member states. The final details still need to be agreed, with some northern countries opposing the idea of transfers. But should the plan be signed off, it would take some of the pressure off the ECB and would also mark the first small step in greater fiscal unity within the Eurozone. Arguably, this should be euro positive. This and our change in ECB view sees our near term euro-dollar call nudged up to $1.09 in the second and third quarters. Our fourth-quarter forecast still stands at $1.10.

United Kingdom

During the 2008 global financial crisis, we often sought comparisons with the 1930s to gauge the depth of the contraction in activity. In the current climate, we need to go further back. First-quarter GDP fell by 2% QoQ. Since then, the scale of the weakness in April's data (e.g. an 18.1% drop in retail sales) suggests our forecast of a 27% fall in the second quarter is in the right ballpark. Even with sizeable rebounds of 25% in the third quarter and 7.5% in the fourth quarter, GDP would fall by 10.8% this year with a peak to trough of 28%, compared with 6% in 2008-09. Historical studies suggest this would be the worst year since 1709.

Under scrutiny are prospects of an upturn in the second half of the year. May's flash PMIs recovered by more than expected from April's record lows - the composite index rose to 28.9 from 13.8. In theory, this means activity fell again between April and May, albeit at a more modest pace. But anecdotal evidence such as transport usage and electricity demand suggests output has risen since mid-April, albeit relatively slowly, as restrictions have been gradually eased. A declining fatality rate helps the case for re-opening more retail stores on 15 June and other parts of the economy in July if the government judges the reinfection rate (R0/R) is sufficiently below 1. The speed with which test and trace can be introduced and a vaccine can be developed will also be critical.

.JPG)

Our GDP forecast +9.7% in 2021 would leave output nearly 2% below pre-pandemic levels at the end of the year. We judge the risks are to the downside if the government is more hesitant in unwinding the lockdown. The chancellor has been bold in launching measures to protect company cashflow and household incomes, but we are now getting an idea of the price tag. Office for Budget Responsibility (OBR) analysis suggests a total cost of £123 billion over 2020-21. The Coronavirus Job Retention Scheme (CJRS), funding the furloughing of workers, is the costliest scheme at £50 billion (net of taxes received on wages). The OBR's latest scenario now envisages borrowing at £298 billion. At some stage, it may be necessary to tighten fiscal policy to safeguard sustainability. But not yet.

In terms of the overall policy stance, the direction is that more stimulus is likely, at least via the Bank of England. The central bank's Monetary Policy Committee (MPC) looks set to sanction a further £100 billion of QE on 18 June, after its next meeting. Moreover, in a 180-degree shift over recent weeks, MPC members, including Governor Andrew Bailey, now say they are actively investigating the possibility of taking the central bank's primary interest rate below zero from the current record low of 0.10%. In common with US markets, the UK yield curve is taking this prospect seriously and is currently pricing in a 45%-50% chance of a 25 basis-point cut to -0.15%. Our central case is that the MPC will not go down this route.

We would not rule out sub-zero rates in the UK, but the BOE would be very wary before introducing them.

A big issue with negative interest rates is the banks. With £644 billion of reserves currently parked at the BOE, they would face a 15 basis-point charge, around £1 billion per annum in total (rising as more QE is added). A de facto tax on banks would be risky when economic prospects depend heavily on credit flow availability. Indeed, bank lending to corporates in March surged as firms acted to secure their cash flow. Other economies, such as the Eurozone, have negative rates, but the ECB tiered its system of liquidity remuneration last year to ease the cost to banks and has not cut its deposit rate below -0.50%. Instead, it now lowers the cost of borrowing through one of its liquidity schemes, TLTRO III. We would not rule out sub-zero rates in the UK, but the BOE would be very wary before introducing them.

Sterling has traded in a range of $1.2075-$1.2650 over the past month. Fears of negative rates have weighed, but a possible resignation of Boris Johnson's top aide, Dominic Cummings, is lending upside on hopes of a less hawkish stance to EU trade talks. There may now be a higher chance of an extension to the transition period before end-year. Our base case has been that both sides agree on zero tariff goods trade, with latitude on checks to limit logjams at each side of the border. We note too that the government announced a schedule of Most Favoured Nation tariffs, including scrapping tariffs on £30 billion of imports from countries where the UK has no trade deal. Our end-year view on the pound is unchanged at $1.26 and 87 pence against the euro.

If you would like to discuss how the coronavirus impacts your exposure to risk, get in contact with us

Browse article in