Public or Private

13 June 2023

As IPO activity slows on both sides of the Atlantic, what does this mean for investors in public and private assets?

5 min read

13 Jun 2023

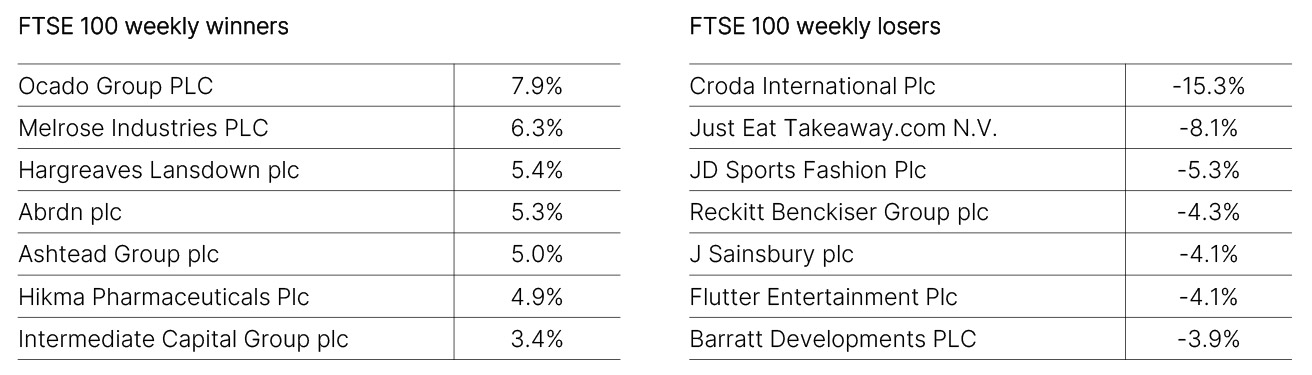

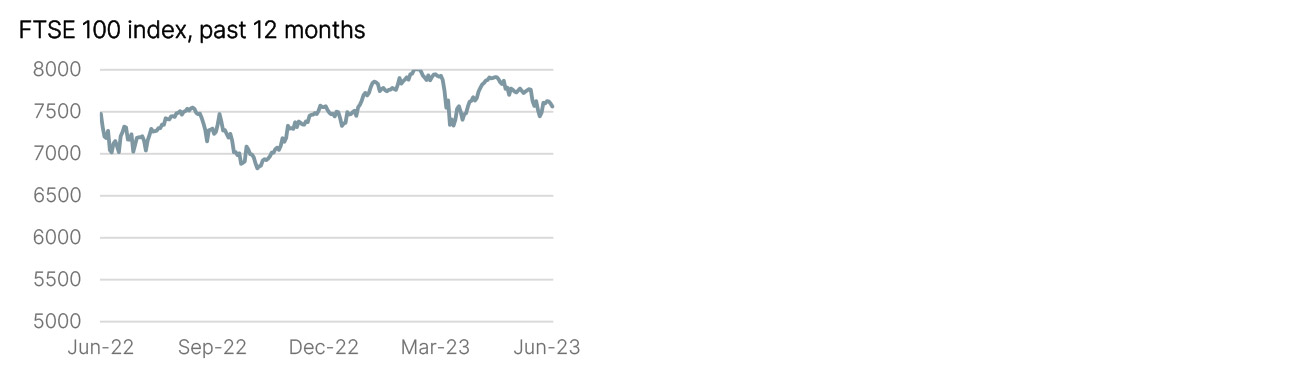

Welcome to our Economic Highlights, bringing you market updates from across the UK, US, Europe and China, as well as the FTSE weekly winners and losers.

The UK Purchasing Managers’ Index (PMI) print for May was released with both the composite and service prints showing some resilience - 55.2 and 54 respectively - indicating moderate growth. Additionally, a construction PMI data print of 51.6 showed some divergence with weakness in housebuilding, whilst civil engineering projects were stronger.

Initial jobless claims came in at 261,000 in the week ending 3 June, which was the highest print since October 2021 – this suggests that the US labour market is continuing to cool. The other data point indicating further cooling in the US economy was the ISM service index, which surprised on the downside with a print of 50.3 against a consensus figure of 52.4. Against this weakness, the final print of S&P’s US composite PMI print for May came in close to consensus at 54.3.

The headline news event during the period was the final print of Eurozone GDP for Q1, with the updated figure showing a print of -0.1%. Given an identical print of -0.1% in Q4 2022, the latest data now indicates that the Eurozone entered a technical recession over the period. More positively, composite Eurozone PMI data for May came in at 52.8, which is lower than the consensus forecast of 53.3 and still suggests that the Eurozone is currently in expansion territory. Producer price data came in at 1% year-on-year in April, which was better than the consensus figure of 1.7% - this suggests a reduction in inflationary pressures over the medium term.

The May Consumer Price Index (CPI) and Producer Price Index (PPI) prints came in at 0.2% and -4.6% respectively, with the latter indicating some medium term deflationary pressures in the Chinese economy. Further evidence of a cooling in Chinese data was seen in both the import and export figures for May, with a year-on-year decline of -4.5% and -7.5% respectively. The Chinese composite PMI figure for May was however more resilient with a print of 55.6.

The information in this document is for private circulation and is believed to be correct but cannot be guaranteed. Opinions, interpretations and conclusions represent our judgement as of this date and are subject to change. The Company and its related Companies, directors, employees and clients may have positions or engage in transactions in any of the securities mentioned. Past performance is not necessarily a guide to future performance. The value of shares, and the income derived from them, may fall as well as rise. The information contained in this publication does not constitute a personal recommendation and the investment or investment services referred to may not be suitable for all investors. Copyright Investec Wealth & Investment Limited. Reproduction prohibited without permission.

Member firm of the London Stock Exchange. Authorised and regulated by the Financial Conduct Authority.

Investec Wealth & Investment Limited is registered in England.

Registered No. 2122340. Registered Office: 30 Gresham Street, London EC2V 7QN.