Speed bumps on the road to recovery

World economic growth prospects remain strong this year as governments unveil fiscal support packages, pandemic restrictions ease and vaccination programmes gather speed. Still, there is a risk that the recovery diverges as some countries see a resurgence of the coronavirus. We have trimmed our growth forecasts for the world and Europe in our latest Global Economics Overview, but see a more robust performance in the US and the UK.

Some countries are immunising their populations rapidly against Covid, but the pandemic is sweeping through others again, especially in India, Brazil and parts of the European Union. But the broad direction of travel is still one of optimism regarding world growth in 2021, as markets eye a gradual loosening of restrictions. We concur, but we have pulled our 2021 global gross domestic product (GDP) forecast down by 0.3 percentage points to 6.2%, principally as China uses space to deleverage its financial sector. But China can already achieve its target of more than 6% GDP growth in 2021, even if its economy treads water for the rest of the year. We now estimate China's economy will expand about 9% this year (compared with our previous forecast of 9.8%). Against rising short-term interest rate and inflation expectations, government bond yields have risen sharply. For example, 10-year Treasury yields are up by 74 basis points on the year so far. However, note that market predictions have tended to overestimate the level of yields since the financial crisis, which has nudged us to make relatively modest changes to our forecasts.

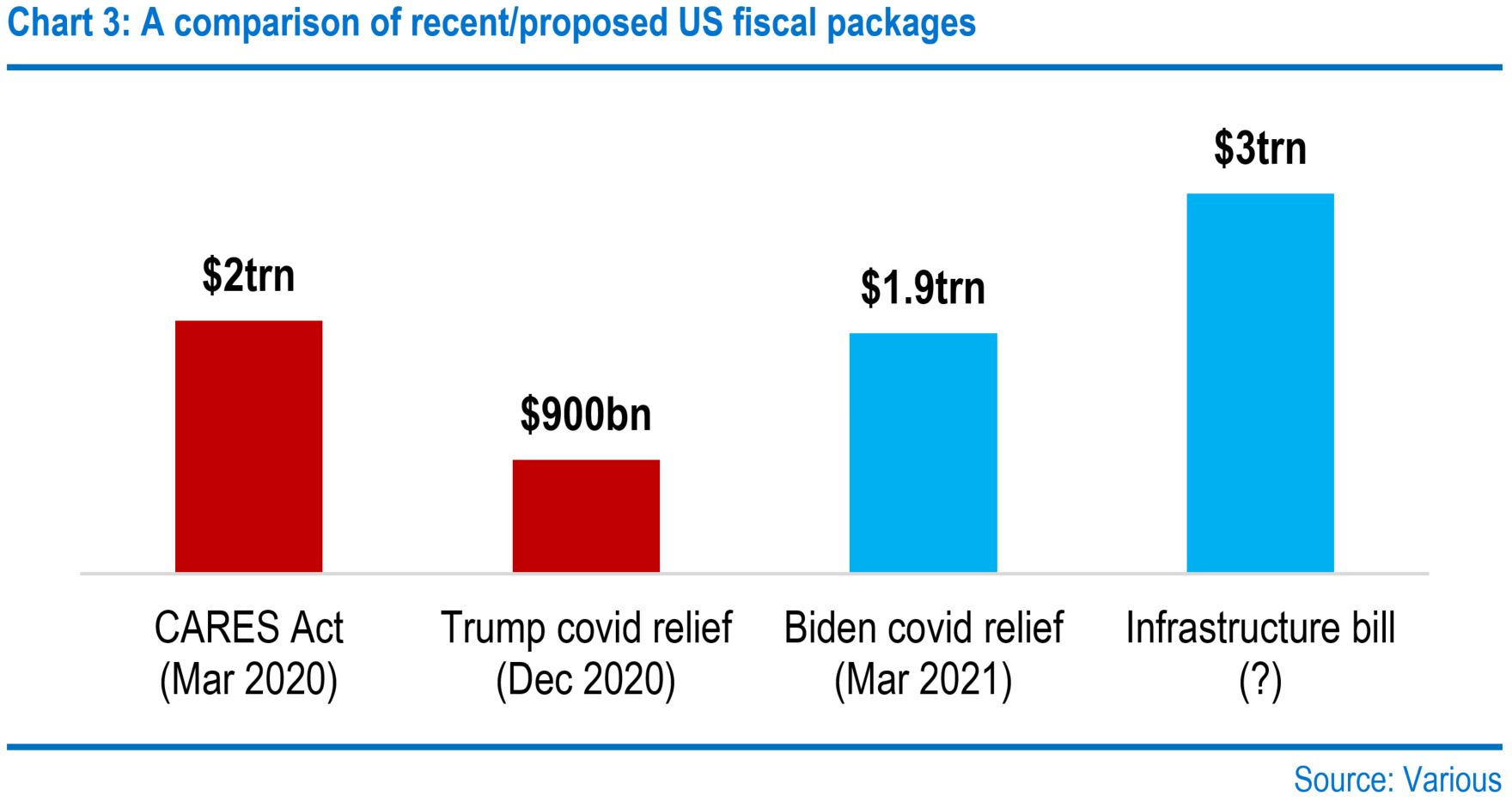

March saw US President Joe Biden sign his $1.9 trillion American Rescue Plan into law, adding to Donald Trump’s $900 billion Covid Relief package. Taken together, this represents an unprecedented fiscal boost worth 13% of GDP. But more stimulus is on the horizon, with the White House considering a multi-trillion dollar infrastructure plan. As such, we forecast growth of 5.9% in 2021, but a figure over 6% is entirely possible. Meanwhile, we have revised our 2022 forecast upwards to 4.8%. For markets, the critical question is what the upgraded outlook means for Federal Reserve policy, with an interest-rate increase in the first quarter of 2023 now fully priced into the curve. Given the Fed’s desire to make up for periods of low inflation, we suspect that the first hike in the Fed funds target rate range will come later in the fourth quarter of 2023. Ahead of a move in rates, we expect the Fed to announce a tapering of asset purchases at the end of this year.

Attention remains firmly focused on the race between the spread of the newer and more contagious strains of Covid-19 on one side and vaccinations on the other. So far, the pace of inoculations has been too slow to contain, let alone diminish the disease’s incidence. As a result, social restrictions have had to be extended in several countries. This will hold back the economic recovery in the second quarter and explains the European Central Bank’s insistence on countering any tightening in financial conditions for the time being, including its decision this month to front-load quantitative easing bond purchases. But if vaccinations take the planned step up during the second quarter, then activity should rebound strongly. Still, we have cut our 2021 GDP growth forecast from 4.6% to 4.4%, and our 2022 forecast from 5.2% to 5% as a result.

Domestically, the economic outlook has brightened. Monthly GDP data for January revealed that economic activity was more resilient than expected during the country’s third national lockdown, contracting by 2.9% on the month, relative to a consensus forecast of a 4.9% drop. In light of this, we have upgraded our first-quarter GDP forecast to -1.8%, which lifts our annual 2021 growth forecast by 0.9 percentage points to 7.3%. On monetary policy, we have opted to shift our first Bank of England interest-rate increase forward by a period of six months to mid-2023. This reflects the optimism regarding the economic recovery’s strength and timing, underpinned by the impressive pace of vaccine rollout, enabling a faster move towards normality than once envisioned.

Global

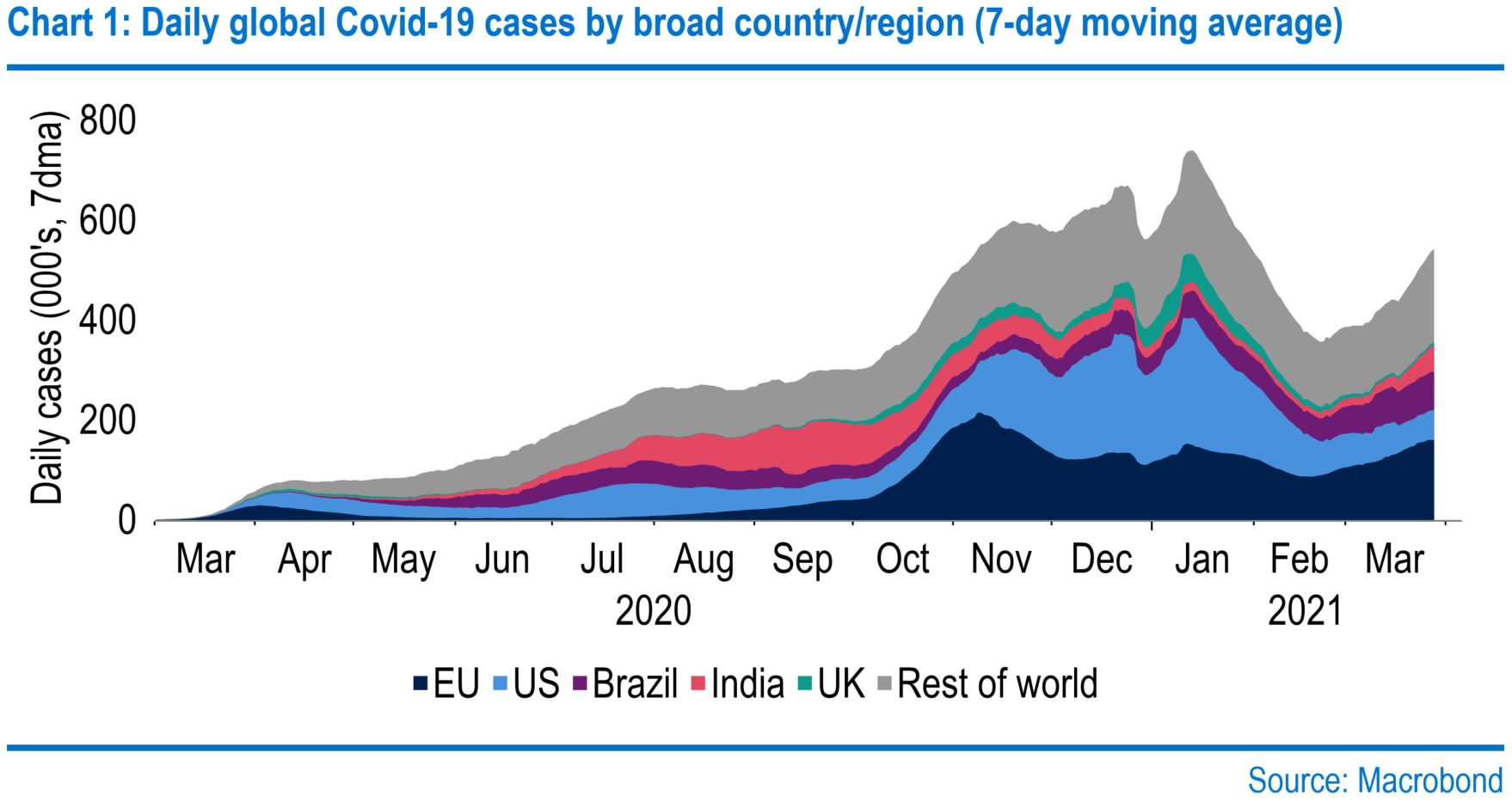

Markets have been looking toward the end of the Covid pandemic, encouraged by the fast pace of vaccinations in various countries. Israel still leads the way, while the UAE and the UK have also immunised more than half of their adult populations. Impressive as this is, new waves of the virus are sweeping through other countries. India and Brazil are now topping the list of daily cases, but there is also a resurgence in various western and eastern European nations, in particular France and Poland. The net result is that the number of global daily cases and fatalities are now climbing, resulting in periodic nerves in equities and supporting the US dollar.

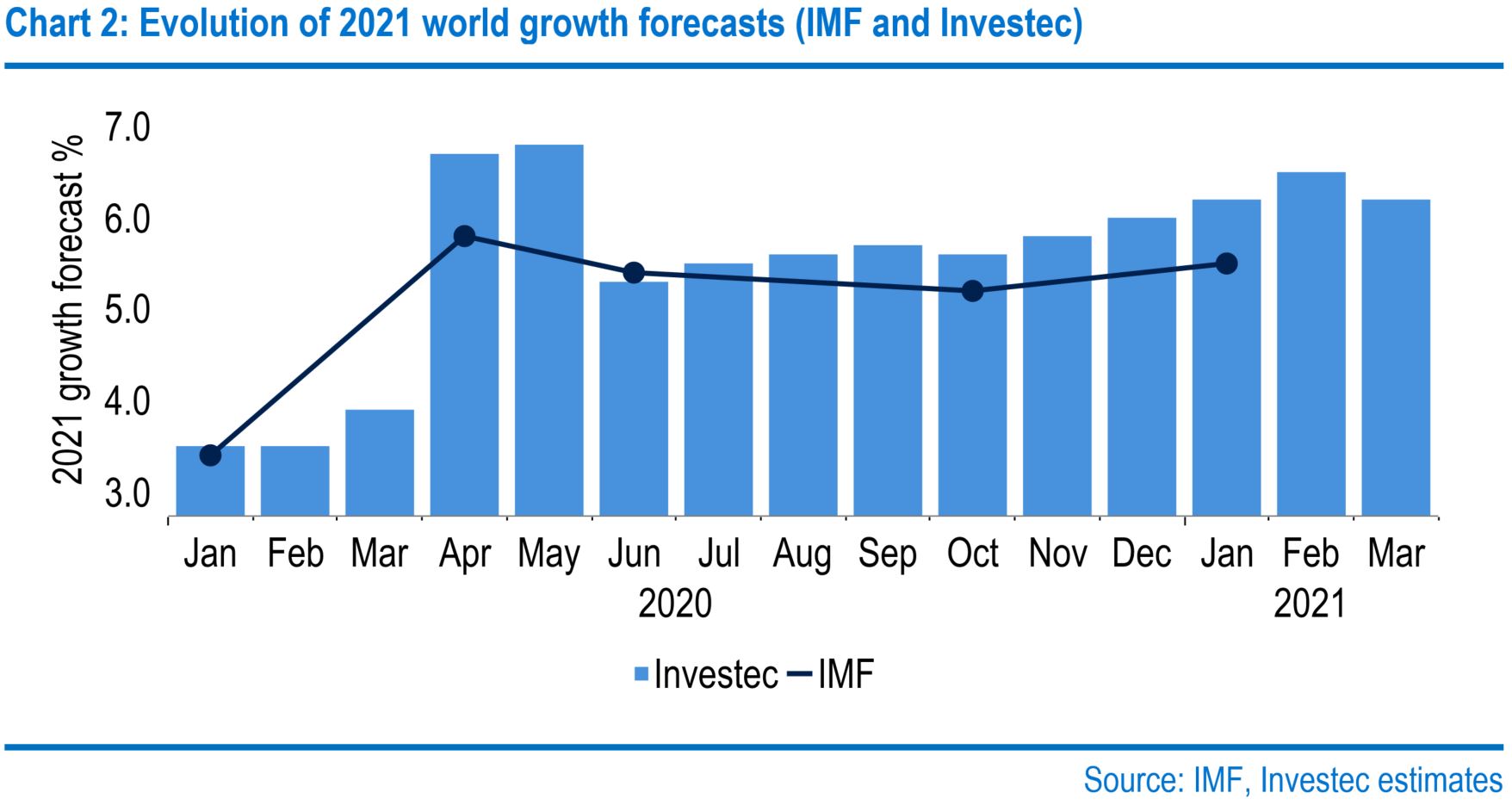

That said, in last month’s Global Economic Overview, we noted that some economies had performed better than expected in the fourth quarter of last year. Economies appear to have gained resilience under lockdown with activity holding up impressively – the UK in January is a good example. Overall, our forecasts of world GDP for 2021 have increased since the back end of last year (Chart 2), reflecting increased optimism, although this is partly due to the magnitude of US fiscal stimulus. However, our growth forecasts are a touch lower this month, mainly because of our view on China. We now look for 6.2% and 5.1% growth this year and next, compared with 6.5% and 5.2% previously.

At China’s recent National People’s Conference, policymakers set a target of above 6% GDP growth in 2021 compared with 2020, an unambitious goal given that the country can reach it on base effects alone and near-zero quarterly growth this year. Premier Li Keqiang himself admitted that China may achieve a faster growth pace and that the focus is more on guiding expectations. Indeed, with China set to benefit from US stimulus, we expect growth to be closer to 9% in 2021. This is a 0.8 percentage point downgrade on our last forecast. We are mindful of the room the lower target leaves for Beijing to implement a policy of reducing financial risk, having already ordered all levels of government to lower their debt levels and banks to trim their loan books this year.

Since the start of the year, a common global theme in markets has been the rise in inflation expectations. A combination of large fiscal stimulus, ultra-loose monetary policy and renewed economic optimism has led market spectators to debate the potential for an increase in future inflation. We can see this in five-year, five-year inflation swap rates, a market measure of where investors believe five-year inflation will be in five years. In the US, the UK and the euro area, markets have upgraded their medium-term inflation expectations. Since the start of the year, euro-area expectations have risen the fastest of the three, but expectations are still firmly below the ECB’s "below, but close to, 2%" target.

In the most recent forecast round, the European Central Bank (ECB) and the Fed made large upward revisions to their inflation outlook for 2021, with the BOE making a more modest upgrade. Indeed, the Fed increased their PCE inflation estimate from 1.8% to 2.4%, significantly above their 2% target, in light of the $1.9 trillion US fiscal stimulus package. In comparison, the inflation outlook beyond 2021 was left relatively unchanged, with only minor upward revisions made across the three central banks. This reinforces the narrative reiterated by both Fed Chair Jerome Powell and ECB President Christine Lagarde that any increase in inflation this year will be a purely transitory rise, which is somewhat at odds with market expectations.

One consequence of recovery trades has been the steepening of yield curves. This has been led by the US, where 10-year Treasury yields have risen by 74 basis points over the year, but other markets have followed with gilt yields increasing 57 basis points and Bund yields gaining 23 basis points. It might seem tempting to extrapolate these increases looking ahead. But although we consider some upward revisions to be justified, we are cautious on the extent of any forecast changes. One of the biggest forecasting mistakes in the post-financial crisis era was to overestimate bond yields. Although significant fiscal stimulus might be a game-changer this time, it still seems right to be prudent.

United States

President Joe Biden's $1.9 trillion American Rescue Plan was signed into law, passing the Senate via the vice president's casting vote. This year's total fiscal boost is now $2.8 trillion, or 13% of GDP, and while we are sticking with our 5.9% 2021 GDP growth forecast, expansion well above 6% is possible. Next will be the administration's infrastructure plan, which looks as if it will be a $3 trillion package, perhaps spread over 10 years. The Democrats aim to fund it with tax hikes partly. Still, the knife-edge party balance in the Senate casts doubt on the feasibility of sanctioning any tax rises, which would maximise the total fiscal stimulus. On this basis, we are raising our 2022 GDP growth forecast to 4.8% from 4.2%.

Markets are scrutinising Fed comments for changes in signals over the likely timing of its stimulus measures' winding down. The Federal Open Market Committee (FOMC) maintained the Fed funds target at 0%-0.25% this month. The central bank's median "dot plot" projection indicated that policymakers would keep it there until after the end of 2023. Markets disagree – the curve is fully factoring in a 25-basis point increase in the first quarter of 2023. No one can be confident about timing, including FOMC members. While fiscal policy will likely pump-prime demand, it is not clear how much wage inflation will ensue. For now, unemployment is elevated at 6.2%, and we note that wage growth failed to reach 3% in the post-financial crisis period, even when the jobless rate fell below 4%.

Also, as we pointed out last month, the US's primary inflation measure has been running 0.4 percentage points below the central bank's 2% objective over the past 10 years, giving the FOMC licence to aim for inflation above 2% for a while via its "makeup" strategy. Overall, we are now looking for a Fed hike in the fourth quarter of 2023 (we previously forecast 2025), partly reflecting the view that the FOMC will leave its balance sheet contraction until later. With Fed members reticent to push back against a steeper yield curve, we think 10-year Treasury yields will rise faster than we previously thought – we now see 10-year Treasury yields rising to 1.75% by the end of the year, compared with 1.25% previously. However, higher mortgage rates may dampen housing activity and slow the economy, acting as a brake on curve steepening.

Important for Fed policy will be how the labour market evolves. The FOMC's projections envisage the unemployment rate falling to 4.5% in the fourth quarter of 2021, 3.9% in the fourth quarter of 2022 and 3.5% in the fourth quarter of 2023 – the latter two being classed as "full employment" since they are below the long-run estimate of 4%. Assuming trend population growth and a swift rebound in participation to pre-pandemic levels, this would require monthly payroll growth to average 700,000 for the rest of this year, 300,000 in 2022 and 120,000 in 2023. With our GDP forecasts, this would imply labour productivity growth of 2%, 1.75% and 0.75%, respectively. But labour productivity and participation rates may evolve differently, altering the speed of unemployment falls.

The Fed's $80 billion per month in asset purchases has been a notable presence in the treasury market. However, it is also worth considering net issuance, where supply has outstripped purchases every month other than between March and May 2020. Looking forward, this is set to continue, with the possibility of 2021 net Treasury issuance reaching $2.8 trillion, should issuance in the second half of the year match that in the first half. This figure could rise even further should a proposed multi-trillion dollar infrastructure plan pass Congress by then. That begs the question of whether this might impact market conditions later this year should the Fed taper its purchases. To date, the market has absorbed supply, but one or two weak auctions have raised concerns.

One question is whether we are potentially facing a stronger US dollar. The correlation recently between the widening in 5-year yield spreads and a firmer dollar suggest that rate differentials are a key theme in currency markets at present. However, there is a multitude of other considerations, which can quickly change in their importance. For example, risk sentiment and safe-haven demand were the key drivers last year. At present, we are not minded to change our forecasts radically. Still, given the potential US economic recovery, fiscal stimulus, possible Fed taper, and our expectations of a faster rise in US Treasury yields relative to other G-10 markets, there is a risk that the US dollar strengthens rather than weakens as currently embodied in our forecasts.

Eurozone

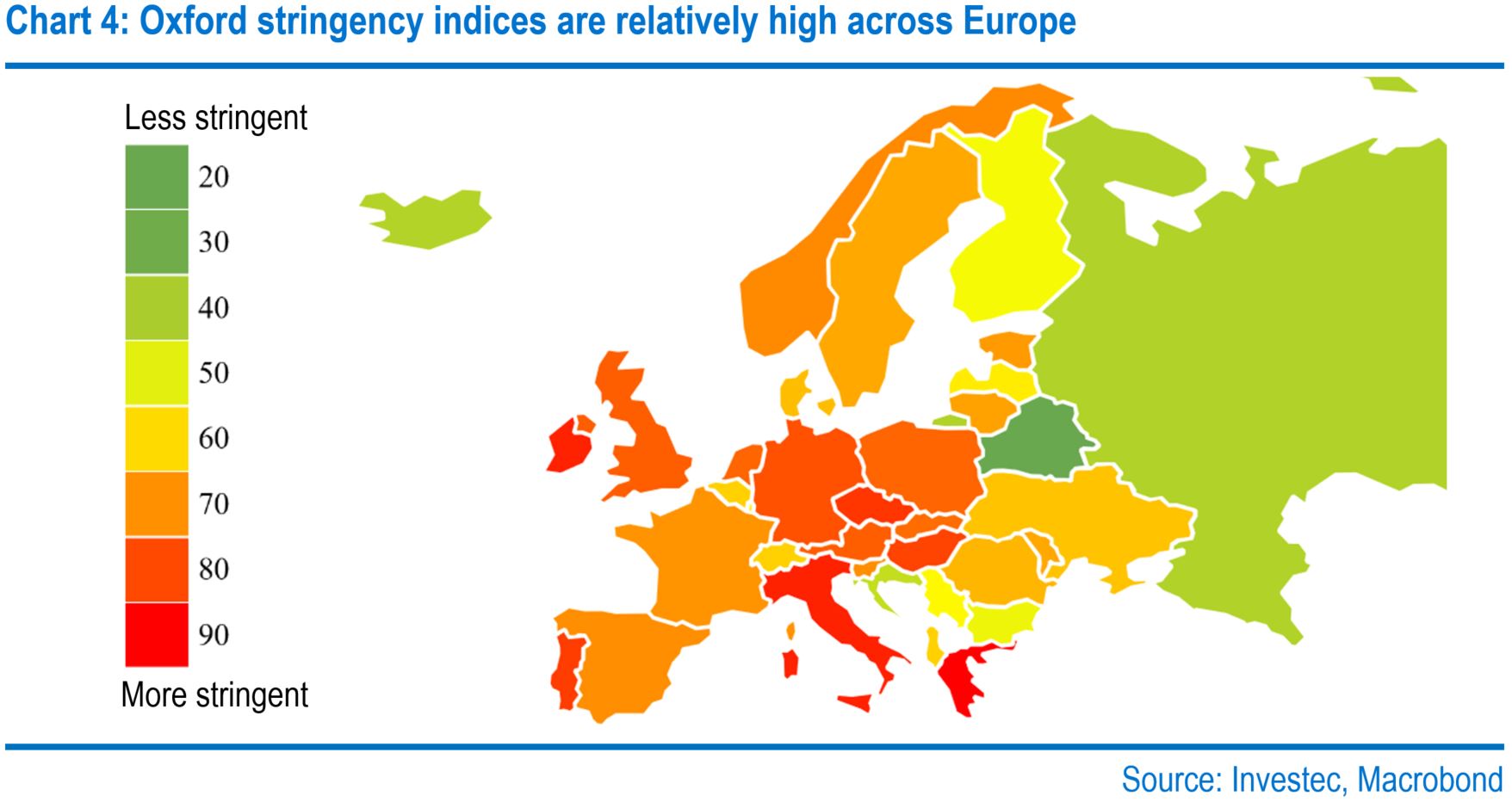

An upturn in cases over the last month has prompted European governments to reassess their coronavirus restrictions. While announcing a three-week extension to Germany’s lockdown until 18 April, Chancellor Angela Merkel pinned the recent surge on the more infectious variant originating in Kent. Although President Emmanuel Macron has been keen to keep France “open”, he has had to bring in new measures, including a third national lockdown.

These rising infections and tighter social rules represent a renewed headwind to near-term economic activity. As such, we have downgraded our Eurozone GDP forecasts for 2021 and 2022 to 4.4% and 5%, respectively. However, while we have nudged our outlook for the first half of 2021 down, we see this as a short delay in the recovery and expect progress in vaccinations and an unwinding of social restrictions toward the end of the second quarter to prompt a significant rebound in activity in the third quarter. In terms of economic growth distribution, the four core countries are expected to see faster expansion than the remaining 15 countries, which is unusual. That reflects the differing severity of the downturn in 2020 and hence the likely size of the rebound.

Like their counterparts in the UK and the US, euro-area households have boosted their savings during the pandemic, providing scope for increasing spending once social restrictions ease. But we estimate excess savings relative to past trends to have been lower than in the UK and the US, perhaps partly because services have a lower weight in consumer spending in the euro area. Moreover, there have been significant divergences between the major euro-area countries. France stands out as having accumulated a relatively large amount of excess savings, at 2.7% of GDP. In contrast, Germany finds itself at the other end of the spectrum, at just 0.8% of GDP.

March’s ECB meeting saw the central bank’s Governing Council commit to a significant pickup in the pace of asset purchases over the next quarter in response to rising sovereign yields. Policymakers gave no specific guidance on the exact size of purchases, but the first week’s data has shown an uptick to €21 billion, 50% higher than the average in January and February. We estimate that monthly purchases will lie in the €70 billion-€100 billion range. But this will be flexible and influenced by broader financial conditions. Note that this is in addition to the €20 billion per month purchased under the original Asset Purchase Programme (APP). More broadly, our views around ECB policy envisage the Pandemic Emergency Purchase Programme (PEPP) ending as planned in March 2022 and the APP running to the end of 2022, before the first rise in interest rates in the fourth quarter of 2023.

This decision to adjust bond purchases was aimed at the recent rise in sovereign yields and to prevent an “unwarranted tightening in financial conditions”. However, yields are not the only variables taken into account when determining the tightness of financial conditions. A working paper by ECB authors last year outlines some other major factors. In the simplified model, long-term yields carry the largest weight, but other variables are influential. More recently, Chief Economist Philip Lane and President Christine Lagarde have elaborated further, noting a focus on broad market conditions (yields and overnight index swaps) and bank-based lending.

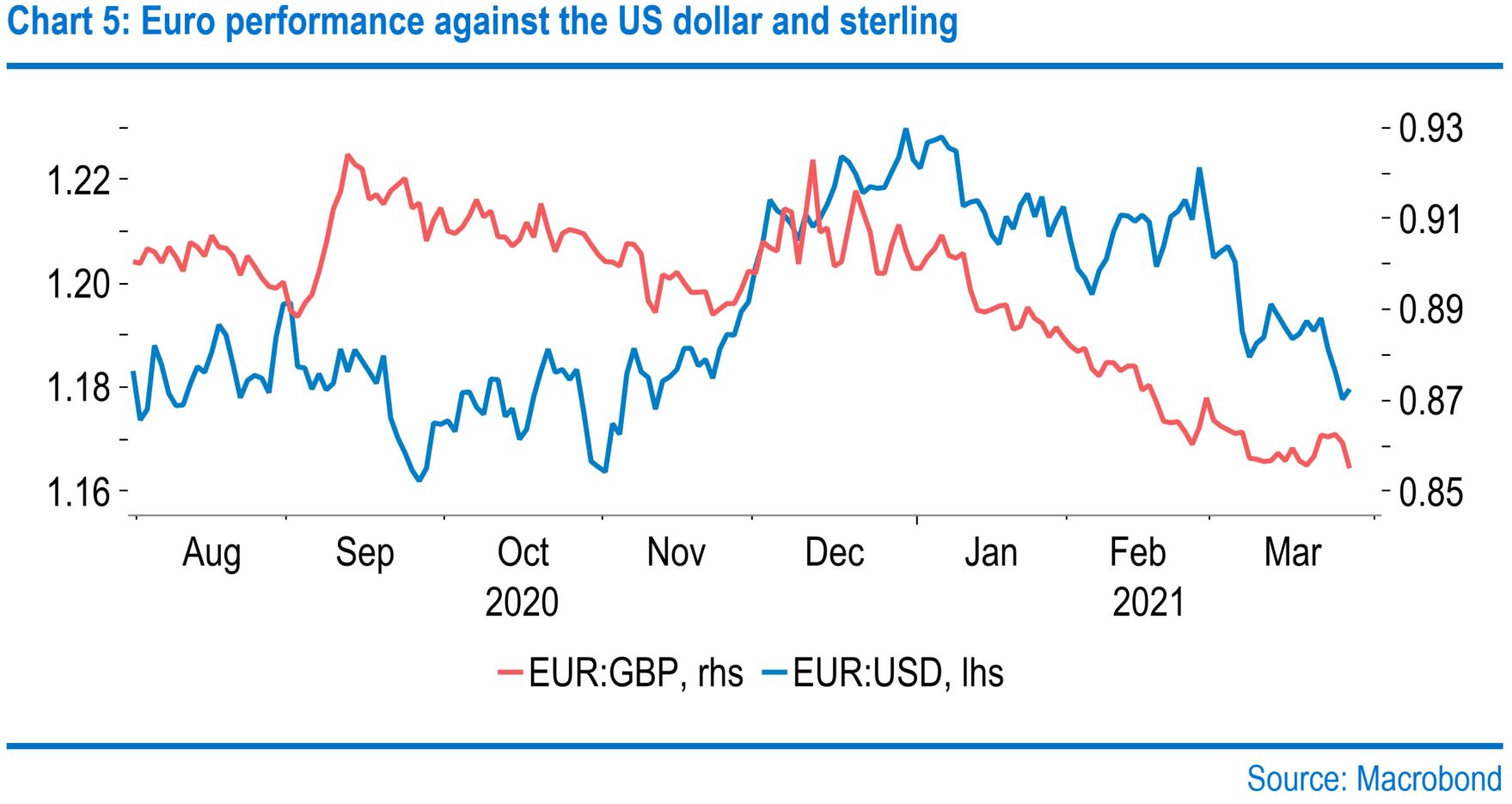

Over the last month, the euro has fallen foul of a stronger US dollar, dropping 3.2% to $1.177 since 23 February. But against sterling it has been more stable, falling just 1.4%. Given the more negative Covid-19 developments in the euro area, and the ECB announcing a front-loading of asset purchases, it is somewhat surprising that the euro has not weakened more significantly against the pound, particularly amid the more positive news from the UK. That said, we have made some marginal near-term revisions to our euro-pound forecasts, but this is a consequence of slightly stronger estimates for cable. In contrast, our euro-dollar forecasts remain unchanged at $1.25 end-2021 and $1.30 end-2022.

United Kingdom

There have been mounting signs in the monthly indicators that the UK economy has withstood its lockdown in the first quarter better than anticipated. We now estimate a quarterly drop in GDP of just 1.8%, a tenth of the plunge in the second quarter of 2020. The roadmap to gradually reopening the economy should bring about a sharp rebound in output in the second quarter if all goes to plan. Still, the scope for recovery is less than if the drop in the first quarter had been more significant. So, we have lowered our second-quarter GDP growth forecast. At this point, we see no need to revise our estimates for the level of output from the third quarter of 2020 onwards. Mathematically, this lifts our 2021 annual growth forecast to 7.3% but cuts our 2022 forecast to 5.6%.

The UK’s trading relationship with the European Union following the end of the transition period has got off to a shaky start, with January’s imports and exports of goods plummeting by 28.8% and 40.7% on the month, respectively. Although stockpiling ahead of the deadline is a significant contributing factor, our rough estimates suggest that it can only fully explain the decline in imports – exports to the EU would still be some 34% lower even without stockpiling effects. That indicates other factors, such as new regulations, are also limiting trade. Indeed, a survey by the British Chambers of Commerce in February confirmed that 49% of UK-based exporters had reported difficulties in adapting to new protocols since the start of the year.

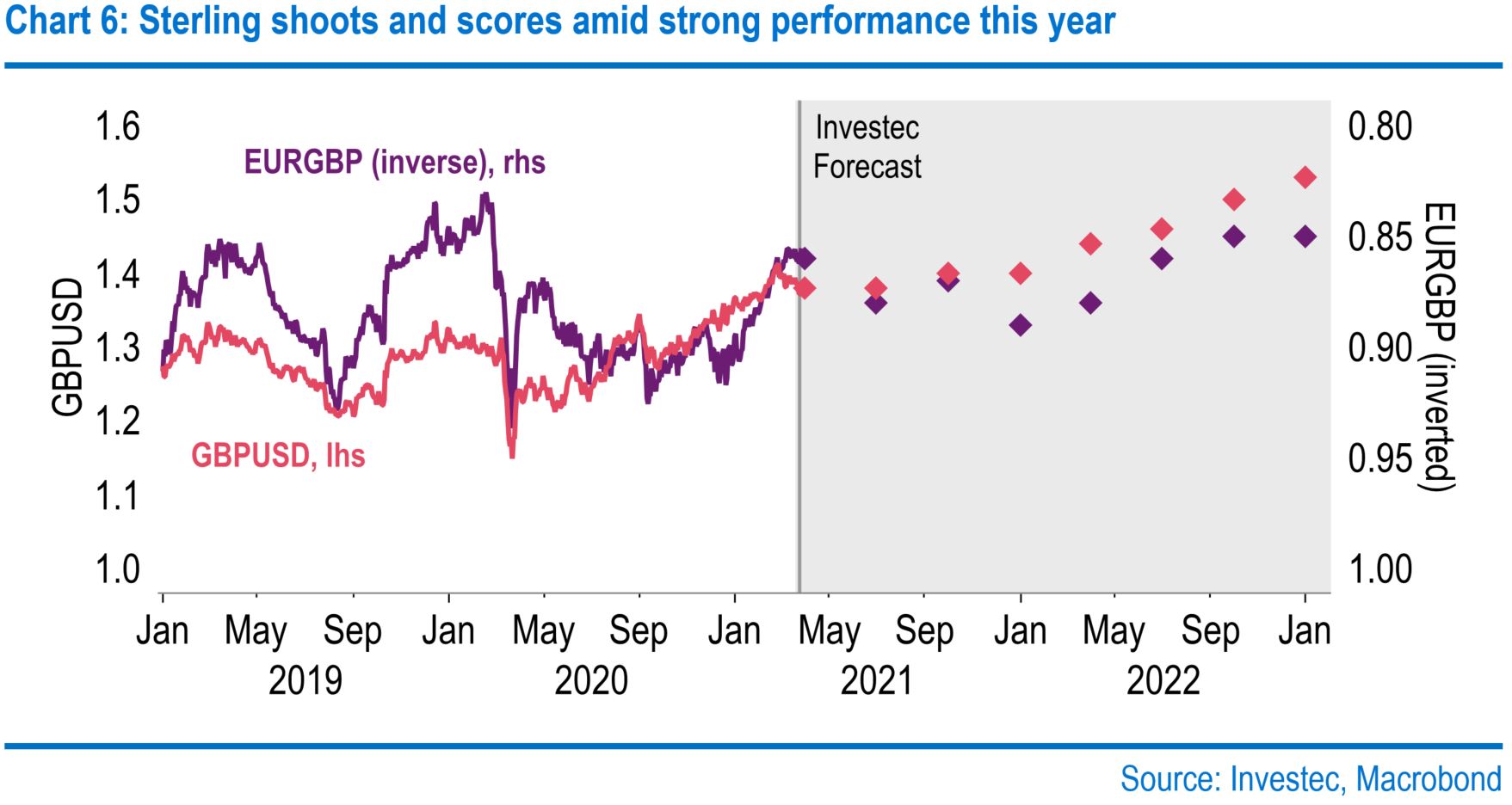

Despite the imposition of a third national lockdown, sterling has had a solid start to the year, reacting positively to the vaccine rollout and the sense of economic optimism, with the Bank of England’s narrow trade-weighted sterling index strengthening by over 3% since the start of the year. The pound has made significant gains against the euro, reflecting the contrast between positive domestic news and the third Covid-19 wave in continental Europe. Looking ahead, as the economy bounces back, we anticipate the pound to continue to thrive this year, with cable ending the year at $1.40. Euro-pound is expected to rise slightly. However, this is more of a euro recovery story.

UK labour force data are derived from a household survey - results are scaled up based on population projections. With unexpected large population swings, this can lead to odd results. Currently, official data show a jump of over 1 million in the UK-born working-age population between the fourth quarter of 2019 and the fourth quarter of 2020. However, suppose one assumes that the number of UK-born people to have been steady. In that case, the data imply tentatively but more plausibly a large net migration out of the UK and a fall in the total working-age population to the tune of 2.8%. It is not clear how many migrants would return in a post-pandemic recovery, particularly from the EU. If so, the pre-pandemic level of GDP may not be a good yardstick to gauge spare capacity.

Another impact of the pandemic has been to significantly alter the composition of the goods and services bought by consumers. Social restrictions have limited the availability of certain services, such as hotel accommodation, and boosted demand for some goods, such as computer games. The Office for National Statistics has taken steps to reflect this changed basket in its Consumer Price Index figures, which has considerably altered the weights used to calculate inflation in 2021. Had this year’s weights been applied last year, we estimate that inflation would, on average, have been 0.1 percentage point lower last year than reported.

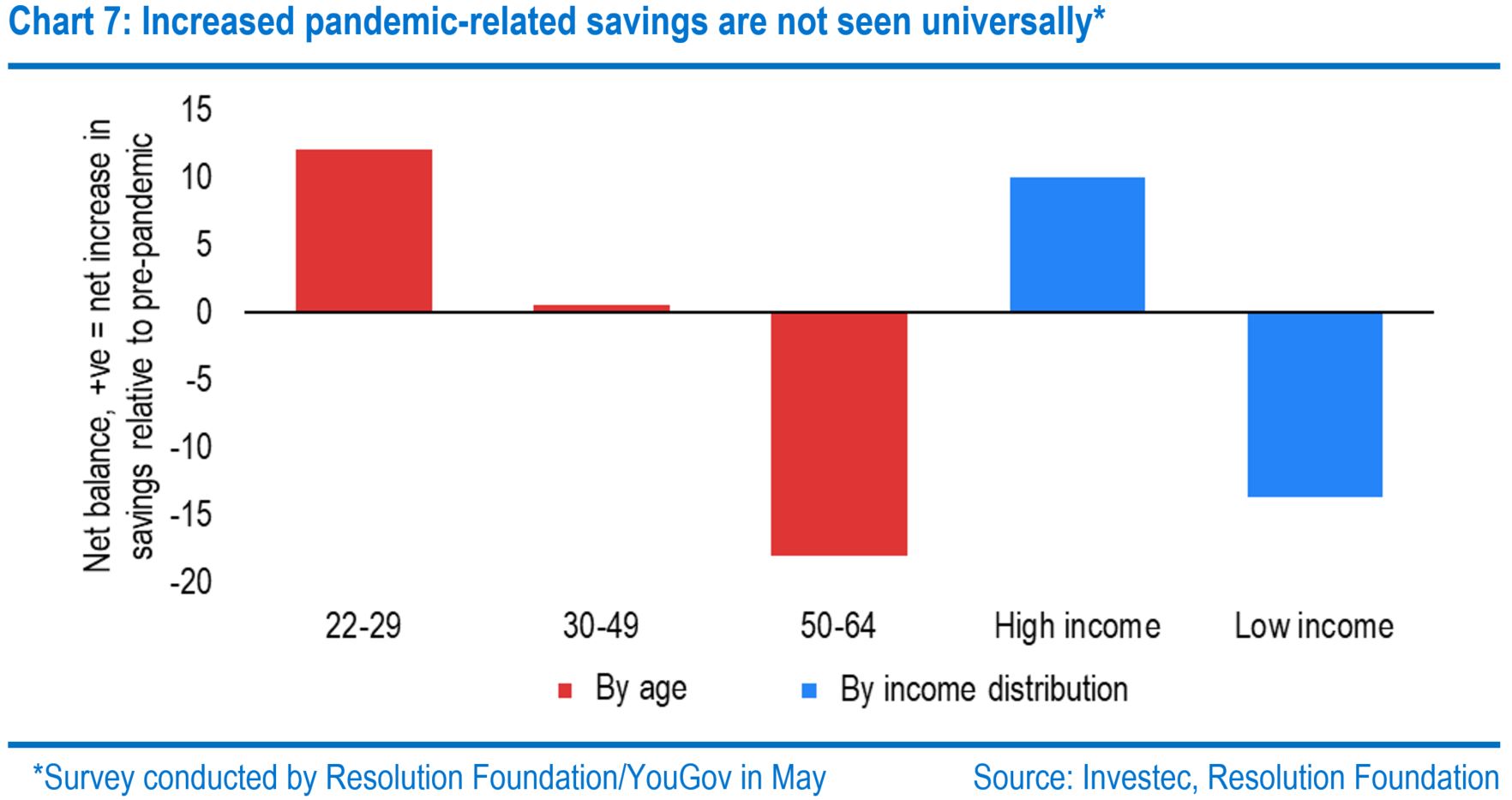

According to our estimates, in January, UK consumers had amassed £108 billion in excess savings since the start of the pandemic. However, this improvement in personal finances has not been seen universally across society, causing concerns regarding widening inequality. Indeed, lower-income groups, who are more likely to be employed in industries hit hardest by the pandemic, have decreased savings. More surprising is the age breakdown, with younger cohorts, who typically have a more significant marginal propensity to consume, building up a stock of savings. In contrast, the 50-64 age group have reported a net decrease in savings.

Would you like to hear from our economists directly?

Sign up to receive invites to our monthly economic Q&A with a member of our team.

Browse articles in

Please note: the content on this page is provided for information purposes only and should not be construed as an offer, or a solicitation of an offer, to buy or sell financial instruments. This content does not constitute a personal recommendation and is not investment advice.