17 Jan 2024

Private equity anticipates slower fundraising and more conservative valuations

- The majority (58%) of private equity fund managers (GPs) anticipate a decline in deal valuations in 2024.

- Nearly half (47%) expect fund returns to be lower over the next two years.

- 58% of GPs expect their next fund to take more than three months longer to close than their previous ones, and 27% anticipate it to take at least six months longer.

- Two-thirds of GPs are seeing more broken processes, compared with 41% in 2022

- Opportunities remain in a dislocated market, with a reversal in interest rates an upside kicker.

Private equity professionals are anticipating slower fundraising and more conservative deal valuations and returns in 2024, new research by Investec shows.

Investec’s latest annual Private Equity Trends 2024 Report – launched today – reveals that the industry is bracing itself for a challenging year as the impact of higher interest rates, tighter liquidity and slower deal markets continues to be felt. However, the report also identifies opportunities within the dislocated market, noting that the improving outlook for interest rates could turn sentiment quickly.

Valuations and returns

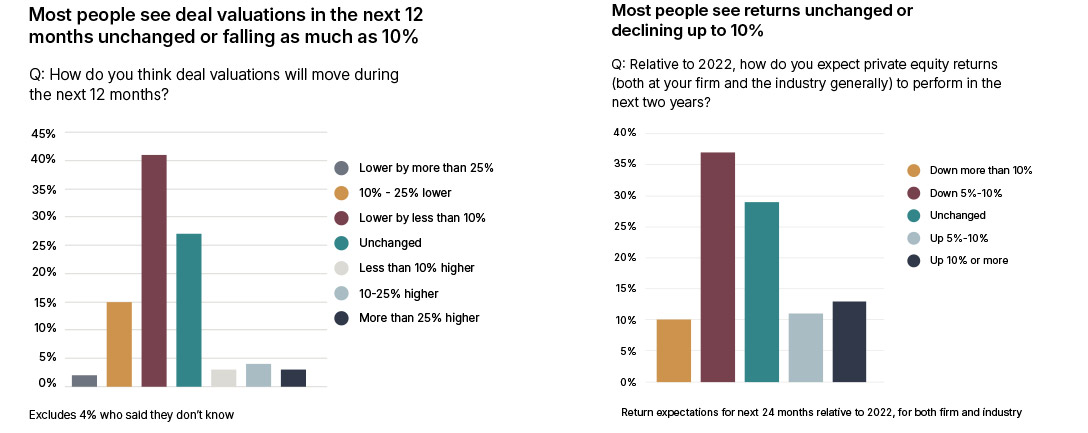

Almost two-thirds (58%) of private equity general partners (GPs) anticipate a decline in deal valuations in 2024, according to the Investec study, which polled around 150 leading GPs across the UK, Europe and the US. Approximately 17% expect a substantial decrease of more than 10%.

This conservative attitude towards deal valuations is reflected in expectations around returns. The survey indicates that nearly half (47%) of respondents foresee a decline in returns over the next two years, while only 24% expect to see an improvement.

The survey shows a divergence in return expectations between large and mid-sized funds versus smaller ones (AUM <$1bn). Managers of smaller funds are the most pessimistic, with just 12% expecting returns to rise compared to 56% expecting a fall. The greater optimism among managers with bigger funds reflects the longer-term trend for investors to allocate more capital to larger private equity platforms.

Positively, despite anticipation of reduced returns, 92% of respondents still expect to see their current funds clear the minimum return hurdle rates to make carried interest payments.

Exits and fundraising

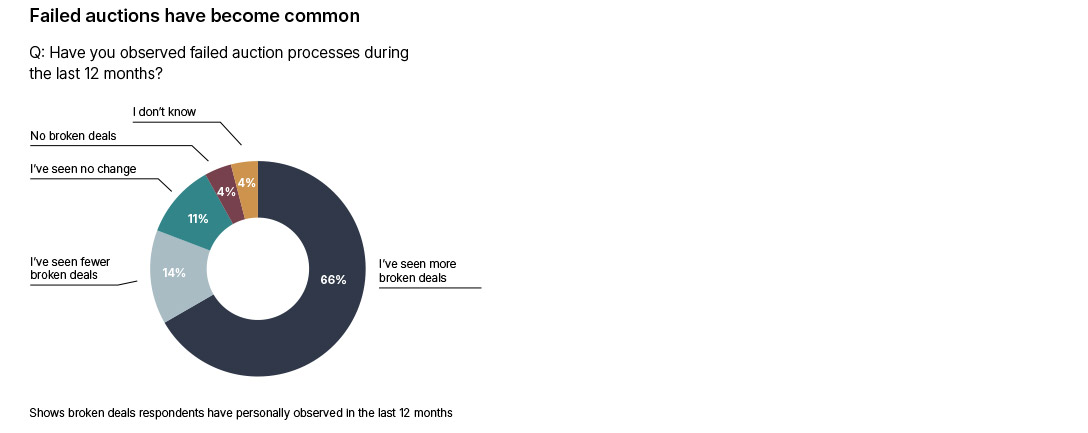

The challenging deal landscape has resulted in an increase in failed auctions. Two-thirds (66%) of GPs have experienced more broken processes over the past 12 months, compared with 41% in 2022. This has added another layer of complexity to exit strategies and fundraising efforts, impacting GPs’ track records.

As liquidity has shrunk, fundraising timelines have been extended. More than half (58%) of GPs expect their next fund to take more than three months longer to close than their previous one, with 27% anticipating it to take at least six months longer.

While almost half (46%) of GPs in 2022 anticipated their next fund to be 25%-50% larger, optimism has waned. Only one-fifth (19%) expect the same level of growth in 2024. Additionally, 19% of respondents now expect their next fund to be smaller, a notable increase from the 2% reported just a year prior.

ESG

Despite the challenging conditions, Environmental, Social, and Governance (ESG) considerations remain a priority and are starting to impact company valuations.

Sixty percent of GPs believe that implementing ESG best practices adds value to a portfolio company, and 18% believe it creates a valuation uplift of more than 10%. ESG or ethical factors significantly influenced the decision to invest or not invest in a portfolio company for 83% of GPs in the past year, with 48% noting an increased impact over the period.

Kate Gribbon, Head of Financial Sponsor Coverage at Investec, said:

“Our research shows that GPs are under no illusions about the challenges that lie ahead. But while the industry understands the need for pragmatism, the private equity model remains as relevant as ever. The market may not match the extraordinary deal volumes and fundraising observed at the top of the cycle in 2021, but transactions are still being done and GPs are successfully closing fundraises.

“As at any time of dislocation, quality is shining through. When high-quality assets come to market, competition among bidders is as fierce as ever. Meanwhile, limited partners (LPs) continue to support the most trusted fund managers, as seen by a series of record fund closes in 2023. This may be a tough time to be a GP, but opportunities continue to present themselves. As the macroeconomic picture becomes clearer and hope grows for rate cuts, we believe sentiment could improve quickly.”

Investec’s Private Equity Trends Report, formerly known as GP Trends, has been running for more than 12 years, taking the temperature of the market. This year’s report examines the latest trends in fund finance, M&A and leveraged finance as well as progress on ESG and diversity.

The 2024 report also reveals that the private equity industry has taken a more conservative approach to debt since interest rates began rising, shifting towards lower-risk bank loans and seeing leverage multiples come down.

Senior bank debt/term loan A finance was the most-used financing option over the last twelve months for more than half (54%) of respondents. The appeal of this type of financing comes from the ability of banks to provide fewer turns of leverage at lower margins, helping GPs manage costs at a time when the overall cost of capital is rising.

GPs have also been reducing the level of debt they use in their financial strategies. Three-quarters of managers (73%) say their leverage multiples for new deals has come down compared with 12 months ago, with 45% reporting a decrease of at least 1x EBITDA.

This could be the result of private equity taking a more prudent approach to debt, a reflection of the availability of higher-risk debt or a combination of the two.

Over the past 12 months, more than half (56%) of GPs have noted a reduction in the number of active lenders, while almost all (87%) reported experiencing more covenants or tighter terms on financing.

For more information

Please visit our Media hub for our team's contact details.