1 Apr 2025

PE Trends 2025

Helen Lucas | UK

Jonathan Harvey | UK

Our 14th report comes at a crucial time for the industry, as GPs get back to the business of selling portfolio companies and raising new funds.

2024 was a tough year for private equity and the overriding view from our survey of 253 general partners (GPs)* is that 2025 will be different.

Our findings show an industry which, despite challenges over the past few years, is resilient, adaptable, and anticipating a more favourable period ahead.

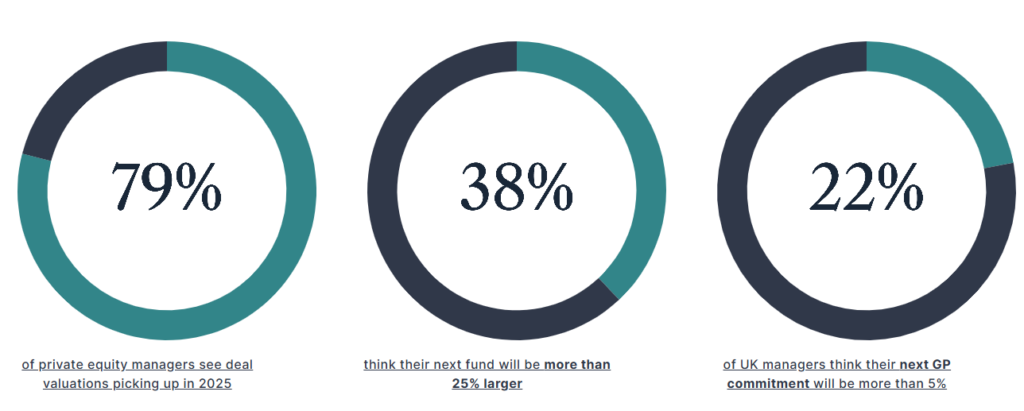

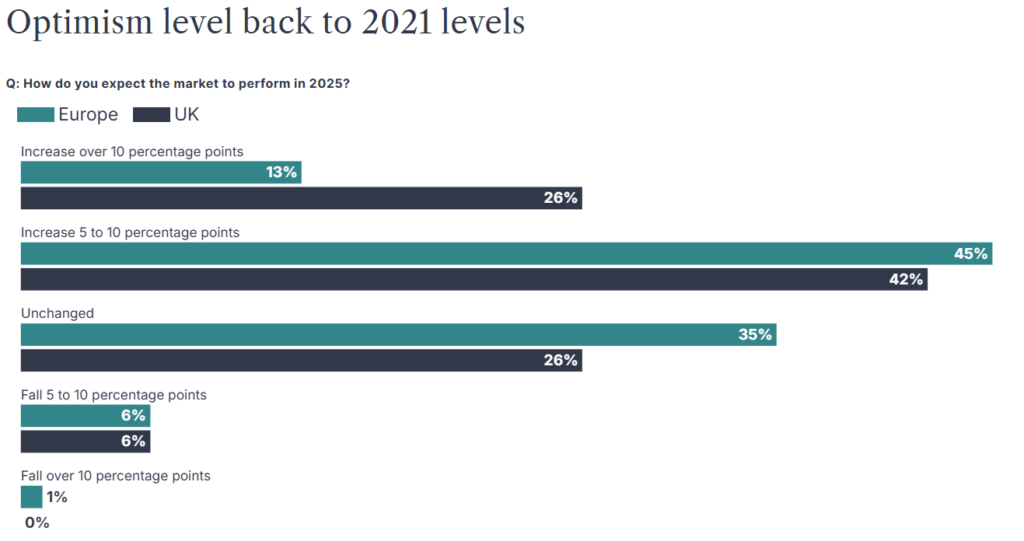

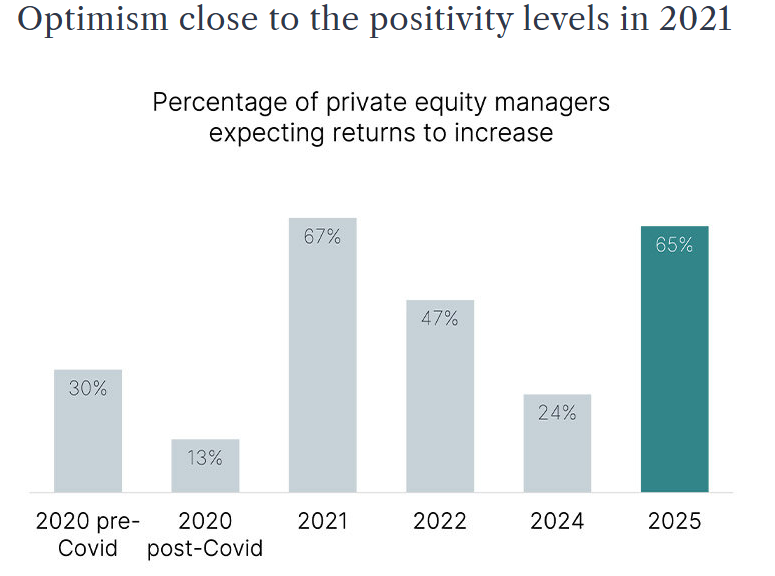

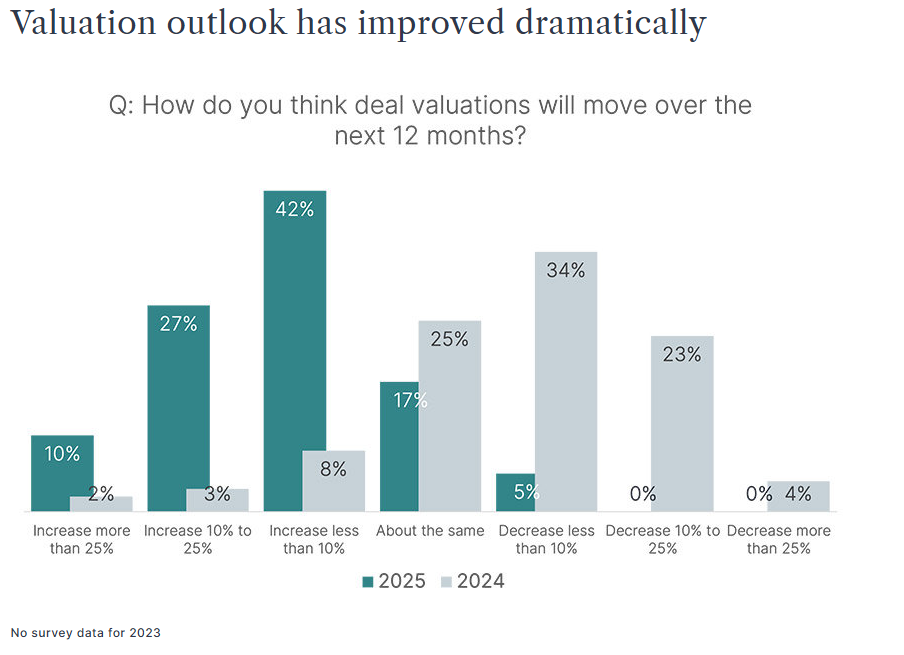

Four in five GPs expect deal valuations to increase in 2025 as interest rates come down, helping to clear exit bottlenecks and accelerate investors’ distributions. The outlook for returns is also brighter, with improvements registered across geographies and fund sizes. Close to two thirds (65%) of investors see returns improving in 2025, up from only 24% in 2024.

Dealmakers still must navigate ongoing geopolitical and macroeconomic risk, as trade tariff tit-for-tats continue and conflicts in the Middle East and Ukraine remain unresolved. It is a complex market, but the backdrop for M&A is better than it was a year ago.

Jump to a section:

Future fundraisings

GP commitments

New world of debt

Innovations and exits

GPs at a crossroads

Future fundraisings

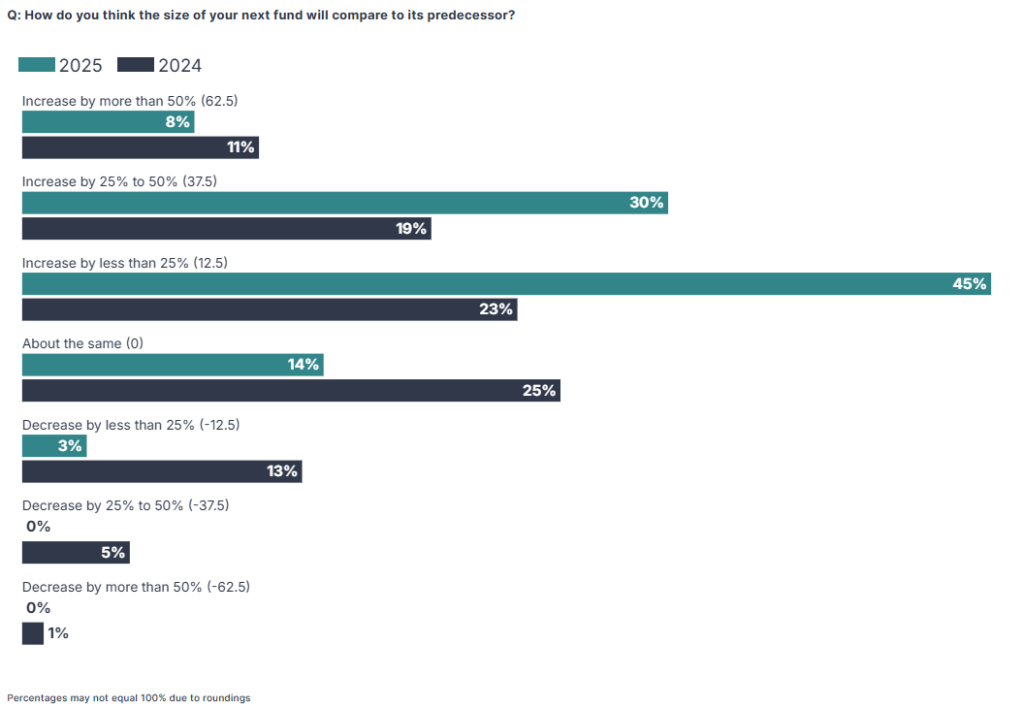

In 2024, 21% of respondents expected a down raise for their next fund: the 2025 research shows only 3% anticipating the same scenario.

There is also a large cohort of super-optimists – 38% expect their next raise will be a blockbuster increase of 25% or more over their previous fund.

Limited partners (LPs), however, are expected to remain highly selective in 2025. In 2024, according to PEI figures1, the ten largest funds to close in 2024 all secured more than $10 billion and absorbed more than a fifth of total fundraising allocations while a Coller Capital LP survey2 showed that the top focus for 98% of investors is that a new manager has a team with a strong track record.

Our survey findings tie in with this theme – close to a third of respondents (31%) expect an increasing number of GPs to move into wind-down. However, this does not mean the opportunity for new managers has passed; just 26% agreed that “very few new GPs will be launched”.

Although fundraising conditions are improving, LPs continue to consolidate GP relationships, focusing on managers of scale and mid-market specialists with differentiated investment strategies and exceptional returns.

Fundraising optimism surges

Jump to a section:

Deal valuations

GP commitments

New world of debt

Innovations and exits

GPs at a crossroads

GP commitments

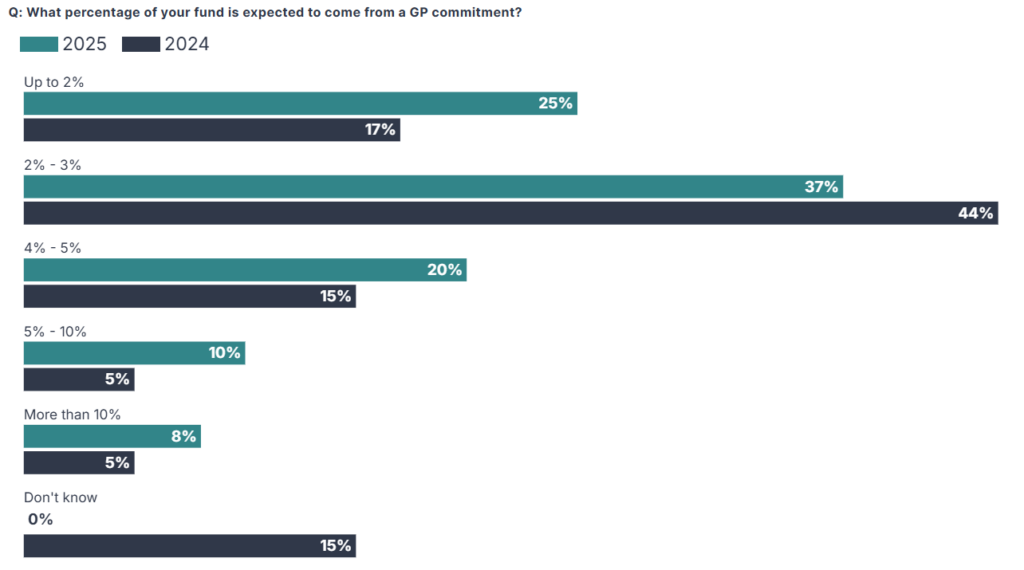

The survey shows GPs are planning to up their commitment from the typical 2% to 3% to strengthen alignment with investors and boost fundraising momentum.

- One in five GPs expect to commit 4-5% of their next fundraise.

- One in ten expect their next commitment to be 6-10%.

- 8% expect to commit more than 10% in 2025.

Managers are taking a blended approach to financing these higher commitments including existing resources, reinvesting carried interest and external debt, which is gaining favour. Most are using two options to fulfil their obligations, with 13% expecting to use three options.

Where are commitments highest?

The findings reveal interesting regional variations when it comes to GP commitments.

UK managers are more likely to be asked for a big commitment: 22% were asked for more than 5% versus just 8% of managers in Europe. Managers in France, meanwhile, seem to be asked for a particularly slim commitment, with more than half expecting to be asked for less than 2%.

Overall, a significant minority of investors expect to up commitments in the future.

Jump to a section:

Deal valuations

Future fundraisings

New world of debt

Innovations and exits

GPs at a crossroads

New world of debt

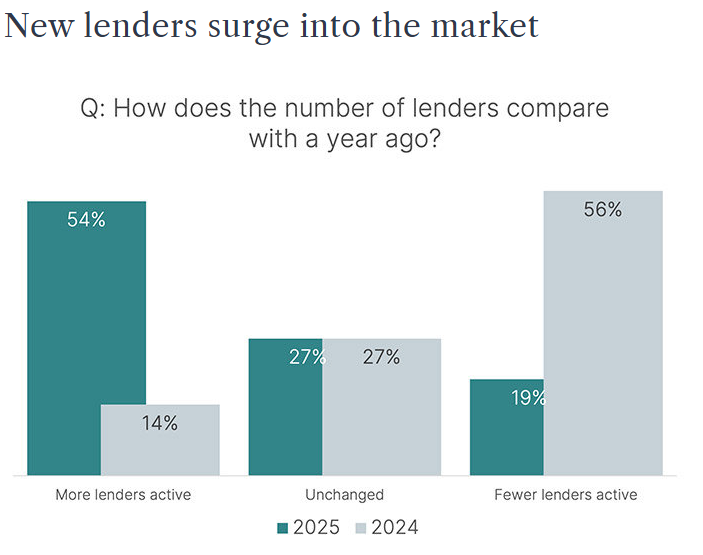

Debt markets are open for business with a substantial number of new lenders entering the market to provide GPs with enhanced financing optionality.

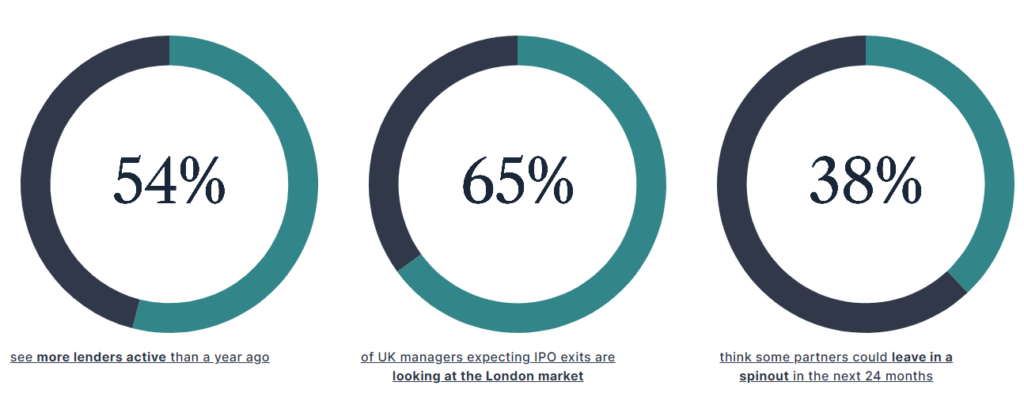

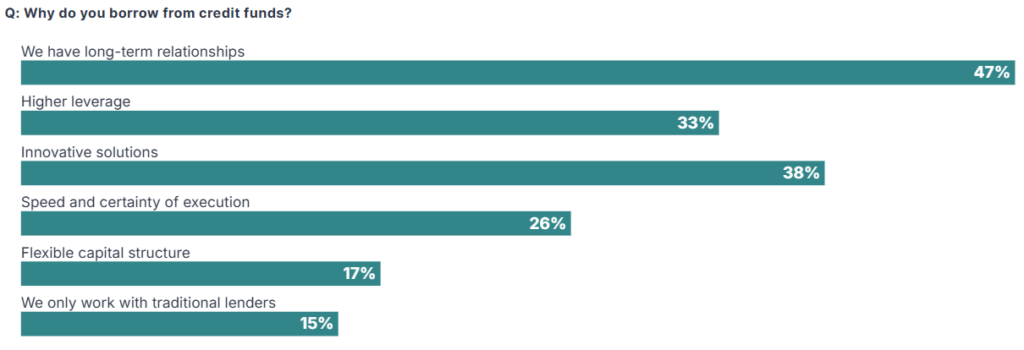

More than half (54%) of GPs say they will have new lenders to work with in 2024. This marks a shift from last year’s findings, when 56% of respondents saw a contraction in new lender activity. The majority of GPs who took part in our survey are working with credit funds and the top three reasons cited for working with a private credit included higher leverage levels and innovative financing solutions.

UK managers are hopeful that increasing competition will result in looser terms, with 54% of UK managers reporting either private debt narrowing margins or terms loosening generally. Outside of the UK, however, GPs are more cautious, with only 35% forecasting looser terms.

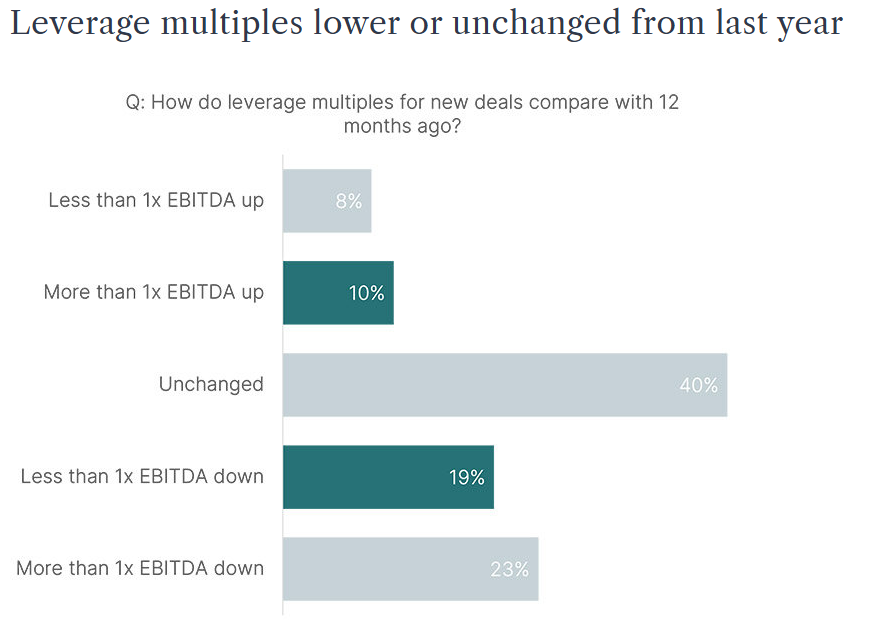

Despite these expectations, lenders are remaining disciplined. Well over a third of respondents (43%) report that leverage multiples have lowered from a year ago.

Competition is fierce for trophy assets in certain sectors, and these companies will be able to negotiate more favourable terms, but lenders will be highly selective.

Interest rates may have come down, but the risk-free rate remains elevated when compared with recent years, making additional leverage costly to service. Debt is available (European leveraged loan issuance climbed by more than 90% in 20243 and private debt managers have $126.4 billion of dry powder available to invest4), but the survey findings on leverage multiples show that capital structures remain relatively conservative.

Covenant flexibility

Even as interest rates have come down, GPs have still had to work hard to protect portfolio companies.

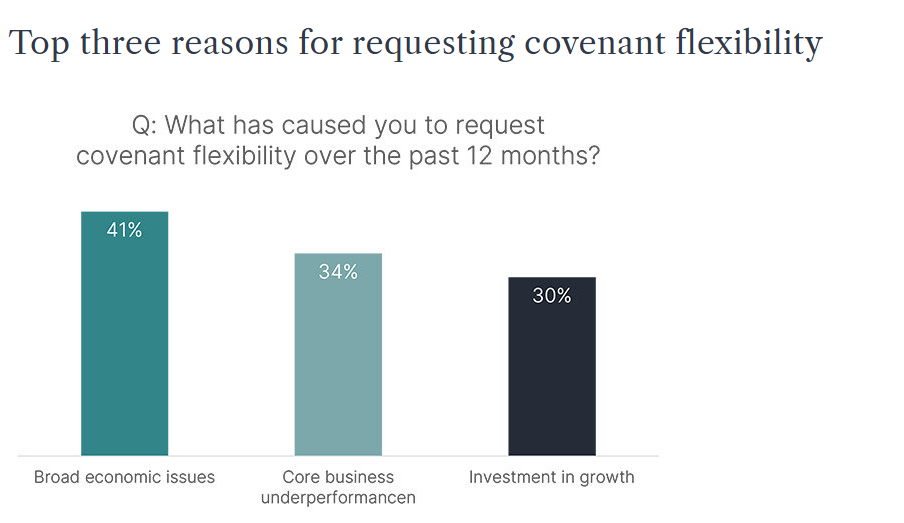

Some 87% of respondents say they have gone to lenders to request covenant flexibility for one or more portfolio companies. Broad economic issues (cited by 41%) and business underperformance (cited by 34%) are the main reasons for requesting flexibility.

Interestingly, close to a third of respondents (30%) have requested covenant flexibility to fund growth as GPs hold some portfolio companies for prolonged periods.

“We will always be open to a conversation about covenant flexibility. If a business is growing and wants to re-lever, or the sponsor wants to hold an asset for longer, loosening covenants can have a positive impact on supporting growth.” – Helen Lucas, Co-Head of UK Origination, Direct Lending, Investec

Lending landscape

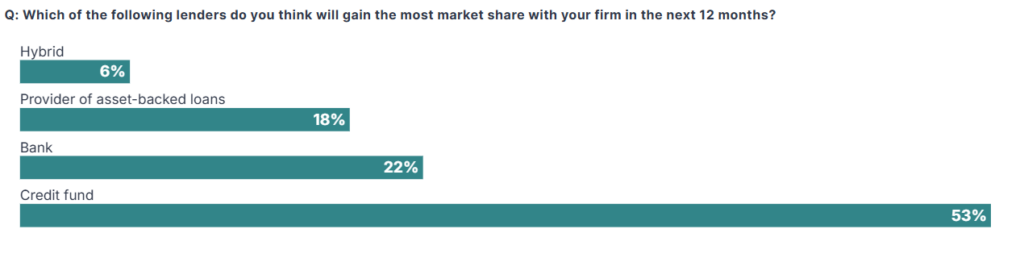

As more lenders entered the private equity space, there has also been increased use of some newer debt products. Innovation continues; survey respondents expect ESG-linked lending, fund-level finance and asset-based lending to increase market share.

Around half of the respondents expect credit funds to do more business with their firm during the year, but banks remain highly competitive; almost a quarter (22%) say they expect to place more lending with banks in the next 12 months. Hybrid capital is gaining particular traction for smaller managers with assets of $250m or less, with a quarter of these saying this type of lender will gain the most market share at their firm in the next year.

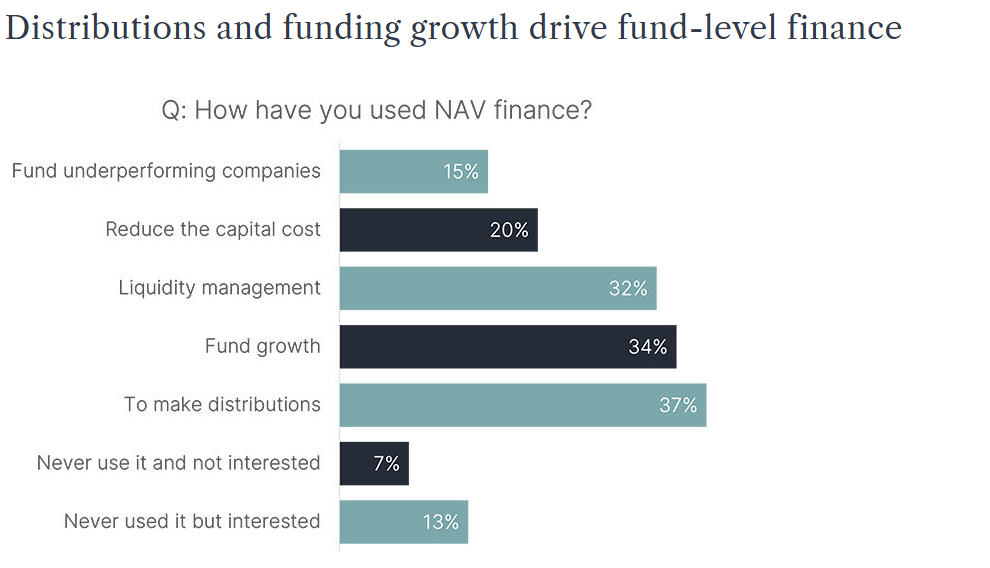

NAV lending

Net asset value (NAV) finance has proven particularly popular with managers in an environment where liquidity has been constrained.

Four in five GPs said they used NAV finance in the last year, with distributions the most-cited use case (37%).

Uptake of NAV finance looks set to continue accelerating, with two thirds (65%) of respondents who had not used NAV finance previously saying they were interested in taking up NAV loans.

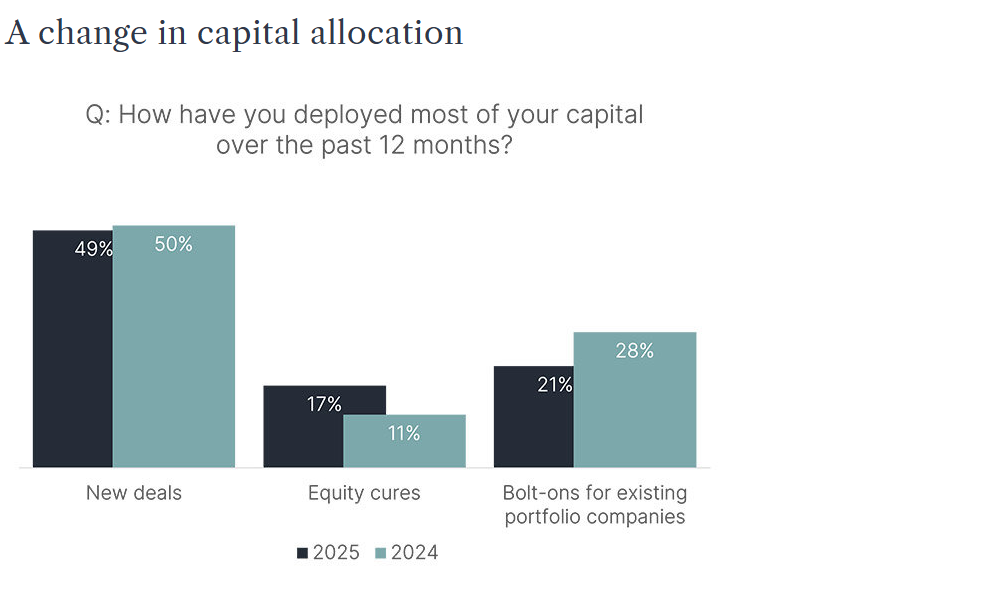

Deployment and operations

Less than half of GPs (49%) have deployed most of their capital in new deals during the past 12 months, with just over a fifth (21%) focusing efforts on smaller bolt-on acquisitions to support buy-and-build portfolios – down from 28% in our previous survey. An increase in the number of GPs deploying most of their capital in equity cures – up to 17% from 11% last year – further highlights the tough backdrop for managers during the past year.

The improving outlook means that the next 12 months should be more favourable for deployment. Somewhat surprisingly, the public-to-private outlook is mixed and not much changed from last year despite low stock market valuations, most notably in the UK5. Some 50% say they expect to look at more public-to-privates but 40% expect to look at less.

Big-ticket take-private deals during 20246 have ensured that P2P remains on the managers’ radars and may result in activity in this area.

“Private equity managers are ready to deploy, but it is taking much longer to originate deals. GPs will be forming relationships with management teams up to three years ahead of a formal process. During the last two years we have seen a number of processes fall over, and it does take time to rebuild before businesses come back to market.” – Kate Gribbon, Head of Financial Sponsor Coverage & Origination, Investec

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

Innovations and exits

GPs at a crossroads

Innovations and exits

One of the single biggest challenges for private equity managers through the rising interest-rate cycle has been to sell portfolio assets at valuations that deliver adequate returns.

In tepid IPO and M&A markets, GPs often opted to sit tight rather than offload assets at lower-than-hoped-for multiples. Hold periods remain above long-term averages, with the backlog of private equity-backed companies sitting at record levels7.

This has had repercussions on fundraising – slowing distributions to LPs have limited their ability to allocate to new funds.

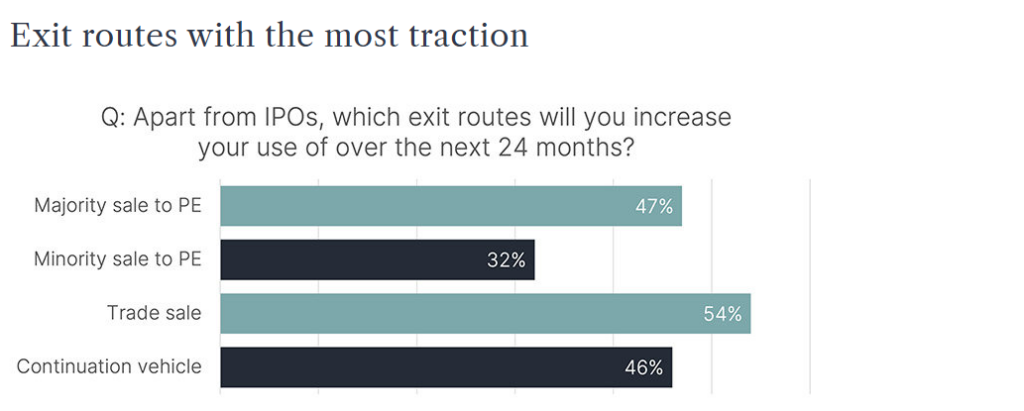

Managers looking at exits will explore all options to crystallise returns, with the survey findings ranking expectations for different exit routes in a narrow band.

More than half of GPs (54%) think trade sales will be the busiest exit route during the next 24 months. But after a long barren spell the IPO is back in the frame again, with the typical manager optimistic that two portfolio companies could be an IPO candidate over the next two years.

The squeeze on other exit routes meant there has been greater use of continuation vehicles which are here to stay as a mainstream exit path: more than 40% of GPs say a continuation fund will be an exit option they are more likely to use in the next 12 months.

The UK IPO question

Private equity-backed portfolio company IPOs haven’t always been crowd-pleasers, particularly on UK markets8, but the survey findings show managers warming to the UK stock market – albeit with some reservations.

Some 65% of UK managers who expect to list a portfolio company in the next two years consider the UK a potential venue – although they will also look at other venues such as Amsterdam or New York.

The size of the manager and portfolio is a factor in stock market selection. Larger managers with bigger assets to float think a UK IPO is less attractive, indicating that larger IPOs are considered more challenging for UK public markets.

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

New world of debt

GPs at a crossroads

GPs at a crossroads

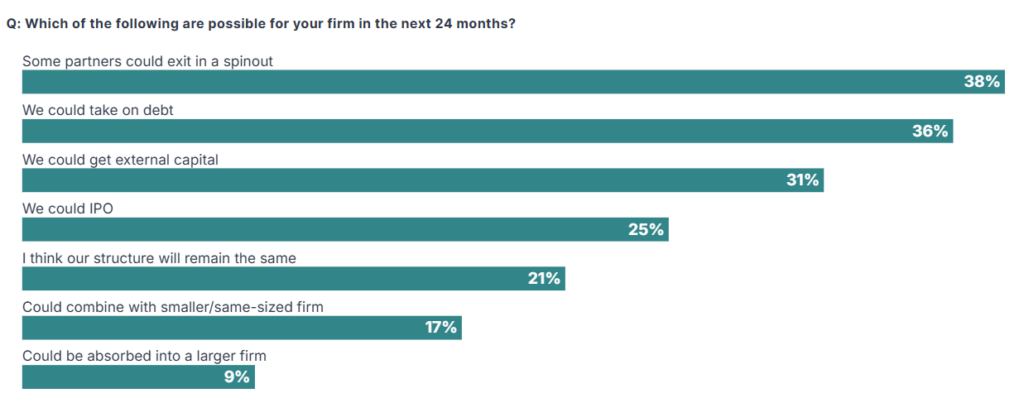

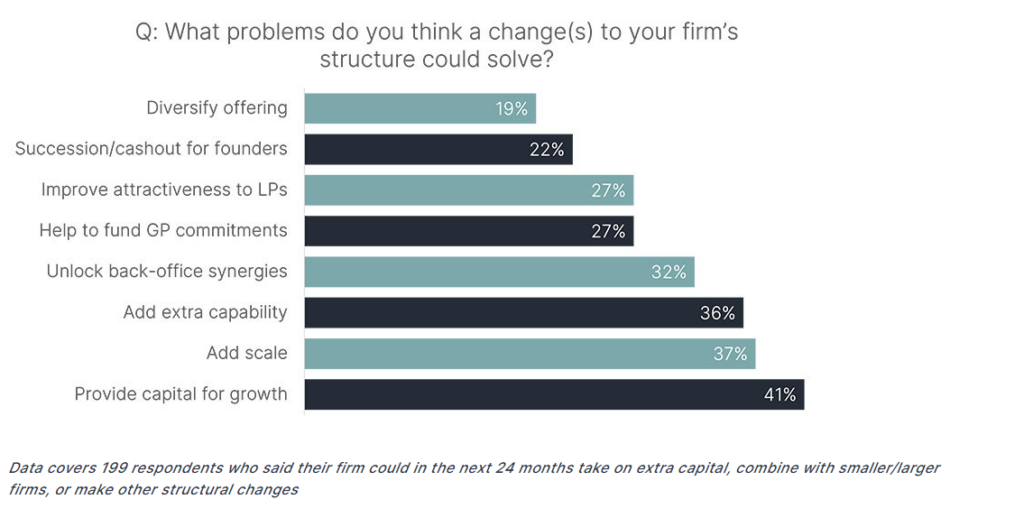

According to Pitchbook figures, GP-to-GP M&A reached record highs at the end of 20249 and the survey points to a long runway of further deals, with 79% of respondents expecting some kind of change to their firm’s structure.

In addition to GP consolidation deals, new teams are forming in spinouts and minority stake investment is proliferating.

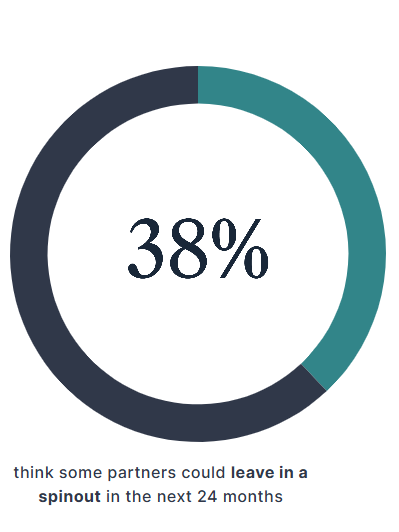

Indeed, 38% of GPs say some partners could leave their firm via a spinout in the next 24 months. This is reflective of a tougher fundraising environment, particularly for smaller managers with assets under management (AUM) below $1bn, where spinouts are more likely as junior partners explore other options when fundraisings stall.

Getting ready to capture growth

Historically, the main driver for taking on third-party capital or merging with another firm was likely to unlock liquidity and facilitate succession. While this reason was selected by 22% of respondents, the majority see a transaction as a tool to provide capital for growth or expand service lines and scale.

Ideally, twice as many managers say they would like to be the acquirer rather than target in a consolidation scenario.

What is also worth noting is that when it came to continuation vehicles, our survey showed that 40% of GPs think there will be more single-asset continuation vehicles over the next 24 months and over 25% thought they are likely to become more specialised. Single-asset continuation vehicles allow GPs to remain invested in a prized portfolio company and could potentially lead to a spin-out by a manager.

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

New world of debt

Innovations and exits

* Demographic info

This report is based on 253 responses to an online survey conducted between 7 January and 22 January 2025. Respondents were sourced from a prequalified panel and no PE firm was represented more than once.

178 were based in the UK, 75 in Europe including 22 in Germany, 14 in Spain and 11 in France. Some 34% of respondents were investment directors, other eligible job titles were CFO, VP of finance, director of finance, principal and manager of finance/investments.

Footnotes:

2 https://www.collercapital.com/41-barometer-winter-2024/

4 https://www.muzinich.com/opinions/corporate-credit-outlook-2025-private-markets

6 https://www.ft.com/content/ec9aa2ae-f56a-4373-8c4b-88effc01a25d

7 https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report

9 https://pitchbook.com/news/articles/blackrock-hps-purchase-record-year-gp-consolidation