L’évolution des comportements des consommateurs, l’innovation dans les différentes catégories de produits et le repositionnement stratégique ouvrent de nouvelles perspectives de croissance au marché européen des boissons.

Ces thèmes étaient au cœur de la conférence organisée par Investec et OC&C à Haarlem, aux Pays-Bas, où 40 dirigeants de grandes entreprises de boissons alcoolisées et non alcoolisées s’étaient réunis aux côtés d’investisseurs en capital-investissement détenant des participations dans ce secteur.

Organisé à la brasserie Jopenkerk, l’événement a permis de mettre en lumière des perspectives macroéconomiques, stratégiques et opérationnelles pour examiner où se crée de la valeur sur un marché de plus en plus concurrentiel.

Une demande résiliente, des comportements en mutation

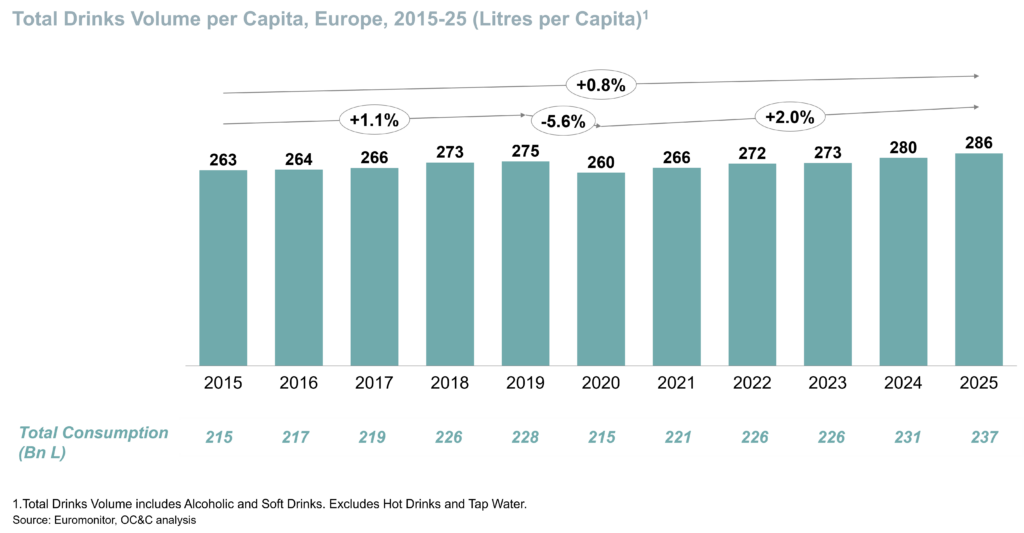

Alors que le contexte économique général reste mitigé, le secteur des boissons continue de faire preuve de résilience en tant que catégorie de consommation. Les habitudes d’achat régulières, la fréquence des occasions de consommation et la forte fidélité à la marque ont toujours soutenu la demande lors des périodes difficiles.

Philip Shaw a expliqué comment l’inflation, les coûts énergétiques et les incertitudes géopolitiques continuent d’influencer les budgets des ménages et la planification des entreprises. Malgré cela, la demande en boissons est restée relativement stable. Pour les acteurs de l’ensemble de la chaîne de valeur, la résilience à elle seule ne suffit plus. La flexibilité en matière de tarification, de gestion de portefeuille et de mise en œuvre des stratégies de commercialisation revêt une importance croissante.

La croissance devient de plus en plus sélective

Si la croissance globale des marchés européens a été modeste ces dernières années, les performances sous la surface affichent des écarts marqués.

Dan Zubaida a souligné que la dynamique la plus forte se concentre désormais sur des catégories en phase avec l’évolution des préférences des consommateurs :

boissons fonctionnelles,

hydratation,

alternatives à faible teneur en alcool ou sans alcool,

formats axés sur la commodité,

offres haut de gamme dotées d’une identité de marque claire.

Dans le même temps, les segments plus traditionnels sont confrontés à une croissance plus lente et à une concurrence plus intense. Il en résulte un marché plus polarisé, où un positionnement ciblé importe davantage qu’une large exposition à la catégorie.

Pour les équipes de direction comme pour les investisseurs, l’opportunité réside de plus en plus dans l’identification de poches spécifiques de croissance structurelle plutôt que dans l’espoir d’une reprise uniforme du marché.

La force de la marque reste le moteur de la surperformance

À mesure que l’innovation s’accélère et que l’espace en rayon devient de plus en plus disputé, la clarté de la marque s’impose comme un atout de plus en plus déterminant.

Les exemples évoqués lors de la conférence ont montré que les marques les plus performantes associent souvent une proposition claire adressée au consommateur à une exécution rigoureuse :

des qualités gustatives indéniables,

une pertinence en matière de bien-être,

un développement efficace de nouveaux produits,

un marketing convaincant,

une stratégie de distribution intelligente.

Dans les catégories où les barrières à l’entrée sont moins élevées et où les marques challengers peuvent se développer rapidement, le succès durable ne repose pas simplement sur le lancement de nouveaux produits. Développer des marques susceptibles de générer des achats répétés présentent un intérêt pour les détaillants.

La modération crée de nouvelles occasions de consommation

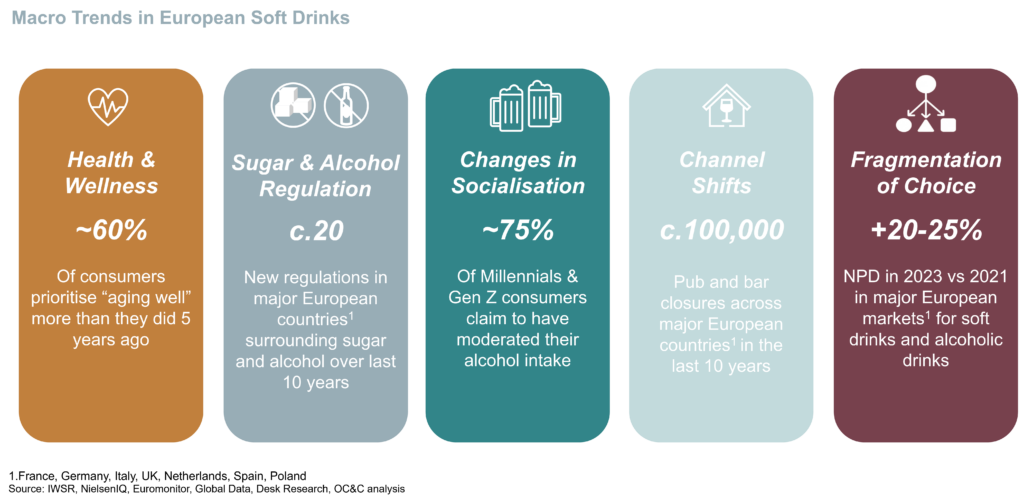

L’un des débats les plus animés a porté sur l’évolution des habitudes de consommation d’alcool, en particulier chez les jeunes consommateurs.

Les tendances à la modération redéfinissent les schémas, de nombreux consommateurs recherchant l’équilibre plutôt que l’abstinence. Cela favorise la croissance des bières sans alcool, des boissons non alcoolisées destinées aux adultes, ainsi que des boissons et des produits conçus pour des occasions sociales sans alcool.

Plutôt que de représenter une simple tendance de substitution, les catégories sans alcool et à faible teneur en alcool pourraient également élargir l’ensemble des occasions de consommation en créant de nouveaux cas d’utilisation dans des contextes sociaux en semaine, axés sur le bien-être et impliquant des groupes mixtes.

Que ce soit pour les acteurs du secteur des boissons alcoolisées ou des boissons non alcoolisées, la frontière de plus en plus floue entre les catégories ouvre de nouvelles perspectives stratégiques.

Tendances en matière de santé et effet du GLP-1

L’impact des médicaments à base de GLP-1, notamment ceux utilisés pour la perte de poids, sur le marché des boissons a également fait l’objet de vifs débats.

Les participants ont noté qu’à court terme, les entreprises du secteur des boissons répondent à la demande en s’orientant vers des catégories « complémentaires » adjacentes, telles que:

les produits riches en protéines,

l’hydratation,

les offres à teneur réduite en sucre

les boissons bien-être,

qui sont en phase avec l’évolution des priorités et des préférences des consommateurs en matière de santé.

Les participants ont débattu de la question de savoir si l’innovation de la forme d’administration du GLP-1 sous forme de boissons pourrait, à terme, créer de nouvelles opportunités de croissance connexes. Bien qu’il s’agisse encore d’un thème émergent et soumis à des évolutions réglementaires et commerciales, la discussion a mis en évidence la manière dont les tendances externes en matière de santé peuvent influencer la stratégie de portefeuille à long terme et l’innovation produit dans l’ensemble du secteur.

La taille, les fusions-acquisitions et l’expansion géographique restent des leviers clés

Un sondage réalisé auprès du public pendant la conférence a révélé les priorités qui déterminent actuellement les agendas des conseils d’administration. L’innovation produit a été identifiée comme le levier de croissance le plus crucial par 39 % des participants, suivie par l’expansion géographique (32 %) et les fusions-acquisitions (25 %).

Ces réponses reflètent un marché où de nombreuses entreprises cherchent à équilibrer leurs initiatives de croissance organique avec des opportunités de croissance inorganique ciblées. Les acquisitions peuvent accélérer l’entrée sur des niches à croissance rapide, tandis que l’expansion internationale offre l’accès à de nouveaux bassins de consommateurs au-delà des marchés nationaux.

Le marché européen des boissons restant fragmenté en de nombreux sous-segments, la consolidation devrait rester un thème important.

La mise en œuvre continue de faire la différence entre les leaders et les autres

S’appuyant sur l’expérience d’A.G. Barr, Euan Sutherland a expliqué en quoi la croissance dépend en fin de compte d’une mise en œuvre cohérente des priorités commerciales, opérationnelles et d’innovation.

Cela implique d’investir dans les marques phares, de se développer dans des catégories connexes, d’améliorer la pénétration des canaux de distribution et de maintenir la capacité de la chaîne d’approvisionnement nécessaire pour soutenir la croissance. Sur un marché où les préférences des consommateurs peuvent évoluer rapidement, la rapidité et la capacité d’adaptation sont des atouts de plus en plus précieux. La stratégie définit la direction à suivre, mais c’est l’exécution qui crée de la valeur.

Perspectives

Le marché européen des boissons reste attractif, mais la croissance devient plus sélective. Les entreprises capables d’adapter leur portefeuille aux besoins changeants des consommateurs, de développer des marques distinctives et d’investir leur capital avec rigueur devraient afficher des performances supérieures à la moyenne.

Pour les investisseurs et les entreprises, la prochaine vague de création de valeur pourrait provenir moins de la seule croissance du marché que du soutien apporté aux catégories, aux compétences et aux marques les mieux placées pour répondre à l’évolution de la demande.

Galerie photos de l’événement

Nous sommes ravis d’accueillir Jens Rutten en tant qu’associé au sein de notre bureau de Zurich.

Jens nous rejoint après avoir travaillé chez Oaklins, où il a acquis une expertise approfondie en matière de successions et de cessions d’entreprises, principalement dans le cadre d’opérations transfrontalières.

Il possède un parcours exceptionnel dans les secteurs de l’industrie, de l’agroalimentaire et des biens de consommation.

Sa nomination confirme la volonté d’Investec de renforcer son équipe dédiée aux entreprises de taille intermédiaire en Suisse, en alliant une présence locale à notre plateforme mondiale comptant plus de 300 professionnels spécialisés dans les fusions-acquisitions à travers le monde.

Retrouvez l’entretien de Michel Degryck, Managing Partner, dans le numéro de NextStep n°22 de juin 2025 consacré aux cessions d’entreprises détenues par des fonds d’investissement.

Les cessions des entreprises détenues par les fonds se font toujours au compte-goutte malgré la pression des investisseurs pour le retour de liquidité et l’allongement de la durée de détention firtant avec les sept années en moyenne. (…)

Extrait :

“”

La situation est très contrastée selon la taille des entreprises. Sur le large cap, les transactions sont gelées car les cibles sont plus exposées à l’international et aux incertitudes de l’environnement macro-économique, d’une part et à la raréfaction des acquéreurs potentiels à des valorisations conformes aux attentes des cédants, d’autres part.

Dans un marché des fusions-acquisitions de plus en plus exigeant, la question de la « préparation à la cession » (exit readiness) prend une importance croissante : stratégie, indicateurs clés, equity story, vendor due diligence – comment l’intégration précoce de la planification de la cession dans le développement stratégique de l’entreprise devient un facteur clé de succès.

Que peuvent réellement apprendre les dirigeants et propriétaires d’entreprise des rois du deal – les investisseurs en capital-investissement – en matière de préparation à la vente, afin de rendre les résultats de cession plus prévisibles et optimaux ?

Dans cet épisode de What’s up, Corporate Finance?, Thorsten Gladiator, Managing Partner chez Investec, et Sebastian Markowsky, Managing Director, échangent avec le journaliste économique Michael Hedtstück sur les enseignements que les entrepreneurs peuvent tirer des fonds de private equity en matière de préparation stratégique à la cession.

Les questions clés abordées :

Que peuvent réellement apprendre les entrepreneurs des « Kings of deals » – les investisseurs financiers – en matière de préparation à la cession ?

Existe-t-il un décalage manifeste entre la perspective à long terme adoptée par les fonds de private equity pour préparer leurs sorties et les horizons de planification M&A des dirigeants d’entreprise ?

Quels sujets doivent impérativement être clarifiés en amont d’un processus M&A, plutôt que d’être laissés à l’appréciation de l’acheteur potentiel ? Dans quelle mesure est-il essentiel de bien répéter l’equity story et la présentation du management ?

Quelle est la réalité pour les entreprises de taille intermédiaire ? Dans quelle mesure les dirigeants sont-ils prêts à s’inspirer des pratiques des fonds de private equity ?

Cliquez ici pour écouter le podcast :

What’s up, Corporate Finance? est un blog et un podcast du Finance Think Tank Network. Grâce à des analyses régulières et des décryptages approfondis sur des sujets liés au private equity, private & venture debt, corporate & investment banking, M&A, au financement et au restructuring, ils décryptent l’univers de la finance d’entreprise avec expertise et passion journalistique.

🎙 Écoutez le podcast, disponible sur toutes les plateformes d’écoute.

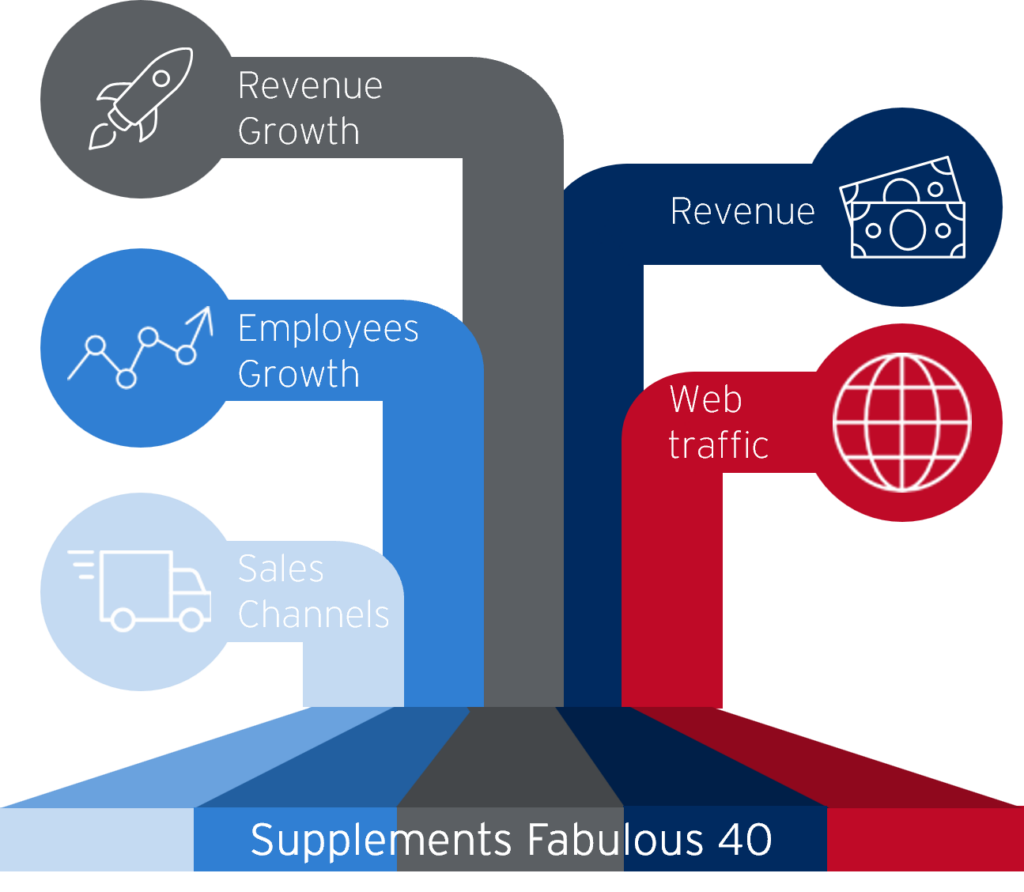

INCREASING HEALTH AWARENESS AND CHANGING LIFESTYLES HAVE LED TO A SURGE IN DEMAND FOR DIETARY SUPPLEMENTS. THIS DEMAND HAS FURTHER INCREASED DURING THE COVID-19 PANDEMIC, WITH A STRONG GROWTH FORECAST FOR THE MARKET VOLUME IN EUROPE IN THE NEXT TEN YEARS.

In recent years, notable transactions and innovations have characterized the supplement market in Germany. The number of start-ups in the sector has been at a high level, as they were able to quickly gain significant attention and market share through targeted marketing, for example through social media.

For Germany, we identified more than 400 relevant companies in the sector. From these, we have summarized what we consider to be the 40 most attractive in a ranking. To accomplish this task, a comprehensive review of all 400 companies was conducted, assessing them based on five key factors deemed relevant to our evaluation criteria: revenue, revenue growth, employee growth, web traffic, and diversity of distribution channels served. In all areas, a higher number correlated with a more favorable ranking.

In order to be included in our ranking, companies had to possess a unique characteristic that sets them apart from their peers. This could be anything from an extraordinary story or an emerging trend, to a unique market approach or growth pattern. Our Fabulous 40 list consists only of companies that have this unique quality. This means that even smaller companies have the potential to make it to the top of our Fab40 list. It is worth noting that all companies on our list are considered to be among the top 10% of companies in their sector.

Investec has acquired a strong expertise in the Healthcare sector by accompanying large groups, entrepreneurs, and mid-caps in their sales processes, acquisitions, and financings. Together with Investec as a significant majority shareholder, Investec has a global reaching network of M&A professionals.

Interview

As we enter 2024, the M&A landscape shows signs of recovery, albeit cautiously.

In the episode of the February 20, 2024 of No Ordinary Wednesday, Jeremy Maggs in conversation with Investec experts Jürgen Schwarz, Marleen Vermeer, and Kilian de Gourcuff, Investec’s Head of Cross-Border Finance and International Advisory Charles Barlow, on what key sectors, trends and risks to keep an eye on in 2024.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Extensive track record combined with deep industry knowledge

Interview with Jürgen Schwarz, Managing Partner of Investec about the role aggregators play in the e-commerce market:

How is the client’s situation?

How is the e-commerce market structured?

How can we operate the sales process?

Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

The dynamic and rapidly changing consumer goods sector is facing major challenges due to advancing digitalisation and the emergence of new disruptive business models. We drill down into sub-sectors that show strong growth potential and/or an increase in consolidation.

In the context of this fiercer competition and increasing consolidation activity, we support you in identifying and realising entrepreneurial opportunities.

The majority of our transactions are cross-border – within Europe and beyond – and are carried out by an international team of experienced advisors with extensive sector and transaction expertise.

Financial restructuring for Shareholders & Lenders

Helping clients to navigate uncertainties while putting their businesses back on track

Interview with Jürgen Schwarz, Managing Partner of Investec about Restructuring with the help of a M&A process:

How did the market change in recent years?

What is your approach?

Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

Sale from insolvency

Due to our pan-European presence and track record we are well placed to advise on international and cross-border restructurings.

Our international sector teams implement more than 50 transactions p.a. and in many sectors they know the active buyers, the acquisition criteria, the behaviour of individual decision makers. We also have an up-to-date overview of the market prices paid, which vary considerably over time and depending on the positioning in the sector.

Investec has direct access to numerous international equity and debt capital providers and has carried out numerous restructurings ranging from approximately 10 million Euros to several billion Euros.

Financing and Market trends | 2023

Why the German industry has a great need for investment.

German industry is facing significant challenges, including the effects of digitalization, the shift from analogue to digital business models, the need for environmental protection measures and sustainable production processes, as well as demographic change, which is leading to a shortage of skilled workers and an ageing workforce. In order to successfully master these processes, significantly higher investment efforts are required than in the past.

Digitalization and Industry 4.0: At present, Germany ranks at best in the middle of the EU in terms of the use of digital technologies in the economy1. German industry must invest in digital technologies and automation to remain competitive. However, in order to catch up with comparable countries, IT and digitalization investments in Germany would have to double or triple from EUR 49 billion to EUR 100 to 150 billion annually. In the SME sector alone, digitalization expenditure would have to increase from EUR 18 billion in 2019 to EUR 35 to 50 billion per year.

Sustainability and environmental protection: Companies are increasingly focusing on environmentally friendly technologies and processes in order to achieve sustainability goals and reduce their environmental impact. These investments not only serve to protect the environment, but also contribute to long-term competitiveness. A recent study commissioned by KfW puts the climate protection investments required to achieve the goal of climate neutrality by 2050 at around EUR 5 trillion or around EUR 190 billion per year1. This enormous sum makes it clear that considerably greater efforts will be required to achieve the target than has been the case to date.

Thorsten Gladiator, Managing Partner Investec: As corporate finance advisors, we see the importance of ESG in general and sustainability aspects in particular in almost every transaction, both in M&A situations and in financing mandates.

Equity and debt investors place a strong focus on ESG compliant investments in the interest of their financiers and / or due to investment criteria that are binding for them.

For business sellers as well as CFOs, this has pricing and process consequences:

A clearly defined and documented ESG strategy creates confidence among investors and the company’s other stakeholders

The same applies to the (early) implementation of legal requirements for sustainability reporting (CSRD)

A focus on sustainability aspects provides positive differentiation features compared to competitors and can thus have a value-creating effect

The lack of a corresponding strategy can lead to price discounts in the valuation as well as higher financing costs

In the due diligence phase of a transaction, lack of ESG information leads to prolonged processes, higher management burden and the withdrawal of investors with clearly defined ESG investment criteria

The following article from AIM – Advice in Motion highlights the various aspects for medium-sized companies and shows examples of successful ESG strategies.

Opportunities and challenges of sustainability for smaller and medium-sized enterprises

The sustainability performance of a company today is the decisive factor for its competitiveness tomorrow. In this context, medium-sized companies in Germany in particular are faced with tasks whose extent has not yet been fully recognized in many cases and which involve major challenges in terms of resources, time and expertise.

Even though sustainability is a ubiquitous and much-discussed topic that is omnipresent both in the media and in public debate, it is by no means a new issue. Rather, sustainability has a long and exciting history that spans centuries and has been shaped by various actors and concepts.

Where do the roots of sustainability lie?

As far back as the Middle Ages, the moral ideal of the honorable merchant played a decisive role in promoting sustainable principles. Many a family entrepreneur rightly sees himself or herself in the tradition of the honorable merchant and aligns his or her business conduct with principles such as honesty, responsibility and sustainability.

In the 18th century, the Saxon chief miner Carl von Carlowitz coined the term sustainability in his work « Sylvicultura Oeconomica. » He introduced the idea that forest resources should be managed sustainably by cutting only as much wood as can naturally grow back. What was interesting about Carlowitz’s concept of sustainability was that sustained yield was precisely not antithetical to sustainability. Rather, forestry yield acted as the cornerstone for this oft-cited source of the concept of sustainability. The mining area of the Erzgebirge was simply dependent on the sustainable use of wood for construction, mining and smelting purposes.

Another significant milestone in the development of sustainability was the Brundtland Report, published in 1987 under the title « Our Common Future ». The report defined sustainable development as « development that meets the needs of the present without compromising the ability of future generations to meet their own needs. » Here, sustainability clearly went beyond a purely economic consideration. The report emphasized the need to integrate economic, social and environmental aspects to create a sustainable future.

Since then, the understanding of sustainability has evolved to encompass a variety of dimensions. One key concept is ESG (environmental, social, governance) criteria, which encompass environmental, social and governance-related factors. Differentiation of individual sustainable development goals is achieved through the United Nations Sustainable Development Goals (SDGs), which were adopted in 2015. The SDGs include 17 global goals to promote sustainable development at the economic, social and environmental levels by 2030. These goals range from poverty reduction, health, education and gender equality to renewable energy and sustainable cities.

The SDGs are an excellent framework for linking the principle of sustainability with economic, ecological and social development and provide a suitable orientation framework for a company’s sustainability strategy:

SDGs as guidelines for sustainable management

Alignment of products and services with the SDGs

Business activities can contribute directly to achieving the SDGs

Nowadays, at the current edge of development trends around sustainability, so to speak, ESG expression is thus considered a leitmotif and fundamental approach for responsible and sustainable development. It is about combining economic, social and ecological aspects in order to create a world worth living in for present and future generations.

The individual SDGs are suitable targets for integrating ESG into corporate strategies, as they are more concrete and easier to measure using indicators than the more fundamental ESG concept.

Importance of the midmarket

As the backbone of the economy, the SME sector comprises a large number of companies that operate both regionally and internationally. It is of great importance for economic performance and employment in the country. Around 2.5 million companies in Germany belong to the Mittelstand, in the definition of a small and medium-sized enterprise (SME). These range from microenterprises to medium-sized companies with up to 250 employees, which generate around one-third of total sales for Germany and employ more than half of all employees.

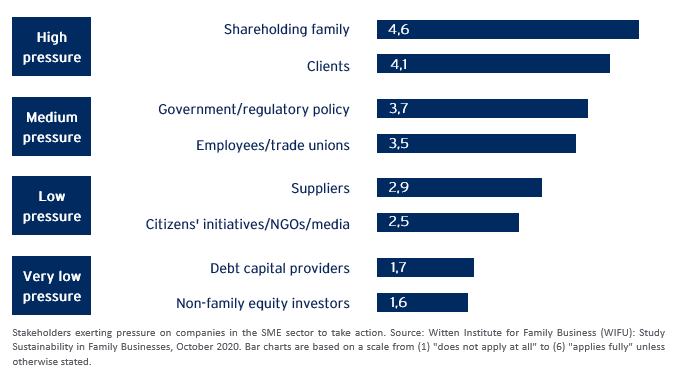

Expectations around an ESG expression of the SME business model arise in a wide variety of internal and external stakeholder groups. Typical stakeholders include shareholder families, employees, customers and suppliers, financiers (EC and FC), NGOs and the media, and to an increasing extent regulatory policy.

The reasons for which companies address ESG requirements also vary. The most common motives include:

The assumption of ecological and social-societal responsibility,

Ethical reasons and intrinsic motivation,

Requirements of customers and employees,

Cost reduction and expectation of increasing sales,

Requirements of capital providers,

And last but not least, the increasing regulatory requirements.

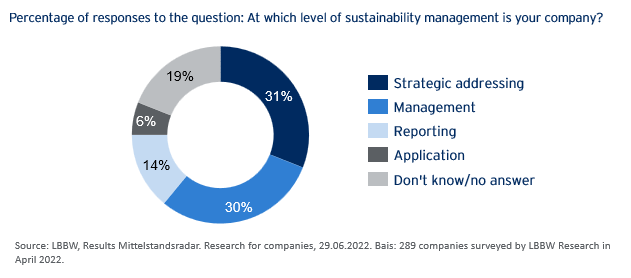

The majority of companies are in the early stages of sustainability management.

Pressure to act and status quo around ESG in SMEs

The pressure to develop and implement ESG strategies is immense and relevant stakeholders are demanding this. In addition to opportunities of an ESG orientation such as cost reduction, successful positioning of the company, revenue and profitability advantages, there are clear business risks of a lack of consideration of sustainability requirements up to the withdrawal of the « license to operate » (violation of regulatory requirements, exclusion from supply chains, lack of financing or perspective withdrawal of insurance coverage).

If, against this background, surveys come to the conclusion that, despite pressure to act and explicit expectations of the relevant stakeholders, only around half of the companies in the SME sector have developed and implemented ESG strategies, the question arises as to why.

A ´decisive factor is the lack of time and resources in many SMEs to deal with the challenges and requirements of sustainability. Time is traditionally a scarce commodity, especially in owner-managed companies. Teams and specialists for ESG strategies and sustainability cannot simply be plucked out of the ground: the market for ESG specialists is empty and salary expectations are correspondingly high.

Support from external consultants is the obvious choice, but here, too, capacities are stretched and for many a large consulting firm it is obvious and more lucrative to advise the large DAX companies with entire teams of consultants before they delve into the peculiarities of the business model of a geographically decentralized SME.

AIM – Advice in Motion GmbH

This is where AIM, as an independent sustainability consultancy and partner in the Investec network, can provide effective support. AIM thinks and speaks medium-sized. Their clients include medium-sized companies from a wide range of industries in Germany, France, Portugal, Luxembourg and Switzerland. AIM supports with:

Creation, coordination and implementation of ESG strategies in medium-sized companies,

Preparation for mandatory sustainability reporting (CSRD),

Directive-compliant calculation of the carbon footprint of companies (CCF) and products (PC),

Preparation of climate strategies, derivation of targets and measures from the climate footprint,

Communication around ESG and climate protection: avoidance of reputation risks.

Examples of successful ESG implementation in medium-sized companies:

I. Initial situation: Sustainability requirements for a medium-sized company in the wood industry in Germany with around 1,200 employees. In addition to the intrinsic motivation of the shareholders, a major impetus for action arose from the initiative of the industry association, which demands the implementation of climate protection measures for all member companies. Another impetus for action was for the company, as a supplier in the value chain of a large trading house, to support its ambition (climate protection and other social goals throughout the supply chain). AIM supported the development of a climate strategy, the calculation of the corporate carbon footprint and the compensation of unavoidable emissions in order to achieve climate neutrality.

II. Initial situation: market positioning of a 5-star resort hotel in Provence with its own vineyard. A key impetus for action was to reconcile a luxury resort with sustainability requirements and climate change mitigation measures. AIM developed an ESG strategy for the resort. This was based on a selection of sustainable development goals (SDGs) to which the resort can contribute. Corresponding measures were defined and implemented. At the same time, climate neutrality was achieved for the resort by offsetting unavoidable emissions. (AIM has implemented a comparable project with a resort in Portugal, which has since been nominated for the Sustainability Award of the Portuguese Tourism Association).

III. Initial situation: product positioning for a manufacturer of high-quality competition racing bikes from Switzerland. The company wants to make competitive sports compatible with sustainability and climate protection in particular. In order to provide buyers and users of the competition bike with an assessment of the carbon footprint of the racing bike product, AIM calculated the product-related carbon footprint for the bike, taking into account all phases of the life cycle of the racing bike, from cradle to grave.

IV. Initial situation: A medium-sized holding company with around 1000 employees in Germany will be subject to mandatory sustainability reporting in accordance with CSRD for the first time from the calendar year 2024. The extended reporting affects around 15,000 companies in Germany. The company’s sustainability performance will be considered from two perspectives: the impact of sustainability aspects on the corporate business model and the impact of the company’s activities on the environment and stakeholders. At the same time, the company aims to create a comprehensive ESG strategy that brings together all the actions taken to date to support sustainability goals. AIM has worked with the company to develop an ESG strategy that is aligned and parameterized with metrics to best prepare for upcoming sustainability reporting.

The development of company specific ESG and climate strategies and the requirements associated with the expansion of sustainability reporting pose major challenges for entrepreneurs in the SME sector. We support your company effectively in the sustainable transformation to ensure together with you the future and the competitiveness of your company for you and future generations.

Author: Andreas Kuschmann, Founding Partner AIM – Advice in Motion GmbH.

Unlocking Working Capital potential to fuel operational growth

Amidst the aftermath of the COVID-19 pandemic, geopolitical tensions, and persistent inflation, it is crucial for companies to prioritize efficient working capital management (WCM) in order to navigate near-term uncertainty and foster growth during the economic recovery. We identified four key reasons that make WCM crucial:

1.Economic headwinds are expected to be persistent: Despite the recovery of most advanced economies to pre-pandemic levels of output, growth in 2023 is projected to be sluggish. Recent downward revisions in growth forecasts highlight the challenges that lie ahead. For instance, the GDP growth forecast for the EU has been reduced to around 0.75%, a mere one-fifth of the previous year’s growth1. The IMF has also predicted that Germany will be the second weakest G7 economy next year, following the UK, with an anticipated GDP contraction of 0.11%1. Moreover, recent data reveals that the German economy contracted slightly for two consecutive quarters, by 0.5% in Q4 2022 and 0.3% in Q1 20232.

2. Inflationary pressure remains high until at least 2024: The Russian invasion of Ukraine has led to skyrocketing energy and food prices, resulting in persistent inflationary pressures. Additionally, rising material costs and supply chain challenges pose a threat to inventory levels, leaving businesses susceptible to supply shortages and price fluctuations. Although the IMF predicts a decline in inflation in Germany from 8.7% in 2022 to 6.1% in 2023, a return to the 2% target is not expected until at least 2025. Consequently, some companies have turned to forward buying and speculative upstocking. However, this strategy strains working capital and depletes cash reserves.

3. Interest rate peak has probably been reached: Central banks across the world have continued to tighten monetary policy and roll back quantitative easing to defeat red-hot inflation. In Europe, the ECB has raised its key interest rate by 0.25 percentage points to 3.5% in June, marking the eighth consecutive increase since July 2023. This rate-hiking cycle is the fastest in the ECB‘s history. ECB President Christine Lagarde announced further rate hikes in July, indicating an ongoing trend. According to a survey conducted by Bloomberg, it is projected that the peak will be reached at 4% in September 2023. Consequently, financing and working capital is becoming increasingly expensive.

4.Corporate cash flows are coming under increasing pressure: According to PwC, Days Cash on Hand of companies decreased by 10% in 20214. In 2022, the intensified efforts of central banks worldwide to combat inflation by raising interest rates have significantly impacted corporate cash flows. Mounting challenges stem from factors such as cost inflation, supply chain disruptions, and geopolitical events like the war in Ukraine, which have also influenced lender sentiment and global debt markets. In Europe, institutional loan issuance suffered a decline of 42% so far in 2023 compared to the previous year (as of July)5. As a result, the management of liquidity and working capital has become increasingly important.

Thorsten Gladiator, Managing PartnerInvestec: Supply chain issues and increasing (raw) material prices lead to higher funding requirements in working capital. A variety of working capital financing products allows for tailor-made solutions.

This report focuses solely on the automotive downstream market, i.e. the sale and use phase of a car.

Next to tremendous changes in the automotive downstream market environment, consumer demand for more flexibility in mobility as well as holistic and environmentally sustainable mobility concepts are gaining more importance.

Therefore, market participants need to adapt and rethink their business models in order to strengthen their market position, diversify their revenue streams and create stronger customer relationships.

M&A is a key instrument for both traditional automotive downstream players, to gain (digital) expertise and expand their footprint across the value chain, as well as new market participants, who are trying to gain scale, market share and international footprint quickly by leveraging their digital competencies.

In 2021, the global M&A activity in the Automotive Downstream sector experienced an increase of 15% (by number of deals).

The proportion of cross-border deals has increased from 36% in 2019 to 47% in H1 2022, underlining the trend of seeking international footprint.

Deal activity is strongly driven by strategic buyers, with 65% of global M&A activity in 2021 involving a strategic buyer.

We expect financial investor involvement to increase over the coming years, as younger companies develop towards attractive platforms for consolidation.

Valuations range from

“A high degree of innovation and shifting consumer demand pose a variety of challenges for traditional automotive downstream players while creating chances for disruptive new market entries. The fight for scale and market position has only just begun.”

Propos recueillis par Jessica Huynh, CosmétiqueMag Hebdo, Juin 2020

Plusieurs fusions-acquisitions ont été finalisées depuis le début de la crise sanitaire. Est-ce selon vous surprenant ou attendu ?

Une acquisition passe par plusieurs phases : entre la signature (signing) et la clôture (closing), il peut se passer quelques jours à plusieurs semaines. Plusieurs opérations ont donc pu être signées avant le confinement et mécaniquement se concrétiser pendant. En parallèle, d’autres ont été interrompues. Pour certains rachats dont les discussions ont été commencées avant et qui n’auraient pas franchi la phase de signing, les acheteurs peuvent facilement quitter la table des négociations. Pour d’autres qui auraient fait l’objet d’un signing, l’acheteur peut se libérer de l’accord en faisant jouer quelques astuces juridiques.

La crise sanitaire peut-elle avoir un impact sur les prix des entreprises ?

La valeur d’une entreprise, c’est le reflet de l’anticipation de ses résultats futurs. Dans la beauté, on observait pré-Covid des multiples de valorisation allant de 2 à 5 fois le chiffre d’affaires et / ou 10 à 20 fois l’EBITDA pour les marques. Actuellement, les entreprises de packaging cotées qui dégagent en moyenne une rentabilité d’exploitation (de l’ordre de 15 % d’EBITDA et 10 % d’EBIT en 2019) et une croissance historique de +4 à 5 % par an sur les trois dernières années (avant impact Covid) valent autour de 9 fois l’EBITDA et 13 fois l’EBIT, avec toutefois des disparités importantes. Fatalement, le Covid-19 va avoir un impact sur les prix. Ce phénomène reste à mon sens plutôt conjoncturel et devrait se corriger sous 18 à 24 mois.

Les fusions-acquisitions vont-elles rapidement reprendre, une fois la crise derrière nous ?

Le volume d’opérations va clairement être en retrait en 2020. Les actionnaires d’entreprises sont aujourd’hui davantage préoccupés par la gestion de la crise pour limiter les impacts pour leur entreprise que par des réflexions de cession. Ceux qui y pensaient ou qui venaient de lancer la cession vont avoir du mal à atteindre leurs objectifs de prix. Après un gros coup de frein en 2020, nous pensons que le volume de transactions repartira progressivement au deuxième semestre 2021 pour revenir à la normale en 2022.

Le dossier complet du magazine, dédié à l’impact du Covid19 sur le secteur des cosmétiques, est téléchargeable ici

It was a banner year for beauty deals in 2019, as strategic investors and others looked to bring new brands and innovations in-house. Premium skincare, in particular, attracted a wide range of buyers:

led by the beauty giants, who secured several innovative high-growth brands – eg. acquisitions by Coty (Kylie), Estee Lauder (Have and Be) and Shisiedo (Drunk Elephant);

personal care corporates, attracted by the high margins and growth trends (Colgate-Palmolive acquired Filorga, and Unilever acquired Tatcha and Garancia);

fragrance players, who widened their strategic focus (L’Occitane acquired Elemis);

and financial investors, who also ramped up investments (EQT acquired Nestle Skin Health, Sofina invested in Nuxe).

In 2020, we expect private equity and strategic investor enthusiasm to persist. Popular product categories include skincare brands with proven scientific efficacy, sustainability credentials, and young customer bases. Haircare is also popular.

The beauty giants are seeking high-growth brands that access strategically important consumer demographics, while the personal-care corporates are looking to expand their beauty and skincare portfolios. For example, Unileverhas become a serial acquirer, highlighted by the Tatcha and Garancia deals. (Acquisitions account for the main share of growth within Unilever’s skincare portfolio, which includes Murad, Dermalogica, REN Clean Skincare, Kate Somerville, Living Proof, and Hourglass.) Likewise, Colgate Palmolive is finally engaging in focused acquisitions in skincare to grow its beauty portfolio and develop outside oral care.

Private equity investments are on the rise in beauty and skincare. These savvy financial investors are attracted by the high gross margins, repeat purchase trends, alternative sales channels, and the large international markets that provide additional runways for growth. Private equity was responsible for almost half of the deal activity in the Beauty sector in 2019.

The Swedish private equity firm EQT Partners (a subsidiary of the Abu Dhabi Investment Authority) led a consortium to acquire Nestle’s non-core ‘skin health’ business (rev: $2.7bn) in a deal reportedly worth $10bn. This transaction followed a fiercely competitive sales process in which private equity firms KKR, Advent International and Cinven were other high-profile suitors, as were Unilever and Colgate-Palmolive.

Premium natural cosmetics specialist L’Occitane International acquired the luxury skincare company Elemis (UK; 2018 rev: $140m) for $900m. Elemis is the leading independent British skincare brand, one with strong cross-generational consumer appeal, including the millennial demographic, but has been working to establish itself in new channels and geographies.

Coty acquired a majority 51% stake in Kylie Cosmetics (US; 2018 rev: $170m) for $600m. Kylie Cosmetics was founded by the 22-year-old ‘mega-influencer’ Kylie Jenner, who has no less than 163 million followers on Instagram. The deal makes Coty the first major strategic beauty company to buy into the influencer life. Coty plans to expand the brand geographically and into new beauty categories.

The German consumer goods group Beiersdorf (owner of Nivea) acquired the sun-care brand Coppertone (US; 2018 rev: $213m) for $550m. The deal strengthens Beiersdorf’s position in North America and “adds complementary expertise to its brand portfolio”. The company is actively seeking acquisitions and sitting on a cash pile of more than 4 billion euros.

Estée Lauder acquired full control of Have & Be Co. (KOR; 2019 rev: c. $500m), the Seoul-based skincare company behind Dr. Jart+ and men’s grooming brand Do The Right Thing. This is Estée Lauder’s first acquisition of an Asia-based beauty brand. Have & Be is growing rapidly, renowned for its leading and fast-moving innovation pipeline that offers a wide variety of high-performing skincare products that appeal to a broad range of consumers, including millennials in Asia and the US.

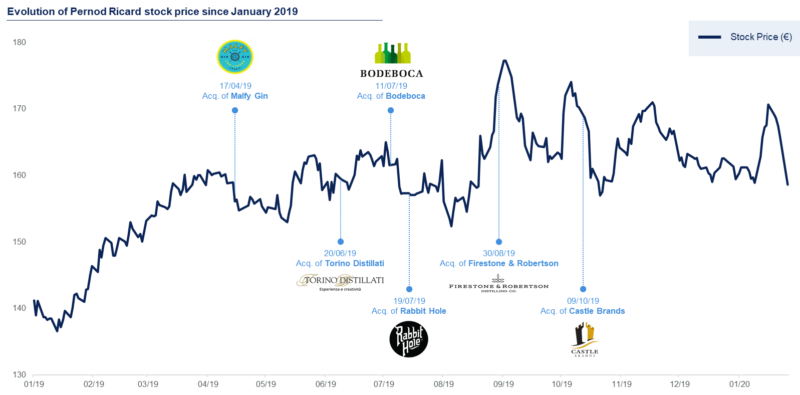

The French wine & spirits group made six key acquisitions in 2019, designed to strengthen its premium brands portfolio.

The premium segment of the Alcoholic Beverages market is forecast to grow at c. 5% CAGR between 2019 and 2023, compared to just 0.4% for ‘standard-and-below’ spirits over the same period.*

“The acquisition strategy is leveraging booming categories and reinforcing must-win, key strategic markets,” explains Pernod Ricard’s CEO Alexandre Ricard, who has made the group one of the most acquisitive in the industry.

When Alexandre Ricard became CEO of Pernod Ricard in 2015, the world’s second largest wines & spirits group was experiencing sluggish sales and the stock price was flatlining. Since then, the group’s sales have increased by c. 25% (FY19 rev: €9.2bn) and the stock price by c. 60%.

His thoughts on the premiumization trend:

“I think premiumisation is here to stay and is still by far a big value creation lever. People are trading up to higher quality brands all over the world, led by the US. People always aspire to ‘better’ and that is the story of civilisation…That is the area we want to play in. We do not see any strategic interest in the trade down part (standard and value-for-money segments). We like selling premium products that have a story.”

And on organic & external growth:

“Last year, for the first time, more than half of the world’s population had enough disposable income to be categorized as middle class. By 2030, there will be 2 billion more middle-class people in this world…People are drinking less but drinking better – and we expect the premiumization of our brands, our strong position in luxury spirits, to be one of the factors accelerating our growth.”

“From an M&A point of view, our strategy is clear and simple. Number one is to leverage dynamic categories. The gin and whisky categories and bourbon in particular. It drove us to do Smooth Ambler [acquired in 2017], TX Whiskey [acquired Firestone & Robertson Distilling Co in 2019], Rabbit Hole [acquired in 2019], and Castle Brands [acquired in 2019]…Some of these US whiskey brands are designed to stay regional, others to be national, and of course travel retail will be an opportunity for some of these to go beyond the US market…Where we see ‘demand spaces’ that we are not in, and believe we ought to be in, we will look to new products, bolt-on acquisitions or partnerships where the entrepreneur who created this new brand is still driving the business. This is what we have done with Smooth Ambler bourbon and artisanal mezcal producer Del Maguey Single Village…”

Is Nike’s ‘Zoom X Vaporfly’ the fastest running shoe on the planet?

Technological leaps in running shoes are rare, but Nike’s ‘Zoom X Vaporfly’ is a genuine game-changer in the massive EUR 13 billion running shoes market.

When the first version of the Vaporfly was launched in 2016, Nike called it « a racing shoe that breaks records », which sounded like marketing, but it wasn’t. The shoe is literally breaking records. Too many, according to the International Association of Athletics Federations (IAAF), creating controversy within the running community and forcing the sporting goods market to innovate or face losing market share.

What’s so special about the Zoom X Vaporfly?Before the Vaporfly, little had changed in the footwear for elite marathon runners in 50 years. Previously, running shoes only had to be light and thin, and were usually constructed from thin slabs of rubber. The Vaporfly is very different: constructed with light-weight foam that is stacked high and containing a carbon fibre plate, which is the feature mentioned most prominently in Nike’s patent application. Runners say it feels like the shoe is propelling them forward, and the evidence supports this.

In 2019…

In the six world marathon majors, 31 of the 36 podium positions were won by athletes wearing Vaporfly.

Kenyan runner Eliud Kipchoge wore Vaporfly in the first marathon ever completed in under two hours, which was considered a time mark that could not be broken.

Brigid Kosgei used the Vaporfly to break the women’s world marathon record.

The New York Times conducted a study on the Vaporfly and found that it did make runners faster, by around 4%.

Following these events, and after several professional runners voiced complaints about the technology within the Vaporfly, the IAAF was forced to update its rules.

It is now prohibited to use “soles thicker than 40mm”, and to use “more than one carbon-fibre plate, or similar item, in the sole”. It means that Nike’s controversial Vaporfly range remains compliant and is permitted for use – the ‘Zoom X Vaporfly 4%’ and ‘Zoom X Vaporfly Next%’ running shoes both have a 36mm midsole. However the prototype model worn by Eliud Kipchoge to break the two-hour marathon record is now banned, as it provides too much of a performance advantage with its even chunkier sole and three carbon-fibre plates.

The new rules make sense, given that without clear restrictions, it was only a matter of time before someone developed a runner with more powerful springs, or footwear that we don’t even recognize as shoes.

“It is clear that some forms of technology would provide an athlete with assistance that runs contrary to the values of the sport.” IAAF

Running shoes is a $13 billion market that is expected to grow at a CAGR of 7% over the next five years. Nike is the clear leader, holding 51% of the market, while Asics is its biggest rival, with a 15% market share. Meanwhile, shoes account for about 47% of Nike’s total revenues, so an increasing share within a rapidly growing market will meaningfully affect Nike’s revenue growth going forward.

The stock price of Nike’s largest competitor in the running market, Asics Corp, dropped c. 10% when Kenyan runner Eliud Kipchoge became the first human to run a marathon in less than two hours. (Nike is reportedly adjusting the banned prototype design used in this race to make it competition legal before the Tokyo 2020 Olympics.)

This innovation race in running shoe design is only getting started, as Nike’s competitors have started launching high-tech running shoes of their own:

New Balance Athletic has launched a line of shoes with technical foams and carbon fibre plates that its runners can wear in Tokyo, and is “very concerned by the fact that these rules were adopted without meaningful consultation involving sporting goods industry”.

Saucony launched a new model in late 2019 called the Endorphin Pro, which Runner’s World magazine called the “closest approximation we’ve seen” to the Vaporfly.

Brooks has a new running shoe called the Hyperion Elite that goes on sale Feb. 27, according to the brand. Like Nike’s Vaporfly it is a light-weight shoe made for breaking records and includes a carbon-fibre plate sandwiched in the midsole foam to promote propulsion.

Les groupes de beauté et les fonds d’investissement s’intéressent de près aux marques capillaires professionnelles. En 2019, quelques indépendantes telles que Olaplex, DevaCurl ou encore Christophe Robin, ont fait l’objet de rachat.

Les produits professionnels, contrairement à d’autres catégories comme le maquillage, ont l’avantage d’être un peu plus à l’abri des effets de mode…

Pour découvrir l’article rédigé en partenariat avec Cosmétiquemag, cliquez ici

Les marques de sport en pleine forme

Le marché mondial des articles de sport continue d’afficher des performances exceptionnelles, soutenues par une pratique croissante des activités sportives, ainsi que par les tendances de la mode casual. Plus que jamais, le consommateur est roi et les marques cherchent de nouvelles façons de le fidéliser, en développant des stratégies omnicanales toujours plus attractives et innovantes.

Sur le marché du M&A, les opérations se poursuivent. Les acquéreurs en profitent pour élargir leurs portefeuilles de produits (synergies de coûts et de distribution) et pour étendre leur empreinte géographique.

Le marché des articles de sport était évalué à 471 mds$ en 2018 et devrait atteindre 627 mds$ en 2023, avec 7% de CAGR2017-2023.

La croissance varie d’un segment à l’autre. En 2018, c’est le basketball qui affichait la plus élevée (+11%), suivi par le running (+7%), le football (+7%), et le cyclisme (+6%). En termes de volume, c’est le cycle qui remporte la mise avec 62 mds$, puis le sportswear (49 mds$), la randonnée (39 mds$) et le running (33 mds$).

Le marché bénéficie d’excellents fondamentaux industriels, mais le positionnement produit reste essentiel. La croissance des gammes féminines, l’outdoor, la personnalisation, l’éco-référencement et les canaux de distribution directs sont les stratégies privilégiées.

Les grandes marques mondiales et les fonds d’investissement sont très actifs. La plupart des opérations sont recensées en Europe (env. 50 % du total des opérations), où la consolidation s’accélère. Les acquisitions transfrontalières sont en hausse, les marques cherchant à accroître leur clientèle internationale.

Certaines transactions ont fait la une en 2019, comme l’acquisition du géant finlandais de l’équipement sportif Amer Sports (CA 3,2 mds$) par le leader chinois Anta Sports (CA 3,6 mds$) – qui étend la portée internationale d’Anta et répond à une stratégie de croissance pour compléter le marché intérieur chinois.

Les multiples de valorisation moyens sont de 14,8x EBITDA en 2019 pour les sociétés cotées. Sur le mid-market européen, l’EBITDA à deux chiffres est “la nouvelle norme”.

When Alexandre Ricard became CEO of Pernod Ricard in 2015, the world’s second largest wines & spirits group was experiencing sluggish sales and the stock price was flatlining. Since then, the group’s sales have increased by c. 25% (FY19 rev: €9.2bn) and the stock price by c. 60%.

When Alexandre Ricard became CEO of Pernod Ricard in 2015, the world’s second largest wines & spirits group was experiencing sluggish sales and the stock price was flatlining. Since then, the group’s sales have increased by c. 25% (FY19 rev: €9.2bn) and the stock price by c. 60%.