As we enter 2024, the M&A landscape shows signs of recovery, albeit cautiously.

In the episode of the February 20, 2024 of No Ordinary Wednesday, Jeremy Maggs in conversation with Investec experts Jürgen Schwarz, Marleen Vermeer, and Kilian de Gourcuff, Investec’s Head of Cross-Border Finance and International Advisory Charles Barlow, on what key sectors, trends and risks to keep an eye on in 2024.

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Extensive track record combined with deep industry knowledge

Interview with Jürgen Schwarz, Managing Partner of Investec about the role aggregators play in the e-commerce market:

How is the client’s situation?

How is the e-commerce market structured?

How can we operate the sales process?

Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

The dynamic and rapidly changing consumer goods sector is facing major challenges due to advancing digitalisation and the emergence of new disruptive business models. We drill down into sub-sectors that show strong growth potential and/or an increase in consolidation.

In the context of this fiercer competition and increasing consolidation activity, we support you in identifying and realising entrepreneurial opportunities.

The majority of our transactions are cross-border – within Europe and beyond – and are carried out by an international team of experienced advisors with extensive sector and transaction expertise.

Financial restructuring for Shareholders & Lenders

Helping clients to navigate uncertainties while putting their businesses back on track

Interview with Jürgen Schwarz, Managing Partner of Investec about Restructuring with the help of a M&A process:

How did the market change in recent years?

What is your approach?

Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

Sale from insolvency

Due to our pan-European presence and track record we are well placed to advise on international and cross-border restructurings.

Our international sector teams implement more than 50 transactions p.a. and in many sectors they know the active buyers, the acquisition criteria, the behaviour of individual decision makers. We also have an up-to-date overview of the market prices paid, which vary considerably over time and depending on the positioning in the sector.

Investec has direct access to numerous international equity and debt capital providers and has carried out numerous restructurings ranging from approximately 10 million Euros to several billion Euros.

Financiering en markttrends | 2023

Waarom de Duitse industrie grote behoefte heeft aan investeringen.

De Duitse industrie staat voor grote uitdagingen, waaronder de effecten van digitalisering, de verschuiving van analoge naar digitale bedrijfsmodellen, de behoefte aan milieubeschermende maatregelen en duurzame productieprocessen, evenals demografische veranderingen, die leiden tot een tekort aan geschoolde werknemers en een vergrijzende beroepsbevolking. Om deze processen succesvol te beheersen, zijn aanzienlijk hogere investeringsinspanningen nodig dan in het verleden.

Digitalisering en Industrie 4.0: Op dit moment staat Duitsland op zijn best in de middenmoot van de EU wat betreft het gebruik van digitale technologieën in de economie1. De Duitse industrie moet investeren in digitale technologieën en automatisering om concurrerend te blijven. Maar om de achterstand op vergelijkbare landen in te lopen, zouden de investeringen in IT en digitalisering in Duitsland moeten verdubbelen of verdrievoudigen van 49 miljard euro naar 100 tot 150 miljard euro per jaar. Alleen al in het mkb zouden de uitgaven voor digitalisering moeten stijgen van 18 miljard euro in 2019 naar 35 tot 50 miljard euro per jaar.

Duurzaamheid en milieubescherming: Bedrijven richten zich steeds meer op milieuvriendelijke technologieën en processen om hun duurzaamheidsdoelstellingen te halen en hun impact op het milieu te verminderen. Deze investeringen dienen niet alleen om het milieu te beschermen, maar dragen ook bij aan het concurrentievermogen op lange termijn. Een recente studie in opdracht van KfW schat de klimaatbeschermingsinvesteringen die nodig zijn om de doelstelling van klimaatneutraliteit tegen 2050 te bereiken op ongeveer 5 biljoen euro of ongeveer 190 miljard euro per jaar1. Dit enorme bedrag maakt duidelijk dat er aanzienlijk grotere inspanningen nodig zullen zijn om de doelstelling te halen dan tot nu toe het geval is geweest.

Thorsten Gladiator, Managing Partner Investec: As corporate finance advisors, we see the importance of ESG in general and sustainability aspects in particular in almost every transaction, both in M&A situations and in financing mandates.

Equity and debt investors place a strong focus on ESG compliant investments in the interest of their financiers and / or due to investment criteria that are binding for them.

For business sellers as well as CFOs, this has pricing and process consequences:

A clearly defined and documented ESG strategy creates confidence among investors and the company’s other stakeholders

The same applies to the (early) implementation of legal requirements for sustainability reporting (CSRD)

A focus on sustainability aspects provides positive differentiation features compared to competitors and can thus have a value-creating effect

The lack of a corresponding strategy can lead to price discounts in the valuation as well as higher financing costs

In the due diligence phase of a transaction, lack of ESG information leads to prolonged processes, higher management burden and the withdrawal of investors with clearly defined ESG investment criteria

The following article from AIM – Advice in Motion highlights the various aspects for medium-sized companies and shows examples of successful ESG strategies.

Opportunities and challenges of sustainability for smaller and medium-sized enterprises

The sustainability performance of a company today is the decisive factor for its competitiveness tomorrow. In this context, medium-sized companies in Germany in particular are faced with tasks whose extent has not yet been fully recognized in many cases and which involve major challenges in terms of resources, time and expertise.

Even though sustainability is a ubiquitous and much-discussed topic that is omnipresent both in the media and in public debate, it is by no means a new issue. Rather, sustainability has a long and exciting history that spans centuries and has been shaped by various actors and concepts.

Where do the roots of sustainability lie?

As far back as the Middle Ages, the moral ideal of the honorable merchant played a decisive role in promoting sustainable principles. Many a family entrepreneur rightly sees himself or herself in the tradition of the honorable merchant and aligns his or her business conduct with principles such as honesty, responsibility and sustainability.

In the 18th century, the Saxon chief miner Carl von Carlowitz coined the term sustainability in his work “Sylvicultura Oeconomica.” He introduced the idea that forest resources should be managed sustainably by cutting only as much wood as can naturally grow back. What was interesting about Carlowitz’s concept of sustainability was that sustained yield was precisely not antithetical to sustainability. Rather, forestry yield acted as the cornerstone for this oft-cited source of the concept of sustainability. The mining area of the Erzgebirge was simply dependent on the sustainable use of wood for construction, mining and smelting purposes.

Another significant milestone in the development of sustainability was the Brundtland Report, published in 1987 under the title “Our Common Future”. The report defined sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” Here, sustainability clearly went beyond a purely economic consideration. The report emphasized the need to integrate economic, social and environmental aspects to create a sustainable future.

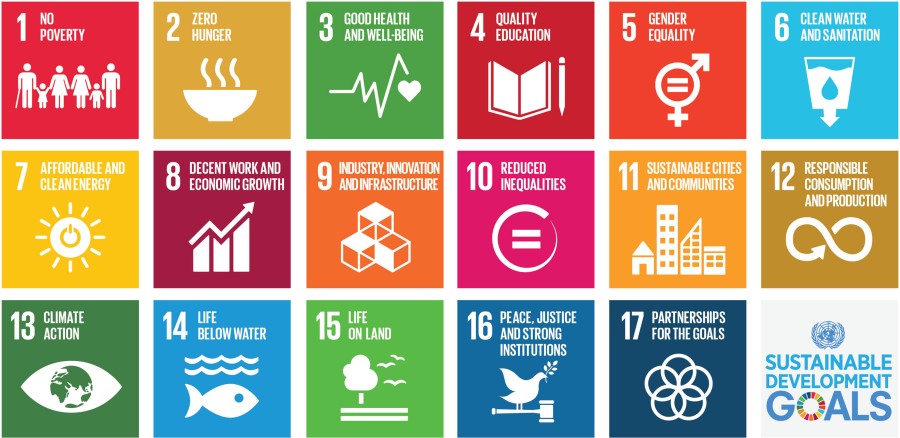

Since then, the understanding of sustainability has evolved to encompass a variety of dimensions. One key concept is ESG (environmental, social, governance) criteria, which encompass environmental, social and governance-related factors. Differentiation of individual sustainable development goals is achieved through the United Nations Sustainable Development Goals (SDGs), which were adopted in 2015. The SDGs include 17 global goals to promote sustainable development at the economic, social and environmental levels by 2030. These goals range from poverty reduction, health, education and gender equality to renewable energy and sustainable cities.

The SDGs are an excellent framework for linking the principle of sustainability with economic, ecological and social development and provide a suitable orientation framework for a company’s sustainability strategy:

SDGs as guidelines for sustainable management

Alignment of products and services with the SDGs

Business activities can contribute directly to achieving the SDGs

Nowadays, at the current edge of development trends around sustainability, so to speak, ESG expression is thus considered a leitmotif and fundamental approach for responsible and sustainable development. It is about combining economic, social and ecological aspects in order to create a world worth living in for present and future generations.

The individual SDGs are suitable targets for integrating ESG into corporate strategies, as they are more concrete and easier to measure using indicators than the more fundamental ESG concept.

Importance of the midmarket

As the backbone of the economy, the SME sector comprises a large number of companies that operate both regionally and internationally. It is of great importance for economic performance and employment in the country. Around 2.5 million companies in Germany belong to the Mittelstand, in the definition of a small and medium-sized enterprise (SME). These range from microenterprises to medium-sized companies with up to 250 employees, which generate around one-third of total sales for Germany and employ more than half of all employees.

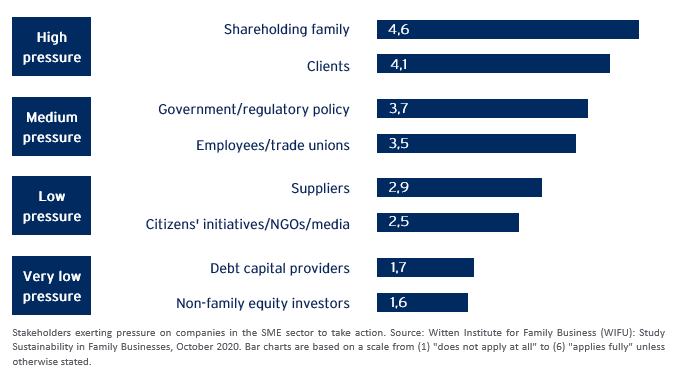

Expectations around an ESG expression of the SME business model arise in a wide variety of internal and external stakeholder groups. Typical stakeholders include shareholder families, employees, customers and suppliers, financiers (EC and FC), NGOs and the media, and to an increasing extent regulatory policy.

The reasons for which companies address ESG requirements also vary. The most common motives include:

The assumption of ecological and social-societal responsibility,

Ethical reasons and intrinsic motivation,

Requirements of customers and employees,

Cost reduction and expectation of increasing sales,

Requirements of capital providers,

And last but not least, the increasing regulatory requirements.

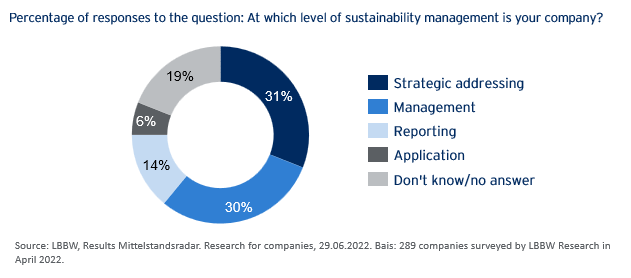

The majority of companies are in the early stages of sustainability management.

Pressure to act and status quo around ESG in SMEs

The pressure to develop and implement ESG strategies is immense and relevant stakeholders are demanding this. In addition to opportunities of an ESG orientation such as cost reduction, successful positioning of the company, revenue and profitability advantages, there are clear business risks of a lack of consideration of sustainability requirements up to the withdrawal of the “license to operate” (violation of regulatory requirements, exclusion from supply chains, lack of financing or perspective withdrawal of insurance coverage).

If, against this background, surveys come to the conclusion that, despite pressure to act and explicit expectations of the relevant stakeholders, only around half of the companies in the SME sector have developed and implemented ESG strategies, the question arises as to why.

A ´decisive factor is the lack of time and resources in many SMEs to deal with the challenges and requirements of sustainability. Time is traditionally a scarce commodity, especially in owner-managed companies. Teams and specialists for ESG strategies and sustainability cannot simply be plucked out of the ground: the market for ESG specialists is empty and salary expectations are correspondingly high.

Support from external consultants is the obvious choice, but here, too, capacities are stretched and for many a large consulting firm it is obvious and more lucrative to advise the large DAX companies with entire teams of consultants before they delve into the peculiarities of the business model of a geographically decentralized SME.

AIM – Advice in Motion GmbH

This is where AIM, as an independent sustainability consultancy and partner in the Investec network, can provide effective support. AIM thinks and speaks medium-sized. Their clients include medium-sized companies from a wide range of industries in Germany, France, Portugal, Luxembourg and Switzerland. AIM supports with:

Creation, coordination and implementation of ESG strategies in medium-sized companies,

Preparation for mandatory sustainability reporting (CSRD),

Directive-compliant calculation of the carbon footprint of companies (CCF) and products (PC),

Preparation of climate strategies, derivation of targets and measures from the climate footprint,

Communication around ESG and climate protection: avoidance of reputation risks.

Examples of successful ESG implementation in medium-sized companies:

I. Initial situation: Sustainability requirements for a medium-sized company in the wood industry in Germany with around 1,200 employees. In addition to the intrinsic motivation of the shareholders, a major impetus for action arose from the initiative of the industry association, which demands the implementation of climate protection measures for all member companies. Another impetus for action was for the company, as a supplier in the value chain of a large trading house, to support its ambition (climate protection and other social goals throughout the supply chain). AIM supported the development of a climate strategy, the calculation of the corporate carbon footprint and the compensation of unavoidable emissions in order to achieve climate neutrality.

II. Initial situation: market positioning of a 5-star resort hotel in Provence with its own vineyard. A key impetus for action was to reconcile a luxury resort with sustainability requirements and climate change mitigation measures. AIM developed an ESG strategy for the resort. This was based on a selection of sustainable development goals (SDGs) to which the resort can contribute. Corresponding measures were defined and implemented. At the same time, climate neutrality was achieved for the resort by offsetting unavoidable emissions. (AIM has implemented a comparable project with a resort in Portugal, which has since been nominated for the Sustainability Award of the Portuguese Tourism Association).

III. Initial situation: product positioning for a manufacturer of high-quality competition racing bikes from Switzerland. The company wants to make competitive sports compatible with sustainability and climate protection in particular. In order to provide buyers and users of the competition bike with an assessment of the carbon footprint of the racing bike product, AIM calculated the product-related carbon footprint for the bike, taking into account all phases of the life cycle of the racing bike, from cradle to grave.

IV. Initial situation: A medium-sized holding company with around 1000 employees in Germany will be subject to mandatory sustainability reporting in accordance with CSRD for the first time from the calendar year 2024. The extended reporting affects around 15,000 companies in Germany. The company’s sustainability performance will be considered from two perspectives: the impact of sustainability aspects on the corporate business model and the impact of the company’s activities on the environment and stakeholders. At the same time, the company aims to create a comprehensive ESG strategy that brings together all the actions taken to date to support sustainability goals. AIM has worked with the company to develop an ESG strategy that is aligned and parameterized with metrics to best prepare for upcoming sustainability reporting.

The development of company specific ESG and climate strategies and the requirements associated with the expansion of sustainability reporting pose major challenges for entrepreneurs in the SME sector. We support your company effectively in the sustainable transformation to ensure together with you the future and the competitiveness of your company for you and future generations.

Author: Andreas Kuschmann, Founding Partner AIM – Advice in Motion GmbH.

Unlocking Working Capital potential to fuel operational growth

Amidst the aftermath of the COVID-19 pandemic, geopolitical tensions, and persistent inflation, it is crucial for companies to prioritize efficient working capital management (WCM) in order to navigate near-term uncertainty and foster growth during the economic recovery. We identified four key reasons that make WCM crucial:

1.Economic headwinds are expected to be persistent: Despite the recovery of most advanced economies to pre-pandemic levels of output, growth in 2023 is projected to be sluggish. Recent downward revisions in growth forecasts highlight the challenges that lie ahead. For instance, the GDP growth forecast for the EU has been reduced to around 0.75%, a mere one-fifth of the previous year’s growth1. The IMF has also predicted that Germany will be the second weakest G7 economy next year, following the UK, with an anticipated GDP contraction of 0.11%1. Moreover, recent data reveals that the German economy contracted slightly for two consecutive quarters, by 0.5% in Q4 2022 and 0.3% in Q1 20232.

2. Inflationary pressure remains high until at least 2024: The Russian invasion of Ukraine has led to skyrocketing energy and food prices, resulting in persistent inflationary pressures. Additionally, rising material costs and supply chain challenges pose a threat to inventory levels, leaving businesses susceptible to supply shortages and price fluctuations. Although the IMF predicts a decline in inflation in Germany from 8.7% in 2022 to 6.1% in 2023, a return to the 2% target is not expected until at least 2025. Consequently, some companies have turned to forward buying and speculative upstocking. However, this strategy strains working capital and depletes cash reserves.

3. Interest rate peak has probably been reached: Central banks across the world have continued to tighten monetary policy and roll back quantitative easing to defeat red-hot inflation. In Europe, the ECB has raised its key interest rate by 0.25 percentage points to 3.5% in June, marking the eighth consecutive increase since July 2023. This rate-hiking cycle is the fastest in the ECB‘s history. ECB President Christine Lagarde announced further rate hikes in July, indicating an ongoing trend. According to a survey conducted by Bloomberg, it is projected that the peak will be reached at 4% in September 2023. Consequently, financing and working capital is becoming increasingly expensive.

4.Corporate cash flows are coming under increasing pressure: According to PwC, Days Cash on Hand of companies decreased by 10% in 20214. In 2022, the intensified efforts of central banks worldwide to combat inflation by raising interest rates have significantly impacted corporate cash flows. Mounting challenges stem from factors such as cost inflation, supply chain disruptions, and geopolitical events like the war in Ukraine, which have also influenced lender sentiment and global debt markets. In Europe, institutional loan issuance suffered a decline of 42% so far in 2023 compared to the previous year (as of July)5. As a result, the management of liquidity and working capital has become increasingly important.

Thorsten Gladiator, Managing PartnerInvestec: Supply chain issues and increasing (raw) material prices lead to higher funding requirements in working capital. A variety of working capital financing products allows for tailor-made solutions.

This report focuses solely on the automotive downstream market, i.e. the sale and use phase of a car.

Next to tremendous changes in the automotive downstream market environment, consumer demand for more flexibility in mobility as well as holistic and environmentally sustainable mobility concepts are gaining more importance.

Therefore, market participants need to adapt and rethink their business models in order to strengthen their market position, diversify their revenue streams and create stronger customer relationships.

M&A is a key instrument for both traditional automotive downstream players, to gain (digital) expertise and expand their footprint across the value chain, as well as new market participants, who are trying to gain scale, market share and international footprint quickly by leveraging their digital competencies.

In 2021, the global M&A activity in the Automotive Downstream sector experienced an increase of 15% (by number of deals).

The proportion of cross-border deals has increased from 36% in 2019 to 47% in H1 2022, underlining the trend of seeking international footprint.

Deal activity is strongly driven by strategic buyers, with 65% of global M&A activity in 2021 involving a strategic buyer.

We expect financial investor involvement to increase over the coming years, as younger companies develop towards attractive platforms for consolidation.

Valuations range from <1x Sales for smaller traditional businesses up to ~8.0x Sales for established high-growth digital businesses.

“A high degree of innovation and shifting consumer demand pose a variety of challenges for traditional automotive downstream players while creating chances for disruptive new market entries. The fight for scale and market position has only just begun.”

What to do when earnings fall, liquidity becomes scarce and existing investors say no?

In crises such as COVID-19, the first priority is to ensure the company’s liquidity by taking advantage of all aid programmes and by securing promotional and guarantee loans. However, falling earnings and cash flows and weak liquidity also require rapid operational and financial restructuring to make the company weatherproof in the long term.

While the basis of a restructuring is of course always a solid operational restructuring concept, the existing capital structure must be adapted to future cash flows with the same high priority. Refinancing/rescheduling of debt and the sale of non-strategic or non-operational assets are often essential elements in this process.

Dissolve blockade with a clear concept for restructuring

Although a good operational concept often exists, unfortunately many companies slide into insolvency despite good approaches because they cannot (or not fast enough) explain to stakeholders what the concept means for them financially and what their specific benefit will be after its implementation.

In more complex cases, a financial restructuring concept depicting the cash flows and values throughout the restructuring phase and thereafter across the various financing instruments and capital providers is required. The concept clarifies to all stakeholders the consequences of the restructuring for their own values and the associated opportunities and risks. A consensus can only be reached if this is done professionally, i.e. if each stakeholder knows his options and perspectives.

The capital structure must be adapted as best as possible to the new cash flow patterns in the crisis. In this way, insolvency can be avoided, values preserved, and the success of the company secured.

Clear restructuring concept, debt payback via sale of non-core assets and subsidiaries, refinancing via syndicated loan

Due to inefficient operating structures, excursions into risky project development and a barely manageable complexity of bilateral loan agreements and special purpose companies, the residential real estate company of the City of Mainz was plunged into an earnings and liquidity crisis with dimensions threatening its existence. We were given the mandate to develop and implement a concept for the financial restructuring of their approximately € 1bn million balance sheet.

Standstill agreement and restructuring agreement negotiated

Following our appointment, we worked with the CRO and the operational restructuring advisors to develop a viable restructuring concept for the shareholders’ meeting and the creditors’ committee, within a few weeks. The concept detailed and clarified the rating and valuation consequences of all structural and operational measures as well as the sale of assets proposed by us for the individual stakeholders.

On this basis, we were first able to conclude a standstill agreement with the lenders and then based on an IBR (IDW S6 expert opinion) we were able to negotiate a restructuring agreement with all parties.

Conversion and refinancing in syndicated loan for Wohnbau

The agreed sales and cost-cutting measures were implemented, thereby improving the debt capacity and debt service capacity of Wohnbau Mainz.

The company was split up into a stable residential construction company with an investment grade rating and a rather risky project development company. Non-strategic property portfolios were sold. The proceeds were used to reduce debt and to renegotiate over 80 bilateral and cross collateralized loans that were ultimately bundled into a syndicated loan.

Solidly positioned after successful financial restructuring

Today Wohnbau Mainz is once again a solidly positioned company with a stable and sustainable financing structure. The value of the company has been maintained for the shareholders and creditors. An insolvency and thus a massive destruction of value was avoided.

Investec has successfully accompanied more than 60 financial restructurings over the last decade

Investec, has been assisting its clients in such complex refinancing and restructuring transactions for over 15 years. We know the objectives of all stakeholders well, having successfully solved cases for companies and their shareholders as well as for banks and other creditors. In over 90% of cases, on whichever side, we have been able to reach a consensus between these groups on the necessary restructuring measures.

Core competences, company valuation, rating, financial modeling, capital raising and Selling companies

Our core competencies include financial modelling, rating analysis and company valuation as well as the preparation of internal committee documents for banks/creditor pools and shareholder/supervisory bodies. We develop a conclusive debt and equity story for existing creditors and new debt and equity investors.

We subsequently implement the measures, negotiate restructuring agreements and raise capital. We support you in the sale of subsidiaries and non-strategic business units through restructurings which are advised in close cooperation between our global sector teams and our capital advisory groups.

It was a banner year for beauty deals in 2019, as strategic investors and others looked to bring new brands and innovations in-house. Premium skincare, in particular, attracted a wide range of buyers:

led by the beauty giants, who secured several innovative high-growth brands – eg. acquisitions by Coty (Kylie), Estee Lauder (Have and Be) and Shisiedo (Drunk Elephant);

personal care corporates, attracted by the high margins and growth trends (Colgate-Palmolive acquired Filorga, and Unilever acquired Tatcha and Garancia);

fragrance players, who widened their strategic focus (L’Occitane acquired Elemis);

and financial investors, who also ramped up investments (EQT acquired Nestle Skin Health, Sofina invested in Nuxe).

In 2020, we expect private equity and strategic investor enthusiasm to persist. Popular product categories include skincare brands with proven scientific efficacy, sustainability credentials, and young customer bases. Haircare is also popular.

The beauty giants are seeking high-growth brands that access strategically important consumer demographics, while the personal-care corporates are looking to expand their beauty and skincare portfolios. For example, Unileverhas become a serial acquirer, highlighted by the Tatcha and Garancia deals. (Acquisitions account for the main share of growth within Unilever’s skincare portfolio, which includes Murad, Dermalogica, REN Clean Skincare, Kate Somerville, Living Proof, and Hourglass.) Likewise, Colgate Palmolive is finally engaging in focused acquisitions in skincare to grow its beauty portfolio and develop outside oral care.

Private equity investments are on the rise in beauty and skincare. These savvy financial investors are attracted by the high gross margins, repeat purchase trends, alternative sales channels, and the large international markets that provide additional runways for growth. Private equity was responsible for almost half of the deal activity in the Beauty sector in 2019.

The Swedish private equity firm EQT Partners (a subsidiary of the Abu Dhabi Investment Authority) led a consortium to acquire Nestle’s non-core ‘skin health’ business (rev: $2.7bn) in a deal reportedly worth $10bn. This transaction followed a fiercely competitive sales process in which private equity firms KKR, Advent International and Cinven were other high-profile suitors, as were Unilever and Colgate-Palmolive.

Premium natural cosmetics specialist L’Occitane International acquired the luxury skincare company Elemis (UK; 2018 rev: $140m) for $900m. Elemis is the leading independent British skincare brand, one with strong cross-generational consumer appeal, including the millennial demographic, but has been working to establish itself in new channels and geographies.

Coty acquired a majority 51% stake in Kylie Cosmetics (US; 2018 rev: $170m) for $600m. Kylie Cosmetics was founded by the 22-year-old ‘mega-influencer’ Kylie Jenner, who has no less than 163 million followers on Instagram. The deal makes Coty the first major strategic beauty company to buy into the influencer life. Coty plans to expand the brand geographically and into new beauty categories.

The German consumer goods group Beiersdorf (owner of Nivea) acquired the sun-care brand Coppertone (US; 2018 rev: $213m) for $550m. The deal strengthens Beiersdorf’s position in North America and “adds complementary expertise to its brand portfolio”. The company is actively seeking acquisitions and sitting on a cash pile of more than 4 billion euros.

Estée Lauder acquired full control of Have & Be Co. (KOR; 2019 rev: c. $500m), the Seoul-based skincare company behind Dr. Jart+ and men’s grooming brand Do The Right Thing. This is Estée Lauder’s first acquisition of an Asia-based beauty brand. Have & Be is growing rapidly, renowned for its leading and fast-moving innovation pipeline that offers a wide variety of high-performing skincare products that appeal to a broad range of consumers, including millennials in Asia and the US.

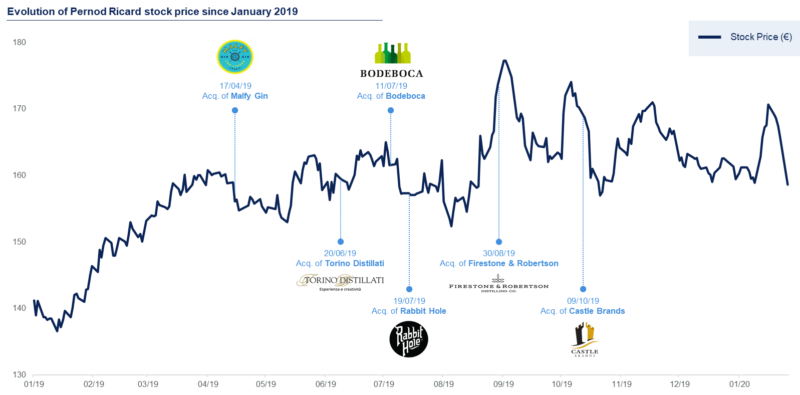

The French wine & spirits group made six key acquisitions in 2019, designed to strengthen its premium brands portfolio.

The premium segment of the Alcoholic Beverages market is forecast to grow at c. 5% CAGR between 2019 and 2023, compared to just 0.4% for ‘standard-and-below’ spirits over the same period.*

“The acquisition strategy is leveraging booming categories and reinforcing must-win, key strategic markets,” explains Pernod Ricard’s CEO Alexandre Ricard, who has made the group one of the most acquisitive in the industry.

When Alexandre Ricard became CEO of Pernod Ricard in 2015, the world’s second largest wines & spirits group was experiencing sluggish sales and the stock price was flatlining. Since then, the group’s sales have increased by c. 25% (FY19 rev: €9.2bn) and the stock price by c. 60%.

His thoughts on the premiumization trend:

“I think premiumisation is here to stay and is still by far a big value creation lever. People are trading up to higher quality brands all over the world, led by the US. People always aspire to ‘better’ and that is the story of civilisation…That is the area we want to play in. We do not see any strategic interest in the trade down part (standard and value-for-money segments). We like selling premium products that have a story.”

And on organic & external growth:

“Last year, for the first time, more than half of the world’s population had enough disposable income to be categorized as middle class. By 2030, there will be 2 billion more middle-class people in this world…People are drinking less but drinking better – and we expect the premiumization of our brands, our strong position in luxury spirits, to be one of the factors accelerating our growth.”

“From an M&A point of view, our strategy is clear and simple. Number one is to leverage dynamic categories. The gin and whisky categories and bourbon in particular. It drove us to do Smooth Ambler [acquired in 2017], TX Whiskey [acquired Firestone & Robertson Distilling Co in 2019], Rabbit Hole [acquired in 2019], and Castle Brands [acquired in 2019]…Some of these US whiskey brands are designed to stay regional, others to be national, and of course travel retail will be an opportunity for some of these to go beyond the US market…Where we see ‘demand spaces’ that we are not in, and believe we ought to be in, we will look to new products, bolt-on acquisitions or partnerships where the entrepreneur who created this new brand is still driving the business. This is what we have done with Smooth Ambler bourbon and artisanal mezcal producer Del Maguey Single Village…”

Is Nike’s ‘Zoom X Vaporfly’ the fastest running shoe on the planet?

Technological leaps in running shoes are rare, but Nike’s ‘Zoom X Vaporfly’ is a genuine game-changer in the massive EUR 13 billion running shoes market.

When the first version of the Vaporfly was launched in 2016, Nike called it “a racing shoe that breaks records”, which sounded like marketing, but it wasn’t. The shoe is literally breaking records. Too many, according to the International Association of Athletics Federations (IAAF), creating controversy within the running community and forcing the sporting goods market to innovate or face losing market share.

What’s so special about the Zoom X Vaporfly?Before the Vaporfly, little had changed in the footwear for elite marathon runners in 50 years. Previously, running shoes only had to be light and thin, and were usually constructed from thin slabs of rubber. The Vaporfly is very different: constructed with light-weight foam that is stacked high and containing a carbon fibre plate, which is the feature mentioned most prominently in Nike’s patent application. Runners say it feels like the shoe is propelling them forward, and the evidence supports this.

In 2019…

In the six world marathon majors, 31 of the 36 podium positions were won by athletes wearing Vaporfly.

Kenyan runner Eliud Kipchoge wore Vaporfly in the first marathon ever completed in under two hours, which was considered a time mark that could not be broken.

Brigid Kosgei used the Vaporfly to break the women’s world marathon record.

The New York Times conducted a study on the Vaporfly and found that it did make runners faster, by around 4%.

Following these events, and after several professional runners voiced complaints about the technology within the Vaporfly, the IAAF was forced to update its rules.

It is now prohibited to use “soles thicker than 40mm”, and to use “more than one carbon-fibre plate, or similar item, in the sole”. It means that Nike’s controversial Vaporfly range remains compliant and is permitted for use – the ‘Zoom X Vaporfly 4%’ and ‘Zoom X Vaporfly Next%’ running shoes both have a 36mm midsole. However the prototype model worn by Eliud Kipchoge to break the two-hour marathon record is now banned, as it provides too much of a performance advantage with its even chunkier sole and three carbon-fibre plates.

The new rules make sense, given that without clear restrictions, it was only a matter of time before someone developed a runner with more powerful springs, or footwear that we don’t even recognize as shoes.

“It is clear that some forms of technology would provide an athlete with assistance that runs contrary to the values of the sport.” IAAF

Running shoes is a $13 billion market that is expected to grow at a CAGR of 7% over the next five years. Nike is the clear leader, holding 51% of the market, while Asics is its biggest rival, with a 15% market share. Meanwhile, shoes account for about 47% of Nike’s total revenues, so an increasing share within a rapidly growing market will meaningfully affect Nike’s revenue growth going forward.

The stock price of Nike’s largest competitor in the running market, Asics Corp, dropped c. 10% when Kenyan runner Eliud Kipchoge became the first human to run a marathon in less than two hours. (Nike is reportedly adjusting the banned prototype design used in this race to make it competition legal before the Tokyo 2020 Olympics.)

This innovation race in running shoe design is only getting started, as Nike’s competitors have started launching high-tech running shoes of their own:

New Balance Athletic has launched a line of shoes with technical foams and carbon fibre plates that its runners can wear in Tokyo, and is “very concerned by the fact that these rules were adopted without meaningful consultation involving sporting goods industry”.

Saucony launched a new model in late 2019 called the Endorphin Pro, which Runner’s World magazine called the “closest approximation we’ve seen” to the Vaporfly.

Brooks has a new running shoe called the Hyperion Elite that goes on sale Feb. 27, according to the brand. Like Nike’s Vaporfly it is a light-weight shoe made for breaking records and includes a carbon-fibre plate sandwiched in the midsole foam to promote propulsion.

Sporting goods brands lead the pack

The global sporting goods market continues to perform exceptionally well, supported by rising levels of sports participation in both mature and emerging markets, as well as casual fashion trends (‘athleisure’). More than ever, the consumer is king and brands are finding new ways to engage with them – developing smarter omni-channel strategies and more compelling and innovative customer offers and journeys. In the M&A market there is a healthy appetite for acquisitions. Buyers are using deals to expand product portfolios (cost and distribution synergies), and to extend geographic footprints.

The sporting goods market was valued at $471bn in 2018, and is forecast to reach $627bn by 2023, growing at a 7% CAGR2017-2023.

Growth rates vary widely between different product groups. In 2018, the highest YoY rates were basketball (+11%), running (+7%), football (+7%), cycling (+6%) and gym-wear (+6%); while the largest by size were cycling ($62bn), gym-wear ($49bn), walking/hiking/camping ($39bn), and running ($33bn).

The market benefits from excellent industry fundamentals, however positioning is still key. Some of the leading strategies include growing women’s lines, outdoor, exclusivity & customization, eco-credentials, and direct-to-consumer channels.

The top 20 global players and private equity are highly acquisitive. The most active region for deal-making is Europe (c. 50% of total deals), where market consolidation is accelerating. Cross-border acquisitions are also rising, as brands look to grow their international customer bases.

There were some headline grabbing deals in 2019. Most notably, the Chinese leader Anta Sports’ (rev: $3.6bn, rising 44% YoY) acquisition of the giant Finnish sports equipment maker Amer Sports (rev: $3.2bn) – a deal that extends Anta’s overseas reach, fulfilling a core strategy to grow by acquiring international brands that complement the Chinese home market.

Trading multiples are c. 14.8x EBITDA in 2019, on average. In the European mid-market, double-digit EBITDA is ‘the new norm’.

I’m happy to share Jean Paul Agon’s thoughts on the big questions facing L’Oréal, including the rise of Digitally Native Vertical Brands, growth through acquisitions, his views on e-commerce, digital disruption, the Chinese market, and the future of beauty.

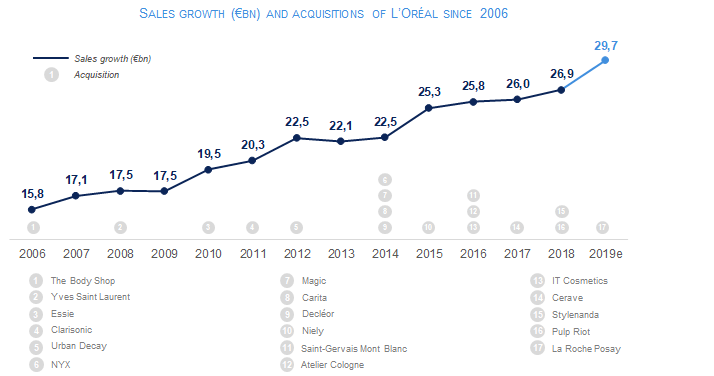

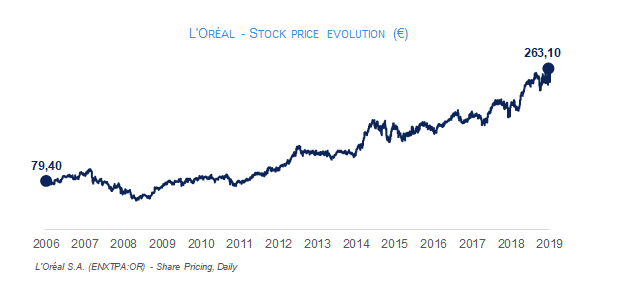

Since Jean Paul Agon became CEO of L’Oréal in 2006, revenues have grown by more than 3x and the stock price by more than 4x. According to Agon, the 112-year-old French beauty conglomerate has strengthened its position as the undisputed leader in the global beauty market due to a healthy appetite for acquisitions, as well as a robust and well balanced business model that covers all circuits, all categories, all price points and all consumers.

The below Q&A is taken from a collection of interviews conducted in 2019.

I – On M&A – growth through acquisitions:

“Our model is, and has been for 50 years, to buy a brand at an early stage because we think it can become a globally successful player. For example, we bought Kiehl’s in 2000, when the business was generating $20 million annually. It was a single store in New York City and had a few counters at Saks (department store). Then, for 20 years, we built the business and now it is a $1.37 billion business. The way we grow is exactly this combination of buy-and-grow – not buy or grow. And that’s what we do every year. Once the brands have been acquired, they are brands that we build.”

“We are looking every year at all opportunities, and we continue to do this. Make-up, skin care, hair care, hair colour – everything.”

“We currently have 35 international brands. L’Oréal is just one of them, but it’s obviously the one that we started with, and it represents around 25% of our sales. And, in fact, it’s the only brand that we didn’t buy.”

II – On e-commerce:

“There is a clear and very powerful movement towards e-commerce, which is very good, because it allows us to reach more consumers and it’s also pretty profitable.”

“E-commerce is currently about 10% of our total [global] sales, already almost three billion euros, so it’s not irrelevant. And it’s growing at 35% a year. We don’t see any slowdown in e-commerce beauty sales across the globe.”

“In China, where e-commerce is the most advanced, it’s huge – it’s more than 30% of sales.”

“With the new digital augmented services (which look at skin colour, hair colour and skin diagnosis) there is another tool to support online sales in the future.”

III – On digital disruption – in 2018, L’Oréal acquired Modiface, an ‘augmented reality’ company that digitally shows consumers the make-up they can wear. This is the first time that L’Oréal has acquired a pure tech company.

“We really believe that the future of beauty will be digital, and in this we are well ahead of the game. For us it is priority number one. In all aspects – social media, e-commerce, data, artificial intelligence. In terms of services, facilitating greater choice for consumers, helping them use products, individualizing products, etc. With digital, the possibilities become limitless. We are only scratching the surface of what will be possible.”

“Since we accelerated our digital initiatives we have seen profit margins increase, so there is a clear correlation between margin improvement and digital.”

“In the case of Modiface, the business case was obvious because this company is the best at what they do in terms of augmented reality, virtual simulation and obviously when you sell make-up, hair colour and skin care this capacity to simulate virtual reality is absolutely critical. It gives us a competitive advantage that is immense. Modiface helps all our brands to create new [augmented] services for consumers on their own sites or e-commerce sites. It is more an ROI thing, rather than a business itself.”

IV – On the future of beauty:

“The future is still about brands, more than ever. In a world of hyper choice and hyper segmentation, what consumers have on their minds in the end is brands. For example, when we acquire technology companies it’s not for business per se, it’s to serve the business.”

V – On competition from new direct-to-consumer brands on social media platforms:

“It’s true that it’s easier for new brands to enter the market because the barriers to entry have disappeared. However most, or 99.9%, of the new brands that enter the market will stay small because the barriers to scale up still exist. And on the contrary, digital is boosting the power of big brands. Our biggest brands – Lancôme, Yves Saint Laurent, Armani, Kiehl’s, L’Oréal, Maybelline – have all had their best years ever in 2019.”

VI – On China:

“We started in China in 1997, which was a bit late as many of our competitors were already there. We started in an apartment with 10 people. (I was based there then as well.) And now I’m very happy to say that we are number 1 in China and China is a major part of our growth and business.”

“China has always been about skincare, compared to the rest of the world. Most people in China use a skincare product. So, number 1, skincare is still growing in China. But the interesting news is that consumers are now also going for make-up. Previously, make-up was very small in China, and 40 years ago it was almost forbidden. And now young consumers are excited about wearing make-up. And the lucky thing for us is that younger consumers in China are starting by going directly to luxury make-up brands. In a tier 3 or tier 4 city, it’s common for teenagers to go straight to the Armani or Yves Saint Laurent counter to buy their lipstick, mascara or powder. They are starting directly with more expensive products. It’s one of the reasons for the extraordinary boom we are experiencing in China.”

VII – On sustainability and ethics:

“We are recognised as a number 1 company on sustainability. The Carbon Disclosure Project (CDP), which is the authority in terms of the environment, awarded L’Oréal for the third year in a row the ‘AAA’ recognition. ‘A’ for forest, for water and for carbon impact.”

“When I took over as CEO, I understood that ethics would be something very important for the future. Again, I decided with the team that L’Oréal should be, and could be, the number one company in ethics. If you think about it, it’s not that difficult for L’Oréal to be a great company in terms of sustainability. Also, ethics is not really a problem in our industry. And gender equality also. We could have said, ‘it’s not difficult for us, let’s do something else’. On the contrary, what we said is, ‘it’s not that difficult, so let’s be exemplary, and be number one in the world’.”

[In 2019, L’Oréal was named for the 10th time as one of the World’s Most Ethical Companies. The Covalence ESG (Ethical Quote reputation index) also awarded L’Oréal the #1 ranking out of 581 of the largest listed companies worldwide.]

VIII – On the key shareholders of L’Oréal:

“We have two great shareholders – the Bettencourt family, who own 33% of the shares; and Nestle, with 23% of the shares. These large investors give us the possibility to think really long term, to be very strategic, and I think that it’s also part of the success of L’Oréal.”

A recent survey by the brand-tracking group YPulse asked 60,000 Millennial and Gen Z consumers in the US which fashion brands they think are “hot” right now. The results highlight how the ‘athleisure’ trend has made some sports brands “hot fashion brands” in their own right.

• Clothes are a major theme among young consumers: 43% of 13-36-year-olds choose to buy clothes/accessories when they treat themselves.

• Young consumers are shopping online but also looking for in-store experiences to connect to brands.

• 95% of Millennials are active and 30% see themselves as core athletes (3x the US population).*

• Millennials value outdoor sports, where discovery and challenges prevail.

• Gen Z’ers see sports as a holistic wellness routine and a meritocracy symbol. These digital-natives enjoy using sports apps to add fun and share data (eg. burnt calories, distance travelled, speed). One Gen Z’er out of 3 shares content from a fitness app at least once a week.

• Brands are delivering youth-focused sportswear with an emphasis on design and comfort – performance shoe sales have dropped in favour of trendy athleisure footwear.

• Skateboarding has become the leader in streetwear designs for Gen Z’ers, which is impacting sneaker sales: six years ago, basketball sneakers accounted for 13% of US sales; today, they are down to 4%.* Skate brands such as Supreme and Vans are capitalizing on this youth athleisure trend.

*Millennials are defined as those people born between 1981 and 1996, according to the Pew Research Center. Gen Z shoppers are typically referred to as those consumers born thereafter.

*YPulse’s 2019 youth brand tracker measures young consumers’ relationships with brands based on a weighted 6-point scale, ranging from “Never heard of this brand” to “This brand is one of my favourites.” The survey asked respondents “Which of the following are hot right now?”

*Source: NPD Group research

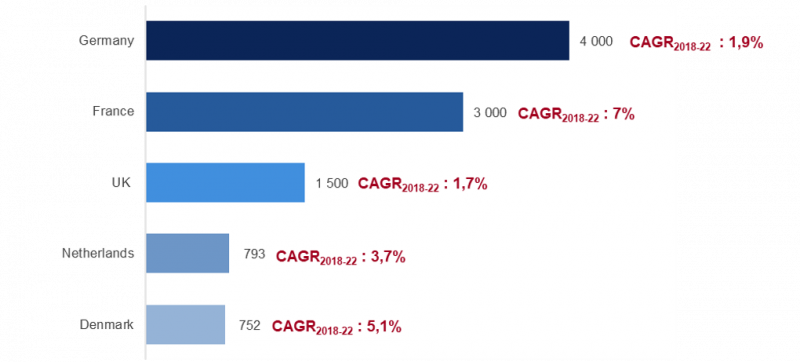

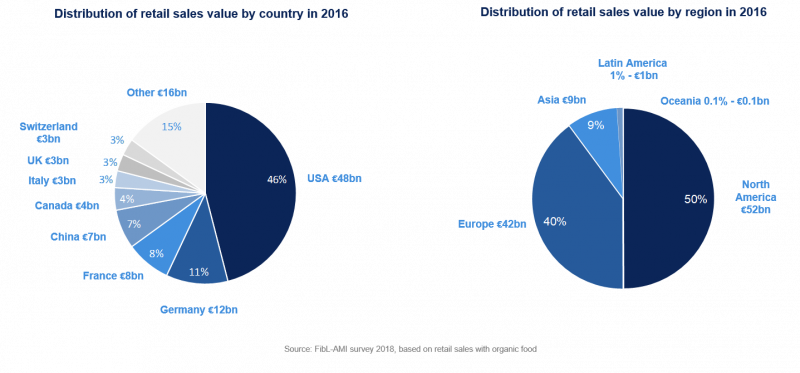

The global consumer organic packaged food & beverage market is worth around €38.4 billion, and continues to grow strongly across the globe, at a CAGR2017-2021 of 15%.*

Here in Western Europe growth varies widely: France is the 3rd largest market in the world and forecast to grow at a much faster rate than the European average, at a CAGR2018-2022 of 7%.*

We are seeing the entire value chain (farmers, industrial producers, processors and retailers) reposition for future growth. We are also seeing more opportunities for M&A – to tap growth and consolidate this fragmented market.

ORGANIC PACKAGED FOOD & BEVERAGES (MARKET WORTH in €m)

Rising lifestyle diseases such as diabetes and obesity are making people more health conscious.

Millennials are generally more health conscious, and driving sales growth as they mature and earn higher incomes.

Social media continues to raise awareness; and the rise of ‘influencers’, whose preferences also tend to be organic.

Upstream innovations are improving efficiencies and production rates – eg. automation (robots) are supporting farmers without the need for chemicals.

Rising disposable incomes in mature and emerging markets.

DISTRIBUTION OF ORGANIC RETAIL SALES BY GEOGRAPHY

Worldwide net sales of all organic food amounts to c. $110 billion. (Note: this includes the entire organic food market including raw fruit & veg, etc.)

FRENCH MARKET

*France is the EU’s largest agricultural producing country, while its organic food & beverage market is already the third largest in the world, worth c. US$3.1bn in 2017.

*The organic farming market grew by a massive 17% in 2017, reaching €8.3bn, according to the French Agency for the Development and Promotion of Organic Agriculture. At the end of 2017, there were a total of 36,691 organic farmers in France, up 14.7% on the previous year, representing 8.3% of all French farms and 6.6% of total cultivated areas. In 10 years, areas producing organic has more than tripled, from 517,000 hectares to 1.78 million hectares.

*And yet, in 2017, domestic production couldn’t keep up: organic food imports grew in 2016 and 2017 for the first time since 2009, accounting for almost one-third of the organic food consumed in France, according to a Coface study.

*The major supermarket chains are rapidly expanding their organic offerings: Lidl recently introduced a line of 40 organic products; and Carrefour is now opening dedicated organic outlets in cities outside Paris, where it already has 10; and speeding up its creation of a range of everyday “French organic” products sold under its Carrefour Bio brand. Carrefour France generated revenues of €1.2 billion from sales of organic products in 2017 (compared with total revenues of €35 billion). The aim is to increase this figure two-fold between now and 2022, with the emphasis on increasing sales of organic products made in France.

*Sustainable farming is taken extremely seriously in France. For example, the country has forbidden the growth of GMO foods since 2008; and recently took a radical step towards protecting its dwindling bee population by becoming the first country in Europe to ban all five pesticides researchers believe are killing off the insects – the EU only voted to outlaw the use of three of them in crop fields. France also has many historic quality labels, such as Label Rouge, which ensures that animals are raised according to strict dietary and humane standards including access to the outdoors. Label Rouge beef is grass-fed, and Label Rouge veal and lamb are allowed to consume milk for a longer period of time before being weaned. This label also forbids the use of antibiotics and growth hormones, and medical treatments of animals bearing the label are kept to a strict minimum.

A FRAGMENTED MARKET RIPE FOR DEALMAKING

In France, the competitive landscape is widely fragmented and also highly competitive, led by a small number of large Food & Agro groups, and increasingly private equity funds. These larger players are interested in making acquisitions that consolidate the market and provide growth opportunities to ‘buy & build’ innovative organic concepts.

We have seen some interesting deals emerge in the French organic retail market over the past 12 months.

April 2019: PAI Partners and investor Charles Jobson agree to acquire 100% of Koninklijke Wessanen (2018 rev: €628m) – the Dutch leader in healthy, organic and sustainable products. The investors will support management’s existing strategy, including upgrading operations to improve efficiencies across the entire value chain of the business, and adding scale in core categories and markets through acquisitions. “Our vision is to build a European leader in organic and sustainable food,” explains Christophe Barnouin, CEO of Wessanen. “We want to remain at the forefront of making food healthier and more sustainable for the benefit of both consumers and the planet. It is all the more critical in an era where organic, sustainable and healthy themes have grown increasingly popular, which in turn has resulted in a more competitive environment.”

December 2018: The Japanese food distribution giant Aeon takes a 20% stake in the French bio store chain Bio c’Bon (2018 rev: €150m), which is owned by the French private equity house Marne & Finance. The chain currently operates 154 outlets, of which 64 are in the Paris region and 33 are abroad. Together the owners plan to open 50 additional stores in Japan within five years; and to develop a new warehouse of 12,500 m² in Athis-Mons (Essonne), combining the logistics of three initial sites and adding a laboratory for the production of prepared meals.

September, 2018: The agricultural group InVivo acquires Bio & Co, a chain of six organic food stores in southern France, with annual sales of €22m. InVivo aims to have 150 Bio & Co food stores by 2025, as it looks to expand its retail business in the high growth organic segment. Most of the additional Bio & Co stores will be located next to InVivo’s existing gardening centers/ stores, which it believes is a complementary customer offering. The investment is also designed to support the handful of grocery outlets selling local products that InVivo has been trialling in the past two years under the brand, Frais d’Ici.

March, 2017: The French private equity house Ardian acquires a majority stake in the French grocery chain Grand Frais. Grand Frais has earned itself the title of ‘category killer’ in the grocery retail business by focusing on quality fresh food at affordable prices, of which organic is a large part. Based in Lyon, the specialist retail concept has grown exceptionally well, with 15-25 new openings a year. The business currently has 185 stores, and an annual turnover of c. €1.1 billion. Grand Frais’s stores are located mainly on the outskirts of major cities and tend to be large, covering an average area of c. 1,000 sqm – a traditional indoor covered market, selling fruit & vegetables, dairy, fish and meat, as well as specialized grocery items. Suppliers are usually local and specialized.

*Source: Sprout Intelligence, 2017

The leading Chinese sporting goods brand Anta Sports (FY2018 rev: €545m, rising 44% YoY) acquires the giant Finnish sports equipment maker Amer Sports (FY2018 rev: €2,7bn), in a deal valued at c. €4.6bn. This transaction is backed by an international buyout consortium and is expected to be completed by Q2/2019. Under the deal, Anta acquires 58% of Amer, while other investors in the consortium are reported to include the Hong Kong-based private equity fund FountainVest (21.3%) and the Canadian billionaire Chip Wilson, founder of yoga apparel company Lululemon (20.6%).

Amer Sports: A Finnish sporting goods company listed on the Nasdaq Helsinki stock exchange with a number of leading brands, including Salomon, Arc’teryx, Peak Performance, Atomic, Mavic, Suunto, Wilson and Precor. Founded in 1950, the company began life as a tobacco manufacturer & distributor, but has since evolved into a multinational company devoted to the production of sporting goods. The Group’s business is balanced by its broad product portfolio, as well as by a presence in all major global markets.

Anta Sports: China’s largest sporting goods brand (and the third-largest in the world by market capitalization, after Nike and Adidas). Its high-growth brand ‘Anta’ focuses on athletic footwear & apparel products, catering to lower and middle-income groups. In addition, Anta Sports is a leading sports retailer in China, with 11,316+ brick & mortar stores. The company is pursuing a multi-brand and onmi-channel strategy – broadening its customer base through acquisitions of high-end international sportswear brands that leverage sales in its home markets.

Deal delivers:

Extends Anta’s overseas reach, fulfilling a core strategy to grow by acquiring established international brands that complement the Chinese home market: 43% of Amer’s sales are in EMEA, 43% in the Americas, but just 14% in Asia Pacific.

Expands Anta’s scale in a bid to challenge the market leaders Nike & Adidas, both in its home market and also internationally (there are plans to launch the Anta brand in Europe in 2019).

Enables Anta to diversify and expand market share in a number of new categories, such as ball sports (Wilson, DeMarini, Louisville Slugger), winter sports (Atomic, Armada Skis), sports instruments (Suunto), and cycling (Mavic, ENVE Composites). These segment-leading brands offer synergies.

Distribution scale in the Chinese market, where Anta has 11,316 retail stores and a large portfolio of brands positioned across the mass market to high-end market spectrum. Amer has already enjoyed strong growth in China over the last five years – its sales there have grown at CAGR5YR of 29%, and represented 6% of sales in 2018.

Reduces debt: the consortium will pay down EUR1 billion euros in debt from Amer Sports.

“Through our multi-brand strategy, we aspire to become a competitive, global, multi-brand company with newly added brands. To that end, we are launching our globalization strategy in 2018. Through product innovation and R&D investment. We will tap into the global market with our best brands.” Ding Shizhong, Anta’s chairman and CEO.

Deze week vond op 10 april de 9e editie van het Voedingsbodem voor Groei! Een vruchtbare samenwerking tussen ZLTO, Investec, ABN-Amro en PwC. Het event vond voor het eerst plaats op een externe locatie namelijk in Eersel op de inspirerende Venco Campus van Vencomatic Group.

Het event stond in het teken van de trend van gezond en vers voedsel in combinatie met gemak voor de eindklant. Hierbij stond innovatie in productie, het vermarkten en kennis van je klant centraal. De vraag was dus hoe te innoveren?

Op het event werd er gesproken door:

Lotte van de Ven: CEO Vencomatic: Innoveren in een traditionele sector

Jos van Mil: Managing Partner product- en marktinnovatie bij Greenco – De innovatiemotor

Tim Hehenkamp: Executive Director Data & Personalisation bij Jumbo – Dé klant bestaat niet

Na afloop van het inhoudelijke programma is er onder het genot van een hapje en een drankje nagepraat over de ervaringen van de middag. Een mooie afsluiting van een inspirerende en verbindende middag.

Was je verhinderd en nieuwsgierig naar het event ‘Voedingsbodem voor Groei’, neem dan gerust contact op met een van de organiserende partijen of stuur een e-mail naar info@voedingsbodemvoorgroei.nl. We komen graag met u in verbinding! Komend jaar staat immers onze 10e editie op het programma.

Selling non-core businesses – How to optimize value creation?

Key takeaways from our report:

Create value

Research shows that businesses that engage in regular divestitures create significant shareholder value down the road. Actively pruning the business portfolio reduces complexity, sharpens the operational focus and generates cash for the next phase of growth. Also note that a pure play is easier for investors to understand.

Transformation

Most businesses are set up to buy assets, not sell them, which means decisions to sell are often made at the wrong time or in the wrong manner. The key is to avoid ad-hoc or reactive decisions, and to carefully manage and prepare the planned divestiture so that it supports the company’s core strategy. Don’t let emotions get in the way. View divesting as a strategic tool.

Plan & prepare We are seeing higher valuation multiples and faster closings for assets that have been properly prepared – ie. made attractive to potential acquirers. This means setting up a control centre so the process is run professionally and systematically. Communicate clearly, promptly, and frequently: inform shareholders and employees about the divestiture early on, and keep them informed as it progresses.

Target the right buyers Identifying buyers usually means hiring the right advisors with exposure to the best-owner universe – serious, credible and with genuine sector expertise. Tell a clear and compelling business story. Explain the growth opportunity, the assets’ capabilities, and tailor the potential synergies for investors.

Sell at the right time Work out what drives the industry cycle, and time the divestiture to optimize the valuation. For companies, now is an ideal time to consider a sale because valuation multiples are at historically high levels in the mid-market and buyers are acquisitive and sitting on large war chests of cash. Also, the decision to divest needs to be proactive rather than reactive. Executives often hesitate to sell assets, which is leaving a lot of value on the table.

When Alexandre Ricard became CEO of Pernod Ricard in 2015, the world’s second largest wines & spirits group was experiencing sluggish sales and the stock price was flatlining. Since then, the group’s sales have increased by c. 25% (FY19 rev: €9.2bn) and the stock price by c. 60%.

When Alexandre Ricard became CEO of Pernod Ricard in 2015, the world’s second largest wines & spirits group was experiencing sluggish sales and the stock price was flatlining. Since then, the group’s sales have increased by c. 25% (FY19 rev: €9.2bn) and the stock price by c. 60%.

December 2018: The Japanese food distribution giant Aeon takes a 20% stake in the French bio store chain Bio c’Bon (2018 rev: €150m), which is owned by the French private equity house Marne & Finance. The chain currently operates 154 outlets, of which 64 are in the Paris region and 33 are abroad. Together the owners plan to open 50 additional stores in Japan within five years; and to develop a new warehouse of 12,500 m² in Athis-Mons (Essonne), combining the logistics of three initial sites and adding a laboratory for the production of prepared meals.

December 2018: The Japanese food distribution giant Aeon takes a 20% stake in the French bio store chain Bio c’Bon (2018 rev: €150m), which is owned by the French private equity house Marne & Finance. The chain currently operates 154 outlets, of which 64 are in the Paris region and 33 are abroad. Together the owners plan to open 50 additional stores in Japan within five years; and to develop a new warehouse of 12,500 m² in Athis-Mons (Essonne), combining the logistics of three initial sites and adding a laboratory for the production of prepared meals. March, 2017: The French private equity house Ardian acquires a majority stake in the French grocery chain Grand Frais. Grand Frais has earned itself the title of ‘category killer’ in the grocery retail business by focusing on quality fresh food at affordable prices, of which organic is a large part. Based in Lyon, the specialist retail concept has grown exceptionally well, with 15-25 new openings a year. The business currently has 185 stores, and an annual turnover of c. €1.1 billion. Grand Frais’s stores are located mainly on the outskirts of major cities and tend to be large, covering an average area of c. 1,000 sqm – a traditional indoor covered market, selling fruit & vegetables, dairy, fish and meat, as well as specialized grocery items. Suppliers are usually local and specialized.

March, 2017: The French private equity house Ardian acquires a majority stake in the French grocery chain Grand Frais. Grand Frais has earned itself the title of ‘category killer’ in the grocery retail business by focusing on quality fresh food at affordable prices, of which organic is a large part. Based in Lyon, the specialist retail concept has grown exceptionally well, with 15-25 new openings a year. The business currently has 185 stores, and an annual turnover of c. €1.1 billion. Grand Frais’s stores are located mainly on the outskirts of major cities and tend to be large, covering an average area of c. 1,000 sqm – a traditional indoor covered market, selling fruit & vegetables, dairy, fish and meat, as well as specialized grocery items. Suppliers are usually local and specialized.