29 Apr 2026

The Perfect Blend: Unlocking New Demand in Beverages

Shifting consumer behaviours, category innovation and strategic repositioning are creating new growth opportunities across the European beverage market.

Those themes were at the centre of Investec’s and OC&C’s recent beverage sector conference in Haarlem, the Netherlands, where 40 senior leaders from alcoholic and non-alcoholic beverage companies gathered alongside a select group of private equity investors with portfolio exposure to the sector.

Hosted at brewery Jopenkerk, the event brought together macroeconomic, strategic and operational perspectives to examine where value creation is emerging in an increasingly competitive market.

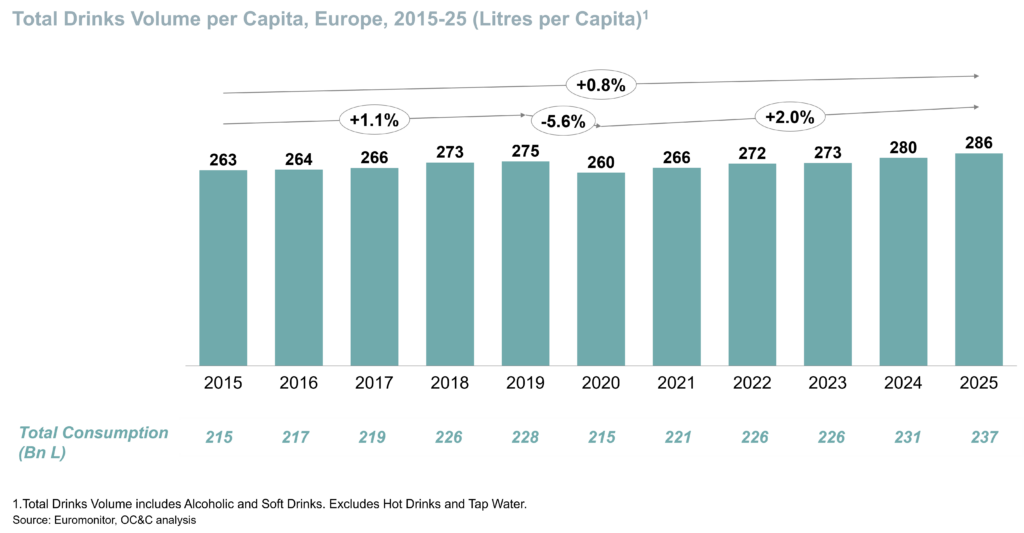

Resilient demand, evolving behaviours

While the broader economic backdrop remains mixed, beverages continue to demonstrate resilience as a consumer category. Repeat purchasing habits, frequent consumption occasions and strong brand loyalty have historically supported demand through periods of pressure.

Philip Shaw outlined how inflation, energy costs and geopolitical uncertainty continue to shape household budgets and corporate planning. Even so, beverage demand has remained comparatively durable. For operators across the value chain, resilience alone is no longer enough. Agility in pricing, portfolio management and route-to-market execution is becoming increasingly important.

Growth is becoming more selective

Headline market growth across Europe has been modest in recent years, but performance beneath the surface is diverging sharply.

Dan Zubaida highlighted that some of the strongest momentum is now concentrated in categories aligned with changing consumer preferences: functional drinks, hydration, low- and no-alcohol alternatives, convenience-led formats and premium propositions with clear brand identities.

At the same time, more traditional segments face slower growth and greater competitive intensity. The result is a more polarised market, where targeted positioning matters more than broad category exposure.

For management teams and investors alike, the opportunity increasingly lies in identifying specific pockets of structural growth rather than relying on the market to rise uniformly.

Brand strength still drives outperformance

As innovation accelerates and shelf space becomes more contested, brand clarity is becoming a more important source of advantage.

Examples discussed during the event showed that outperforming brands often combine a clear consumer proposition with disciplined execution: strong flavour credentials, wellness relevance, effective new product development, compelling marketing and smart channel strategy.

In categories where barriers to entry are lower and challenger brands can scale quickly, sustained success depends not simply on launching new products, but on building brands with repeat purchase potential and retailer relevance.

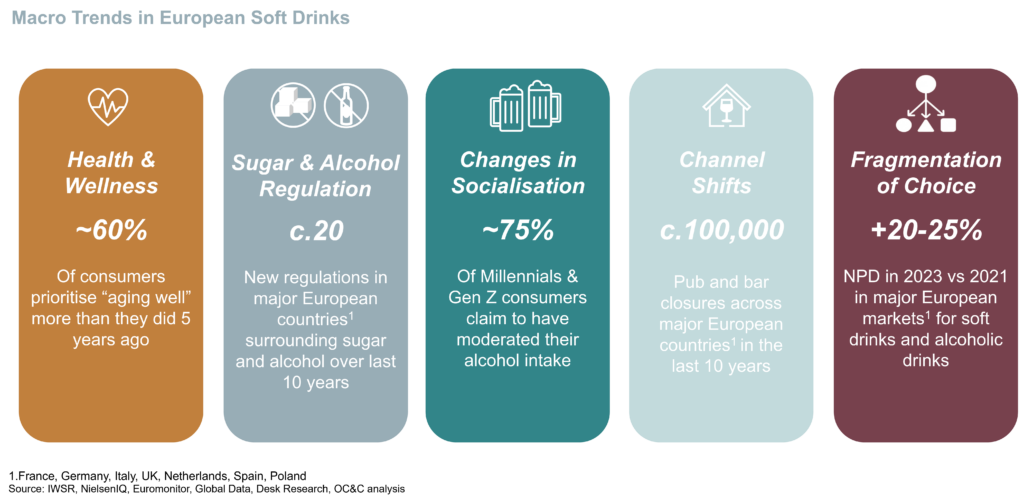

Moderation is creating new occasions

One of the liveliest discussions focused on changing alcohol consumption habits, particularly among younger consumers.

Moderation trends are reshaping demand patterns, with many consumers seeking balance rather than abstention. That is supporting growth in alcohol-free beer, adult soft drinks, functional beverages and products designed for social occasions without alcohol.

Rather than representing a simple substitution trend, no- and low-alcohol categories may also expand total consumption occasions by creating new use cases across weekday, wellness-led and mixed-group social settings.

For alcohol and soft drinks players alike, the continued blurring of category boundaries is opening new strategic options.

Health trends and the GLP-1 effect

The impact of GLP-1 medications, including popular weight-management treatments, on the drinks market was another lively topic.

Participants noted that in the near term beverage companies are capturing demand through adjacent “companion” categories such as protein-led products, hydration, reduced-sugar offerings and functional wellness beverages aligned with evolving consumer health priorities and preferences.

Attendees discussed whether innovation in beverage-based GLP-1 delivery formats may, over time, create new adjacent growth opportunities. While still an emerging theme and subject to regulatory and commercial developments, the discussion highlighted how external health trends can influence long-term portfolio strategy and product innovation across the sector.

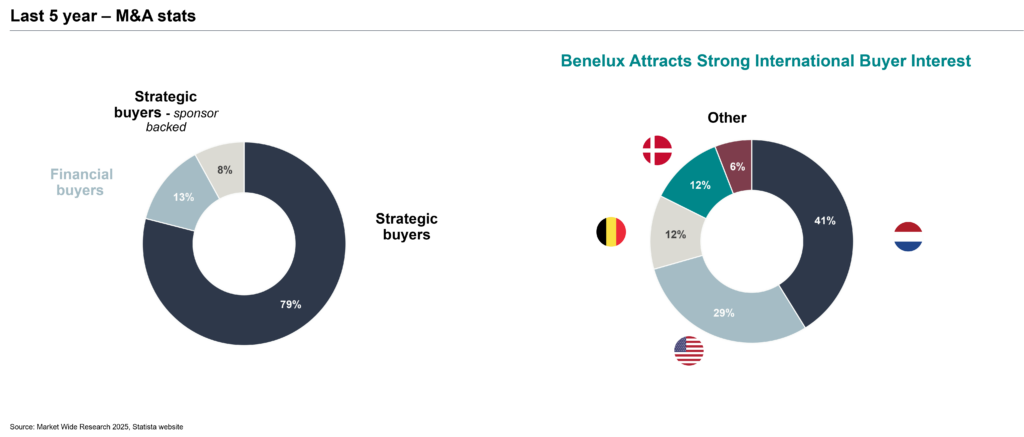

Scale, M&A and geographic expansion remain key levers

Audience polling during the event revealed the priorities currently shaping boardroom agendas. Product innovation was identified as the most critical growth lever by 39% of attendees, followed by geographic expansion at 32% and M&A at 25%.

Those responses reflect a market in which many companies are balancing organic growth initiatives with selective inorganic opportunities. Acquisitions can accelerate entry into faster-growing niches, while international expansion offers access to new consumer pools beyond domestic markets.

With the European drinks market still fragmented across many subsegments, consolidation is likely to remain an important theme.

Execution still separates winners from the rest

Drawing on A.G. Barr’s experience, Euan Sutherland discussed how growth ultimately depends on consistent execution across commercial, operational and innovation priorities.

That includes investing behind core brands, expanding into adjacent categories, improving channel penetration and maintaining the supply chain capacity needed to support growth. In a market where consumer preferences can shift quickly, pace and adaptability are increasingly valuable capabilities. Strategy creates direction, but execution creates value.

Outlook

The European beverage market remains attractive, but growth is becoming more selective. Companies that can align portfolios to changing consumer needs, build distinctive brands and deploy capital with discipline are likely to outperform.

For investors and corporates, the next wave of value creation may come less from market growth alone, and more from backing the categories, capabilities and brands best positioned to capture changing demand.

Event Gallery