Investec is proud to announce that our French team is awarded as one of the Best Investment Bank – LBO Small to Mid Cap with a Silver Award at the recent Sommet des Leaders de la Finance in Paris.

Organised by Décideurs Corporate Finance, this event recognises excellence in corporate finance and highlights the work of professionals who lead complex and strategic transactions.

We warmly thank our teams for their dedication, and our clients for their continued trust.

We are pleased to present the latest edition of our transaction and valuation update on the food and beverage sector.

With over 300 professionals and ~150 transactions worldwide in the last two years, we have a very good overview of the transaction market, valuations and relevant buyer interest in the food & beverage sector.

For the second half of 2025, we expect a further increase in transaction activity as well as rising valuations, as market participants have largely adapted to supply chain challenges and inflationary pressures.

We recently appeared on the M&A podcast “CLOSE THE DEAL” (a German language format) to discuss the topic of M&A in the food & beverage industry and key considerations for maximizing valuations in a sales process. Click here to listen

Do you have questions regarding M&A or (growth) financing?

We would be happy to schedule a call to discuss further.

Click here to download the report.

The Rheingau Music Festival is one of the largest music festivals in Europe and organises over 170 concerts every year throughout the region from Frankfurt and Wiesbaden to the Middle Rhine Valley.

Unique cultural monuments such as Eberbach Monastery, Johannisberg Castle, Vollrads Castle or the Wiesbaden Kurhaus as well as picturesque vineyards are transformed every summer into concert stages for stars of the international classical music scene and interesting up-and-coming artists from classical music and jazz to cabaret and world music.

In over 30 years, the Rheingau and its festival have become a centre of attraction for music enthusiasts from all over the world in a unique interplay of culture and nature, music, enjoyment and joie de vivre.

Investec is delighted once again to sponsor the Rheingau Music Festival 2024 and invites you to join us from 22 June to 7 September 2024!

A special feature this year? For the first time, there will be two opening concerts: Traditionally, the festival opens in the Eberbach Monastery, followed by another opening concert in the Kurhaus Wiesbaden. This year’s focus artists are also particularly outstanding: violinist Christian Tetzlaff, cellist Anastasia Kobekina, pianist Bruce Liu and jazz saxophonist Candy Dulfer.

Once again this year, various themes and focuses will ensure a varied and exciting programme. Under the motto “Spot on: Hollywood”, the world of film music comes to life in twelve concerts. Under the motto “Brazil!”, the contrasts and beauties of the country will be explored musically. The programme is also dedicated to the works of Antonín Dvořák and a true classic: Vivaldi’s “Four Seasons”.

The stages of the 37th festival season will be graced by numerous stars from the worlds of classical and pop music. Highlights include star pianist Lang Lang, singers Álvaro Soler, Max Mutzke and Max Giesinger, violinist Anne-Sophie Mutter, opera singer Rolando Villazón and entertainer Eckart von Hirschhausen.

Investec has been a committed sponsor of the Rheingau Music Festival for more than 15 years. This long-standing partnership is characterised by our deep appreciation for the arts and a strong connection to local culture. We look forward to experiencing a rousing summer full of music together with you again this year.

You can view the detailed program here.

Ook dit jaar organiseerde Investec samen met ABN Amro en PwC de 14e editie van het inspirerende voedselevenement: Voedingsbodem voor Groei. Het evenement vond plaats op de prachtige externe locatie VRIJ in Culemborg waar dagvoorzitter Joost Hoebink de groep ondernemers, CEO’s en CFO’s binnen de Nederlandse Food & Agro sector enthousiast ontving.

Het evenement draaide om ‘impactful sourcing’ in een instabiele en onrustige wereld. Centrale thema’s waren hoe de voedselvoorziening in tijden van geopolitieke onrust en klimaatverandering te waarborgen en wat de voor- en nadalen zijn van lokale versus wereldwijde sourcing. Daarnaast werd ook ingegaan op de vraag hoe we de voedselketen transparanter en duurzamer kunnen maken.

Externe sprekers van gerenommeerde bedrijven gaven stof tot nadenken:

Louise van Schaik (Head of Unit EU & Global Affairs bij Clingendael) deelde een inzicht dat ons allen raakte:

‘De geopolitieke situatie waar we ons nu in bevinden zorgt voor de-globalisering en dat maakt handelsstromen extra kwetsbaar.” Ze voegde eraan toe: “De huidige geopolitieke onrust leidt tot protectionisme met als gevolg dat landen zoals China en ook de EU nadenken hoe zij hun eigen voedselzekerheid binnen de landsgrenzen kunnen borgen.

Volkert Engelsman (oprichter van Eosta) benadrukte het belang van netjes rekenen. Hij legde uit dat in de nieuwe economie winst pas echt winst is als de planeet en samenleving ook winnen. Dat is straks voorwaarde om te kunnen voldoen aan de verwachtingen van je accountant (CSRD), bank (klimaat- en biodiversiteit stresstests), klant, NGO’s en overige stakeholders.

‘Niks mis met winst maar dan wel netjes rekenen en de maatschappelijke kosten niet stiekem afwentelen op de belastingbetaler of toekomstige generaties.’

Nadia Menkveld (sectoreconoom bij ABN AMRO) herinnerde ons aan de kwetsbaarheid van onze voedingsindustrie in het licht van klimaatverandering:

Onze voedingsindustrie is kwetsbaar voor klimaatverandering.

Na het officiële programma was er ruimte voor een informele borrel, inclusief vegan & organic bites en het socializen met branchegenoten – een zinvolle afsluiting van een inspirerende dag.

Als je er niet bij kon zijn, maar wel nieuwsgierig bent naar het evenement, neem dan contact op met Jasper Erhardt voor meer informatie of voor het evenement van volgend jaar.

Interview

As we enter 2024, the M&A landscape shows signs of recovery, albeit cautiously.

In the episode of the February 20, 2024 of No Ordinary Wednesday, Jeremy Maggs in conversation with Investec experts Jürgen Schwarz, Marleen Vermeer, and Kilian de Gourcuff, Investec’s Head of Cross-Border Finance and International Advisory Charles Barlow, on what key sectors, trends and risks to keep an eye on in 2024.

Click below to listen to the podcast:

Where does opportunity lie for dealmaking in 2024? (investec.com)

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Listen to the best of No Ordinary Wednesday: https://www.investec.com/en_za/focus/no-ordinary-wednesday-with-jeremy-maggs.html

Financial restructuring for Shareholders & Lenders

Helping clients to navigate uncertainties while putting their businesses back on track

Interview with Jürgen Schwarz, Managing Partner of Investec about Restructuring with the help of a M&A process:

- How did the market change in recent years?

- What is your approach?

- Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

Sale from insolvency

Due to our pan-European presence and track record we are well placed to advise on international and cross-border restructurings.

Our international sector teams implement more than 50 transactions p.a. and in many sectors they know the active buyers, the acquisition criteria, the behaviour of individual decision makers. We also have an up-to-date overview of the market prices paid, which vary considerably over time and depending on the positioning in the sector.

Investec has direct access to numerous international equity and debt capital providers and has carried out numerous restructurings ranging from approximately 10 million Euros to several billion Euros.

Financiering en markttrends | 2023

Waarom de Duitse industrie grote behoefte heeft aan investeringen.

De Duitse industrie staat voor grote uitdagingen, waaronder de effecten van digitalisering, de verschuiving van analoge naar digitale bedrijfsmodellen, de behoefte aan milieubeschermende maatregelen en duurzame productieprocessen, evenals demografische veranderingen, die leiden tot een tekort aan geschoolde werknemers en een vergrijzende beroepsbevolking. Om deze processen succesvol te beheersen, zijn aanzienlijk hogere investeringsinspanningen nodig dan in het verleden.

Digitalisering en Industrie 4.0: Op dit moment staat Duitsland op zijn best in de middenmoot van de EU wat betreft het gebruik van digitale technologieën in de economie1. De Duitse industrie moet investeren in digitale technologieën en automatisering om concurrerend te blijven. Maar om de achterstand op vergelijkbare landen in te lopen, zouden de investeringen in IT en digitalisering in Duitsland moeten verdubbelen of verdrievoudigen van 49 miljard euro naar 100 tot 150 miljard euro per jaar. Alleen al in het mkb zouden de uitgaven voor digitalisering moeten stijgen van 18 miljard euro in 2019 naar 35 tot 50 miljard euro per jaar.

Duurzaamheid en milieubescherming: Bedrijven richten zich steeds meer op milieuvriendelijke technologieën en processen om hun duurzaamheidsdoelstellingen te halen en hun impact op het milieu te verminderen. Deze investeringen dienen niet alleen om het milieu te beschermen, maar dragen ook bij aan het concurrentievermogen op lange termijn. Een recente studie in opdracht van KfW schat de klimaatbeschermingsinvesteringen die nodig zijn om de doelstelling van klimaatneutraliteit tegen 2050 te bereiken op ongeveer 5 biljoen euro of ongeveer 190 miljard euro per jaar1. Dit enorme bedrag maakt duidelijk dat er aanzienlijk grotere inspanningen nodig zullen zijn om de doelstelling te halen dan tot nu toe het geval is geweest.

Lees de volledige insight hier.

Thorsten Gladiator, Managing Partner Investec: As corporate finance advisors, we see the importance of ESG in general and sustainability aspects in particular in almost every transaction, both in M&A situations and in financing mandates.

Equity and debt investors place a strong focus on ESG compliant investments in the interest of their financiers and / or due to investment criteria that are binding for them.

For business sellers as well as CFOs, this has pricing and process consequences:

- A clearly defined and documented ESG strategy creates confidence among investors and the company’s other stakeholders

- The same applies to the (early) implementation of legal requirements for sustainability reporting (CSRD)

- A focus on sustainability aspects provides positive differentiation features compared to competitors and can thus have a value-creating effect

- The lack of a corresponding strategy can lead to price discounts in the valuation as well as higher financing costs

- In the due diligence phase of a transaction, lack of ESG information leads to prolonged processes, higher management burden and the withdrawal of investors with clearly defined ESG investment criteria

The following article from AIM – Advice in Motion highlights the various aspects for medium-sized companies and shows examples of successful ESG strategies.

Opportunities and challenges of sustainability for smaller and medium-sized enterprises

The sustainability performance of a company today is the decisive factor for its competitiveness tomorrow. In this context, medium-sized companies in Germany in particular are faced with tasks whose extent has not yet been fully recognized in many cases and which involve major challenges in terms of resources, time and expertise.

Even though sustainability is a ubiquitous and much-discussed topic that is omnipresent both in the media and in public debate, it is by no means a new issue. Rather, sustainability has a long and exciting history that spans centuries and has been shaped by various actors and concepts.

Where do the roots of sustainability lie?

As far back as the Middle Ages, the moral ideal of the honorable merchant played a decisive role in promoting sustainable principles. Many a family entrepreneur rightly sees himself or herself in the tradition of the honorable merchant and aligns his or her business conduct with principles such as honesty, responsibility and sustainability.

In the 18th century, the Saxon chief miner Carl von Carlowitz coined the term sustainability in his work “Sylvicultura Oeconomica.” He introduced the idea that forest resources should be managed sustainably by cutting only as much wood as can naturally grow back. What was interesting about Carlowitz’s concept of sustainability was that sustained yield was precisely not antithetical to sustainability. Rather, forestry yield acted as the cornerstone for this oft-cited source of the concept of sustainability. The mining area of the Erzgebirge was simply dependent on the sustainable use of wood for construction, mining and smelting purposes.

Another significant milestone in the development of sustainability was the Brundtland Report, published in 1987 under the title “Our Common Future”. The report defined sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” Here, sustainability clearly went beyond a purely economic consideration. The report emphasized the need to integrate economic, social and environmental aspects to create a sustainable future.

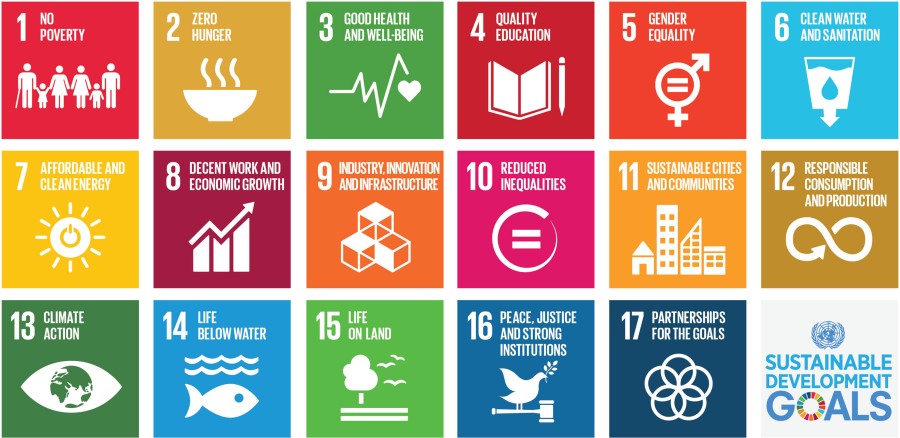

Since then, the understanding of sustainability has evolved to encompass a variety of dimensions. One key concept is ESG (environmental, social, governance) criteria, which encompass environmental, social and governance-related factors. Differentiation of individual sustainable development goals is achieved through the United Nations Sustainable Development Goals (SDGs), which were adopted in 2015. The SDGs include 17 global goals to promote sustainable development at the economic, social and environmental levels by 2030. These goals range from poverty reduction, health, education and gender equality to renewable energy and sustainable cities.

The SDGs are an excellent framework for linking the principle of sustainability with economic, ecological and social development and provide a suitable orientation framework for a company’s sustainability strategy:

- SDGs as guidelines for sustainable management

- Alignment of products and services with the SDGs

- Business activities can contribute directly to achieving the SDGs

Nowadays, at the current edge of development trends around sustainability, so to speak, ESG expression is thus considered a leitmotif and fundamental approach for responsible and sustainable development. It is about combining economic, social and ecological aspects in order to create a world worth living in for present and future generations.

The individual SDGs are suitable targets for integrating ESG into corporate strategies, as they are more concrete and easier to measure using indicators than the more fundamental ESG concept.

Importance of the midmarket

As the backbone of the economy, the SME sector comprises a large number of companies that operate both regionally and internationally. It is of great importance for economic performance and employment in the country. Around 2.5 million companies in Germany belong to the Mittelstand, in the definition of a small and medium-sized enterprise (SME). These range from microenterprises to medium-sized companies with up to 250 employees, which generate around one-third of total sales for Germany and employ more than half of all employees.

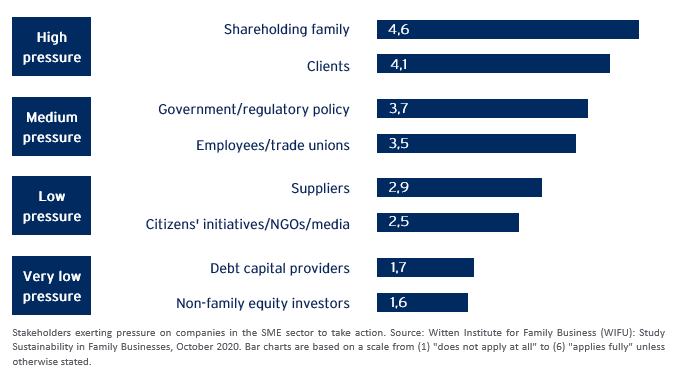

Expectations around an ESG expression of the SME business model arise in a wide variety of internal and external stakeholder groups. Typical stakeholders include shareholder families, employees, customers and suppliers, financiers (EC and FC), NGOs and the media, and to an increasing extent regulatory policy.

The reasons for which companies address ESG requirements also vary. The most common motives include:

- The assumption of ecological and social-societal responsibility,

- Ethical reasons and intrinsic motivation,

- Requirements of customers and employees,

- Cost reduction and expectation of increasing sales,

- Requirements of capital providers,

- And last but not least, the increasing regulatory requirements.

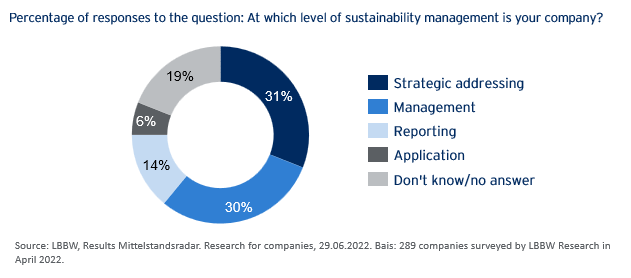

The majority of companies are in the early stages of sustainability management.

Pressure to act and status quo around ESG in SMEs

The pressure to develop and implement ESG strategies is immense and relevant stakeholders are demanding this. In addition to opportunities of an ESG orientation such as cost reduction, successful positioning of the company, revenue and profitability advantages, there are clear business risks of a lack of consideration of sustainability requirements up to the withdrawal of the “license to operate” (violation of regulatory requirements, exclusion from supply chains, lack of financing or perspective withdrawal of insurance coverage).

If, against this background, surveys come to the conclusion that, despite pressure to act and explicit expectations of the relevant stakeholders, only around half of the companies in the SME sector have developed and implemented ESG strategies, the question arises as to why.

A ´decisive factor is the lack of time and resources in many SMEs to deal with the challenges and requirements of sustainability. Time is traditionally a scarce commodity, especially in owner-managed companies. Teams and specialists for ESG strategies and sustainability cannot simply be plucked out of the ground: the market for ESG specialists is empty and salary expectations are correspondingly high.

Support from external consultants is the obvious choice, but here, too, capacities are stretched and for many a large consulting firm it is obvious and more lucrative to advise the large DAX companies with entire teams of consultants before they delve into the peculiarities of the business model of a geographically decentralized SME.

AIM – Advice in Motion GmbH

This is where AIM, as an independent sustainability consultancy and partner in the Investec network, can provide effective support. AIM thinks and speaks medium-sized. Their clients include medium-sized companies from a wide range of industries in Germany, France, Portugal, Luxembourg and Switzerland. AIM supports with:

- Creation, coordination and implementation of ESG strategies in medium-sized companies,

- Preparation for mandatory sustainability reporting (CSRD),

- Directive-compliant calculation of the carbon footprint of companies (CCF) and products (PC),

- Preparation of climate strategies, derivation of targets and measures from the climate footprint,

- Communication around ESG and climate protection: avoidance of reputation risks.

Examples of successful ESG implementation in medium-sized companies:

I. Initial situation: Sustainability requirements for a medium-sized company in the wood industry in Germany with around 1,200 employees. In addition to the intrinsic motivation of the shareholders, a major impetus for action arose from the initiative of the industry association, which demands the implementation of climate protection measures for all member companies. Another impetus for action was for the company, as a supplier in the value chain of a large trading house, to support its ambition (climate protection and other social goals throughout the supply chain). AIM supported the development of a climate strategy, the calculation of the corporate carbon footprint and the compensation of unavoidable emissions in order to achieve climate neutrality.

II. Initial situation: market positioning of a 5-star resort hotel in Provence with its own vineyard. A key impetus for action was to reconcile a luxury resort with sustainability requirements and climate change mitigation measures. AIM developed an ESG strategy for the resort. This was based on a selection of sustainable development goals (SDGs) to which the resort can contribute. Corresponding measures were defined and implemented. At the same time, climate neutrality was achieved for the resort by offsetting unavoidable emissions. (AIM has implemented a comparable project with a resort in Portugal, which has since been nominated for the Sustainability Award of the Portuguese Tourism Association).

III. Initial situation: product positioning for a manufacturer of high-quality competition racing bikes from Switzerland. The company wants to make competitive sports compatible with sustainability and climate protection in particular. In order to provide buyers and users of the competition bike with an assessment of the carbon footprint of the racing bike product, AIM calculated the product-related carbon footprint for the bike, taking into account all phases of the life cycle of the racing bike, from cradle to grave.

IV. Initial situation: A medium-sized holding company with around 1000 employees in Germany will be subject to mandatory sustainability reporting in accordance with CSRD for the first time from the calendar year 2024. The extended reporting affects around 15,000 companies in Germany. The company’s sustainability performance will be considered from two perspectives: the impact of sustainability aspects on the corporate business model and the impact of the company’s activities on the environment and stakeholders. At the same time, the company aims to create a comprehensive ESG strategy that brings together all the actions taken to date to support sustainability goals. AIM has worked with the company to develop an ESG strategy that is aligned and parameterized with metrics to best prepare for upcoming sustainability reporting.

The development of company specific ESG and climate strategies and the requirements associated with the expansion of sustainability reporting pose major challenges for entrepreneurs in the SME sector. We support your company effectively in the sustainable transformation to ensure together with you the future and the competitiveness of your company for you and future generations.

Author: Andreas Kuschmann, Founding Partner AIM – Advice in Motion GmbH.

Unlocking Working Capital potential to fuel operational growth

Amidst the aftermath of the COVID-19 pandemic, geopolitical tensions, and persistent inflation, it is crucial for companies to prioritize efficient working capital management (WCM) in order to navigate near-term uncertainty and foster growth during the economic recovery. We identified four key reasons that make WCM crucial:

1. Economic headwinds are expected to be persistent: Despite the recovery of most advanced economies to pre-pandemic levels of output, growth in 2023 is projected to be sluggish. Recent downward revisions in growth forecasts highlight the challenges that lie ahead. For instance, the GDP growth forecast for the EU has been reduced to around 0.75%, a mere one-fifth of the previous year’s growth1. The IMF has also predicted that Germany will be the second weakest G7 economy next year, following the UK, with an anticipated GDP contraction of 0.11%1. Moreover, recent data reveals that the German economy contracted slightly for two consecutive quarters, by 0.5% in Q4 2022 and 0.3% in Q1 20232.

2. Inflationary pressure remains high until at least 2024: The Russian invasion of Ukraine has led to skyrocketing energy and food prices, resulting in persistent inflationary pressures. Additionally, rising material costs and supply chain challenges pose a threat to inventory levels, leaving businesses susceptible to supply shortages and price fluctuations. Although the IMF predicts a decline in inflation in Germany from 8.7% in 2022 to 6.1% in 2023, a return to the 2% target is not expected until at least 2025. Consequently, some companies have turned to forward buying and speculative upstocking. However, this strategy strains working capital and depletes cash reserves.

3. Interest rate peak has probably been reached: Central banks across the world have continued to tighten monetary policy and roll back quantitative easing to defeat red-hot inflation. In Europe, the ECB has raised its key interest rate by 0.25 percentage points to 3.5% in June, marking the eighth consecutive increase since July 2023. This rate-hiking cycle is the fastest in the ECB‘s history. ECB President Christine Lagarde announced further rate hikes in July, indicating an ongoing trend. According to a survey conducted by Bloomberg, it is projected that the peak will be reached at 4% in September 2023. Consequently, financing and working capital is becoming increasingly expensive.

4. Corporate cash flows are coming under increasing pressure: According to PwC, Days Cash on Hand of companies decreased by 10% in 20214. In 2022, the intensified efforts of central banks worldwide to combat inflation by raising interest rates have significantly impacted corporate cash flows. Mounting challenges stem from factors such as cost inflation, supply chain disruptions, and geopolitical events like the war in Ukraine, which have also influenced lender sentiment and global debt markets. In Europe, institutional loan issuance suffered a decline of 42% so far in 2023 compared to the previous year (as of July)5. As a result, the management of liquidity and working capital has become increasingly important.

Thorsten Gladiator, Managing Partner Investec: Supply chain issues and increasing (raw) material prices lead to higher funding requirements in working capital. A variety of working capital financing products allows for tailor-made solutions.

De markt voor ingrediënten is een snelgroeiende sector met hoge marges die aansluit op seculaire consumententrends, met mogelijk aanzienlijke toetredingsdrempels als gevolg van onder andere de complexiteit van ingrediënten en technische expertise.

Smaken en smaakversterkers vormen samen het grootste segment binnen de categorie zintuiglijke waarneming van ingrediënten voor voeding en dranken, met een verwachte jaarlijkse groei van 5-10% in het komende decennium.

Zoals in ons rapport te lezen is, zijn er veel mondiale en Amerikaanse PE-platforms. Bij Investec hebben we een wereldwijd ingrediëntennetwerk dat grensoverschrijdende toegang tot strategische en financiële kopers over de hele wereld vergemakkelijkt, zodat we een optimaal resultaat voor onze klanten kunnen garanderen.

Neem gerust contact met ons op.

Samen met ABN Amro en PwC organiseerde Investec de 13e editie van het inspirerende voedselevenement: Voedingsbodem voor Groei. Het evenement vond plaats op de prachtige externe locatie: Landgoed Luchtenburg, waar Pieter Dirven van de biologische ‘De Smaakspecialist’ de groep CEO’s en CFO’s van Nederlandse Food & Agro bedrijven enthousiast ontving.

Het evenement draaide om de ‘eiwittransitie’ naar een meer evenwichtige, duurzame en gezonde plantaardige voedselconsumptie. Centrale thema’s waren productinnovatie, hoe om te gaan met reststromen van grondstoffen, verbetering van smaak, textuur en gezondheid. De hoofdvraag was: hoe zorg je voor een duurzame voedseltransitie?

Externe sprekers van gerenommeerde voedingsbedrijven gaven stof tot nadenken: Herman Heijtmeijer (CFO Voergroep Zuid) en Willem Cranenbroek (CEO ME-AT, onderdeel van Vion), professioneel voorgezeten door Joost Hoebink.

Na het officiële programma was er ruimte voor een informele borrel, inclusief vegan & organic bites en het socializen met branchegenoten – een zinvolle afsluiting van een inspirerende dag.

Als je er niet bij kon zijn, maar wel nieuwsgierig bent naar het evenement, neem dan contact op met Jasper Erhardt of Maxim Zwaan voor meer informatie of voor het evenement van volgend jaar.

M&A appetite in the Nordics Food & Agro space remains strong during H2’22 with deal activity increasing 21% compared to the same period in 2021.

Market uncertainties and a turbulent economic environment has not put a stop to the wish for continuous growth through M&A as we have witnessed one of the most active H2 periods in six years. Intra-Nordic transactions remain the key growth driver with a lot of Nordic companies seeking to expand their Scandinavian presence. The Food sub-segment continues to be the most attractive space accounting for almost 2/5 of all transactions in H2’22, while the Agribusiness and Aquabusiness sub-segments each account for approximately 1/5 of the transactions in this period. Nordic companies operating within Beverage and Food Service & Distribution have both seen M&A activity in just above 1/10 deals the past half year.

Key insights:

- Nordics Food & Agro deal flow was tremendously strong in H2’22 exceeding the same period in both 2018, 2019 and 2021, while at par with H2 in 2017 and 2020.

- Intra-Nordic and domestic deals still drive M&A in the Nordics Food & Agro space, although we have witnessed an increase from international buyers.

- Private Equity involvement remains fairly consistent on a four-year basis accounting for 16% of transactions during 2022.

- Eight Nordic serial acquirers dominate the buy-side in the Food & Agro space with involvement in almost one out of five deals between 2017-2022.

- Stock performance in Nordic Food & Agro sub-segments have had a rough year with only the Aquabusiness index outperforming the overall market, while the Food index ends on par with the Nordic stock market and the other indexes underperform.

- Rolling 3-month average EV / NTM EBITDA multiples for listed peers in all sub-segments trade below their five-year average, implying a market still concerned with macroeconomic uncertainties and conflicts around the world.

- The past six months have delivered some truly interesting deals, including: The largest Danish merger in history between Chr. Hansen and Novozymes (EUR 11.7 bn), SalMar’s acquisition of an additional 37% stake in NTS ASA giving them the majority control, The Lindström Family’s sale of Bubs Godis to Orkla, and Mowi’s majority-stake acquisition of Arctic Fish (EUR 169m).

You are welcome to access the entire report via the following link: Nordics Food & Agro M&A H2 2022 review (DocSend), or you can have it sent to you by contacting us.

Please do not hesitate to contact us.

You can find more information on our website at www.capitalmind.com/food-agro/

De ingrediëntensector wordt gekenmerkt door hoge O&O-uitgaven, strenge regelgeving en een aanzienlijk groeipotentieel. De trends naar een gezondere levensstijl en steun voor welzijn ondersteunen de toenemende fusie- en overnameactiviteiten.

Belangrijkste inzichten:

Innovatieve bedrijven zijn het doelwit

Grote voedingsingrediëntenbedrijven zullen zich blijven richten op nicheleveranciers met een bewezen staat van dienst op het gebied van innovatie om hun productportefeuilles uit te breiden naar snelgroeiende segmenten, zoals speciale eiwitten en probiotica.

Veel subsectoren zijn gefragmenteerd

Er is een groot potentieel voor consolidatie in markten zoals die voor eiwitten, vezels, bakkerij- en hartige ingrediënten. De markt voor gezondheids- en voedingsingrediënten is momenteel gefragmenteerd en zeer aantrekkelijk voor financiële en strategische kopers.

kopers.

Er worden hoge multiples betaald

Overnemers zijn bereid hoge multiples te betalen om toegang te krijgen tot deze snelgroeiende sectoren, aangezien de gemiddelde EV/EBITDA multiple in onze transactieanalyse 17,2x bedraagt. Belangrijke waarderingselementen zijn de gevestigde klantenrelaties en technologische expertise.

Overnames zijn een cruciaal middel om toegang te krijgen tot deze markt vanwege de strenge lokale regelgeving en de noodzaak van technische expertise.

Beursgenoteerde spelers worden gewaardeerd tegen 3,1x omzet (2021) en 16,7x EBITDA (2021).

Een belangrijke reden voor de hoge gemiddelde waarderingen in de voedselingrediëntenmarkt is de EBITDA-marge die door de beursgenoteerde bedrijven wordt gerealiseerd.

Case study

The support provided by Investec’s teams is characterised by a tailor-made approach, based on the sharing of know-how, which is conducive to building lasting client relationships, as Xavier Dorchies, Strategy Director of the Avril Group, a major industrial player in the vegetable oil and protein sectors in France, explains in this video concerning Investec’s role on the sale of Theseo to Lanxess.

Investec has assisted Groupe Avril all along the sale process of Theseo: advising transaction strategy, defining deal tactics, qualifying buyers, identifying the best partner for the business, and organizing a competitive bid up to closing.

This deal illustrates Investec’s know-how in supporting companies in their growth project over the long-term: this is our 17th transaction for Avril group and our 4th for its subsidiary Theseo.

For over 20 years, we have been advising the senior management and strategy and M&A teams of major groups on the design, preparation and management of divestments of non-strategic assets and external growth transactions:

- Project for the disposal of non-strategic activities and/or subsidiaries / carve-out

- Where appropriate, pre-sale feasibility study of non-strategic activities to define the key success factors of a potential operation

- Acquisition in France and abroad

Case study

The Investec teams pay particular attention to the preparation of transactions, devoting time to the necessary education of stakeholders, as Yannick Gueho, CEO of Sopral, a subsidiary of the Avril group specialising in the formulation, production and marketing of pet food, reminds us when he joined forces with an investment fund.

Investec assisted Avril Group throughout the sell-side process:

- pre-sounding appetite for the asset in the market,

- monitoring of the financial VDD,

- approach of interested acquirers,

- creation of the marketing documentation,

- identification of carve out issues,

- management of the due diligence, and

- assistance in negotiating the deal and the legal documentation.

This sale is the 14th transaction advised by Investec for the Avril Group.

We are very proud to have been by their side since 2011.

Find the interview of Yannick Gueho, CEO of Sopral, on his experience with Investec during the sale of Sopral:

For over 20 years, we have been advising the senior management and strategy and M&A teams of major groups on the design, preparation and management of divestments of non-strategic assets and external growth transactions:

- Project for the disposal of non-strategic activities and/or subsidiaries / carve-out

- Where appropriate, pre-sale feasibility study of non-strategic activities to define the key success factors of a potential operation

- Acquisition projects in France and abroad

The support provided by Investec’s teams is characterised by a tailor-made approach, based on the sharing of know-how, which is conducive to building lasting client relationships.

Both financial and strategic investors increasingly submit purchase offers directly to company owners. They are often completely unprepared for such an offer. Buyers try to take advantage of this surprise effect.

Both interested parties from the private equity segment and companies themselves are now once again directly approaching company owners or making indicative offers for the purchase of privately owned companies to an extent rarely seen. Due to the ongoing low interest rate policy of central banks, high valuations, attractive growth prospects and high liquidity available for investments, private equity companies are under considerable investment pressure and have therefore significantly increased their direct investment efforts. Similarly, large companies are seeking growth through acquisitions to gain access to technologies and user end markets or to support their record high share prices. Both types of buyers seek to avoid highly competitive and structured transaction processes led by M&A advisors. From the buyer’s point of view, this can optimise the transaction duration and the purchase price – to the detriment of the seller.

Optimise sale price

Recently, we were approached by a business owner who had received an unsolicited offer to buy his company from a larger industrial partner. This original offer was around EUR 28 million. The entrepreneur sought advice because he was unable to assess the offer due to the lack of an accurate idea of the value of his company. At the same time, no preparations had been made for a possible sales process. Although there was a certain curiosity about a sale in terms of long-term succession planning, the topic of a company sale was not (yet) on the agenda due to positive business prospects.

The company had a current EBITDA of around EUR 4 million, attractive margins, a good reputation, and long-standing relationships with an international customer base. As with many SMEs, there was a noticeable concentration on certain customer sectors in this case.

We were able to argue and convince the entrepreneur that a higher sales price usually could be achieved through a thorough preparation of information and documents as well as a competitive sales process. Special attention was paid to the formulation of an attractive “equity story”, which was derived from the positioning of the company, its unique selling propositions, and its growth potential. Equally important was a review and preparation of the financial history as well as the short- and medium-term corporate planning, ideally consisting of an integrated P&L, balance sheet and cash flow planning.

After preparing the sales documents, a multi-stage sales process was initiated and structured in which both potential strategic buyers and selected financial investors such as private equity companies and family offices were approached. Relevant company information was first made available to interested parties by means of a teaser and investment memorandum and, in a later step, via an electronic data room. The confidentiality and sensitivity of certain information was always taken into account through the gradual disclosure, which was adapted to the stage of the process or negotiations.

The company was ultimately sold to the original bidder for more than EUR 36 million. This represents a significant improvement over the initial bid – without any material change in the operational or financial situation.

Don’t get rattled

Buyers try to take advantage of the element of surprise by proactively making offers. Such offers are often not only below the achievable market price, but they address companies and owners unprepared. A professionally structured divestment process can increase the probability of success of a transaction and optimise the transaction terms, including the final purchase price, in favor of the seller.

Don’t reveal too much too soon

Sometimes, as advisors, we are only brought into a sales process when talks with the prospective buyer are already underway or – regrettably – deadlocked. By this time, a lot of information has often already been given to the prospective buyer, which tends to weaken the seller’s position. In such a situation, it is important to regain control of the transaction process. By preparing well for the due diligence and by including possible other interested parties in the divestment process, the seller’s negotiating position can be improved. The further process may or may not include the original bidder.

By proceeding in this way, business owners can be sure that they can optimise the valuation as well as better control the contractual arrangements of the final buyer. With a view to a careful preparation and structured implementation of a sale, it is in this respect helpful to involve or cooperate with specialised advisors as early as possible.

Cooperation with “business confidants”

We have been “in the market” since 1999, during which time Investec has built trusting relationships with numerous financial institutions, tax advisors, auditors, and other business confidants. We understand and respect the history of relationships, therefore clear agreements and responsibilities are important to us. As an advisor specialised in corporate transactions and financing, we rely on close cooperation with these players as well, in order to bring together expertise and drive for the benefit of the client.

What to do when earnings fall, liquidity becomes scarce and existing investors say no?

In crises such as COVID-19, the first priority is to ensure the company’s liquidity by taking advantage of all aid programmes and by securing promotional and guarantee loans. However, falling earnings and cash flows and weak liquidity also require rapid operational and financial restructuring to make the company weatherproof in the long term.

While the basis of a restructuring is of course always a solid operational restructuring concept, the existing capital structure must be adapted to future cash flows with the same high priority. Refinancing/rescheduling of debt and the sale of non-strategic or non-operational assets are often essential elements in this process.

Dissolve blockade with a clear concept for restructuring

Although a good operational concept often exists, unfortunately many companies slide into insolvency despite good approaches because they cannot (or not fast enough) explain to stakeholders what the concept means for them financially and what their specific benefit will be after its implementation.

In more complex cases, a financial restructuring concept depicting the cash flows and values throughout the restructuring phase and thereafter across the various financing instruments and capital providers is required. The concept clarifies to all stakeholders the consequences of the restructuring for their own values and the associated opportunities and risks. A consensus can only be reached if this is done professionally, i.e. if each stakeholder knows his options and perspectives.

The capital structure must be adapted as best as possible to the new cash flow patterns in the crisis. In this way, insolvency can be avoided, values preserved, and the success of the company secured.

Investec case study Wohnbau Mainz

Clear restructuring concept, debt payback via sale of non-core assets and subsidiaries, refinancing via syndicated loan

Due to inefficient operating structures, excursions into risky project development and a barely manageable complexity of bilateral loan agreements and special purpose companies, the residential real estate company of the City of Mainz was plunged into an earnings and liquidity crisis with dimensions threatening its existence. We were given the mandate to develop and implement a concept for the financial restructuring of their approximately € 1bn million balance sheet.

Standstill agreement and restructuring agreement negotiated

Following our appointment, we worked with the CRO and the operational restructuring advisors to develop a viable restructuring concept for the shareholders’ meeting and the creditors’ committee, within a few weeks. The concept detailed and clarified the rating and valuation consequences of all structural and operational measures as well as the sale of assets proposed by us for the individual stakeholders.

On this basis, we were first able to conclude a standstill agreement with the lenders and then based on an IBR (IDW S6 expert opinion) we were able to negotiate a restructuring agreement with all parties.

Conversion and refinancing in syndicated loan for Wohnbau

The agreed sales and cost-cutting measures were implemented, thereby improving the debt capacity and debt service capacity of Wohnbau Mainz.

The company was split up into a stable residential construction company with an investment grade rating and a rather risky project development company. Non-strategic property portfolios were sold. The proceeds were used to reduce debt and to renegotiate over 80 bilateral and cross collateralized loans that were ultimately bundled into a syndicated loan.

Solidly positioned after successful financial restructuring

Today Wohnbau Mainz is once again a solidly positioned company with a stable and sustainable financing structure. The value of the company has been maintained for the shareholders and creditors. An insolvency and thus a massive destruction of value was avoided.

Investec has successfully accompanied more than 60 financial restructurings over the last decade

Investec, has been assisting its clients in such complex refinancing and restructuring transactions for over 15 years. We know the objectives of all stakeholders well, having successfully solved cases for companies and their shareholders as well as for banks and other creditors. In over 90% of cases, on whichever side, we have been able to reach a consensus between these groups on the necessary restructuring measures.

Core competences, company valuation, rating, financial modeling, capital raising and Selling companies

Our core competencies include financial modelling, rating analysis and company valuation as well as the preparation of internal committee documents for banks/creditor pools and shareholder/supervisory bodies. We develop a conclusive debt and equity story for existing creditors and new debt and equity investors.

We subsequently implement the measures, negotiate restructuring agreements and raise capital. We support you in the sale of subsidiaries and non-strategic business units through restructurings which are advised in close cooperation between our global sector teams and our capital advisory groups.

The Investec Fabulous 20 Food and Drink 2019 shows the 20 fastest growing companies in the Dutch Food and Beverage industry. This annually recurring ranking is compiled in cooperation with the Dutch magazine FoodPersonality.

‘With the acquisition of Bakkersland, Borgesius takes the first place in the list with an astonishing average growth rate of 94.9%. The top 3 is complemented by Nedato and Van Loon Group, with respectively 28,6% and 25,8% average growth. The list displays that M&A is a prime catalysator for growth as 45% of the companies in the list acquired one or more companies in the measured period.’

A link to the full article on our Fabulous 20 Food and Beverage – tenth edition (2019), can be found here.