Versterking van ons Industrial Tech & Services team

Investec heet Matthias Odrobina van harte welkom als Managing Director van ons European Business Advisory en als senior lid van het wereldwijde sectorteam dat Europa, het Verenigd Koninkrijk, Afrika, de VS en Azië bedient met onafhankelijk advies over grensoverschrijdende transacties.

Matthias beschikt over diepgaande sectorexpertise op het gebied van industriële technologie – met bijzondere aandacht voor smart industries, B2B-software en digitale transformatie.

Hij heeft 20 jaar ervaring als vertrouwd partner voor raden van bestuur en eigenaren op het gebied van fusies, overnames, desinvesteringen, financieringen en buyouts, met een bijzondere focus op de industriële sector, B2B-software en zakelijke dienstverlening.

Contact: Matthias Odrobina

How a professional dialogue is now moving companies forward

Interview with Thorsten Gladiator, Managing Partner of Investec about how a professional dialogue is now moving companies forward:

- Why companies should entertain a professional dialogue with their investors and lenders?.

- What other challenges are companies facing?

- As a financial expert and transaction specialist what advice do you have for companies when dealing with debt and equity investors?

- Giving an example.

This video answers these questions and give you an idea and overview in a few minutes.

Finding the right type of capital and investor to help grow your business

Our team has a long track record of successfully raising equity and debt capital and has the necessary expertise and networks:

- Raising capital to support business growth

- Securing capital from private equity and/or other Investors to support MBO/MBI projects

- Securing capital from private equity and/or other investors to manage changes in the shareholding structure (such as supporting the buyout of one or more shareholders and the reallocation of equity shares)

- Project financing: supporting companies in realizing essential investments or working capital

- Refinancing: supporting companies in reorganizing/reducing their debt burden

Investec is proud to announce that our French team is awarded as one of the Best Investment Bank – LBO Small to Mid Cap with a Silver Award at the recent Sommet des Leaders de la Finance in Paris.

Organised by Décideurs Corporate Finance, this event recognises excellence in corporate finance and highlights the work of professionals who lead complex and strategic transactions.

We warmly thank our teams for their dedication, and our clients for their continued trust.

Navigating Market Crosswinds Through Strategic M&A

The M&A market for industrial system integrators is currently experiencing decreased deal activity due to global uncertainty. Buyers have become more cautious, prioritizing strategic acquisitions in key end-markets and technologies.

Private equity firms remain highly active, leveraging buy-and-build platforms. With strong capital positions, strategic positioning in key end-markets and technologies, players are well-placed to capitalize current market crosswinds through M&A.

Ongoing consolidation, underscores the sector’s long-term potential for scalable growth.

Ervin Schellenberg, Managing Partner Investec

This report provides an overview of valuations, transactions, buyers, etc. in the European industrial systems integrator market.

To access and read the full report click here

Case Study

Aqseptence Group, a global leader in autonomous water and filtration technology, equipment and system solutions specialising in water treatment and liquid/solid separation, has attracted Oaktree, a leading global investment manager, as an investor.

Oaktree’s investment and expertise will provide Aqseptence Group with the necessary resources to continue to grow and innovate to best serve existing and new markets.

Interview with Baldassare La Gaetana, CEO of Aqseptence Group and Ervin Schellenberg, Managing Partner of Investec, taking us through the process and decision making of Oaktree’s majority investment in Aqseptence in a short video:

- What is the Aqseptence Group? Why a new shareholder?

- What is your sector and investor perception? – Opinion Ervin Schellenberg

- Why is it important to work with an M&A advisor? – Opinion Baldassare La Gaetana

- How was the collaboration with Investec?

For nearly 25 years, Investec has been assisting its clients in reaching their strategic goals, whatever it takes, whether it’s by securing a strategic business, or maneuvering and winning a competitive auction process:

We are particularly adept at advising on the following situations:

- Acquiring (family-owned) companies, groups, or other mid-market companies

- Acquiring subsidiaries or business units from (international) corporates, including carve-outs

- Acquiring businesses from a founder/(majority) shareholder, including succession

- Acquiring shares owned by a private equity firm, family office or other investors

Designing and executing such transactions is what our team does on a daily basis. To ensure success, our team also leverages its extensive experience and unique capabilities, which include: deal intelligence, tactical, technical and project management skills, negotiation skills, and an understanding of the personal interests/sensitivities of relevant stakeholders.

The Rheingau Music Festival is one of the largest music festivals in Europe and organises over 170 concerts every year throughout the region from Frankfurt and Wiesbaden to the Middle Rhine Valley.

Unique cultural monuments such as Eberbach Monastery, Johannisberg Castle, Vollrads Castle or the Wiesbaden Kurhaus as well as picturesque vineyards are transformed every summer into concert stages for stars of the international classical music scene and interesting up-and-coming artists from classical music and jazz to cabaret and world music.

In over 30 years, the Rheingau and its festival have become a centre of attraction for music enthusiasts from all over the world in a unique interplay of culture and nature, music, enjoyment and joie de vivre.

Investec is delighted once again to sponsor the Rheingau Music Festival 2024 and invites you to join us from 22 June to 7 September 2024!

A special feature this year? For the first time, there will be two opening concerts: Traditionally, the festival opens in the Eberbach Monastery, followed by another opening concert in the Kurhaus Wiesbaden. This year’s focus artists are also particularly outstanding: violinist Christian Tetzlaff, cellist Anastasia Kobekina, pianist Bruce Liu and jazz saxophonist Candy Dulfer.

Once again this year, various themes and focuses will ensure a varied and exciting programme. Under the motto “Spot on: Hollywood”, the world of film music comes to life in twelve concerts. Under the motto “Brazil!”, the contrasts and beauties of the country will be explored musically. The programme is also dedicated to the works of Antonín Dvořák and a true classic: Vivaldi’s “Four Seasons”.

The stages of the 37th festival season will be graced by numerous stars from the worlds of classical and pop music. Highlights include star pianist Lang Lang, singers Álvaro Soler, Max Mutzke and Max Giesinger, violinist Anne-Sophie Mutter, opera singer Rolando Villazón and entertainer Eckart von Hirschhausen.

Investec has been a committed sponsor of the Rheingau Music Festival for more than 15 years. This long-standing partnership is characterised by our deep appreciation for the arts and a strong connection to local culture. We look forward to experiencing a rousing summer full of music together with you again this year.

You can view the detailed program here.

Digital Disruption and Strategic Consolidation: Navigating the New Frontier in Industrial Services

Global Industrial Service

Technologization and Electrification along the full asset lifecycle to increase efficiency in industrial services and processes and comply with CO2 emission regulation.

Industrial Service Valuation drivers

The valuation of industrial services is primarily influenced by three pivotal factors. An increased involvement in the asset lifecycle and the ability to manage complex assets significantly enhance valuation metrics. Moreover, the intricacy of the service offered, and the dynamics of the target market further underpin these valuations. There is a notable shift towards a more comprehensive degree of asset stewardship, ranging from deploying personnel capable of operating the assets on-site to achieving full autonomy in asset management, thereby enhancing and operating the assets entirely independently from the end-user. Specifically, sectors such as energy and chemicals necessitate sophisticated services and assets, due to their inherent complexity and the critical nature of their operations.

Investec has extensive experience in advising deals in the Industrial Service sector. With 25 focused dealmakers across Europe, we can help you to achieve your strategic ambitions.

Interview

As we enter 2024, the M&A landscape shows signs of recovery, albeit cautiously.

In the episode of the February 20, 2024 of No Ordinary Wednesday, Jeremy Maggs in conversation with Investec experts Jürgen Schwarz, Marleen Vermeer, and Kilian de Gourcuff, Investec’s Head of Cross-Border Finance and International Advisory Charles Barlow, on what key sectors, trends and risks to keep an eye on in 2024.

Click below to listen to the podcast:

Where does opportunity lie for dealmaking in 2024? (investec.com)

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Listen to the best of No Ordinary Wednesday: https://www.investec.com/en_za/focus/no-ordinary-wednesday-with-jeremy-maggs.html

Sustainable underlying trends, attracting interest from all market participants, coupled with high risks and investments in the development phase are paving the way for a thriving market.

The European M&A market for industrial software continues to be fuelled by consolidation across all end market segments. Ongoing trends of digitalization within the industrial sector, increasing convergence of sectors and the demand for more (factory) automation to counteract the increasing shortage of talent are just a few selected trends contributing to the growing interest from private equity firms and strategic players crossing sector and geographic borders.

Software as a solution to competition gaps

The advancement of Industry 4.0 implementation, integrating digital technologies into the manufacturing process, positions digitalization at the core of most sectors. Compliance with this trend has become inevitable for companies striving to stay at the forefront of innovation. Both micro- and macroeconomic trends, such as skilled labor shortages, ESG policies, and reshoring of complete production plants, are accelerating this process. Meanwhile, safeguarding assets is essential as the industrial system becomes more (cyber)connected and online. The German industry, accounting for approximately 25% of the country’s GDP, is considered critical infrastructure, emphasizing the need to ensure data integrity.

Market interest from different strategic angles

Software has always attracted various buyer pools with different strategic interests. Financial sponsors are particularly interested in recurring and scalable revenues combined with high-profit margins. In contrast, strategic players seek capabilities expansion and the “softwarization“ of their hardware (IoT). The industrial software market demonstrates sustainable growth underpinnings, with optimizing and modernizing the IT landscape being more crucial than the hardware itself.

Deal examples:

Growth capital unlocked for Desk by Software Partners Group

“SPG is a partner that combines excellent technology know-how and buy & build expertise, which will enable us to reach the next stage of our buy&build journey.” Volker Schneider (CEO, Desk)

wenglor sensoric group acquires Berlin based AI and Image processing Start-Up deevio

“With the acquisition of deevio GmbH, we have this opportunity to further strengthen our expertise and capability in the field of machine vision. In recent years, deevio has developed a great deal of know-how in using AI and data science for image processing applications within the automation industry, which is a considerable advantage for us.” Rafael Baur (Managing Director, wenglor)

Data (analytics) driven production: The new standard

New levels of data accessibility have been achieved, with standard APIs implemented across the entire IT landscape of the industry and collaboration between industrial technology providers. Data lakes are formed through a multi-sourcing policy from (digital twin) machinery and sensors, the IT architecture (ERP, MES, etc.), and human-generated data (quality management, observations, etc.). Recent technologies, such as AI, cloud computing, and predictive models, enable the treatment and analysis of the vast amount of generated data. Decision-makers now have access to aggregated and qualitative information for data-driven decisions.

Deal examples:

Majority investment of FSN Capital in Lobster

“In a world of exponentially growing amounts of data, complexity of data flows and application stacks, Lobster offers easy to use, economic and powerful software solutions to integrate data, applications, and processes of all forms and variations.” Robin Mürer (Co-Managing Partner, FSN Capital Partners)

The same old challenge… – make or buy

The ultimate question in growth strategies making companies consider M&A as an option is whether to make or buy. The combination of high development costs (in time and opportunity) but risky success rates is the primary rationale for market activity within (industrial) software to expand its capabilities and/or geographical footprint. The principle of Moore’s Law is still true in today’s technology ecosystem. Rapid cycles leave no room to develop everything in-house, acting as a catalyst for market activity.

Deal examples:

“Best Practice IT Solutions’ cloud-based software will complement Aptean’s current Food & Beverage ERP offering and enhance our ability to serve beverage companies.” Duane George (GM, Aptean)

“By bundling the expertise of tisoware and Persis, we create a uniquely comprehensive HR ecosystem for our customers. Together with solutions for access and building security (Security) and for optimizing production processes (MES) in the context of Industry 4.0, we offer an overall workforce portfolio for medium-sized enterprises in the DACH region.” Markus Steinberger (CEO, tisoware)

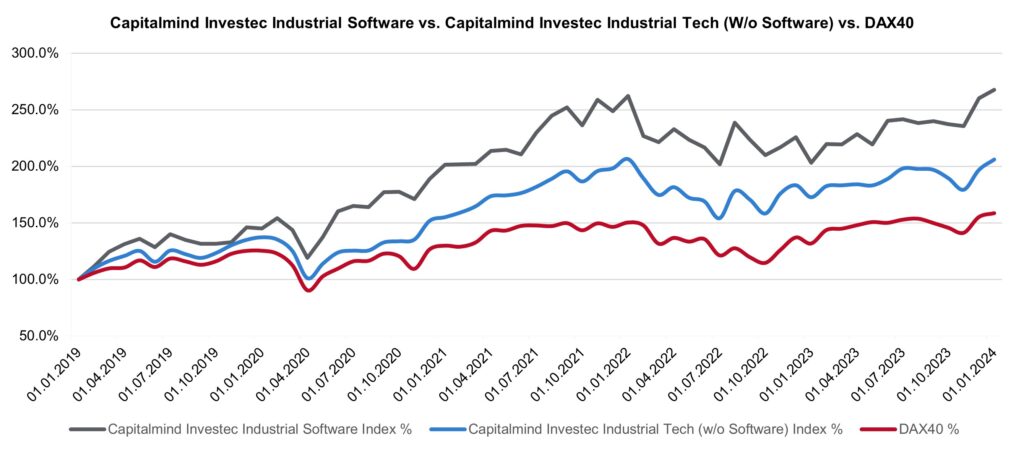

Our industrial software index outruns other indexes

Since 2019, the Industrial Software Index has risen almost threefold, while the main Industrial Technology sector has doubled. A new all-time high has been reached for market capitalization.

The main macroeconomic events over the last 5 years have similarly impacted all indexes, but industrial software market capitalizations seem to recover more quickly.

Valuations for listed industrial software companies, both EV/EBITDA and EV/Sales, remain high, with forward multiples at ca. 11x sales FY2024.

So, industrial software – hot or not?

Most checkboxes are ticked for answering the question positively:

- High valuations are fueling market activity.

- Growing interest, both from financial investors and large software consolidators.

- Sustainable market movers, with both strategic and financial rationale, are dictating most transactions.

Investec Industrial Technology

The Investec Industrial Technology index tracks daily developments in sectors such as Flow & Process Control, Robots/Motion, Electronics/Control / Connect, Integrated providers, Measurement/Vision Tech, Industrial Software, Intralogistics/System integration and Machinery.

The index includes valuations, growth projections, profitability margins and other metrics.

Would you like to learn more about valuations, buyer activity and current opportunities in the market?

Please do not hesitate to contact us.

You can find more information on our website at Industrials | Investec

Understanding your company and your market environment are key factors for the success of your business.

Interview with Ervin Schellenberg, Managing Partner of Investec about how to make a traditional company fit:

- How is the client’s situation?

- How do you support your clients?

- Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

The industrial sector is undergoing profound change. In times of Industry 4.0, digitalisation and the development of alternative energies, new disruptive models are emerging that are forcing the major historical market leaders to rethink their strategy, organisation and industrial processes, integrating new forms of consumption, mobility, the emergence of subscription models, etc.

With more than 100 transactions in the industrial sector, our team is at the heart of the market, trends and M&A operations to provide you with effective support and high commercial added value for your sale, acquisition and financing operations.

Financial restructuring for Shareholders & Lenders

Helping clients to navigate uncertainties while putting their businesses back on track

Interview with Jürgen Schwarz, Managing Partner of Investec about Restructuring with the help of a M&A process:

- How did the market change in recent years?

- What is your approach?

- Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

Sale from insolvency

Due to our pan-European presence and track record we are well placed to advise on international and cross-border restructurings.

Our international sector teams implement more than 50 transactions p.a. and in many sectors they know the active buyers, the acquisition criteria, the behaviour of individual decision makers. We also have an up-to-date overview of the market prices paid, which vary considerably over time and depending on the positioning in the sector.

Investec has direct access to numerous international equity and debt capital providers and has carried out numerous restructurings ranging from approximately 10 million Euros to several billion Euros.

You know your company best but selling it to a suitable buyer at an attractive price is often a major challenge.

Interview with Ervin Schellenberg, Managing Partner of Investec about finding the right partner for medium-sized companies:

- How to find the right partner for a medium-sized company?

- Is my company ready for a transaction?

- What is the equity story?

- Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

Our wealth of experience from many years of successful transactions and our access to relevant decision-makers in national and international buyers ensure the best possible result for you.

Investec has the core competences required to sell companies and has successfully completed hundreds of transactions across all major industries.

Financiering en markttrends | 2023

Waarom de Duitse industrie grote behoefte heeft aan investeringen.

De Duitse industrie staat voor grote uitdagingen, waaronder de effecten van digitalisering, de verschuiving van analoge naar digitale bedrijfsmodellen, de behoefte aan milieubeschermende maatregelen en duurzame productieprocessen, evenals demografische veranderingen, die leiden tot een tekort aan geschoolde werknemers en een vergrijzende beroepsbevolking. Om deze processen succesvol te beheersen, zijn aanzienlijk hogere investeringsinspanningen nodig dan in het verleden.

Digitalisering en Industrie 4.0: Op dit moment staat Duitsland op zijn best in de middenmoot van de EU wat betreft het gebruik van digitale technologieën in de economie1. De Duitse industrie moet investeren in digitale technologieën en automatisering om concurrerend te blijven. Maar om de achterstand op vergelijkbare landen in te lopen, zouden de investeringen in IT en digitalisering in Duitsland moeten verdubbelen of verdrievoudigen van 49 miljard euro naar 100 tot 150 miljard euro per jaar. Alleen al in het mkb zouden de uitgaven voor digitalisering moeten stijgen van 18 miljard euro in 2019 naar 35 tot 50 miljard euro per jaar.

Duurzaamheid en milieubescherming: Bedrijven richten zich steeds meer op milieuvriendelijke technologieën en processen om hun duurzaamheidsdoelstellingen te halen en hun impact op het milieu te verminderen. Deze investeringen dienen niet alleen om het milieu te beschermen, maar dragen ook bij aan het concurrentievermogen op lange termijn. Een recente studie in opdracht van KfW schat de klimaatbeschermingsinvesteringen die nodig zijn om de doelstelling van klimaatneutraliteit tegen 2050 te bereiken op ongeveer 5 biljoen euro of ongeveer 190 miljard euro per jaar1. Dit enorme bedrag maakt duidelijk dat er aanzienlijk grotere inspanningen nodig zullen zijn om de doelstelling te halen dan tot nu toe het geval is geweest.

Lees de volledige insight hier.

Thorsten Gladiator, Managing Partner Investec: As corporate finance advisors, we see the importance of ESG in general and sustainability aspects in particular in almost every transaction, both in M&A situations and in financing mandates.

Equity and debt investors place a strong focus on ESG compliant investments in the interest of their financiers and / or due to investment criteria that are binding for them.

For business sellers as well as CFOs, this has pricing and process consequences:

- A clearly defined and documented ESG strategy creates confidence among investors and the company’s other stakeholders

- The same applies to the (early) implementation of legal requirements for sustainability reporting (CSRD)

- A focus on sustainability aspects provides positive differentiation features compared to competitors and can thus have a value-creating effect

- The lack of a corresponding strategy can lead to price discounts in the valuation as well as higher financing costs

- In the due diligence phase of a transaction, lack of ESG information leads to prolonged processes, higher management burden and the withdrawal of investors with clearly defined ESG investment criteria

The following article from AIM – Advice in Motion highlights the various aspects for medium-sized companies and shows examples of successful ESG strategies.

Opportunities and challenges of sustainability for smaller and medium-sized enterprises

The sustainability performance of a company today is the decisive factor for its competitiveness tomorrow. In this context, medium-sized companies in Germany in particular are faced with tasks whose extent has not yet been fully recognized in many cases and which involve major challenges in terms of resources, time and expertise.

Even though sustainability is a ubiquitous and much-discussed topic that is omnipresent both in the media and in public debate, it is by no means a new issue. Rather, sustainability has a long and exciting history that spans centuries and has been shaped by various actors and concepts.

Where do the roots of sustainability lie?

As far back as the Middle Ages, the moral ideal of the honorable merchant played a decisive role in promoting sustainable principles. Many a family entrepreneur rightly sees himself or herself in the tradition of the honorable merchant and aligns his or her business conduct with principles such as honesty, responsibility and sustainability.

In the 18th century, the Saxon chief miner Carl von Carlowitz coined the term sustainability in his work “Sylvicultura Oeconomica.” He introduced the idea that forest resources should be managed sustainably by cutting only as much wood as can naturally grow back. What was interesting about Carlowitz’s concept of sustainability was that sustained yield was precisely not antithetical to sustainability. Rather, forestry yield acted as the cornerstone for this oft-cited source of the concept of sustainability. The mining area of the Erzgebirge was simply dependent on the sustainable use of wood for construction, mining and smelting purposes.

Another significant milestone in the development of sustainability was the Brundtland Report, published in 1987 under the title “Our Common Future”. The report defined sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” Here, sustainability clearly went beyond a purely economic consideration. The report emphasized the need to integrate economic, social and environmental aspects to create a sustainable future.

Since then, the understanding of sustainability has evolved to encompass a variety of dimensions. One key concept is ESG (environmental, social, governance) criteria, which encompass environmental, social and governance-related factors. Differentiation of individual sustainable development goals is achieved through the United Nations Sustainable Development Goals (SDGs), which were adopted in 2015. The SDGs include 17 global goals to promote sustainable development at the economic, social and environmental levels by 2030. These goals range from poverty reduction, health, education and gender equality to renewable energy and sustainable cities.

The SDGs are an excellent framework for linking the principle of sustainability with economic, ecological and social development and provide a suitable orientation framework for a company’s sustainability strategy:

- SDGs as guidelines for sustainable management

- Alignment of products and services with the SDGs

- Business activities can contribute directly to achieving the SDGs

Nowadays, at the current edge of development trends around sustainability, so to speak, ESG expression is thus considered a leitmotif and fundamental approach for responsible and sustainable development. It is about combining economic, social and ecological aspects in order to create a world worth living in for present and future generations.

The individual SDGs are suitable targets for integrating ESG into corporate strategies, as they are more concrete and easier to measure using indicators than the more fundamental ESG concept.

Importance of the midmarket

As the backbone of the economy, the SME sector comprises a large number of companies that operate both regionally and internationally. It is of great importance for economic performance and employment in the country. Around 2.5 million companies in Germany belong to the Mittelstand, in the definition of a small and medium-sized enterprise (SME). These range from microenterprises to medium-sized companies with up to 250 employees, which generate around one-third of total sales for Germany and employ more than half of all employees.

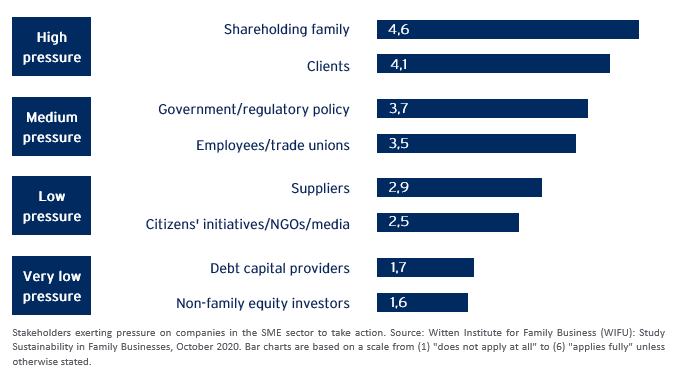

Expectations around an ESG expression of the SME business model arise in a wide variety of internal and external stakeholder groups. Typical stakeholders include shareholder families, employees, customers and suppliers, financiers (EC and FC), NGOs and the media, and to an increasing extent regulatory policy.

The reasons for which companies address ESG requirements also vary. The most common motives include:

- The assumption of ecological and social-societal responsibility,

- Ethical reasons and intrinsic motivation,

- Requirements of customers and employees,

- Cost reduction and expectation of increasing sales,

- Requirements of capital providers,

- And last but not least, the increasing regulatory requirements.

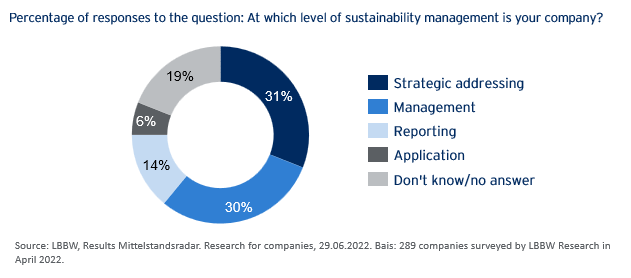

The majority of companies are in the early stages of sustainability management.

Pressure to act and status quo around ESG in SMEs

The pressure to develop and implement ESG strategies is immense and relevant stakeholders are demanding this. In addition to opportunities of an ESG orientation such as cost reduction, successful positioning of the company, revenue and profitability advantages, there are clear business risks of a lack of consideration of sustainability requirements up to the withdrawal of the “license to operate” (violation of regulatory requirements, exclusion from supply chains, lack of financing or perspective withdrawal of insurance coverage).

If, against this background, surveys come to the conclusion that, despite pressure to act and explicit expectations of the relevant stakeholders, only around half of the companies in the SME sector have developed and implemented ESG strategies, the question arises as to why.

A ´decisive factor is the lack of time and resources in many SMEs to deal with the challenges and requirements of sustainability. Time is traditionally a scarce commodity, especially in owner-managed companies. Teams and specialists for ESG strategies and sustainability cannot simply be plucked out of the ground: the market for ESG specialists is empty and salary expectations are correspondingly high.

Support from external consultants is the obvious choice, but here, too, capacities are stretched and for many a large consulting firm it is obvious and more lucrative to advise the large DAX companies with entire teams of consultants before they delve into the peculiarities of the business model of a geographically decentralized SME.

AIM – Advice in Motion GmbH

This is where AIM, as an independent sustainability consultancy and partner in the Investec network, can provide effective support. AIM thinks and speaks medium-sized. Their clients include medium-sized companies from a wide range of industries in Germany, France, Portugal, Luxembourg and Switzerland. AIM supports with:

- Creation, coordination and implementation of ESG strategies in medium-sized companies,

- Preparation for mandatory sustainability reporting (CSRD),

- Directive-compliant calculation of the carbon footprint of companies (CCF) and products (PC),

- Preparation of climate strategies, derivation of targets and measures from the climate footprint,

- Communication around ESG and climate protection: avoidance of reputation risks.

Examples of successful ESG implementation in medium-sized companies:

I. Initial situation: Sustainability requirements for a medium-sized company in the wood industry in Germany with around 1,200 employees. In addition to the intrinsic motivation of the shareholders, a major impetus for action arose from the initiative of the industry association, which demands the implementation of climate protection measures for all member companies. Another impetus for action was for the company, as a supplier in the value chain of a large trading house, to support its ambition (climate protection and other social goals throughout the supply chain). AIM supported the development of a climate strategy, the calculation of the corporate carbon footprint and the compensation of unavoidable emissions in order to achieve climate neutrality.

II. Initial situation: market positioning of a 5-star resort hotel in Provence with its own vineyard. A key impetus for action was to reconcile a luxury resort with sustainability requirements and climate change mitigation measures. AIM developed an ESG strategy for the resort. This was based on a selection of sustainable development goals (SDGs) to which the resort can contribute. Corresponding measures were defined and implemented. At the same time, climate neutrality was achieved for the resort by offsetting unavoidable emissions. (AIM has implemented a comparable project with a resort in Portugal, which has since been nominated for the Sustainability Award of the Portuguese Tourism Association).

III. Initial situation: product positioning for a manufacturer of high-quality competition racing bikes from Switzerland. The company wants to make competitive sports compatible with sustainability and climate protection in particular. In order to provide buyers and users of the competition bike with an assessment of the carbon footprint of the racing bike product, AIM calculated the product-related carbon footprint for the bike, taking into account all phases of the life cycle of the racing bike, from cradle to grave.

IV. Initial situation: A medium-sized holding company with around 1000 employees in Germany will be subject to mandatory sustainability reporting in accordance with CSRD for the first time from the calendar year 2024. The extended reporting affects around 15,000 companies in Germany. The company’s sustainability performance will be considered from two perspectives: the impact of sustainability aspects on the corporate business model and the impact of the company’s activities on the environment and stakeholders. At the same time, the company aims to create a comprehensive ESG strategy that brings together all the actions taken to date to support sustainability goals. AIM has worked with the company to develop an ESG strategy that is aligned and parameterized with metrics to best prepare for upcoming sustainability reporting.

The development of company specific ESG and climate strategies and the requirements associated with the expansion of sustainability reporting pose major challenges for entrepreneurs in the SME sector. We support your company effectively in the sustainable transformation to ensure together with you the future and the competitiveness of your company for you and future generations.

Author: Andreas Kuschmann, Founding Partner AIM – Advice in Motion GmbH.

Unlocking Working Capital potential to fuel operational growth

Amidst the aftermath of the COVID-19 pandemic, geopolitical tensions, and persistent inflation, it is crucial for companies to prioritize efficient working capital management (WCM) in order to navigate near-term uncertainty and foster growth during the economic recovery. We identified four key reasons that make WCM crucial:

1. Economic headwinds are expected to be persistent: Despite the recovery of most advanced economies to pre-pandemic levels of output, growth in 2023 is projected to be sluggish. Recent downward revisions in growth forecasts highlight the challenges that lie ahead. For instance, the GDP growth forecast for the EU has been reduced to around 0.75%, a mere one-fifth of the previous year’s growth1. The IMF has also predicted that Germany will be the second weakest G7 economy next year, following the UK, with an anticipated GDP contraction of 0.11%1. Moreover, recent data reveals that the German economy contracted slightly for two consecutive quarters, by 0.5% in Q4 2022 and 0.3% in Q1 20232.

2. Inflationary pressure remains high until at least 2024: The Russian invasion of Ukraine has led to skyrocketing energy and food prices, resulting in persistent inflationary pressures. Additionally, rising material costs and supply chain challenges pose a threat to inventory levels, leaving businesses susceptible to supply shortages and price fluctuations. Although the IMF predicts a decline in inflation in Germany from 8.7% in 2022 to 6.1% in 2023, a return to the 2% target is not expected until at least 2025. Consequently, some companies have turned to forward buying and speculative upstocking. However, this strategy strains working capital and depletes cash reserves.

3. Interest rate peak has probably been reached: Central banks across the world have continued to tighten monetary policy and roll back quantitative easing to defeat red-hot inflation. In Europe, the ECB has raised its key interest rate by 0.25 percentage points to 3.5% in June, marking the eighth consecutive increase since July 2023. This rate-hiking cycle is the fastest in the ECB‘s history. ECB President Christine Lagarde announced further rate hikes in July, indicating an ongoing trend. According to a survey conducted by Bloomberg, it is projected that the peak will be reached at 4% in September 2023. Consequently, financing and working capital is becoming increasingly expensive.

4. Corporate cash flows are coming under increasing pressure: According to PwC, Days Cash on Hand of companies decreased by 10% in 20214. In 2022, the intensified efforts of central banks worldwide to combat inflation by raising interest rates have significantly impacted corporate cash flows. Mounting challenges stem from factors such as cost inflation, supply chain disruptions, and geopolitical events like the war in Ukraine, which have also influenced lender sentiment and global debt markets. In Europe, institutional loan issuance suffered a decline of 42% so far in 2023 compared to the previous year (as of July)5. As a result, the management of liquidity and working capital has become increasingly important.

Thorsten Gladiator, Managing Partner Investec: Supply chain issues and increasing (raw) material prices lead to higher funding requirements in working capital. A variety of working capital financing products allows for tailor-made solutions.

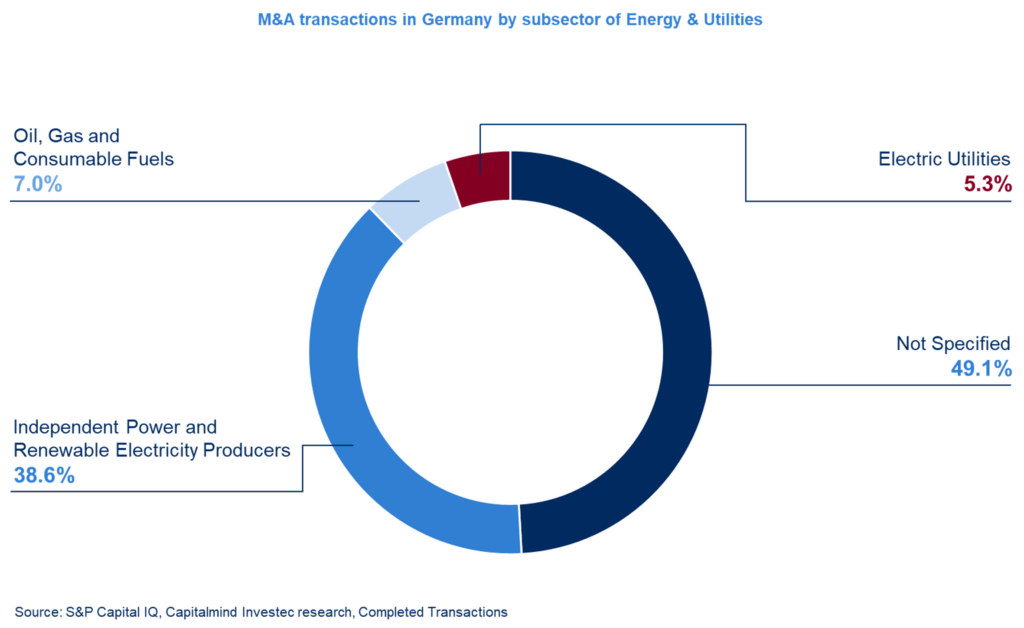

The analysis includes target companies in the Utilities, Energy Equipment and Services, Independent Power and Renewable Electricity Producers, Water and Oil, Gas and Consumable Fuels sectors.

Slight drop in transactions

In 2022, around 2200 transactions were concluded worldwide. This corresponds to a decline of about 9%. Europe’s share remained stable, North America fell back somewhat in favour of the Asia/Pacific region in particular.

Already with eight transactions, it was possible to grab first place in the list of the most active investors in 2022. Russia’s PJSC LUKOIL (acquisition of generation assets, exploration projects and the Spartak Moscow football club) and France’s TotalEnergies SE (acquisition of generation assets, utilities, activities along the natural gas value chain) take first place.

Only Greenbacker Renewable Energy Company and Encavis were already among the top ten in the previous year, accounting for a total of only around 3% of all transactions.

Globally, most deals took place in the Oil, Gas and Consumable Fuels segment, and these predominantly in Europe. The Independent Power and Renewable Electricity Producers category is close behind. This was reversed last year.

Stable conditions in Europe

In 2022, the UK again leads by a wide margin in the number of deals in Europe. The five next-placed countries do not even manage half the number of deals. The clear leaders are purchases of generation plants/companies. Almost 80% of the buyers come from the region (Europe).

Almost every second transaction concerns (green) power generation

In Germany, too, many of the transactions involved renewable energy generation plants. A decline of around 9 percentage points was recorded compared to 2021.

Furthermore, there were also transactions by well-known market participants such as e.g.

- Almost complete acquisition (>99%) of the shares in the listed Uniper AG by the Federal Republic of Germany.

- Full acquisition of G+E GETEC Holding GmbH by Infrastructure Investments Fund (J.P. Morgan Asset Management) from EQT and GETEC Energie Holding.

- Full acquisition of Thyssengas GmbH by Macquarie from the infrastructure fund DIF and an investment company of EdF.

Martin Hallinger, Senior Advisor, Investec: In addition to numerous other transactions in the renewable energy segment, current developments/trends in the M&A business are reflected in isolated cases. These include the development of a hydrogen economy, access to battery storage, charging infrastructure and other activities related to electromobility.

Valuations and M&A activity rebounce

Catching-up from our last Insight, we have seen many companies, both private and public, report excellent results for 2022. Some obstacles like supply chain disruptions and other pandemic effects have eased. Inflation, energy prices, additional effects of multiple geopolitical crises as well as the shortage of skilled work force still have to be considered as risks to the economic development and a recession scenario is not fully off the table. With a market volume of € 14.3bn in 2022 for the German robotics & automation industry, VDMA’s forecast (14.4) was only slightly missed, in 2023 the industry expects a significant 9% growth supported by processing the high order backlog and the continuous high level of demand for innovative automation solutions. This would represent a market volume of €15.7bn, exceeding the pre-pandemic revenue peak (15.1) in 2018.

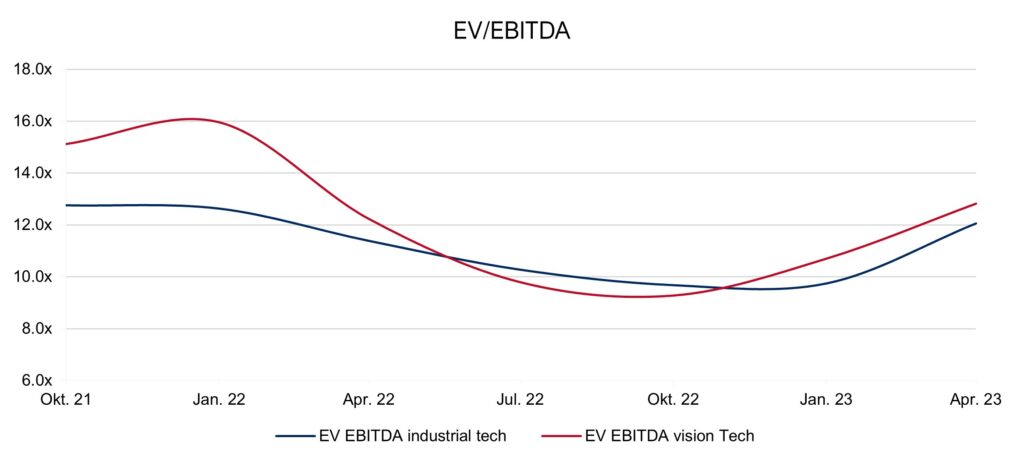

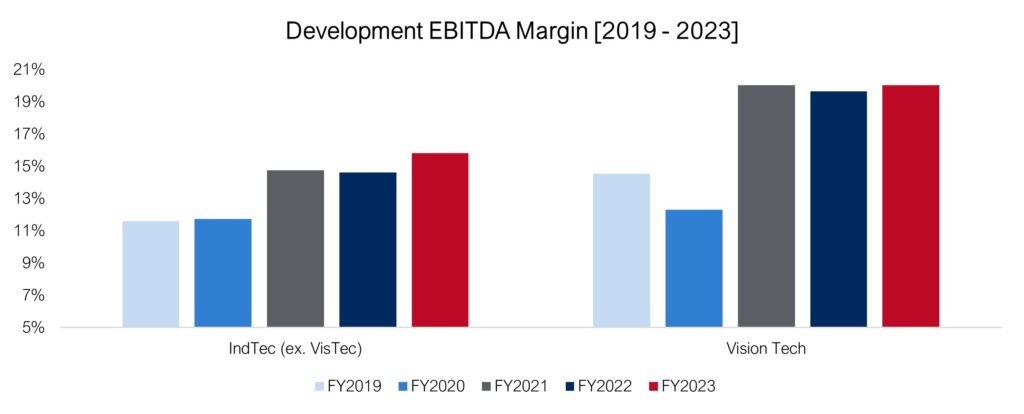

Following the overall stock market recovery since end of 2022, the Investec industrial tech indexes show EV/EBITDA levels back above 10x. It is interesting to observe that vision technology valuations showed relative strength compared to the overall index and are slightly higher. Again, as one would have to note, the lower than the general industrial tech index valuation for vision tech companies from July to October 2022 indeed was a rare exception in the recent past.

This picture is supported by the development of EBITDA margins of vision tech companies, showing a step back to levels of around 20% since 2021.

Despite challenges on multiple ends, there has been a decent number of vision tech related transactions in recent months. Apart from intra-European transactions both from strategic and financial sponsors (e.g., Antares, Marchesini, TKH, Avedon Capital, Ambienta) it should be noted that there was a good level of acquisition interest especially from US strategics in European service and technology assets. Active players included Bruker, Panacea Technologies, Microvision or Cognex, which acquired SAC Sirius Advanced Cybernetics, a transaction in which Investec advised the SAC shareholders in the sale.

Despite risks, which continue to exist, like geopolitical tensions or inflation from our discussions with market participants we take away the continuous high level of interest in attractive assets, which is based on long-term trends supporting the demand for innovative automation solutions in digital transformation or to cope with demographic developments, skilled workforce shortages and the need for more efficient and sustainable production.

Snapshot – SWIR imaging

Taking up our comments regarding hyperspectral imaging, we would like to share a few interesting perspectives recently provided by Yole about SWIR imaging. Although, still to be considered as a niche market with a bit more than 10k units sold globally, Yole estimates SWIR imaging to show a substantial above the market growth rates until 2028, supported by mainly three sectors: the industrial segment (CAGR 2022-2028 28%), due to demand development and price reductions. Second, the defense industry showing a CAGR of “only” 10%, now higher than in the last estimate (3%), as on the back of geopolitical tensions countries are expected to increase their military budgets and become interested in SWIR technologies. The biggest push is estimated to come from consumer applications, as from 2026 onwards, SWIR can probably start replacing NIR imagers in premium smartphones for under-display integration of facial recognition modules. This might drive a $2,074m market by 2028 (CAGR 2022-2028 86%). Currently, several emerging technologies compete to reach cost and performance requirements of large end markets. Besides the established players in the sensor and vision space there are a number of smaller players following different approaches (quantum dot, organics, Ge-based) who could attract M&A interest e.g., by large scale CIS suppliers.

The Investec Industrial Technology Index tracks daily developments in sectors such as Control Tech, Industrial Software, Integrated Providers, Engineering, Machinery, Vision Tech & Robots/Motions. The index includes valuations, growth projections, profitability margins and other metrics. You can find more information on our website and specific industry insights in our latest Systems Integration Report.

Investec has a senior sector team in Technology, who are experienced experts in selling, buying, and financing businesses.

If you have questions and would like to know more about valuations, buyer activity and current opportunities in the market – please get in touch: [email protected]

Backed by megatrend automation vision industry fights recession threat with innovation

Having collected fresh impressions on the 2022 VISION fair it’s only fair to state that the vision industry is well alive, introducing a variety of exciting new products, applications and technology, both from incumbent players as well as from start-ups. Apart from artificial intelligence powered vision another major application topic was (hyper) spectral imaging, which we already mentioned in one of the last Insights.

On the economical side the impacts of a multi-crisis ridden environment (pandemic, Ukraine war, component shortages, inflation/energy prices) leave their trace. However, backed by an ongoing strong order intake VDMA expects in 2022 a growth of 8% in sales (increased by +5% as estimated in early 2022) for the German machine vision industry, which is above the latest estimate for the overall Robotics + Automation sector (+6%) as well as the other two subsegments Integrated Assembly Solutions (+7%) and Robotics (+5%).

Despite short-term recession fears long-term growth perspectives are considered to be still highly attractive, based on ongoing digitization, increasing levels of automatization (in which vision applications are a key component) and high-quality demand in a more sustainable, high-tech production.

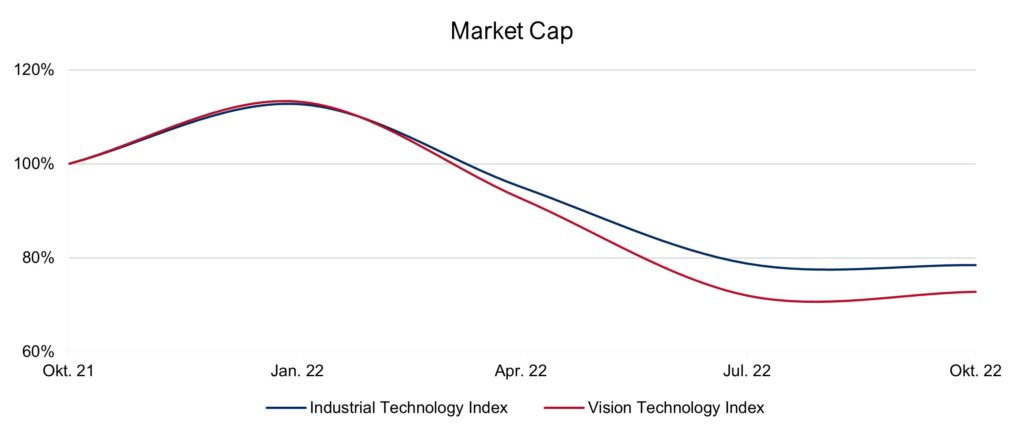

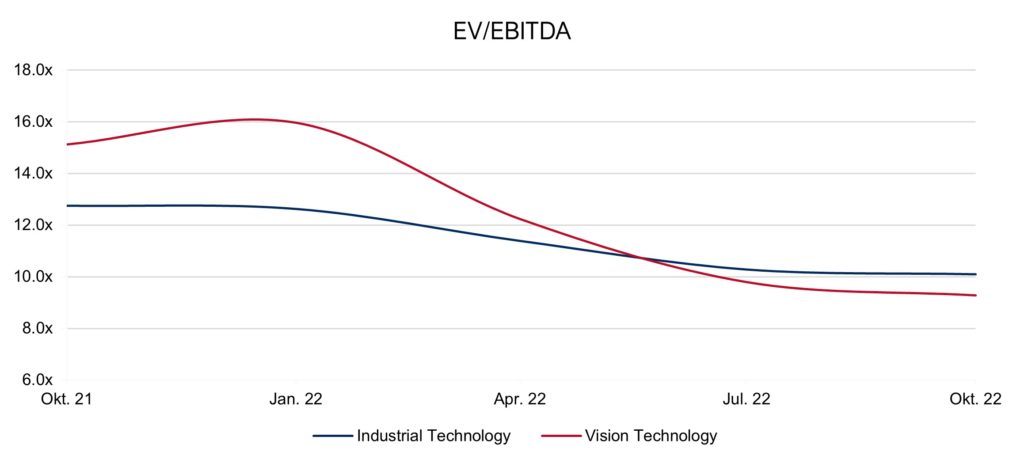

Looking at valuations, both our IndustrialTech and the VisionTech indexes reflect overall market development in terms of market cap since early 2022. Following the begin of the attack against Ukraine and increasing pressure on margins due to cost developments M&A sentiment has somehow slowed. Nevertheless, strategic rationales remain to be valid on many ends and we experience a continuous high level of buy-side interest both from strategic players as well as financial sponsors.

The trend observed at the end of the first half of the year with regard to EBITDA multiples has stabilized, i.e., vision tech companies apparently have suffered more compared to the overall industrial tech sector.

The trend observed at the end of the first half of the year with regard to EBITDA multiples has stabilized, i.e., vision tech companies apparently have suffered more compared to the overall industrial tech sector. Due to global developments already mentioned above, inflation has hit many of the large economies, leading to increased rates – close to 10% in the Eurozone compared to the same month in the previous year. The rapid rise in inflation rates is forcing central banks to act. The exit from an ultra-loose monetary policy has gained pace now in Europe as well: the ECB just announced a significant increase of interest rates for the second time in a row.

Due to global developments already mentioned above, inflation has hit many of the large economies, leading to increased rates – close to 10% in the Eurozone compared to the same month in the previous year. The rapid rise in inflation rates is forcing central banks to act. The exit from an ultra-loose monetary policy has gained pace now in Europe as well: the ECB just announced a significant increase of interest rates for the second time in a row.

Increased costs could have a negative effect on earnings and thus also on the company value. Low interest rates and monetary policy in general have contributed to the development of multiples used in business valuations, e.g., enterprise value/EBITDA and enterprise value/sales, have tended to rise in recent years. It can be assumed that these multiples will contract if interest rates increase – see above.

Even though the current environment is characterized by challenges, there are some response options or solutions for business owners. For example, the effect of increased costs can be mitigated through pricing strategies. Valuation multiples, on the other hand, could be supported by clever acquisitions. Positioning in innovative future topics such as sustainability/ESG, technology, automation, “softwarization” etc. also tends to have a positive effect. Financing costs are still relatively low from a historical perspective despite the latest increase. In the current environment, sellers of companies can still make good succession arrangements and secure attractive valuation levels.

The Investec Industrial Technology Index tracks daily developments in sectors such as Control Tech, Industrial Software, Integrated Providers, Engineering, Machinery, Vision Tech & Robots/Motions. The index includes valuations, growth projections, profitability margins and other metrics. You can find more information on our website at https://www.investec.com/advisory/industrials/

Investec has a senior sector team in Technology, who are experienced experts in selling, buying and financing businesses.

If you have questions and would like to know more about valuations, buyer activity and current opportunities in the market – please get in touch: [email protected]