Russia, China and the economic implications of the war in Ukraine

Investec recently hosted the Institute of International Finance (IIF) team for a panel discussion to talk about the Russia-Ukraine conflict, with reference to the global and emerging market spillover risks, impact on oil prices, China, emerging market flows and positioning.

We summarise some of the key aspects below.

Energy prices

One of the key areas of concern is the impact on energy prices on the world economy. The IIF team notes that historically, a 10% higher oil price would lower global GDP growth by 0.3% – although it should be borne in mind that energy intensity has declined over the past few decades.

This suggests that the risks of a global recession in 2022 are low. While it remains uncertain how long the war will last, a protracted and complex sanctions regime after the end of the conflict suggests that oil prices will remain higher for longer, with OPEC+ members likely to hold firm on maintaining slow oil output.

Sanctions on oil imports from Russia may however trigger higher oil prices, above US$130/bbl (vs. baseline forecast of US$100/bbl), although sanctions on Russian gas remain unlikely.

The IIF argued that higher oil prices, combined with higher gas prices, may lead to contraction in the economies of some European countries in 2022. For example, recent German IFO surveys imply a recession in Germany in the second half of this year. The inversion in the US yield curve inversion suggests that investors are concerned that the Fed’s tightening plans could choke off economic growth in the United States.

The IIF team highlighted four factors that imply weaker global growth in the near-term:

· Higher energy prices

· Tighter liquidity conditions

· Higher food prices

· Intensifying supply chain disruptions.

Russia itself is likely to be hit hard. The IIF forecast downside risks to Russian GDP of 15%, and upside risks to inflation of 15% this year.

While the Russian rouble may stabilise in the near term, the IIF argued in favour of further ruble depreciation, given a balance of payments crisis and an unlikely recovery in Russian exports in the medium-term.

Impact on South Africa

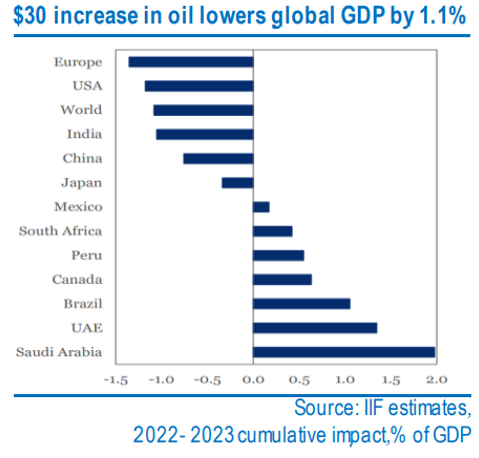

Yet, on a positive note, the IIF reiterated the countries, namely Saudi Arabia, UAE, Brazil, Canada, Peru and South Africa, that have benefitted the most amidst the fog of war, as higher non-fuel commodity prices have offset rising oil prices.

The SA Reserve Bank (SARB) raised rates by 25bp to 4.25% at its last monetary policy meeting, highlighting inflationary pressures. Yet the market pricing of future rate hikes appears aggressive to us. South African CPI recorded 5.7% year-on-year in February, yet is likely to reverse to the mid-point of the target range 3%-6% in 2023. Consequently, in our view, the SARB has scope to be dovish, in sharp contrast to most other central banks.

The rand screens among the best performing emerging market currencies during the war in Ukraine.

In sharp contrast to 2014, when several emerging markets had current account deficits of 4% or more of GDP, the position is much stronger this time around and we expect SA’s current account surplus to persist in 2022. Rhodium and palladium’s contribution to South Africa’s export basket has significantly increased over the past decade. We continue to argue that an inflationary rand appears unlikely, in sharp contrast to the position for other emerging markets.

SA bonds also screen attractive in an emerging market context. South Africa is rare among emerging markets, with a smaller fiscal deficit in 2022 than 2019. We upgraded SA bonds to overweight in early March, forecasting c.15% returns from SA bonds over the next 12 months.

Russia and China

In the medium term, a rebalancing of commodity supply chains remains likely. Interestingly, the Chinese share of Russian oil exports has increased over the years – from 5% in 2010 to 30% in 2020. However, in the near-term, China has signed contracts with the Middle East countries, including Saudi Arabia and Qatar, to provide them with oil and natural gas, limiting the potential need for a significant increase in Chinese imports of oil and gas from Russia.

China remains a wildcard. Weak credit growth, despite central bank efforts to stimulate the economy, suggests that there are early signs of Japanification (structural stagnation caused by an aging demographic). That said, on a more optimistic note, the IIF argued that the worst of the Chinese tech regulations may be behind us.

Except where otherwise stated, the views expressed were those of IIF and are not necessarily those of Investec.

You may also be interested in

Aviation Finance

Navigate the complexities of aircraft financing by choosing a partner that understands your business and the industry you serve.

Asset finance

Free up your cash flow and increase your liquidity. We provide asset finance, on a lease or rental basis, to fund your new and used assets on repayment plans that match your cash flow.

Supply chain finance

Let us help you tailor a unique, digital solution to unlock the potential that lies within your working capital on a leading global platform.

Aviation Finance

Navigate the complexities of aircraft financing by choosing a partner that understands your business and the industry you serve.

Asset finance

Free up your cash flow and increase your liquidity. We provide asset finance, on a lease or rental basis, to fund your new and used assets on repayment plans that match your cash flow.

Supply chain finance

Let us help you tailor a unique, digital solution to unlock the potential that lies within your working capital on a leading global platform.

Browse further in