Versterking van ons Industrial Tech & Services team

Investec heet Matthias Odrobina van harte welkom als Managing Director van ons European Business Advisory en als senior lid van het wereldwijde sectorteam dat Europa, het Verenigd Koninkrijk, Afrika, de VS en Azië bedient met onafhankelijk advies over grensoverschrijdende transacties.

Matthias beschikt over diepgaande sectorexpertise op het gebied van industriële technologie – met bijzondere aandacht voor smart industries, B2B-software en digitale transformatie.

Hij heeft 20 jaar ervaring als vertrouwd partner voor raden van bestuur en eigenaren op het gebied van fusies, overnames, desinvesteringen, financieringen en buyouts, met een bijzondere focus op de industriële sector, B2B-software en zakelijke dienstverlening.

Contact: Matthias Odrobina

How a professional dialogue is now moving companies forward

Interview with Thorsten Gladiator, Managing Partner of Investec about how a professional dialogue is now moving companies forward:

- Why companies should entertain a professional dialogue with their investors and lenders?.

- What other challenges are companies facing?

- As a financial expert and transaction specialist what advice do you have for companies when dealing with debt and equity investors?

- Giving an example.

This video answers these questions and give you an idea and overview in a few minutes.

Finding the right type of capital and investor to help grow your business

Our team has a long track record of successfully raising equity and debt capital and has the necessary expertise and networks:

- Raising capital to support business growth

- Securing capital from private equity and/or other Investors to support MBO/MBI projects

- Securing capital from private equity and/or other investors to manage changes in the shareholding structure (such as supporting the buyout of one or more shareholders and the reallocation of equity shares)

- Project financing: supporting companies in realizing essential investments or working capital

- Refinancing: supporting companies in reorganizing/reducing their debt burden

Investec is proud to announce that our French team is awarded as one of the Best Investment Bank – LBO Small to Mid Cap with a Silver Award at the recent Sommet des Leaders de la Finance in Paris.

Organised by Décideurs Corporate Finance, this event recognises excellence in corporate finance and highlights the work of professionals who lead complex and strategic transactions.

We warmly thank our teams for their dedication, and our clients for their continued trust.

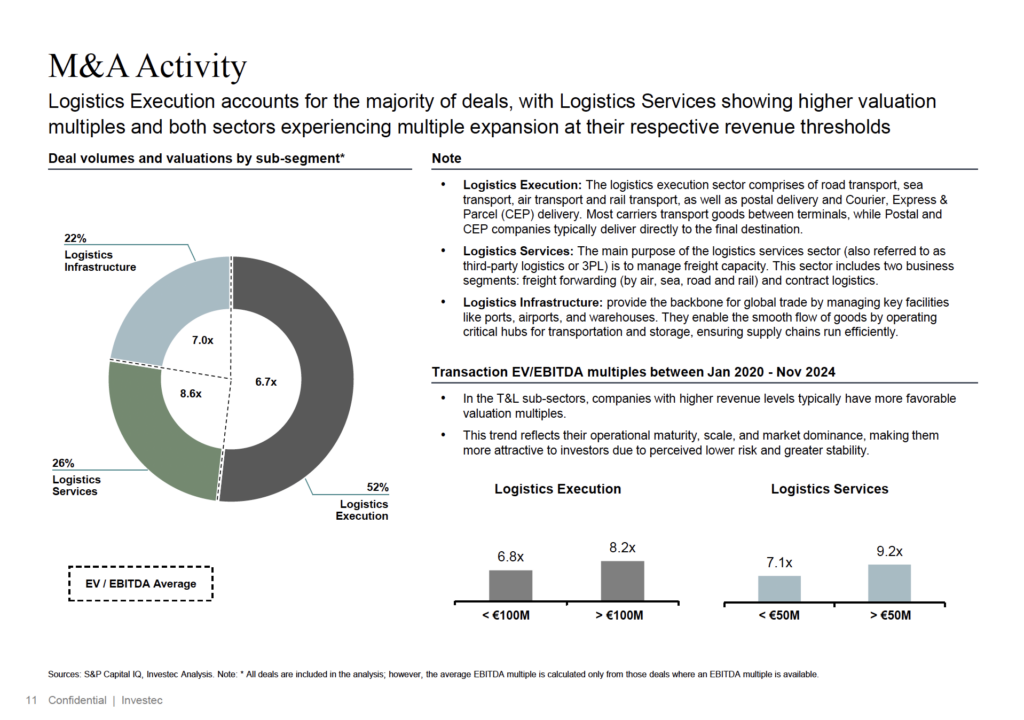

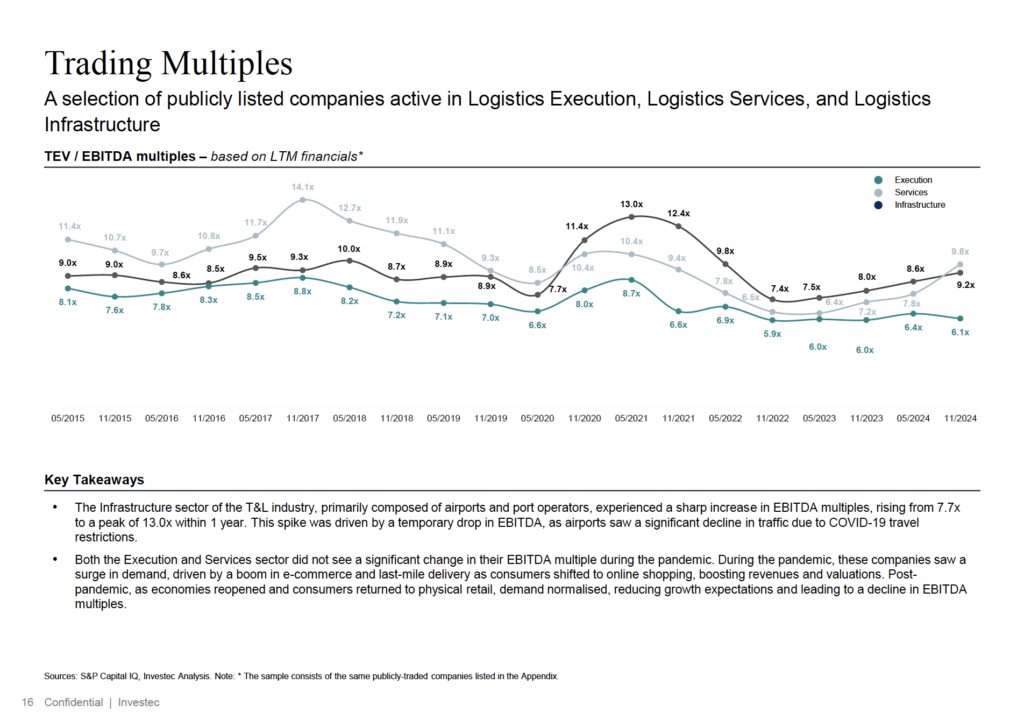

Trends in the T&L Market

The European T&L sector has seen robust M&A activity, with around 1,250 transactions recorded between 2020 and 2024. Market consolidation is driven by strategic buyers and private equity investors, particularly in logistics execution, services, and infrastructure. The UK, France, and the Nordics lead in deal volume. Companies with scalable operations and strong digital capabilities are often valued more highly, as investors prioritize assets that are well-prepared for future growth.

Benelux Market

Benelux remains a key hub for T&L M&A, ranking among the most active European regions for cross-border transactions. Approximately 60% of deals involve international buyers, with UK and Nordic investors being particularly active. The region’s strong logistics infrastructure, central location, and established trade networks make it an attractive target for strategic and financial buyers alike.

Private equity continues to play a significant role in market consolidation, with financial sponsors accounting for ~31% of acquisitions. This trend reflects growing investor interest in scalable logistics platforms and high-performing supply chain assets.

For more insights and our full 2024 T&L M&A report, please contact Jan Willem Jonkman.

Market trends, Financial operations, and Valuations in the Dutch Market

“The fundamental strength of the electrical engineering sector remains evident, propelled by the accelerating push for energy efficiency, the growing adoption of renewable energy sources, and the emergence of innovative technologies”

Marleen Vermeer – Partner Investec Benelux

This report provides an overview of market trends, Financial operations, and valuations in the Dutch Market.

To access and read the full report click here

Case Study

Aqseptence Group, a global leader in autonomous water and filtration technology, equipment and system solutions specialising in water treatment and liquid/solid separation, has attracted Oaktree, a leading global investment manager, as an investor.

Oaktree’s investment and expertise will provide Aqseptence Group with the necessary resources to continue to grow and innovate to best serve existing and new markets.

Interview with Baldassare La Gaetana, CEO of Aqseptence Group and Ervin Schellenberg, Managing Partner of Investec, taking us through the process and decision making of Oaktree’s majority investment in Aqseptence in a short video:

- What is the Aqseptence Group? Why a new shareholder?

- What is your sector and investor perception? – Opinion Ervin Schellenberg

- Why is it important to work with an M&A advisor? – Opinion Baldassare La Gaetana

- How was the collaboration with Investec?

For nearly 25 years, Investec has been assisting its clients in reaching their strategic goals, whatever it takes, whether it’s by securing a strategic business, or maneuvering and winning a competitive auction process:

We are particularly adept at advising on the following situations:

- Acquiring (family-owned) companies, groups, or other mid-market companies

- Acquiring subsidiaries or business units from (international) corporates, including carve-outs

- Acquiring businesses from a founder/(majority) shareholder, including succession

- Acquiring shares owned by a private equity firm, family office or other investors

Designing and executing such transactions is what our team does on a daily basis. To ensure success, our team also leverages its extensive experience and unique capabilities, which include: deal intelligence, tactical, technical and project management skills, negotiation skills, and an understanding of the personal interests/sensitivities of relevant stakeholders.

The Rheingau Music Festival is one of the largest music festivals in Europe and organises over 170 concerts every year throughout the region from Frankfurt and Wiesbaden to the Middle Rhine Valley.

Unique cultural monuments such as Eberbach Monastery, Johannisberg Castle, Vollrads Castle or the Wiesbaden Kurhaus as well as picturesque vineyards are transformed every summer into concert stages for stars of the international classical music scene and interesting up-and-coming artists from classical music and jazz to cabaret and world music.

In over 30 years, the Rheingau and its festival have become a centre of attraction for music enthusiasts from all over the world in a unique interplay of culture and nature, music, enjoyment and joie de vivre.

Investec is delighted once again to sponsor the Rheingau Music Festival 2024 and invites you to join us from 22 June to 7 September 2024!

A special feature this year? For the first time, there will be two opening concerts: Traditionally, the festival opens in the Eberbach Monastery, followed by another opening concert in the Kurhaus Wiesbaden. This year’s focus artists are also particularly outstanding: violinist Christian Tetzlaff, cellist Anastasia Kobekina, pianist Bruce Liu and jazz saxophonist Candy Dulfer.

Once again this year, various themes and focuses will ensure a varied and exciting programme. Under the motto “Spot on: Hollywood”, the world of film music comes to life in twelve concerts. Under the motto “Brazil!”, the contrasts and beauties of the country will be explored musically. The programme is also dedicated to the works of Antonín Dvořák and a true classic: Vivaldi’s “Four Seasons”.

The stages of the 37th festival season will be graced by numerous stars from the worlds of classical and pop music. Highlights include star pianist Lang Lang, singers Álvaro Soler, Max Mutzke and Max Giesinger, violinist Anne-Sophie Mutter, opera singer Rolando Villazón and entertainer Eckart von Hirschhausen.

Investec has been a committed sponsor of the Rheingau Music Festival for more than 15 years. This long-standing partnership is characterised by our deep appreciation for the arts and a strong connection to local culture. We look forward to experiencing a rousing summer full of music together with you again this year.

You can view the detailed program here.

Digital Disruption and Strategic Consolidation: Navigating the New Frontier in Industrial Services

Global Industrial Service

Technologization and Electrification along the full asset lifecycle to increase efficiency in industrial services and processes and comply with CO2 emission regulation.

Industrial Service Valuation drivers

The valuation of industrial services is primarily influenced by three pivotal factors. An increased involvement in the asset lifecycle and the ability to manage complex assets significantly enhance valuation metrics. Moreover, the intricacy of the service offered, and the dynamics of the target market further underpin these valuations. There is a notable shift towards a more comprehensive degree of asset stewardship, ranging from deploying personnel capable of operating the assets on-site to achieving full autonomy in asset management, thereby enhancing and operating the assets entirely independently from the end-user. Specifically, sectors such as energy and chemicals necessitate sophisticated services and assets, due to their inherent complexity and the critical nature of their operations.

Investec has extensive experience in advising deals in the Industrial Service sector. With 25 focused dealmakers across Europe, we can help you to achieve your strategic ambitions.

Interview

As we enter 2024, the M&A landscape shows signs of recovery, albeit cautiously.

In the episode of the February 20, 2024 of No Ordinary Wednesday, Jeremy Maggs in conversation with Investec experts Jürgen Schwarz, Marleen Vermeer, and Kilian de Gourcuff, Investec’s Head of Cross-Border Finance and International Advisory Charles Barlow, on what key sectors, trends and risks to keep an eye on in 2024.

Click below to listen to the podcast:

Where does opportunity lie for dealmaking in 2024? (investec.com)

Hosted by seasoned broadcaster, Jeremy Maggs, the No Ordinary Wednesday podcast unpacks the latest economic, business and political news in South Africa, with an all-star cast of investment and wealth managers, economists and financial planners from Investec. Listen in every second Wednesday for an in-depth look at what’s moving markets, shaping the economy, and changing the game for your wallet and your business.

Listen to the best of No Ordinary Wednesday: https://www.investec.com/en_za/focus/no-ordinary-wednesday-with-jeremy-maggs.html

Innovatie en duurzaamheid omarmen: de toekomst van de TIC-sector

Als langetermijnadviseurs van de TIC-sector organiseerde Investec | Investec in maart 2023 onze inaugurele Europese TIC-conferentie. Leiders uit de sector schoven aan voor een levendige discussie over de toekomst van de sector – inclusief digitalisering, duurzaamheid en fusies en overnames.

Bekijk en lees de hoogtepunten van onze eerste Europese TIC-conferentie

De sector Testing, Inspection & Certification (TIC) speelt al lang een centrale rol bij het leveren van kwaliteits- en veiligheidscontrolediensten om mensen en het milieu waarin wij leven te beschermen. Nu zijn er verschillende transformerende trends die de kansen in de sector vergroten.

Om de discussie over deze trends te vergemakkelijken, organiseerde Investec Investec op 9 maart 2023 onze inaugurele TIC-conferentie. Paul Hesselink – CEO Kiwa; Hervé Montjotin – CEO Socotec; en Mark Williams – Partner Inflexion; gaven ons hun visie op de veranderende dynamiek van de sector.

Door de aanhoudende M&A-activiteit van zowel private equity als handelsconsolidators zijn de waarderingsveelvouden de afgelopen 5 jaar aanzienlijk gestegen. De aanhoudende aantrekkingskracht voor beleggers werd ondersteund door het versterkte regelgevingslandschap in diverse sectoren, naast specifieke groeistimulansen binnen diverse afzonderlijke subsectoren.

Wij blijven zien dat buy-and-build strategieën een belangrijke rol spelen bij het aanjagen van de groei, aangezien de gevestigde spelers de voordelen van schaalgrootte willen benutten om een groot aantal subsectoren aan te pakken en verdere synergieën te ontsluiten.

Bij de bespreking van de toekomst van de TIC-sector kwamen herhaaldelijk drie gemeenschappelijke thema’s naar voren.

Onafhankelijke verificatie voor ESG

De sector is sterk verweven met de groeiende behoefte aan strengere milieu-, sociale en bestuursnormen bij bedrijven. Nu bedrijven in toenemende mate hun ESG-certificaten willen promoten, beschuldigingen van greenwashing willen vermijden en aan nieuwe Europese regelgeving willen voldoen, zal de TIC-sector een cruciale rol spelen, niet alleen bij het verifiëren van ESG-normen, maar ook bij het bieden van begeleiding om bedrijven te helpen bij deze vaak complexe kwesties.

Hervé Montjotin bevestigde de groeiende vraag naar onafhankelijke verificatie: “Wat duurzaamheid betreft, moeten mensen worden gerustgesteld door een betrouwbare derde partij, zodat wij veel waarde kunnen toevoegen en greenwashing kunnen helpen voorkomen.”

Mark Williams benadrukte de noodzaak om te testen op onvoorziene gevolgen nu bedrijven proberen de duurzaamheid van producten te verbeteren. Hij zei: “We gebruiken verschillende materialen om dingen beter en efficiënter te maken, maar deze moeten worden gecontroleerd om ervoor te zorgen dat wat is gemaakt duurzamer is en dat we er niet over 15 jaar achter komen dat er negatieve gevolgen zijn.”

Paul Hesselink merkte op dat TIC-kantoren niet alleen zorgen voor duurzaamheid en ESG-naleving voor hun klanten, maar ook hun eigen prestaties meten aan deze doelstellingen: “Carbon dioxide footprinting, gender diversity indices … we meten deze niet alleen voor onze klanten maar ook voor ons eigen bedrijf – walking the talk en laten zien dat we waarmaken wat we preken.”

De digitaliseringsuitdaging

Zoals in vele sectoren is de digitaliseringstrend – die digitale, gegevens- en nieuwe technologieën omvat (met name sensoren, draagbare instrumenten en het internet der dingen) – voor de TIC-sector een transformatie van interne processen, bedrijfsmodellen en diensten. Ons panel erkende de invloed van digitale hulpmiddelen op de productiviteit en de winstgevendheid.

Zij waarschuwden echter dat het tempo van de potentiële digitale ontwrichting wordt afgeremd door het conservatisme van de sector en de terughoudendheid van de regelgeving. Regelgevers eisen bijvoorbeeld nog steeds persoonlijke inspecties in plaats van het gebruik van digitale hulpmiddelen. Het panel was het erover eens dat de sector een stap voor moet blijven op het gebied van technologie, zodat hij klaar is wanneer zijn klanten en de regelgevers dat zijn, maar erkende dat het onwaarschijnlijk is dat de sector een voortrekker van verandering zal zijn.

Uitbreiding in een klimaat van stijgende rente

Iedereen was het erover eens dat het huidige economische klimaat nieuwe uitdagingen met zich meebrengt, met name op het gebied van fusies en overnames. Mark Williams wees erop dat hogere financieringskosten sommige vormen van fusies en overnames zouden kunnen afremmen, maar merkte op dat “er nog steeds vraag is naar kwaliteitsplatforms en dat er nog steeds ondernemers zijn die willen verkopen.” Hij voegde eraan toe dat de focus op hoge marges bijzonder belangrijk is voor veel private equity-kopers.

Paul Hesselink grapte dat hogere rentevoeten de private equity concurrentie zouden moeten helpen afschudden, en merkte op dat “industriële en private equity kopers een verschillende dynamiek hebben – industriële kopers kunnen minder marge gedreven zijn omdat ze meer tijd hebben om een bedrijf te ontwikkelen als het de juiste culturele fit is.”

Hervé Montjotin voegde eraan toe dat zijn bedrijf naar een meer wereldwijde expansiestrategie heeft gestreefd omdat dit de cyclische risico’s kan helpen verlichten. Hij zei dat de sector weliswaar “cyclisch is, maar dat die cycli vaak op het binnenland gericht zijn en dat een wereldwijde balans dergelijke risico’s kan helpen verminderen.”

Mark Williams vatte tot slot samen waarom de TIC-sector een aantrekkelijk vooruitzicht blijft voor fusies en overnames: “We hebben de sector zien evolueren en een gestage groei zien handhaven; hoewel de thema’s zijn veranderd, is het concept van het veiligstellen van het leven en de toekomst van mensen hetzelfde als 50 jaar geleden. Daarom zal de sector blijven overleven omdat we de wereld om ons heen moeten beveiligen.”

Download onze presentatie

Interesse voor het evenement van volgend jaar? Neem contact op met Marleen Vermeer

De Europese M&A-markt in de sector Transport & Logistiek blijft gedreven door M&A-activiteit en consolidatie in alle marktsegmenten. Verschillende serie-overnemers blijven de motor achter de consolidatie in het VK, DACH, Frankrijk, Scandinavië en de Benelux.

Logistieke diensten worden in hoog tempo aangepakt

Het transport & logistiek deal landschap in Europa heeft 1.367 geregistreerde transacties bereikt in de periode 2016 – H1 2022. De transactieactiviteit wordt voornamelijk gedreven door een groot aantal overnames in het wegvervoer (24,3%) en een snel groeiend aantal transacties in de subsegmenten expeditie (22,4%) en contractlogistiek (14,6%).

Toenemend aantal financiële kopers stimuleert fusies en overnames

Private Equity-investeerders waren betrokken bij 21% van alle transacties in H1 2022, wat aanzienlijk hoger is dan de 9,5% in H1 2021. De toenemende belangstelling van financiële kopers in deze sector is te wijten aan de fragmentatie van de markt en de waarderingskloof tussen grote en kleine T&L-bedrijven.

Meer grensoverschrijdende overnames

De transactieactiviteit in de sector Transport & Logistiek wordt ook gedreven door meer grensoverschrijdende overnames, vooral in de Benelux. Zowel Europese kopers als niet-Europese kopers uit de VS, Canada, het Midden-Oosten en Afrika hebben deze trend gestimuleerd.

Aanzienlijke M&A activiteit in de Verhuursector

Er zijn aanzienlijke fusies en overnames geweest in de verhuursector met multiples tot 10x EBITDA. De sterk groeiende markt in combinatie met de complexiteit, de engineering en het maatwerk van de oplossingen drijven de marges op. Deze factoren stimuleren ook de waarderingsveelvouden, naast de recurrente aard van de activiteiten.

Belangrijke inzichten

De European Rental Association (ERA) schatte de sector in 2018 op €26 mrd. De wereldwijde markt wordt geschat op 93 miljard dollar (2019) en zal naar verwachting groeien met bijna 5% per jaar tot 2027. De grootste markt in Europa (hoewel niet de sterkste groeier) is het VK. Frankrijk en Duitsland zijn de twee andere grootste markten in Europa en behoren ook tot de sterkst groeiende. Daarnaast groeit de Nederlandse markt gelijk aan de totale Europese markt, met een groeipercentage van 4,4%.

Het gebruik van huuroplossingen is nog steeds het sterkst in de markt voor (bouw)materieel. Hoewel we zien dat huuroplossingen zich ook uitbreiden naar andere markten, zoals kantoorapparatuur en industriële en consumentenmarkten.

De belangrijkste motoren voor groei in de huursector zijn:

- De markt groeit sneller dan de algemene economie;

- De toegenomen regelgeving rond veiligheid vraagt om de nieuwste up-to-date oplossingen;

- Toenemende penetratie van huren in plaats van kopen als gevolg van beter gebruik van kapitaal en focus op Total Cost of Ownership besluitvorming;

- Toegenomen erkenning van de rol van verhuur bij het waarborgen van duurzame oplossingen;

Langetermijntrend naar de ‘sharing economy’.De waarderingsmultiples liggen doorgaans rond 7,5x EBITDA, waarbij spelers die zich richten op meer en/of relatief zeldzame complexe oplossingen de hoogste multiples ontvangen. Bovendien, hoe meer recurrente activiteiten, hoe hoger de multiples. Beursgenoteerde bedrijven worden gemiddeld 10x EBITDA gewaardeerd.

Het beheer van de kwaliteit van de (verhuur)vloot is essentieel: onderhoud, vervangingskapitaal en uitbreidingskapitaal.

De test-, inspectie- en certificatiemarkt, kortweg TIC, staat steeds meer bekend als TICC, waarbij Compliance als een belangrijke nevenactiviteit wordt toegevoegd, met assurance als de implementatieprocessen, waarbij wordt nagegaan of aan de Compliance-eisen is voldaan.

De COVID-impact op de TICC-markt

Als we kijken naar de COVID-impact op de markt, zien we dat TICC het erg goed doet in vergelijking met andere sectoren. Binnen de TICC-ruimte zien we dat de inspectieactiviteiten enigszins zijn beïnvloed omdat deze voornamelijk ter plaatse worden uitgevoerd. Certificatie is vrij stabiel, terwijl Testing en Compliance zeer sterk zijn en groeien in deze COVID-omgeving. Testen is uiteraard het gevolg van de toename van het aantal COVID-tests/labs en de toename van het testen en certificeren van medische apparatuur, waaronder ventilatoren en maskers, terwijl naleving/verzekering kritischer is geworden. Er is een grote vraag naar meer end-to-end zichtbaarheid en risicobeheer in toeleveringsketens. Bovendien proberen bedrijven voorbereid te zijn op mogelijke toekomstige gevolgen van strengere regelgeving en normen*.

Binnen Compliance zien we de volgende segmenten:

- EHS (milieu, gezondheid en veiligheid): COVID-19 verhoogde de EHS-naleving door trends als thuiswerken (werkgevers zijn verantwoordelijk voor gezondheids- en veiligheidsaspecten van thuiskantoren) en de invoering van hoogwaardige hulpmiddelen zoals platforms voor webconferencing. Bovendien blijft de naleving van de wetgeving inzake klimaatverandering en de toegenomen regelgeving inzake milieu en duurzaamheid sterk;

- Industriële en openbare veiligheid: De markt voor openbare veiligheid is een markt met sterke groei. Ook hier heeft COVID zijn impact gehad, met bescherming van first responders en uitdagingen rond quarantaine-eisen. Bovendien genereert digitale technologie innovatieve oplossingen die borgingsprocessen vereisen. Aan de industriële kant stimuleren een toename van de veiligheidsvoorschriften en het gebruik van Internet of Things (IoT)-toepassingen de markt voor industriële veiligheid;

- ESG (Environmental, Social en Governance): Binnen ESG-factoren wordt de maatschappelijke verantwoordelijkheid (inclusief diversiteit, politiek en publieke druk) steeds belangrijker, evenals de verschuiving van ’teruggeven aan de maatschappij’ naar het volledig opnemen hiervan in de cultuur van bedrijven. Het verhogen van de prestaties van ESG-factoren om de reputatie en het merk van het bedrijf te verbeteren, zien we ook de digitaliseringstrend die de naleving stimuleert;

- (Cyber)beveiliging & IoT: Een meerderheid van de bedrijven die bezig zijn met de implementatie van IoT / cybersecurity krijgt te maken met incidenten daaromheen, waardoor de relevantie van compliance op dit onderwerp uiterst belangrijk wordt;

- Finance, Legal & Tax: toegenomen regelgeving rond bankieren, alternatieve financiering, privacy, KYC-regelgeving etc;

- Risicobeheer (software): de wereldwijde markt voor risicobeheersoftware werd in 2019 gewaardeerd op 7 miljard dollar** en zal naar verwachting groeien met een CAGR van 19%. De belangrijkste groeidrijvers zijn de steeds complexere regelgeving, toenemende data & beveiligingslekken, groeiende FinTech en IoT-innovaties.

De aan te spreken TIC-markt wordt geschat op 95 miljard euro (47% van de totale TIC-markt, inclusief interne TIC-activiteiten) en zal naar verwachting groeien met een CAGR van 5%. Zoals beschreven in ons meest recente TIC-rapport, veranderen technologieën, gegevens en digitalisering de TIC-sector en stimuleren ze de opkomst van nieuwe bedrijfsmodellen. Naarmate de TIC-markt de technologie omarmt, ontwikkelen zich snel bedrijfsmodellen op basis van abonnementen. TIC-oplossingen worden essentiële digitale instrumenten binnen de bedrijfsactiviteiten, die end-to-end zekerheid bieden voor kwaliteit, veiligheid, beveiliging, compliance en duurzaamheid van activiteiten en producten.

Een succesvol voorbeeld van compliance/assurance in de TICC-markt is het bedrijf Foodchain. Zij investeren in het leveren van blockchain-based assurance om voedselproducten ‘from farm to fork’ te track & tracen. Een ander voorbeeld is KTBA een strategische sparringpartner in hoogwaardige Quality Assurance, Riskplaza & Business Assurance diensten in de food en consumer goods industrie.

Recente overnames van spelers die in Compliance investeren zijn:

- In 2020 kondigde CGE Partners de overname aan van Enhesa, een wereldwijd platform voor informatie over milieu, gezondheid en veiligheid (“EHS”), van Waterland;

- Medio 2019 heeft Alcumus, een toonaangevende Britse aanbieder van softwaregeleide risicobeheeroplossingen, gesteund door de private equity-onderneming Inflexion, een meerderheidsinvestering afgerond in eCompliance, een in Canada gevestigde SaaS-onderneming op het gebied van veiligheid op de werkplek;

- Ook medio 2019 heeft Mérieux NutriSciences KTBA overgenomen;

- Begin 2019 neemt SAI het platform voor naleving van regelgeving Bwise over van NASDAQ voor vergelijkbare veelvouden.

- Intertek heeft in augustus 2018 Alchemy, een toonaangevende leverancier van SaaS-gebaseerde People Assurance-oplossingen, overgenomen voor 7,2x de huidige jaaromzet en 22x de huidige EBITDA.

- In 2018 heeft ProPharma Group, een wereldwijde marktleider in uitgebreide compliance diensten en een portfoliobedrijf van Linden Capital Partners, Xendo overgenomen, een in Nederland gevestigde leverancier van compliance consulting, engineering & technische ondersteuning, regulatory affairs en pharmacovigilance diensten aan de (bio)farmaceutische industrie, medische apparatuur en gezondheidszorg.

In het algemeen zien wij dat in de compliance-sector relatief hoge multiples met dubbele cijfers worden betaald.

Ook Private Equity richt zich steeds meer op het thema Compliance & Risicomanagement. Als voorbeeld heeft Riverside (een wereldwijde Private Equity firma) aangekondigd begin 2021 als onderdeel van haar thematische investeringsstrategie een focus te leggen op Safety, Security, Compliance & Risk Mitigation. “Bedrijven in deze ruimte helpen klanten om risicovolle uitkomsten te voorkomen of te minimaliseren. In een steeds complexere wereld met een verscheidenheid aan bedreigingen voor gezondheid en veiligheid, zijn bedrijven die risico’s beperken of elimineren over het algemeen goed gepositioneerd om te slagen.” Daarnaast verwierf Navis Capital Qima, kwaliteitscontroles en audits voor de naleving van leveranciersvoorschriften voor consumentenproducten (met name textiel, elektronica, speelgoed) en levensmiddelen.

Waarom Investec?

Een goed voorbeeld van één van Investec’s recente transacties in deze ruimte is de overname van KTBA door Merieux Nutrisciences. KTBA is een toonaangevende en betrouwbare adviseur in kwaliteit & bedrijfszekerheid en label compliance in de voedingssector.

Op basis van deze observaties zien we een behoorlijke vraag van kopers in deze ruimte die zich richten op het Compliance element binnen TICC en we verwachten meer transacties in deze ruimte in de komende jaren. Voor meer informatie kunt u contact met ons opnemen.

* Bron: OC&C TICC analysis report 2020 &

** Bron: Risk Management Market Size, Share and Trends | Forecast- 2027 (alliedmarketresearch.com)

With Europe still being the dominant M&A geography in the TIC market (48% of the targets acquired in the last decade were located in Europe), North America is the second largest region (34%) . A large part of the buyers who acquired a business in North America are headquartered in Europe.

North American TIC market

The North American TIC services market is estimated around $ 30bn and is projected to grow by a CAGR of 6%. The growth is related to stringent government regulations and standards in the US. Globalization has led to an increase in global trade agreements, resulting in the growth of TIC services for production companies that need to comply with international standards. Among the main growth drivers of the US TIC market are the growing demand for tech-enabled TIC solutions, popularity of IoT and rise in emphasis towards reducing equipment and machinery downtime (asset management). Moreover, in February 2019, the U.S. FDA announced a new strategy for monitoring and inspecting food imports. Besides, the growth is a result of increased outsourcing of TIC services due to the fact that it becomes more complicated, technical and cost effective, for companies to perform these tests in-house due to the stringent regulatory standards.

Transactions with a US target involved

The testing market has dominated the North American TIC market with 65% market share, related to the growing concern among consumers regarding the quality of products. This is also visible in the type of transactions with a US target involved. Also 65% of all transactions with a US target involved where laboratories and other Testing activities, compared to 18% in Inspection and 4% in Certification (remainder of the transactions where consultancy/training/software related). Since certification services is actually the largest growing market in the US, by a CAGR of 9%, we expect a shift here in number of transactions per business line, although certification will still remain a small segment and pure certification players are rare.

Some examples of recent transactions in the US are:

Beginning 2020, SGS acquired Thomas J. Stephens & associates inc.. Stephens is a nationally recognized clinical research organization serving the cosmetic and personal care industry. It is a leading provider of safety & efficacy testing and contract research services, generating $ 15m in revenues. This acquisition expands SGS’s Consumer & Retail service portfolio in the clinical testing sector for cosmetic and personal care products in the USA.

In 2019, Socotec, a leading European company of testing, inspection and certification services, #1 in technical control in the construction field in France strengthened its international position by acquiring Vidaris in the US. Vidaris is a provider of specialty consulting services within the architecture, engineering and construction industries focusing on high-performance buildings and specialty structures. Through an integrated, holistic approach, our professionals provide solutions for building envelope, energy efficiency, sustainability, dispute resolution, code compliance and construction advisory projects. Vidaris employs over 300 professionals in 15 offices.

In 2018 Bureau Veritas completed the acquisition of EMG Corporation (EMG), a US leader in construction technical assessment and project management assistance, asset management assistance and transaction services, generating € 70m in revenues. A more recent transaction in 2019 was the acquisition of Owen Group. Owen provides buildings and infrastructure asset management and project compliance services including ADA accessibility compliance, deferred maintenance compliance, commissioning, and code compliance, generating around $ 7m in revenues .

In 2019 Dekra has expanded its mechanized and industrial inspection business in the United States through the acquisition of JAMKO’s business operations based in Lyons, New York. JAMKO specializes in remote mechanized visual inspection in nuclear and municipal markets.

Eurofins acquired Test America end of 2018. Test America, which became part of JSTI through its acquisition in September 2016, operates an integrated network of 24 full service testing laboratories and 40 service centres throughout the USA, generating over $ 230m in revenues. Test America expanded the footprint and complement the service offering of Eurofins’ Environmental Testing Business in the USA.

We also see more Tech-enabled TIC companies being acquired. In 2018 for example Intertek expanded its global Assurance business with the acquisition of Alchemy, a leading provider of SaaS-based People Assurance solutions for a total value of $ 480m.

Buyers mainly from Europe

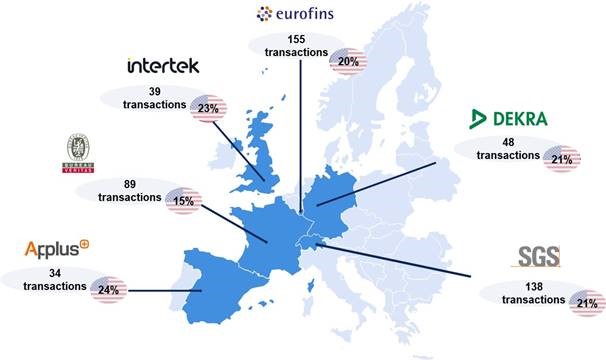

In general the majority of the large TIC players are headquartered in Europe. As you can see in our recent Insight blog (TIC Industry shows considerable M&A activity as growth & innovations stimulator) Eurofins and SGS are the leading acquirers in terms of number of transactions.

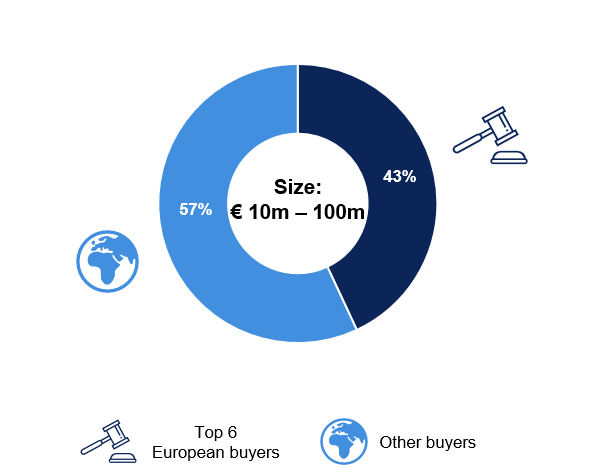

The top 6 European buyers were responsible for 43% of the transactions with a US target involved

(as % of all deals with US targets of which revenue size was known).

Based on our database including over 1,600 TIC transactions over the last decade, almost 500 transactions were deals involving a US based target. Of these 500 transactions over 100 targets were acquired by the large European TIC players, Eurofins and SGS being the leading buyers with 31 acquisitions in the US versus 29. Bureau Veritas, Dekra, Intertek and Applus were also actively looking overseas for interesting US based targets.

Relatively seen, the large European TIC players were involved in a US based acquisition in up to 24% of their transactions closed. We see that this percentage is much higher for larger transactions, around 40 to 50% for acquisitions of targets between € 50 and € 100m revenues. For the coming years we expect an increase in the number of deals with a US based target involved. Several companies mention North America as one of their priorities. Bureau Veritas explicitly mentions “expansion in North America is a priority for the Bureau Veritas 2020 Strategic Plan. Today in North America, the Group has over 7,500 employees and generates 15% of its total revenue”. While Eurofins states “Eurofins provides the North American market with complete analytical solutions supported by a commitment to excellent customer service, high-quality standards, and scientific expertise. Our objective is to be the bioanalytical company of choice in the US”.

Extra rationale behind transactions for European buyers

EEuropean buyers have an important rationale and driver behind a transaction in the US. A recent study based on 2019 transactions, shows that in 46% of the cases entry into new markets is an important driver behind the acquisition. This applies to the TIC market as well, where the large European players prefer entering a new (US) market via a Buy&Build versus organic growth. The study shows another reason in 41% of the cases: acquiring know-how or a team as the rationale behind a transaction.

US-based TIC buyers

Another interesting conclusion is that there has been relatively more PE involvement in acquiring TIC companies in the US compared to globally. In over 11% of deals with a US target, a Private Equity firm was the buyer versus 8% of the deals when looking at all TIC transactions on a global scale.

One of the largest buyers is US -based UL. The majority of the targets UL acquired were located in the US (51%) and mainly focused on Building & Infrastructure and IT segments. Although UL looks for targets overseas as well, like the recently acquired UK-based Wintech, that offers testing and certification services for the building and construction industries.

The more specialised TIC company Food Chain ID, owned by PE firm Paine Schwartz Partners acquired several Food TIC businesses, like the acquisitions of Diversified Laboratories and Decernis. They also look overseas to acquire businesses, like the acquisition of Quality Partner in Belgium mid-2018 and 6 months earlier an acquisition in Italy (Bioagricert).

A more hybrid example of European/US initiative is the recent $1.8 billion investment in 33% of the shares of the European TIC company Socotec (backed by Belgian family office Cobepa) by New York based Private Equity firm Clayton, Dubilier & Rice.

Sources: Investec proprietary TIC transaction database, Graphical Research, Global Market Insights, Business Wire, CMS

Financial restructuring for Shareholders & Lenders

Helping clients to navigate uncertainties while putting their businesses back on track

Interview with Jürgen Schwarz, Managing Partner of Investec about Restructuring with the help of a M&A process:

- How did the market change in recent years?

- What is your approach?

- Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

Sale from insolvency

Due to our pan-European presence and track record we are well placed to advise on international and cross-border restructurings.

Our international sector teams implement more than 50 transactions p.a. and in many sectors they know the active buyers, the acquisition criteria, the behaviour of individual decision makers. We also have an up-to-date overview of the market prices paid, which vary considerably over time and depending on the positioning in the sector.

Investec has direct access to numerous international equity and debt capital providers and has carried out numerous restructurings ranging from approximately 10 million Euros to several billion Euros.

You know your company best but selling it to a suitable buyer at an attractive price is often a major challenge.

Interview with Ervin Schellenberg, Managing Partner of Investec about finding the right partner for medium-sized companies:

- How to find the right partner for a medium-sized company?

- Is my company ready for a transaction?

- What is the equity story?

- Giving an example

This video answers these questions and give you an idea and overview in a few minutes.

Our wealth of experience from many years of successful transactions and our access to relevant decision-makers in national and international buyers ensure the best possible result for you.

Investec has the core competences required to sell companies and has successfully completed hundreds of transactions across all major industries.

Financiering en markttrends | 2023

Waarom de Duitse industrie grote behoefte heeft aan investeringen.

De Duitse industrie staat voor grote uitdagingen, waaronder de effecten van digitalisering, de verschuiving van analoge naar digitale bedrijfsmodellen, de behoefte aan milieubeschermende maatregelen en duurzame productieprocessen, evenals demografische veranderingen, die leiden tot een tekort aan geschoolde werknemers en een vergrijzende beroepsbevolking. Om deze processen succesvol te beheersen, zijn aanzienlijk hogere investeringsinspanningen nodig dan in het verleden.

Digitalisering en Industrie 4.0: Op dit moment staat Duitsland op zijn best in de middenmoot van de EU wat betreft het gebruik van digitale technologieën in de economie1. De Duitse industrie moet investeren in digitale technologieën en automatisering om concurrerend te blijven. Maar om de achterstand op vergelijkbare landen in te lopen, zouden de investeringen in IT en digitalisering in Duitsland moeten verdubbelen of verdrievoudigen van 49 miljard euro naar 100 tot 150 miljard euro per jaar. Alleen al in het mkb zouden de uitgaven voor digitalisering moeten stijgen van 18 miljard euro in 2019 naar 35 tot 50 miljard euro per jaar.

Duurzaamheid en milieubescherming: Bedrijven richten zich steeds meer op milieuvriendelijke technologieën en processen om hun duurzaamheidsdoelstellingen te halen en hun impact op het milieu te verminderen. Deze investeringen dienen niet alleen om het milieu te beschermen, maar dragen ook bij aan het concurrentievermogen op lange termijn. Een recente studie in opdracht van KfW schat de klimaatbeschermingsinvesteringen die nodig zijn om de doelstelling van klimaatneutraliteit tegen 2050 te bereiken op ongeveer 5 biljoen euro of ongeveer 190 miljard euro per jaar1. Dit enorme bedrag maakt duidelijk dat er aanzienlijk grotere inspanningen nodig zullen zijn om de doelstelling te halen dan tot nu toe het geval is geweest.

Lees de volledige insight hier.

Thorsten Gladiator, Managing Partner Investec: As corporate finance advisors, we see the importance of ESG in general and sustainability aspects in particular in almost every transaction, both in M&A situations and in financing mandates.

Equity and debt investors place a strong focus on ESG compliant investments in the interest of their financiers and / or due to investment criteria that are binding for them.

For business sellers as well as CFOs, this has pricing and process consequences:

- A clearly defined and documented ESG strategy creates confidence among investors and the company’s other stakeholders

- The same applies to the (early) implementation of legal requirements for sustainability reporting (CSRD)

- A focus on sustainability aspects provides positive differentiation features compared to competitors and can thus have a value-creating effect

- The lack of a corresponding strategy can lead to price discounts in the valuation as well as higher financing costs

- In the due diligence phase of a transaction, lack of ESG information leads to prolonged processes, higher management burden and the withdrawal of investors with clearly defined ESG investment criteria

The following article from AIM – Advice in Motion highlights the various aspects for medium-sized companies and shows examples of successful ESG strategies.

Opportunities and challenges of sustainability for smaller and medium-sized enterprises

The sustainability performance of a company today is the decisive factor for its competitiveness tomorrow. In this context, medium-sized companies in Germany in particular are faced with tasks whose extent has not yet been fully recognized in many cases and which involve major challenges in terms of resources, time and expertise.

Even though sustainability is a ubiquitous and much-discussed topic that is omnipresent both in the media and in public debate, it is by no means a new issue. Rather, sustainability has a long and exciting history that spans centuries and has been shaped by various actors and concepts.

Where do the roots of sustainability lie?

As far back as the Middle Ages, the moral ideal of the honorable merchant played a decisive role in promoting sustainable principles. Many a family entrepreneur rightly sees himself or herself in the tradition of the honorable merchant and aligns his or her business conduct with principles such as honesty, responsibility and sustainability.

In the 18th century, the Saxon chief miner Carl von Carlowitz coined the term sustainability in his work “Sylvicultura Oeconomica.” He introduced the idea that forest resources should be managed sustainably by cutting only as much wood as can naturally grow back. What was interesting about Carlowitz’s concept of sustainability was that sustained yield was precisely not antithetical to sustainability. Rather, forestry yield acted as the cornerstone for this oft-cited source of the concept of sustainability. The mining area of the Erzgebirge was simply dependent on the sustainable use of wood for construction, mining and smelting purposes.

Another significant milestone in the development of sustainability was the Brundtland Report, published in 1987 under the title “Our Common Future”. The report defined sustainable development as “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” Here, sustainability clearly went beyond a purely economic consideration. The report emphasized the need to integrate economic, social and environmental aspects to create a sustainable future.

Since then, the understanding of sustainability has evolved to encompass a variety of dimensions. One key concept is ESG (environmental, social, governance) criteria, which encompass environmental, social and governance-related factors. Differentiation of individual sustainable development goals is achieved through the United Nations Sustainable Development Goals (SDGs), which were adopted in 2015. The SDGs include 17 global goals to promote sustainable development at the economic, social and environmental levels by 2030. These goals range from poverty reduction, health, education and gender equality to renewable energy and sustainable cities.

The SDGs are an excellent framework for linking the principle of sustainability with economic, ecological and social development and provide a suitable orientation framework for a company’s sustainability strategy:

- SDGs as guidelines for sustainable management

- Alignment of products and services with the SDGs

- Business activities can contribute directly to achieving the SDGs

Nowadays, at the current edge of development trends around sustainability, so to speak, ESG expression is thus considered a leitmotif and fundamental approach for responsible and sustainable development. It is about combining economic, social and ecological aspects in order to create a world worth living in for present and future generations.

The individual SDGs are suitable targets for integrating ESG into corporate strategies, as they are more concrete and easier to measure using indicators than the more fundamental ESG concept.

Importance of the midmarket

As the backbone of the economy, the SME sector comprises a large number of companies that operate both regionally and internationally. It is of great importance for economic performance and employment in the country. Around 2.5 million companies in Germany belong to the Mittelstand, in the definition of a small and medium-sized enterprise (SME). These range from microenterprises to medium-sized companies with up to 250 employees, which generate around one-third of total sales for Germany and employ more than half of all employees.

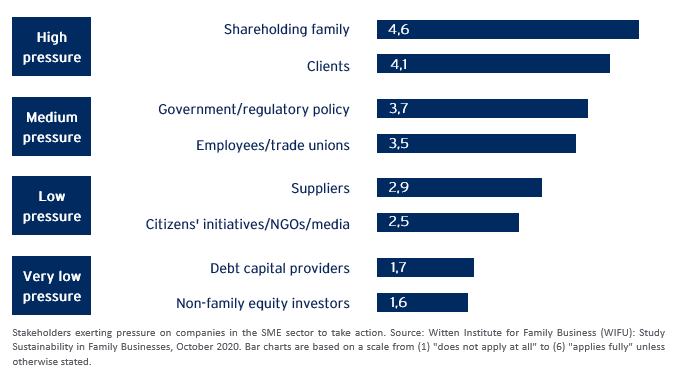

Expectations around an ESG expression of the SME business model arise in a wide variety of internal and external stakeholder groups. Typical stakeholders include shareholder families, employees, customers and suppliers, financiers (EC and FC), NGOs and the media, and to an increasing extent regulatory policy.

The reasons for which companies address ESG requirements also vary. The most common motives include:

- The assumption of ecological and social-societal responsibility,

- Ethical reasons and intrinsic motivation,

- Requirements of customers and employees,

- Cost reduction and expectation of increasing sales,

- Requirements of capital providers,

- And last but not least, the increasing regulatory requirements.

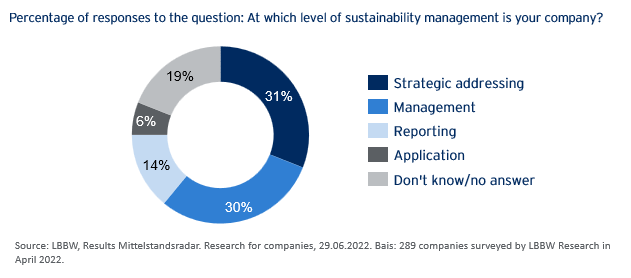

The majority of companies are in the early stages of sustainability management.

Pressure to act and status quo around ESG in SMEs

The pressure to develop and implement ESG strategies is immense and relevant stakeholders are demanding this. In addition to opportunities of an ESG orientation such as cost reduction, successful positioning of the company, revenue and profitability advantages, there are clear business risks of a lack of consideration of sustainability requirements up to the withdrawal of the “license to operate” (violation of regulatory requirements, exclusion from supply chains, lack of financing or perspective withdrawal of insurance coverage).

If, against this background, surveys come to the conclusion that, despite pressure to act and explicit expectations of the relevant stakeholders, only around half of the companies in the SME sector have developed and implemented ESG strategies, the question arises as to why.

A ´decisive factor is the lack of time and resources in many SMEs to deal with the challenges and requirements of sustainability. Time is traditionally a scarce commodity, especially in owner-managed companies. Teams and specialists for ESG strategies and sustainability cannot simply be plucked out of the ground: the market for ESG specialists is empty and salary expectations are correspondingly high.

Support from external consultants is the obvious choice, but here, too, capacities are stretched and for many a large consulting firm it is obvious and more lucrative to advise the large DAX companies with entire teams of consultants before they delve into the peculiarities of the business model of a geographically decentralized SME.

AIM – Advice in Motion GmbH

This is where AIM, as an independent sustainability consultancy and partner in the Investec network, can provide effective support. AIM thinks and speaks medium-sized. Their clients include medium-sized companies from a wide range of industries in Germany, France, Portugal, Luxembourg and Switzerland. AIM supports with:

- Creation, coordination and implementation of ESG strategies in medium-sized companies,

- Preparation for mandatory sustainability reporting (CSRD),

- Directive-compliant calculation of the carbon footprint of companies (CCF) and products (PC),

- Preparation of climate strategies, derivation of targets and measures from the climate footprint,

- Communication around ESG and climate protection: avoidance of reputation risks.

Examples of successful ESG implementation in medium-sized companies:

I. Initial situation: Sustainability requirements for a medium-sized company in the wood industry in Germany with around 1,200 employees. In addition to the intrinsic motivation of the shareholders, a major impetus for action arose from the initiative of the industry association, which demands the implementation of climate protection measures for all member companies. Another impetus for action was for the company, as a supplier in the value chain of a large trading house, to support its ambition (climate protection and other social goals throughout the supply chain). AIM supported the development of a climate strategy, the calculation of the corporate carbon footprint and the compensation of unavoidable emissions in order to achieve climate neutrality.

II. Initial situation: market positioning of a 5-star resort hotel in Provence with its own vineyard. A key impetus for action was to reconcile a luxury resort with sustainability requirements and climate change mitigation measures. AIM developed an ESG strategy for the resort. This was based on a selection of sustainable development goals (SDGs) to which the resort can contribute. Corresponding measures were defined and implemented. At the same time, climate neutrality was achieved for the resort by offsetting unavoidable emissions. (AIM has implemented a comparable project with a resort in Portugal, which has since been nominated for the Sustainability Award of the Portuguese Tourism Association).

III. Initial situation: product positioning for a manufacturer of high-quality competition racing bikes from Switzerland. The company wants to make competitive sports compatible with sustainability and climate protection in particular. In order to provide buyers and users of the competition bike with an assessment of the carbon footprint of the racing bike product, AIM calculated the product-related carbon footprint for the bike, taking into account all phases of the life cycle of the racing bike, from cradle to grave.

IV. Initial situation: A medium-sized holding company with around 1000 employees in Germany will be subject to mandatory sustainability reporting in accordance with CSRD for the first time from the calendar year 2024. The extended reporting affects around 15,000 companies in Germany. The company’s sustainability performance will be considered from two perspectives: the impact of sustainability aspects on the corporate business model and the impact of the company’s activities on the environment and stakeholders. At the same time, the company aims to create a comprehensive ESG strategy that brings together all the actions taken to date to support sustainability goals. AIM has worked with the company to develop an ESG strategy that is aligned and parameterized with metrics to best prepare for upcoming sustainability reporting.

The development of company specific ESG and climate strategies and the requirements associated with the expansion of sustainability reporting pose major challenges for entrepreneurs in the SME sector. We support your company effectively in the sustainable transformation to ensure together with you the future and the competitiveness of your company for you and future generations.

Author: Andreas Kuschmann, Founding Partner AIM – Advice in Motion GmbH.