Michel Degryck, Managing Partner, has been recognised by MergerLinks by Datasite among the Top Investment Bankers in France!

A well-deserved recognition of his leadership and long-standing commitment to clients.

Behind every successful transaction lies trust, judgement and long-term relationships.

Explore the rankings: Top Investment Bankers in France FY 2025

After two years of market volatility, the Life Science Tools sector is entering a recovery phase.

Strong structural fundamentals are driving the rebound: underlying drug innovation, expanding clinical pipelines, biopharma funding stabilization, and strategic acquirers actively seeking consolidation opportunities.

Demand is slowly coming back, now is the window for private mid-caps to professionalize the equity story ahead of a 2026 – 2028 exit.

The report covers the current state and near-term outlook of each subsector, including the structural drivers behind sustained demand such as the growth of complex biologics, GLP-1 therapies, and expanding clinical pipelines. It also examines how the market is recovering from the cyclical headwinds of 2024-2025, where we see growth accelerating, and what the M&A and deal activity landscape looks like heading into 2026-2028.

For a detailed discussion of our findings, feel free to contact Matthias Holtmeyer or Marcel Deutschmann.

Please click below if you would like to receive a copy of the full report.

Market overview and M&A activities in Germany

We are pleased to share our latest report on the market landscape and M&A dynamics in the “digitale Gesundheitsanwendungen” (DiGA) segment. The report provides a comprehensive market mapping, an overview of recent M&A transactions, and insights into exit opportunities for founders and investors.

Executive Summary

The still relatively young market for digital health applications already offers high consolidation potential today and clear exit routes to strategic investors

- Digital health applications (DiGA) have become a permanent part of the German healthcare landscape since their introduction in 2020. With over 1 million doctor-prescribed or approved applications by the end of 2024 and statutory health insurance (GKV) expenditures of around EUR 234m, a considerable sub-market for digital therapy forms has been established. Applications in the areas of mental health, metabolic diseases, and musculoskeletal disorders are in particularly high demand; together, they account for more than 70% of total service expenditures.

- Despite continued growth, it is becoming apparent that the market is entering a phase of consolidation and shake-out. Of a total of 72 approved DiGA, 15 have already been removed, and a growing number of providers are in financial distress. Several prominent insolvencies, including Cara Care, aidhere (zanadio), Mika and Kontina, highlight the structural challenges of a market that until now has been sustained primarily by seed funding and limited reimbursement amounts.

- At the same time, new opportunities are emerging in this phase: for pharmaceutical companies and healthcare service providers, attractive entry options are opening up to systematically integrate digital therapy offerings into existing value chains. Numerous M&A transactions over the past 18 months, such as those involving Selfapy, Sonormed or Mawendo, demonstrate the growing strategic interest of established players in digital therapy platforms.

- Clear and quickly achievable synergies, for example in sales and development or on the cost side in certification, administration, and support, between individual DiGA providers open up exciting platform-building opportunities for private equity. In addition, the larger market participants already show high margins and strong cash conversion.

- The market for digital health applications is comparatively young and therefore offers substantially higher growth opportunities than other sectors in healthcare. In addition, many applications are scalable internationally, as other countries have now also created conditions for the reimbursement of digital therapy formats

The DiGA market appears increasingly ready for consolidation, with some investors already building platforms through acquisitions while others continue to expand organically.

For a detailed discussion of our findings, feel free to contact Matthias Holtmeyer or Marcel Deutschmann.

Financial investors are interested in the healthcare sector. This is hardly surprising: the market is fragmented, hundreds of doctors in private practices are facing succession planning issues, the population is ageing and therefore becoming sicker, and new diagnostic options are emerging – a dynamic environment that promises private equity good prospects and return options.

However, transactions in the healthcare sector have slowed significantly since the end of 2022. In this episode with Editor & Host Isabella-Alessa Bauer, Managing Partner Matthias Holtmeyer and Director Marcel Deutschmann from Investec Advisory explain the reasons for the slump and why the number of deals is now expected to rise again.

The key questions:

- What is the current level of activity in the market? What has it been like over the last 24 to 36 months?

- To what extent is the new regulatory certainty ensuring that the market is picking up again?

- Is there still sufficient potential and attractive targets after the first wave of consolidation?

- Which sub-sectors are attractive? Where is there the most build-up potential?

- How interesting are deals outside the regulated markets?

Click here to listen to the podcast:

What’s up, Corporate Finance? is a blog & podcast from the Finance Think Tank Network. With regular analysis and deep dives on topics related to private equity, private & venture debt, corporate & investment banking, M&A, financing and restructuring, they explain the world of corporate finance with expertise and journalistic passion.

Listen to the 🎙Podcast, which can be found wherever podcasts are available:

🎧 Web-Player

🎧 Apple Podcasts

🎧 Spotify

🎧 Amazon Music

🎧 Deezer

A day full of inspiration and intensive exchange

On 16 September 2025, Investec Advisory together with FINANCE Think Tank co-organised Dealsourcing 2025 in Frankfurt/Oberursel. With over 1,000 industry experts from M&A, private equity and corporate finance, it is one of the largest events in the German corporate finance community.

Pressure to sell or investment crunch: what is driving financial investors?

In the opening plenary session, Ervin Schellenberg, Managing Partner Investec Advisory together with Matthias Weidner, Head of Business Development DPE Deutsche Private Equity, made a clear statement on the current market situation: “Those who need to sell will sell. Those who still have time will first work on optimising their business.” This quote illustrates the current bifurcation of the market: On the one hand, there are companies that have to sell due to pressure, and on the other, there are companies that are optimising their processes and business models before engaging in transactions.

Holger Truckenbrodt, Partner Investec Advisory said: „Great opportunity to get in contact with new potential business partners that weren’t on my radar screen so far.”

In addition to the plenary session, Investec Advisory organised two well-attended workshops:

Is the next wave of M&A coming in healthcare services?

Matthias Holtmeyer, Managing Partner Investec Advisory, discussed the question of whether the healthcare sector is facing a new phase of consolidation and what opportunities and risks investors can expect. A big thank you to our panelists Martin Spirig, Partner at Invision, Ingmar Wegner, Managing Partner at CONVALES, and Dr Thomas Willaschek, Partner and specialist lawyer for medical law at Luther Rechtsanwaltsgesellschaft.

Modern Food – an M&A niche with great potential

Jürgen Schwarz, Managing Partner Investec Advisory led the session, providing exciting insights into the current M&A trends in the food sector from the perspective of manufacturers and investors. A big thank you to our panelists Carsten Hackel, CFO Germany Nestlé, Andreas Holtschneider, Partner PAI Partners, Godo Röben, Supervisory Board & Advisory Board for Plant-Based Foods, and Fabio Ziemssen, Partner Zintinus.

Both sessions addressed highly topical issues and offered not only exciting insights, but also the opportunity to engage directly with industry leaders.

The focus for Investec Advisory was on exchanging ideas with clients, partners, and new contacts. Many of our conversations showed that personal networks are key to success, particularly during challenging market phases. The event provided an opportunity for us to share our expertise, shed light on key market issues and engage in valuable discussions with partners and clients.

We would like to thank all our panelists, contributors and the Deal Sourcing team for the intensive exchange and look forward to Dealsourcing 2026.

Click below for the Aftermovie:

Strategic M&A drives growth across curative and preventive clusters

The global animal health industry remains a resilient and growing market, with strategic players leveraging acquisitions to unlock value across traditional curative portfolios and high-growth preventive platforms.

Driven by regulatory evolution, rising pet ownership, and the shift toward comprehensive health management, animal health has transitioned from a defensive play to a growth-oriented strategic opportunity.

Key Growth Clusters

The animal health sector presents distinct investment opportunities across complementary segments:

- Preventive Solutions (CAGR: 8-10%): Vaccines, feed additives, and diagnostics are outpacing the market through mRNA and AI innovation

- Curative Pharmaceuticals (4-5%): Antibiotics and therapeutics are providing stable cash flows to fund growth investments

- Companion Animals: Premiumisation trends are driving faster growth in developed markets

- Livestock: Representing 60% of total market value, growth is supported by food security needs and operational efficiency demands

M&A Activity

Strategic M&A activity accelerated over the past 18 months, spanning biotech innovators, pharmaceutical companies, and diagnostics specialists. Europe and North America lead transaction volumes, with buyers pursuing geographic expansion, portfolio diversification, and innovation pipeline access.

Leading players adopt dual-portfolio models, using mature curative assets as cash engines to fund targeted acquisitions in high-growth preventive categories. This enables earnings stability while shifting toward innovation-led growth.

The sector’s fragmentation offers compelling consolidation opportunities, ideal for buy-and-build strategies across European and North American markets.

Financial investor momentum accelerates

Private equity funds are actively deploying capital across both clusters, attracted by the sector’s resilience, strong cash generation, and above-economy growth rates. Interest focuses on companion animal and preventive medicine businesses, though curative platforms remain attractive for their margins and regulatory defensibility.

Looking ahead

M&A activity will accelerate as companies optimise portfolios across the curative-preventive spectrum. Both strategic and financial investors recognise animal health’s exceptional blend of defensive characteristics, innovation potential, and consolidation opportunities in a fragmented market.

This is why, at Investec, we view animal health as one of the most compelling sectors in the European and North American mid-markets. For more information and our full 2025 Animal Health Report, please contact Jan Willem Jonkman, Bart Jonkman or Thom Deckers.

How a professional dialogue is now moving companies forward

Interview with Thorsten Gladiator, Managing Partner of Investec about how a professional dialogue is now moving companies forward:

- Why companies should entertain a professional dialogue with their investors and lenders?.

- What other challenges are companies facing?

- As a financial expert and transaction specialist what advice do you have for companies when dealing with debt and equity investors?

- Giving an example.

This video answers these questions and give you an idea and overview in a few minutes.

Finding the right type of capital and investor to help grow your business

Our team has a long track record of successfully raising equity and debt capital and has the necessary expertise and networks:

- Raising capital to support business growth

- Securing capital from private equity and/or other Investors to support MBO/MBI projects

- Securing capital from private equity and/or other investors to manage changes in the shareholding structure (such as supporting the buyout of one or more shareholders and the reallocation of equity shares)

- Project financing: supporting companies in realizing essential investments or working capital

- Refinancing: supporting companies in reorganizing/reducing their debt burden

We’re pleased to announce a further expansion of our international M&A advisory business with the integration of Capitalmind Switzerland into the Investec brand.

The Swiss team, lead by Markus Decker and Thomas Ellenberger, is proud to join Investec, reinforcing our shared commitment to delivering tailored M&A advice and solutions.

It’s an important milestone for our team and clients, strengthening our presence and capabilities across Europe.

This latest acquisition underscores our commitment to expanding our advisory business, where we now have 300 M&A professionals based across 17 offices globally, and complements the growth of Investec’s integrated offering in Switzerland, which includes private banking, wealth management and direct lending.

“By uniting our M&A professionals accross Europe, we are able to bring fresh ideas and tailored solutions to clients in Switzerland and internationally.”

– Markus Decker, Managing Partner of Swiss office

“This acquisition deepens our Swiss presence and enhances global collaboration, connecting clients to international and local investment opportunities.”

– Jonathan Arrowsmith, Head of Investment Banking, Investec

All our Swiss team members:

Markus Decker, Thomas Ellenberger, Yanik Costa, Dr. Miró Feller, Tim Graber, Kai Kiesinger, Lorenzo Mattei, Luca Stalder and Gabi Korolnyk

Learn more:

Switzerland | Investec Advisory

We at Investec Advisory together with FINANCE Think Tank, are delighted to co-host DEALSOURCING2025 – the leading networking event for the German Corporate Finance community – on 16 September 2025 in Oberursel, near Frankfurt. It is one of the largest events in the German corporate finance community, with over 1,000 participants from the fields of M&A, financing, and restructuring.

Highlights in the opening plenary: “Pressure to sell or Investment crunch: What is Driving Financial Investors?”

Our Managing Partner Ervin Schellenberg and Matthias Weidner, Head of Business Development DPE Deutsche Private Equity will discuss the key question in the opening plenary session.

Workshop 1 at 11:00 am: Is the second M&A wave coming in Healthcare Services?

Matthias Holtmeyer, Managing Partner at Investec Advisory, invites visionaries Martin Spirig, Partner at Invision, Ingmar Wegner, Managing Partner at CONVALES, and Dr Thomas Willaschek, Partner and specialist lawyer for medical law at Luther Rechtsanwaltsgesellschaft, to an expert panel to discuss whether the next wave of M&A activity in healthcare services is coming.

Workshop 2 at 15:30 pm: Modern Food – an M&A niche with great potential

Jürgen Schwarz, Managing Partner at Investec Advisory, invites visionaries Carsten Hackel, CFO Germany at Nestlé, Andreas Holtschneider, Partner at PAI Partners, Godo Röben, Supervisory Board & Advisory Board Member for Plant-Based Foods, and Fabio Ziemßen, Partner at Zintinus, to an expert panel discussion on the question of M&A potential in the modern food sector.

We look forward to a day full of knowledge-sharing, fresh ideas, and new connections.

More on the programme: www.dealsourcing.de

Date: Tuesday, 16 September 2025

Location: Dorint Hotel Frankfurt/Oberursel, Königsteiner Str. 29 61440 Oberursel

Good reasons for a sale

In the past, large practice structures in particular were virtually unsellable or could only be sold to a successor for a small fee. The entry of investors has fundamentally changed this situation.

There are many reasons for selling a practice. A decisive factor for many is to hand over the practice, and thus the employees and patients, to suitable successors. But what can be done if there are no internal successors?

In this case, the only option is to sell to a third party. In many cases, this can be and will be doctors who intend to continue running the practice in line with the previous owners’ vision. However, once the practice has reached a certain size, very few doctors feel able to pay an appropriate purchase price. This is where larger groups can fill the gap.

In many specialist areas, investor-financed groups are already active and consolidating the market. They usually pay a (significantly) more attractive price for the practice than other doctors could and also offer support in many administrative areas. However, the doctors remain fully responsible for patient care.

In addition to the financial aspects, choosing the ‘right’ partner for your life’s work is also crucial. According to legal requirements, selling doctors must generally remain employed at the medical care centre for three years, which must be established no later than the date of sale. Practice owners must plan for this time frame accordingly.

In addition, purchase price components are usually agreed in the purchase agreements that only come into effect after two or more years of cooperation.

Do you have questions regarding M&A or selling your business?

We would be happy to schedule a call to discuss further.

Click here to download the report.

Investec is proud to announce that our French team is awarded as one of the Best Investment Bank – LBO Small to Mid Cap with a Silver Award at the recent Sommet des Leaders de la Finance in Paris.

Organised by Décideurs Corporate Finance, this event recognises excellence in corporate finance and highlights the work of professionals who lead complex and strategic transactions.

We warmly thank our teams for their dedication, and our clients for their continued trust.

The outpatient healthcare sector is changing rapidly. While the total number of medical practices is declining, leading software providers are growing by up to 90% annually.

An important driver of this development is mergers and acquisitions. With every practice sale, the likelihood of a change in practice software increases – and with it the opportunity for flexible, specialised providers to gain market share. Specialised solutions for radiology and ophthalmology are growing particularly strongly, despite high integration hurdles.

For our analysis, we compared the installation statistics of the National Association of Statutory Health Insurance Physicians (KBV) from 2016 with the latest data from Q4 2022. The analysis is based on publicly available billing data from the associations of statutory health insurance physicians – i.e. the very systems used for billing statutory health insurance. The figures were sorted by annual growth rates to highlight the most dynamic changes.

The result shows that the market is on the move and specialisation pays off. What developments do you see?

We look forward to hearing from you.

The healthcare clinics market in the Netherlands is a dynamic sector, where clinics play an essential role in the overall healthcare ecosystem. Some key insights and trends include:

- The healthcare sector is considered non-cyclical and has proven resilient during recent economic crises.

- The Dutch health market is the second-largest sector, with an average spend of € 7,129 per person on healthcare.

- Private equity firms continue to show strong interest in the healthcare industry, with their acquisition activity steadily increasing.

- Increased reliance of the general healthcare system (including public hospitals) on private clinics

- Significant consolidation, particularly in the private clinics market, with most private clinics falling under general healthcare insurance, ensuring covered care.

- Variations in investment levels from private equity across different clinic segments.

- Political scrutiny over private equity investments in the healthcare sector.

To receive a complete copy of our insights, feel free to reach out!

DOWNLOAD PREVIEW

Helen Lucas | UK

Jonathan Harvey | UK

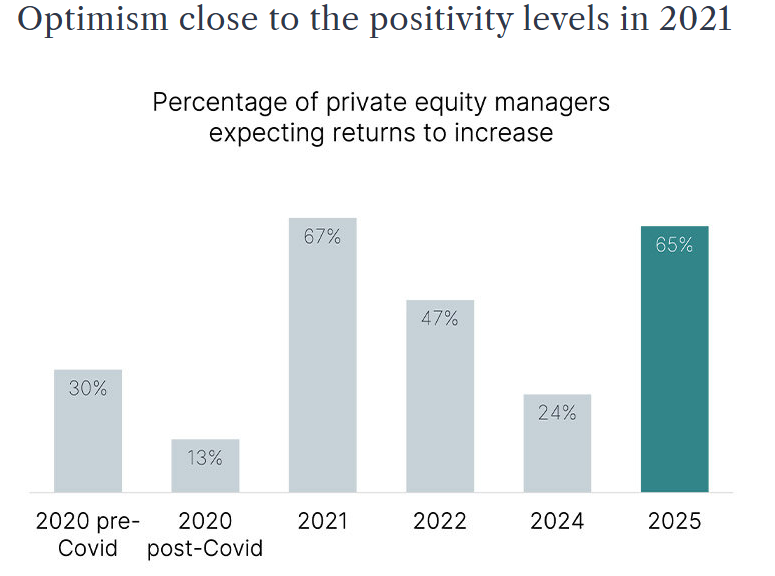

Our 14th report comes at a crucial time for the industry, as GPs get back to the business of selling portfolio companies and raising new funds.

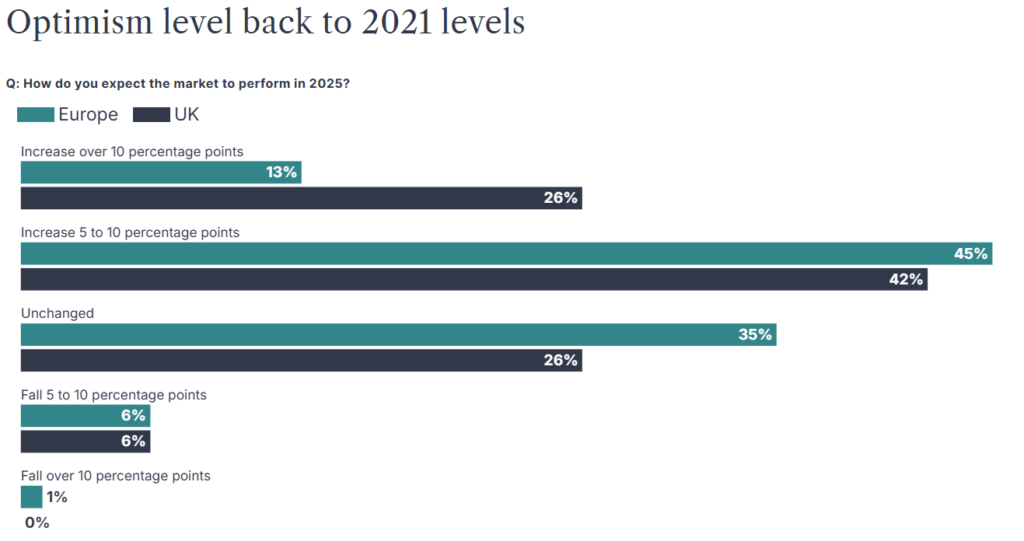

2024 was a tough year for private equity and the overriding view from our survey of 253 general partners (GPs)* is that 2025 will be different.

Our findings show an industry which, despite challenges over the past few years, is resilient, adaptable, and anticipating a more favourable period ahead.

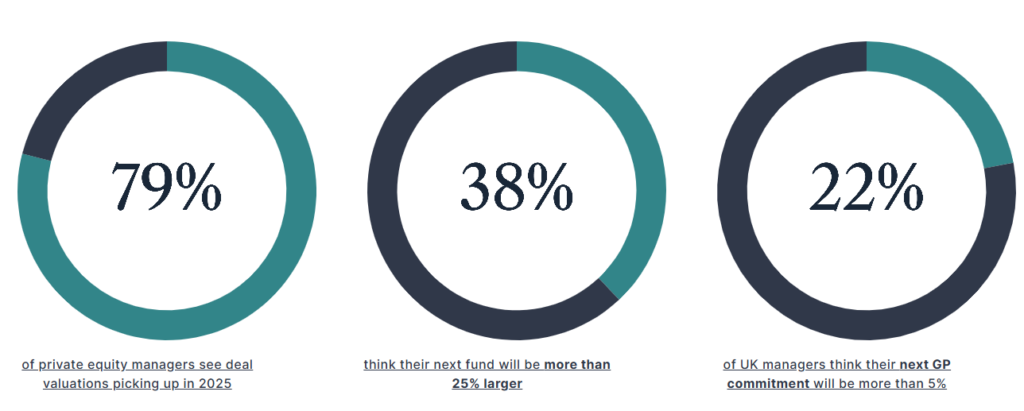

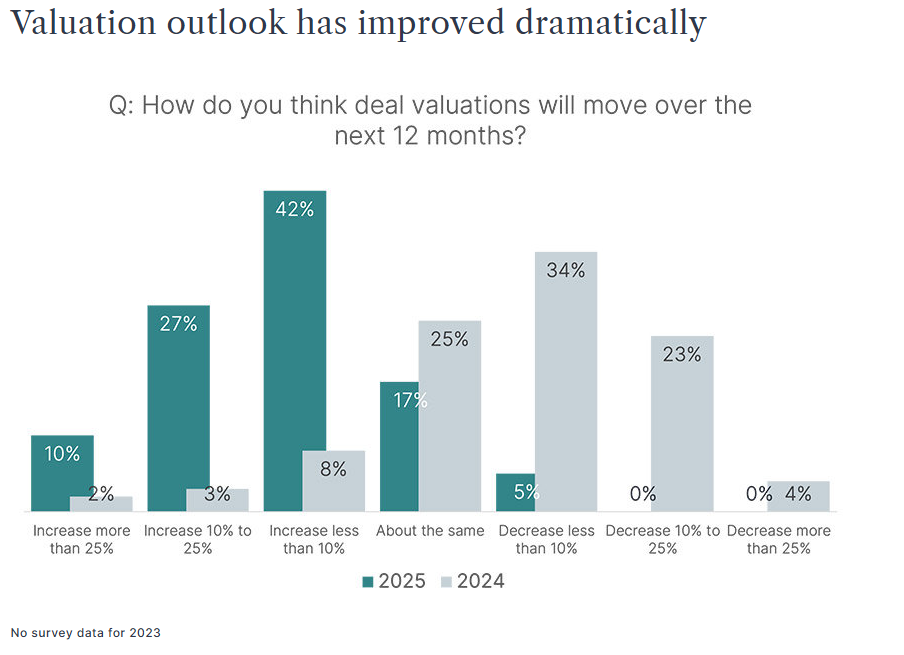

Four in five GPs expect deal valuations to increase in 2025 as interest rates come down, helping to clear exit bottlenecks and accelerate investors’ distributions. The outlook for returns is also brighter, with improvements registered across geographies and fund sizes. Close to two thirds (65%) of investors see returns improving in 2025, up from only 24% in 2024.

Dealmakers still must navigate ongoing geopolitical and macroeconomic risk, as trade tariff tit-for-tats continue and conflicts in the Middle East and Ukraine remain unresolved. It is a complex market, but the backdrop for M&A is better than it was a year ago.

Jump to a section:

Future fundraisings

GP commitments

New world of debt

Innovations and exits

GPs at a crossroads

Future fundraisings

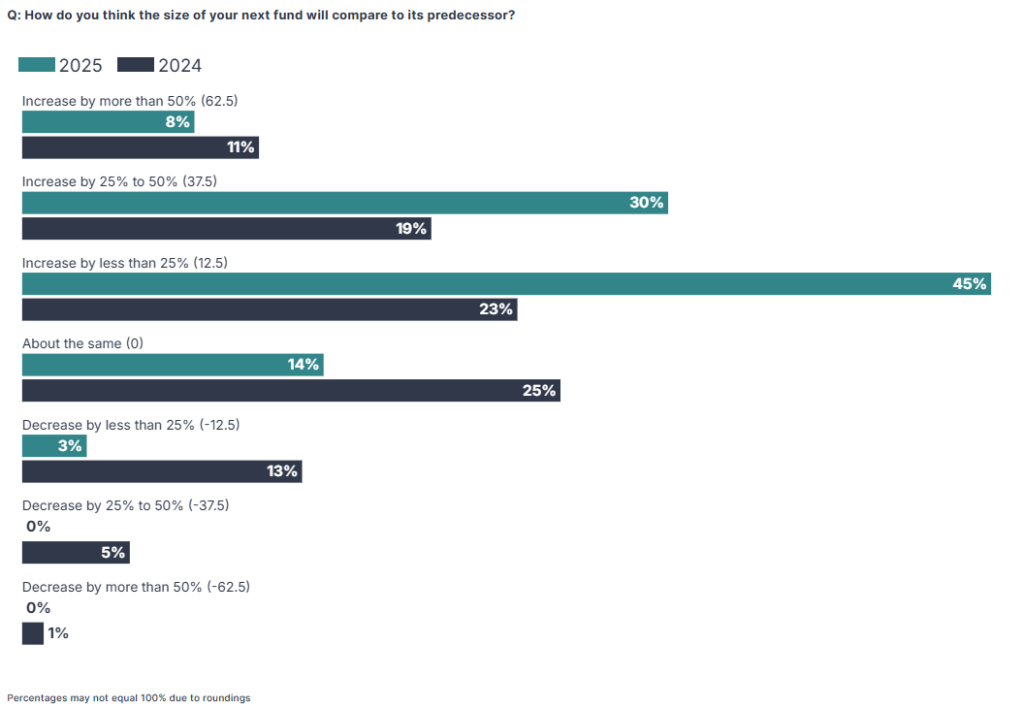

In 2024, 21% of respondents expected a down raise for their next fund: the 2025 research shows only 3% anticipating the same scenario.

There is also a large cohort of super-optimists – 38% expect their next raise will be a blockbuster increase of 25% or more over their previous fund.

Limited partners (LPs), however, are expected to remain highly selective in 2025. In 2024, according to PEI figures1, the ten largest funds to close in 2024 all secured more than $10 billion and absorbed more than a fifth of total fundraising allocations while a Coller Capital LP survey2 showed that the top focus for 98% of investors is that a new manager has a team with a strong track record.

Our survey findings tie in with this theme – close to a third of respondents (31%) expect an increasing number of GPs to move into wind-down. However, this does not mean the opportunity for new managers has passed; just 26% agreed that “very few new GPs will be launched”.

Although fundraising conditions are improving, LPs continue to consolidate GP relationships, focusing on managers of scale and mid-market specialists with differentiated investment strategies and exceptional returns.

Fundraising optimism surges

Jump to a section:

Deal valuations

GP commitments

New world of debt

Innovations and exits

GPs at a crossroads

GP commitments

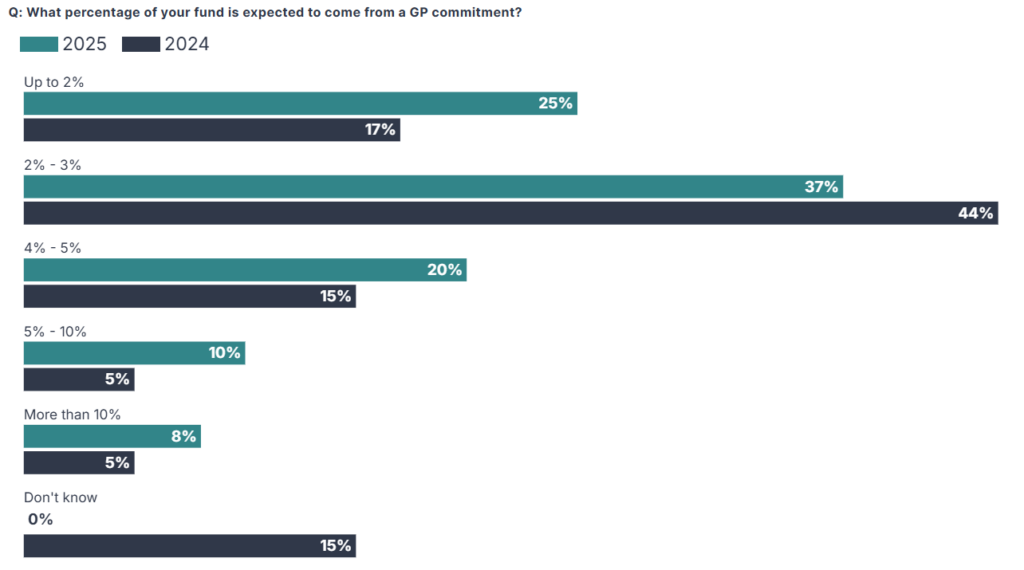

The survey shows GPs are planning to up their commitment from the typical 2% to 3% to strengthen alignment with investors and boost fundraising momentum.

- One in five GPs expect to commit 4-5% of their next fundraise.

- One in ten expect their next commitment to be 6-10%.

- 8% expect to commit more than 10% in 2025.

Managers are taking a blended approach to financing these higher commitments including existing resources, reinvesting carried interest and external debt, which is gaining favour. Most are using two options to fulfil their obligations, with 13% expecting to use three options.

Where are commitments highest?

The findings reveal interesting regional variations when it comes to GP commitments.

UK managers are more likely to be asked for a big commitment: 22% were asked for more than 5% versus just 8% of managers in Europe. Managers in France, meanwhile, seem to be asked for a particularly slim commitment, with more than half expecting to be asked for less than 2%.

Overall, a significant minority of investors expect to up commitments in the future.

Jump to a section:

Deal valuations

Future fundraisings

New world of debt

Innovations and exits

GPs at a crossroads

New world of debt

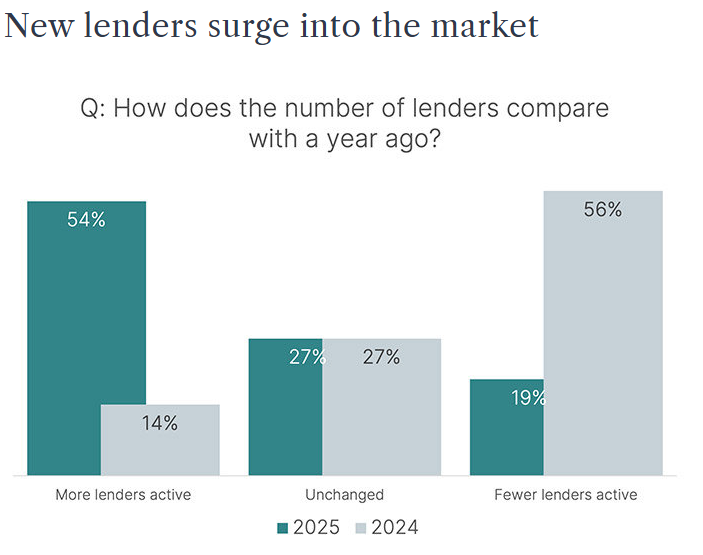

Debt markets are open for business with a substantial number of new lenders entering the market to provide GPs with enhanced financing optionality.

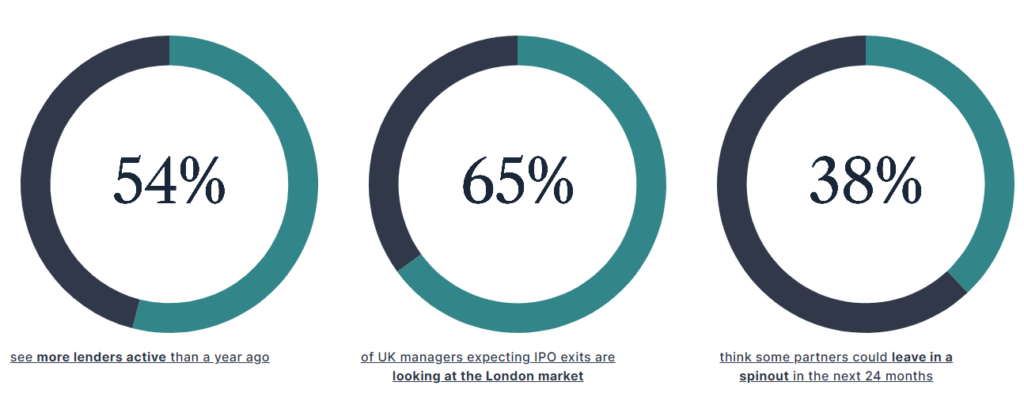

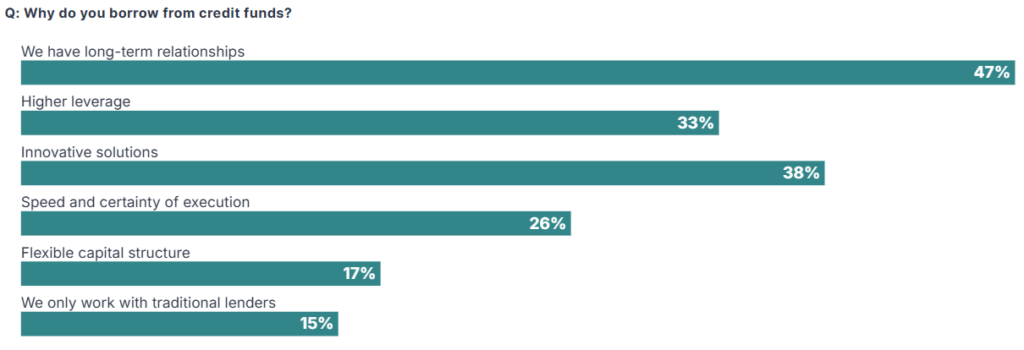

More than half (54%) of GPs say they will have new lenders to work with in 2024. This marks a shift from last year’s findings, when 56% of respondents saw a contraction in new lender activity. The majority of GPs who took part in our survey are working with credit funds and the top three reasons cited for working with a private credit included higher leverage levels and innovative financing solutions.

UK managers are hopeful that increasing competition will result in looser terms, with 54% of UK managers reporting either private debt narrowing margins or terms loosening generally. Outside of the UK, however, GPs are more cautious, with only 35% forecasting looser terms.

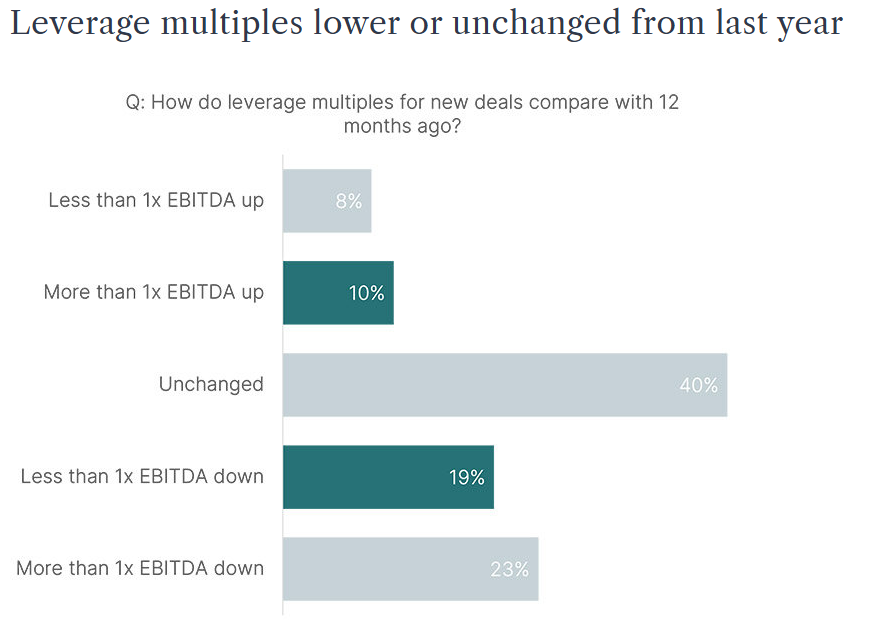

Despite these expectations, lenders are remaining disciplined. Well over a third of respondents (43%) report that leverage multiples have lowered from a year ago.

Competition is fierce for trophy assets in certain sectors, and these companies will be able to negotiate more favourable terms, but lenders will be highly selective.

Interest rates may have come down, but the risk-free rate remains elevated when compared with recent years, making additional leverage costly to service. Debt is available (European leveraged loan issuance climbed by more than 90% in 20243 and private debt managers have $126.4 billion of dry powder available to invest4), but the survey findings on leverage multiples show that capital structures remain relatively conservative.

Covenant flexibility

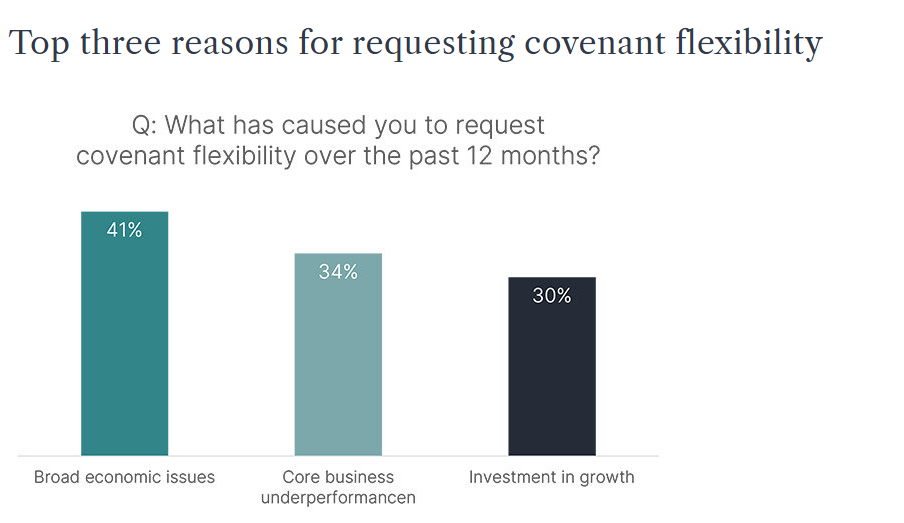

Even as interest rates have come down, GPs have still had to work hard to protect portfolio companies.

Some 87% of respondents say they have gone to lenders to request covenant flexibility for one or more portfolio companies. Broad economic issues (cited by 41%) and business underperformance (cited by 34%) are the main reasons for requesting flexibility.

Interestingly, close to a third of respondents (30%) have requested covenant flexibility to fund growth as GPs hold some portfolio companies for prolonged periods.

“We will always be open to a conversation about covenant flexibility. If a business is growing and wants to re-lever, or the sponsor wants to hold an asset for longer, loosening covenants can have a positive impact on supporting growth.” – Helen Lucas, Co-Head of UK Origination, Direct Lending, Investec

Lending landscape

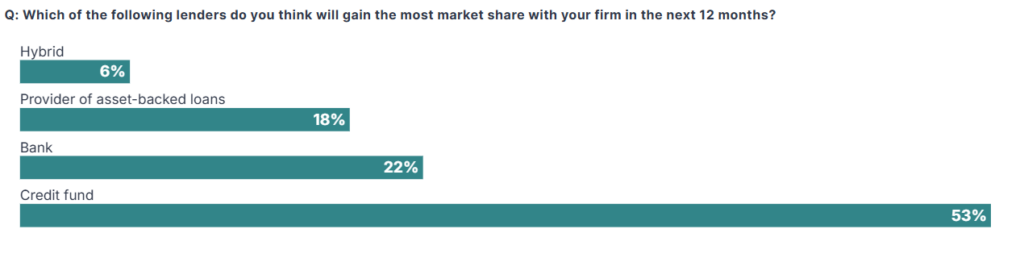

As more lenders entered the private equity space, there has also been increased use of some newer debt products. Innovation continues; survey respondents expect ESG-linked lending, fund-level finance and asset-based lending to increase market share.

Around half of the respondents expect credit funds to do more business with their firm during the year, but banks remain highly competitive; almost a quarter (22%) say they expect to place more lending with banks in the next 12 months. Hybrid capital is gaining particular traction for smaller managers with assets of $250m or less, with a quarter of these saying this type of lender will gain the most market share at their firm in the next year.

NAV lending

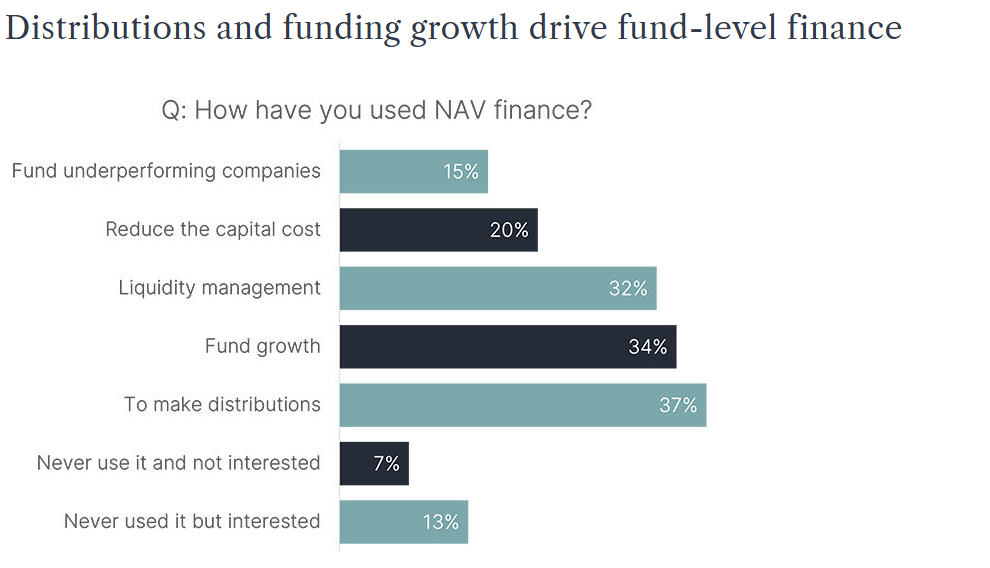

Net asset value (NAV) finance has proven particularly popular with managers in an environment where liquidity has been constrained.

Four in five GPs said they used NAV finance in the last year, with distributions the most-cited use case (37%).

Uptake of NAV finance looks set to continue accelerating, with two thirds (65%) of respondents who had not used NAV finance previously saying they were interested in taking up NAV loans.

Deployment and operations

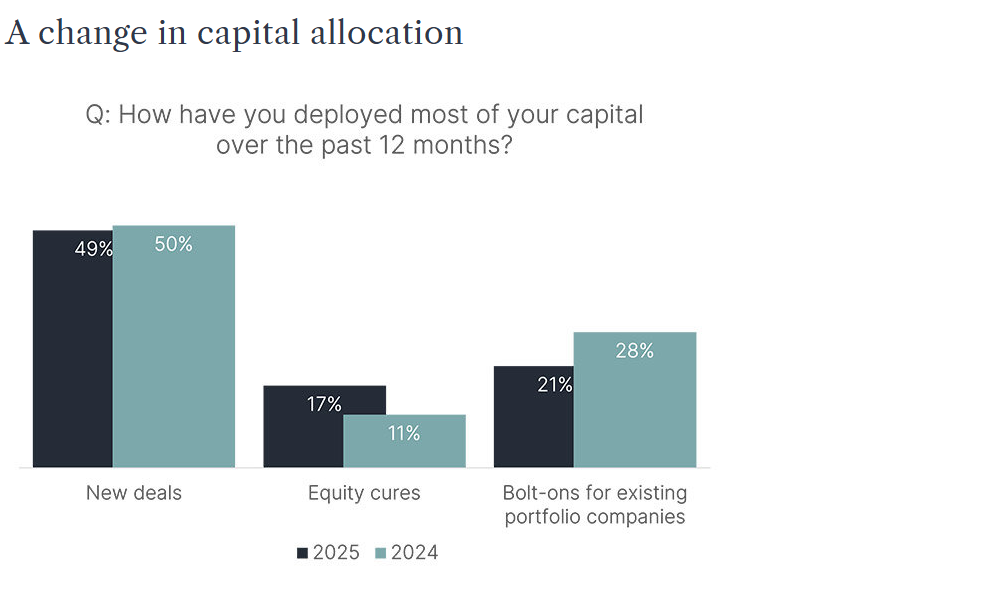

Less than half of GPs (49%) have deployed most of their capital in new deals during the past 12 months, with just over a fifth (21%) focusing efforts on smaller bolt-on acquisitions to support buy-and-build portfolios – down from 28% in our previous survey. An increase in the number of GPs deploying most of their capital in equity cures – up to 17% from 11% last year – further highlights the tough backdrop for managers during the past year.

The improving outlook means that the next 12 months should be more favourable for deployment. Somewhat surprisingly, the public-to-private outlook is mixed and not much changed from last year despite low stock market valuations, most notably in the UK5. Some 50% say they expect to look at more public-to-privates but 40% expect to look at less.

Big-ticket take-private deals during 20246 have ensured that P2P remains on the managers’ radars and may result in activity in this area.

“Private equity managers are ready to deploy, but it is taking much longer to originate deals. GPs will be forming relationships with management teams up to three years ahead of a formal process. During the last two years we have seen a number of processes fall over, and it does take time to rebuild before businesses come back to market.” – Kate Gribbon, Head of Financial Sponsor Coverage & Origination, Investec

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

Innovations and exits

GPs at a crossroads

Innovations and exits

One of the single biggest challenges for private equity managers through the rising interest-rate cycle has been to sell portfolio assets at valuations that deliver adequate returns.

In tepid IPO and M&A markets, GPs often opted to sit tight rather than offload assets at lower-than-hoped-for multiples. Hold periods remain above long-term averages, with the backlog of private equity-backed companies sitting at record levels7.

This has had repercussions on fundraising – slowing distributions to LPs have limited their ability to allocate to new funds.

Managers looking at exits will explore all options to crystallise returns, with the survey findings ranking expectations for different exit routes in a narrow band.

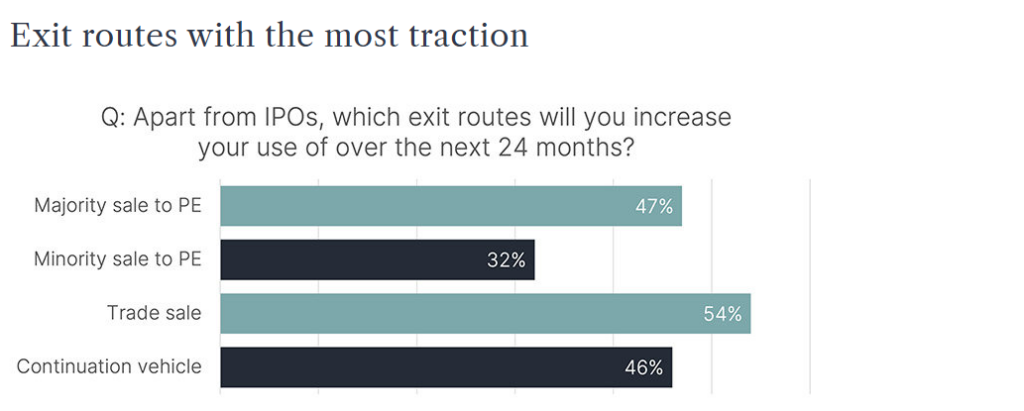

More than half of GPs (54%) think trade sales will be the busiest exit route during the next 24 months. But after a long barren spell the IPO is back in the frame again, with the typical manager optimistic that two portfolio companies could be an IPO candidate over the next two years.

The squeeze on other exit routes meant there has been greater use of continuation vehicles which are here to stay as a mainstream exit path: more than 40% of GPs say a continuation fund will be an exit option they are more likely to use in the next 12 months.

The UK IPO question

Private equity-backed portfolio company IPOs haven’t always been crowd-pleasers, particularly on UK markets8, but the survey findings show managers warming to the UK stock market – albeit with some reservations.

Some 65% of UK managers who expect to list a portfolio company in the next two years consider the UK a potential venue – although they will also look at other venues such as Amsterdam or New York.

The size of the manager and portfolio is a factor in stock market selection. Larger managers with bigger assets to float think a UK IPO is less attractive, indicating that larger IPOs are considered more challenging for UK public markets.

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

New world of debt

GPs at a crossroads

GPs at a crossroads

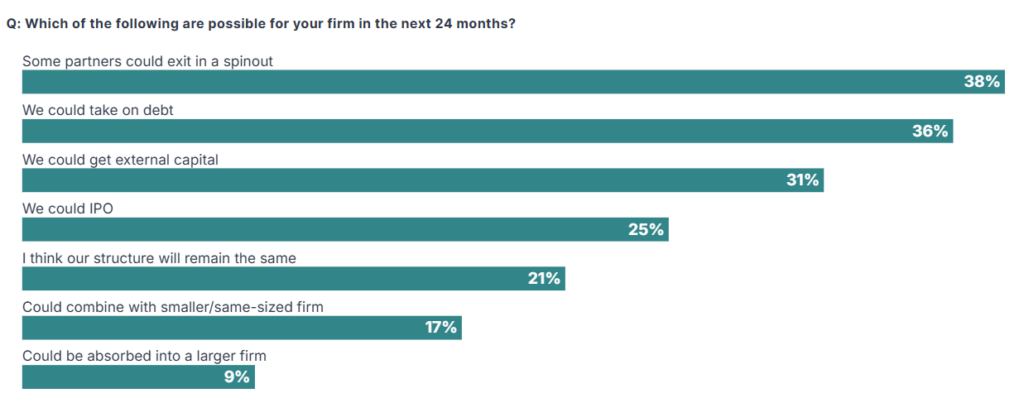

According to Pitchbook figures, GP-to-GP M&A reached record highs at the end of 20249 and the survey points to a long runway of further deals, with 79% of respondents expecting some kind of change to their firm’s structure.

In addition to GP consolidation deals, new teams are forming in spinouts and minority stake investment is proliferating.

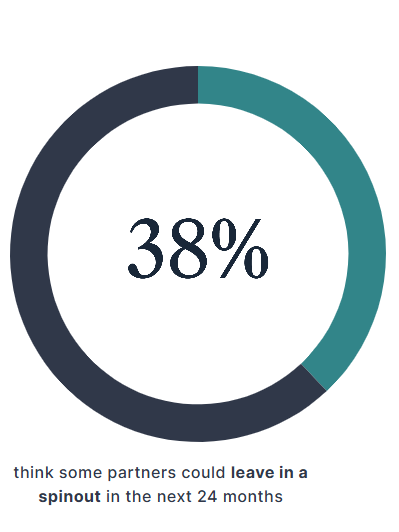

Indeed, 38% of GPs say some partners could leave their firm via a spinout in the next 24 months. This is reflective of a tougher fundraising environment, particularly for smaller managers with assets under management (AUM) below $1bn, where spinouts are more likely as junior partners explore other options when fundraisings stall.

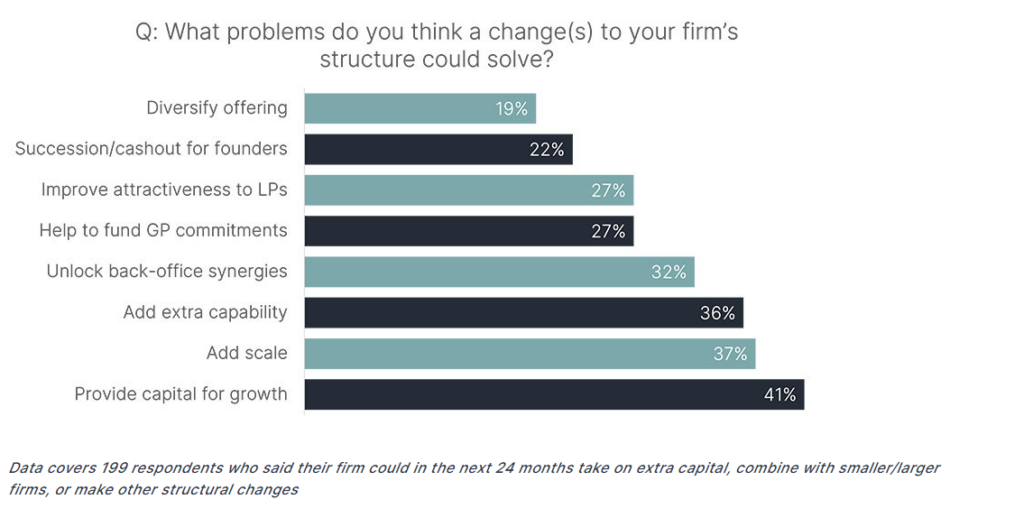

Getting ready to capture growth

Historically, the main driver for taking on third-party capital or merging with another firm was likely to unlock liquidity and facilitate succession. While this reason was selected by 22% of respondents, the majority see a transaction as a tool to provide capital for growth or expand service lines and scale.

Ideally, twice as many managers say they would like to be the acquirer rather than target in a consolidation scenario.

What is also worth noting is that when it came to continuation vehicles, our survey showed that 40% of GPs think there will be more single-asset continuation vehicles over the next 24 months and over 25% thought they are likely to become more specialised. Single-asset continuation vehicles allow GPs to remain invested in a prized portfolio company and could potentially lead to a spin-out by a manager.

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

New world of debt

Innovations and exits

* Demographic info

This report is based on 253 responses to an online survey conducted between 7 January and 22 January 2025. Respondents were sourced from a prequalified panel and no PE firm was represented more than once.

178 were based in the UK, 75 in Europe including 22 in Germany, 14 in Spain and 11 in France. Some 34% of respondents were investment directors, other eligible job titles were CFO, VP of finance, director of finance, principal and manager of finance/investments.

Footnotes:

2 https://www.collercapital.com/41-barometer-winter-2024/

4 https://www.muzinich.com/opinions/corporate-credit-outlook-2025-private-markets

6 https://www.ft.com/content/ec9aa2ae-f56a-4373-8c4b-88effc01a25d

7 https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report

9 https://pitchbook.com/news/articles/blackrock-hps-purchase-record-year-gp-consolidation

Our French team is recognised as the one of the most active firm in LBOs, M&A and Debt Advisory

We are delighted to announce that our French team has been recognised as one of the most active firm in LBOs, M&A, and Debt Advisory by CF News, a leading French publication in Private Equity and Corporate finance.

The team has achieved the following rankings:

- #4 in the LBO segment

- #5 in the M&A Small & mid cap (€50 million to €250 million deal value)

- #5 in Debt Advisory

Under Michel Degryck‘s leadership, the French team of 40 cross-sector professionals has continued to deliver results for clients in a challenging environment, delivering tailored and high-quality solutions to entrepreneurs, family businesses, corporates and private equity firms.

“This recognition reflects the trust our clients place in us and the unwavering commitment of our team. We remain dedicated to providing innovative solutions tailored to their strategic challenges.”

— Michel Degryck, Managing Partner, Investec Advisory France

Investec announces the appointment of Michael Eriksen as Head of Nordic M&A in support of its strategy to significantly grow its presence in Europe. Michael brings over 25 years’ experience as an M&A advisor to companies in the Nordics.

In his new role, Michael will focus on identifying and pursuing growth opportunities for clients, in line with Investec’s 25-year track record as a trusted M&A advisor to clients globally, particularly in Europe. Investec provides tailored M&A advice to clients, many of whom operate in the mid-market across a wide range of sectors, helping them achieve their growth objectives.

In 2023 Investec acquired a majority interest in Capitalmind and, with effect from today, completes its transition to the Investec brand.

“Companies across multiple sectors in the Nordics are actively seeking opportunities to expand beyond their borders. Michael’s established relationships and expertise will be invaluable as we enhance our M&A advisory capabilities in the region. At the same time, we are committed to bringing our broader expertise to the Nordics, including leveraged finance and fund solutions for private equity, such as GP financing, continuation funds, and NAV facilities.”

Jan Willem, Managing Partner and Board Director of Investec Continental European Advisory BV (ICEA)

“The Nordic region is a dynamic and expanding market. I firmly believe that Investec, with its strong client focus and comprehensive banking capabilities, is ideally positioned to capitalise on the opportunities that lie ahead.”

Michael Eriksen, Head of Nordic M&A

R&D to grow or just to be?

Animal health: Is R&D required for growth or survival?

Review of our animal health conference, which explains how the humanisation of animals, success of novel therapeutic approaches and technologies in human health, as well as the increased drug resistance will continue to underpin focus on R&D.

Watch highlights from the 2024 conference:

The humanisation of companion animals, demand for sustainable food sources for livestock, as well as requirements for improvements in animal welfare are driving innovation and consolidation in the animal health sector.

These three trends were at the centre of discussions at our inaugural Animal Health conference, where industry leaders and advisors discussed whether the R&D investment is a prerequisite for survival or is it still predominantly undertaken for growth.

Animal health market comprises multiple categories, such as:

- vaccines & medicines,

- veterinary services,

- pet supplies & serves,

- feed additives.

The sector, which was valued at approximately £130 billion in 2023, has a forecast compound annual growth rate (CAGR) of 5-8% per annum until 2030.

Companion animals to remain a key segment driving future growth

Increased pet ownership in developed economies, the growing importance owners place on their pets, and higher awareness around animal health and wellbeing have boosted spending on veterinary treatments, preventative health measures, and wellness products for companion animals. Pet owners’ primary focus on quality of life and longevity is driving innovation in disease and symptom control. As pet ownership has been shown to have physiological and emotional benefits for humans, the positive impact on global human health cannot be underestimated. However, conversely, 75% of over 30 new human pathogens identified in the last few decades, originated in animals1.

Continuous R&D focus on translating advanced human technologies to animal health

Success of novel therapeutic approaches and technologies in human health are among key drivers of increasing animal health R&D spend. Clinical drivers behind the trend are potential to translate novel treatment benefits from human to animal health (e.g., monoclonal antibodies and mRNA vaccines), growing scientific basis for the use of new technologies to address animal disease (e.g., gene therapies and stem cell therapy), and evolving treatment paradigms due to microbial resistance concerns (including increasing focus on proactive prevention).

Further underpinning the trend are non-clinical drivers such as:

- growing willingness to spend disposable income on pets,

- emerging role of technological advancements in healthcare (e.g., across spectrum of big data and artificial intelligence),

- increasing government and non-government investment into sustainable animal health (e.g., sustainable agriculture / farming)2.

What is clear is that as the animal health market is becoming more specialised and sophisticated. Therefore, investors and operators must carefully consider which are the most appropriate areas and specialties to drive their business forward.

Our guest speakers

David Hallas,

CEO, ECO Animal Health plc

Laurent Flaus,

Co-Founder and CEO, Axience Group

Simon Middleton,

Partner, L.E.K. Consulting

Sources

1 World Health Organization ‘One Health’ guide 2019

2 L.E.K. Consulting

In the past, large practice structures in particular were almost impossible to sell or could only be sold to a successor for a small fee. The entry of investors has fundamentally changed this.

There are many reasons for selling a practice. For many, a decisive point is to hand over the practice and therefore the staff and patients to a suitable successor. But what to do if there is no internal successor?

In this case, the only option is to sell to a third party. In many cases, this can and will be a doctor who will continue to run the practice according to the previous owner’s ideas. However, if the practice has reached a certain size, very few doctors will feel able to pay an appropriate purchase price. This is where larger groups can fill the gap.

In many specialist areas, groups financed by investors are already active today and are consolidating the market. These groups generally pay a (significantly) more attractive price for the practice than other doctors could and also offer support in many administrative areas. However, patient care is still entirely the responsibility of the doctors.

In addition to the financial aspects, choosing the “right” partner for the life’s work is also crucial. Legislation stipulates that the selling doctors must generally continue to work for three years in the medical care centre to be established for the sale at the latest. A corresponding time horizon must be planned for by the practice owners. In addition, earn-out clauses are usually agreed in the purchase agreements, which only come into effect after two or more years of co-operation.

Valuing means comparing: We carry out a structured sales process with all relevant market participants in close consultation with you. The aim is to obtain as many different offers as possible in order to be able to select the most attractive offer.

Click below to read and download the full brochure.