China’s economy is slowing or at least not recovering in the way that many predicted it would. Demand for commodities is relative low, not only as China is not growing the way it used to do (via property investments, etc.), but also as global demand for its manufacturing industry is slowing. Again, South Africa is a China-proxy – an old-school China-proxy to be precise. On a sidenote, what we need is to attach ourselves to the new-China, i.e. India. Australia rose with China’s commodity demand, I do think India could be the same for SA. Thing is that there are not even direct flights from Johannesburg to Mumbai and I have not seen any initiatives to push this angle. Hopefully the private sector will come into play. Coming back to China and our exposure, judging from various articles and research consumption is starting to be a problem there, too - Positioning wise, globally funds are long luxury to play the consumer revival in China (ESG funds, passive funds, active managers). At the same time however, fund managers have been exiting China and are underweight China as a whole now. Some mismatched view to those who are long luxury vs those who sold China generally?! There seems a lot in the price both ways – from an overweight luxury to an underweight China perspective. Long local China retail & consume vs. global luxury seems a proper contrarian trade to me. Add that HK tech (also exposed to the Chinese consumer) is not well owned and (regulatory/government) news flow has been a bit more supportive recently. By the way, Chinese tech companies have not benefited from the AI rally overseas despite proper exposure to this theme. Maybe China tech is a play on both themes (positioning and the Chinese consumer)? The upcoming Politburo meeting is seen as an important one to see what the government will do to revive the local economy. How to play this as South African investors? We have listings exposed to HK tech (Prosus, Naspers) and luxury (Richemont).

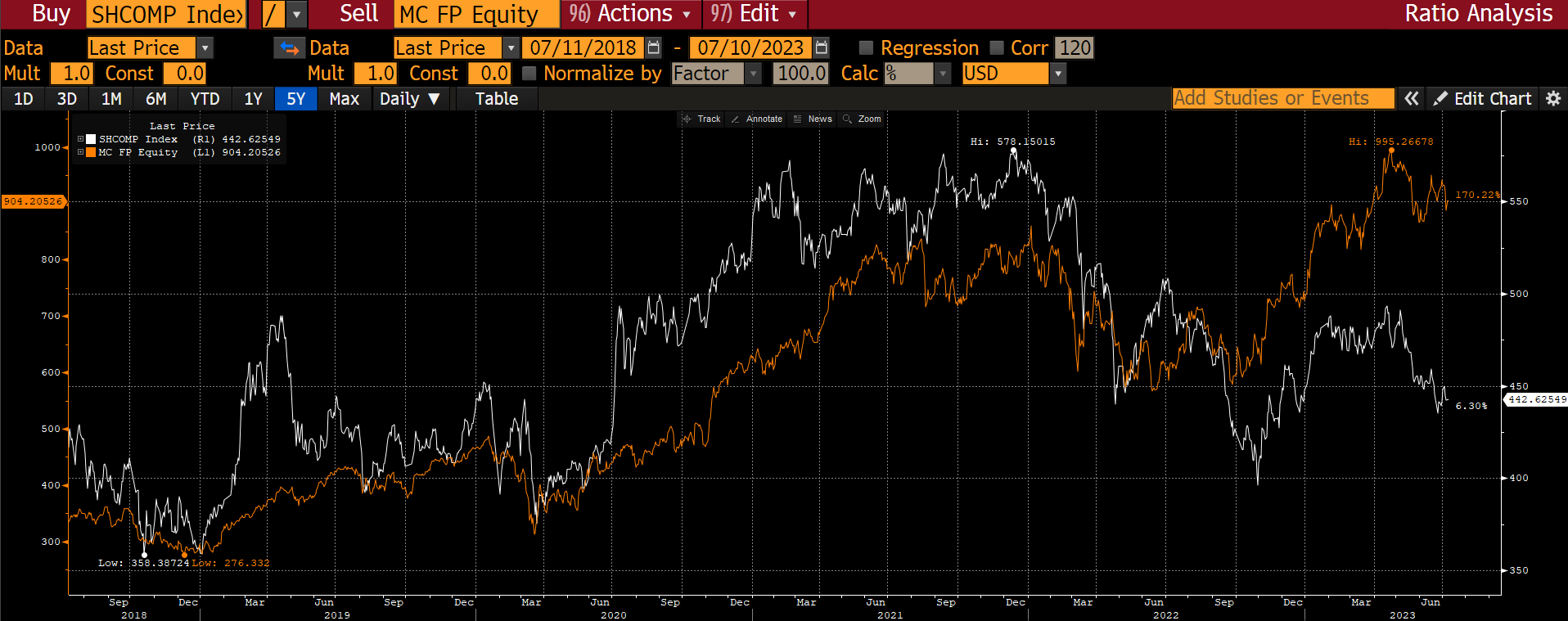

Shanghai Composite vs LVMH (luxury bell-weather):

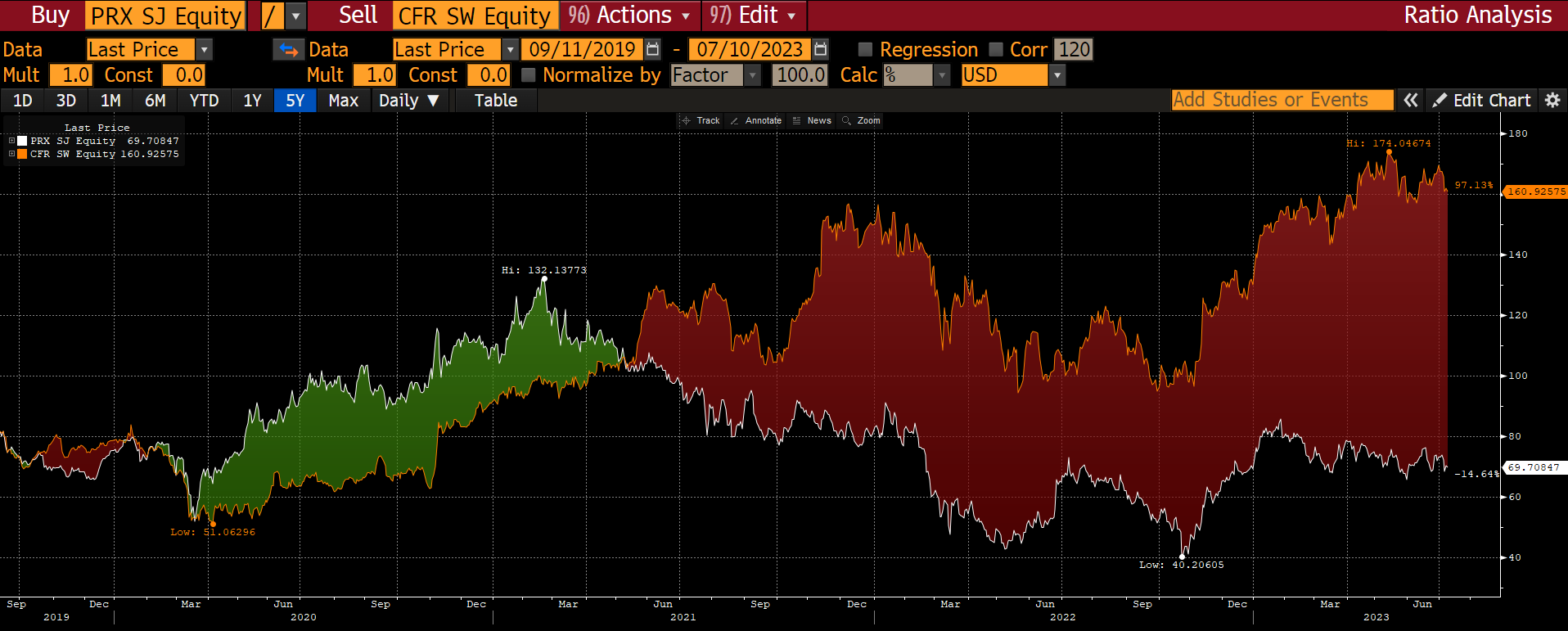

Prosus vs Richemont:

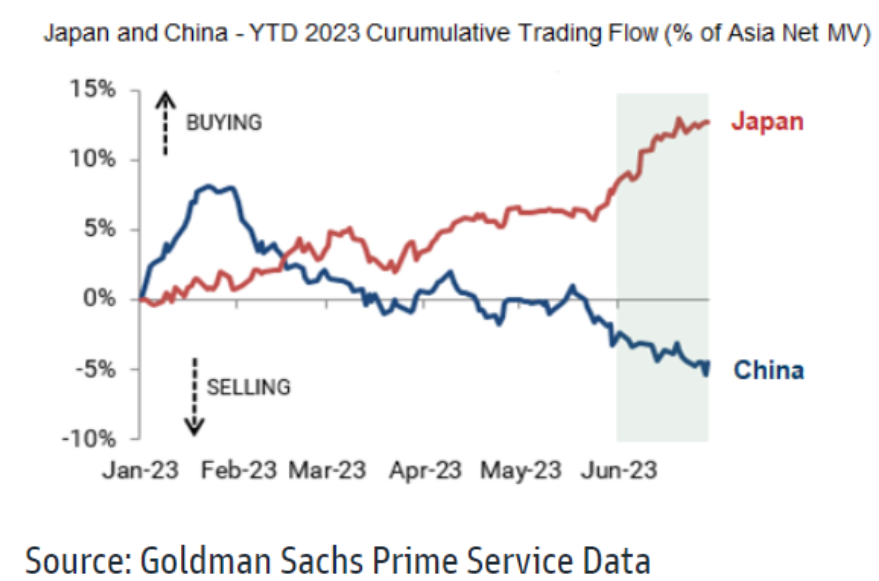

Hedge Funds are exiting China – From a Bloomberg article that quotes GS prime Services.:

Alibaba vs Nasdaq 100: