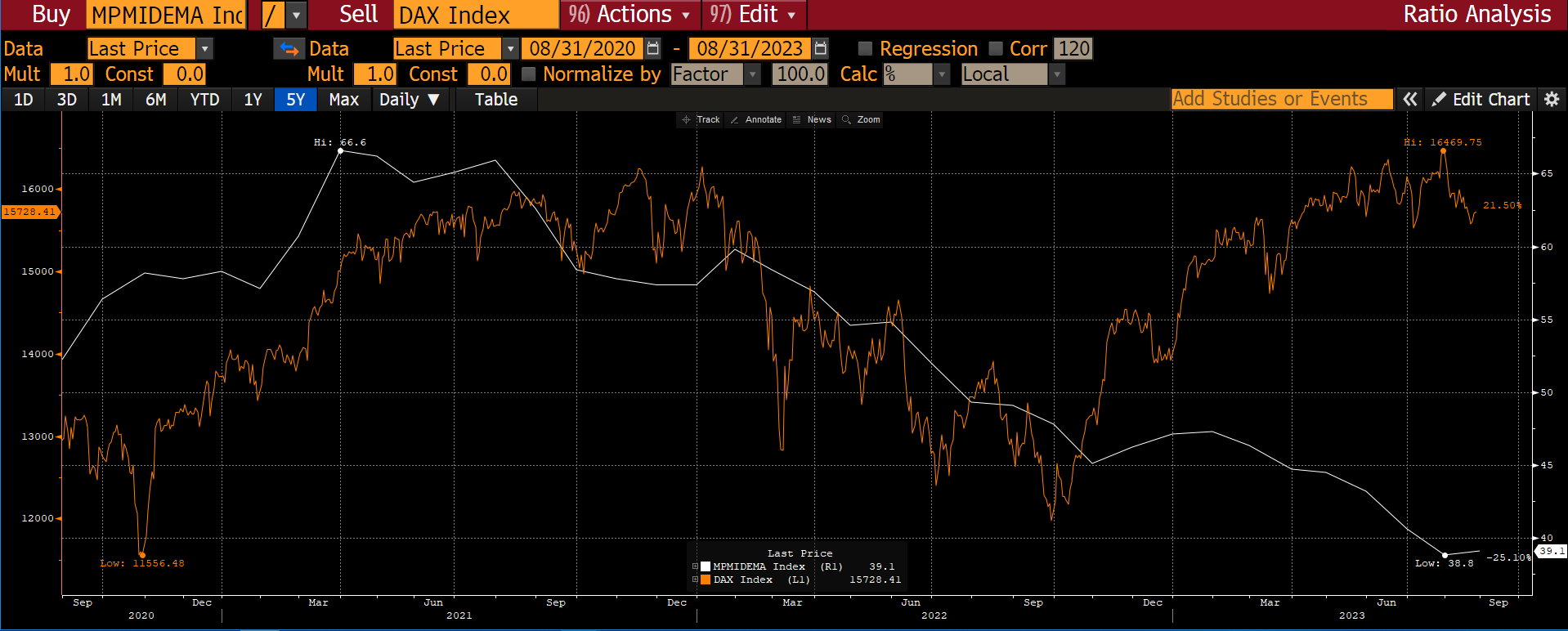

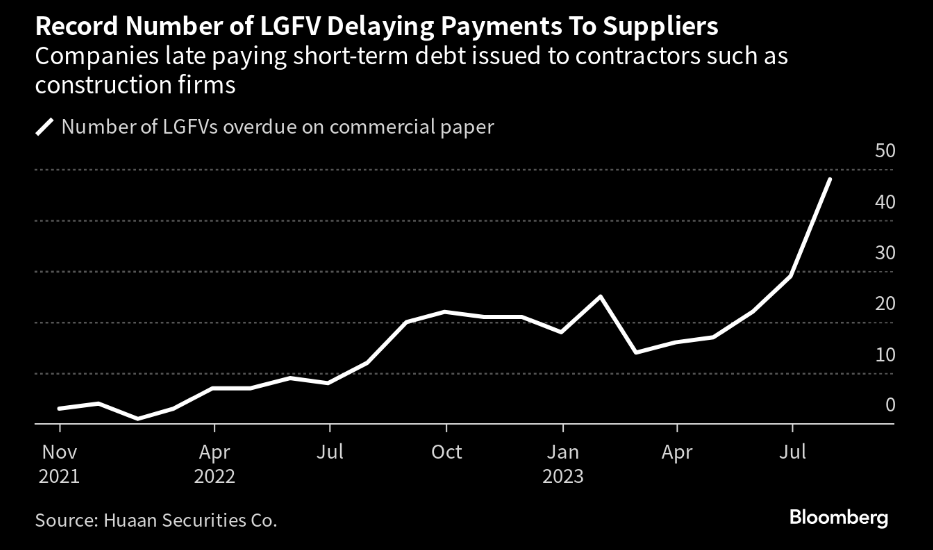

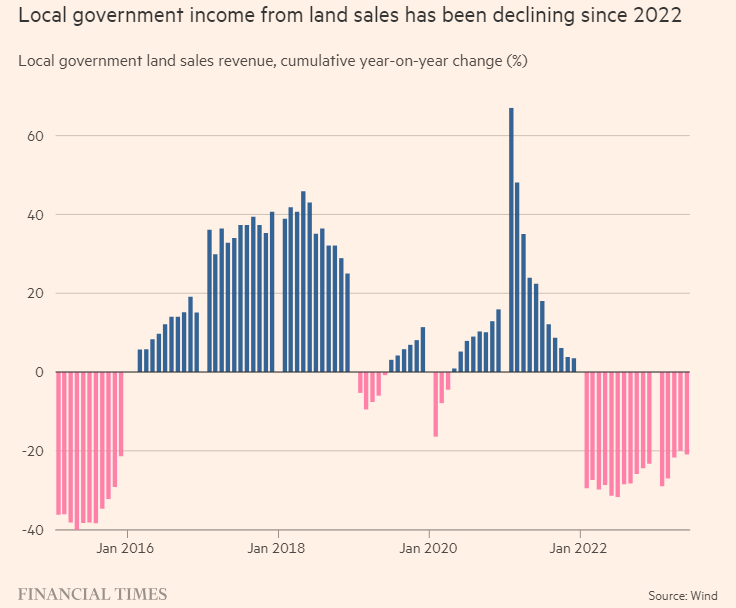

Globally PMIs were released yesterday and all of them were coming in fairly poorly. I cannot remember when a German Manufacturing PMI came in close to 39 the last time. This is an export driven economy and still the 4th largest economy on earth. The global economy and demand are slowing sharply. Long-term yields came under pressure afterwards, i.e. cash was going into bonds. Equity markets interpret this bond move as a risk-on move. The old mantra: “lower yields, buy risk”. Or in other words, bad news is good as the Fed will ease. Inflation is still too high for that scenario though (let’s see what Powell will say at Jackson Hole today) and while rates might have peaked, QT is still here to stay. Add the high (too high) government deficits globally, the fiscal stimulus support is also fading. Talking about the latter, a lot of speculation about China coming to the rescue and stimulating its way out of the crisis. Thing is that China will likely mainly support so called new industries, which is good for the long-term but no traditional quick and easy fix for growth. China also has a financing problem for the old-school “big bazooka” stimulus that many dream about. Yes China talks, but cannot in effect deliver – local-government financing vehicles, or LGFVs are not able to finance in the old way of selling land at the moment – that part has fallen away. Nvidia to the rescue for the bulls – that is excellent and AI will help to spur growth going forward. Going back to lower yields, this should help yield plays to find a bid in the markets. Buying of bond proxies makes sense again. Looking at the released PMIs though, a big part of the economy will face a very hard-landing. Manufacturing is by the way very important for commodity demand, just saying.