Time to think about the next weeks and months. It is the R-trade discussion really. The no-landing at all, soft-landing or hard-landing argument. The no-landing / Goldilocks discussion started particularly after last week’s strong U.S. NFP print. A 6 standard deviation beat (according to Elkhorn Capital Partners). Thing is, ca. 885k full-time jobs were lost in the U.S. while 1.1mn part-time jobs were created, which looks like workers have to take extra part-time jobs to make ends meet. This does not exactly sound like a Goldilocks scenario going into the busiest consumer time of the year to me - it shows the consumer is under more and more pressure. This is also echoed by experts such as former U.S. Walmart CEO Bill Simon, who says consumers are facing pressures they have not felt in years. The soft-landing view comes from people who think inflation has finally peaked and as usual, the Fed’s “put” for markets will be in place soon before these high rates and yields start to break something, i.e. interest rate cuts are coming and the playbook of the last decades is firmly in place. Second round effects coming from wage increases are ignored here. UAW, mining wages, etc. are likely still to be felt though. Central banks are firmly looking to get inflation back to official target levels and we are far from those, unless there are new accepted inflation ranges that are higher than the official ones. For those (and everyone else as well) who think lower rates are coming, please check this article from Oaktree Capital.

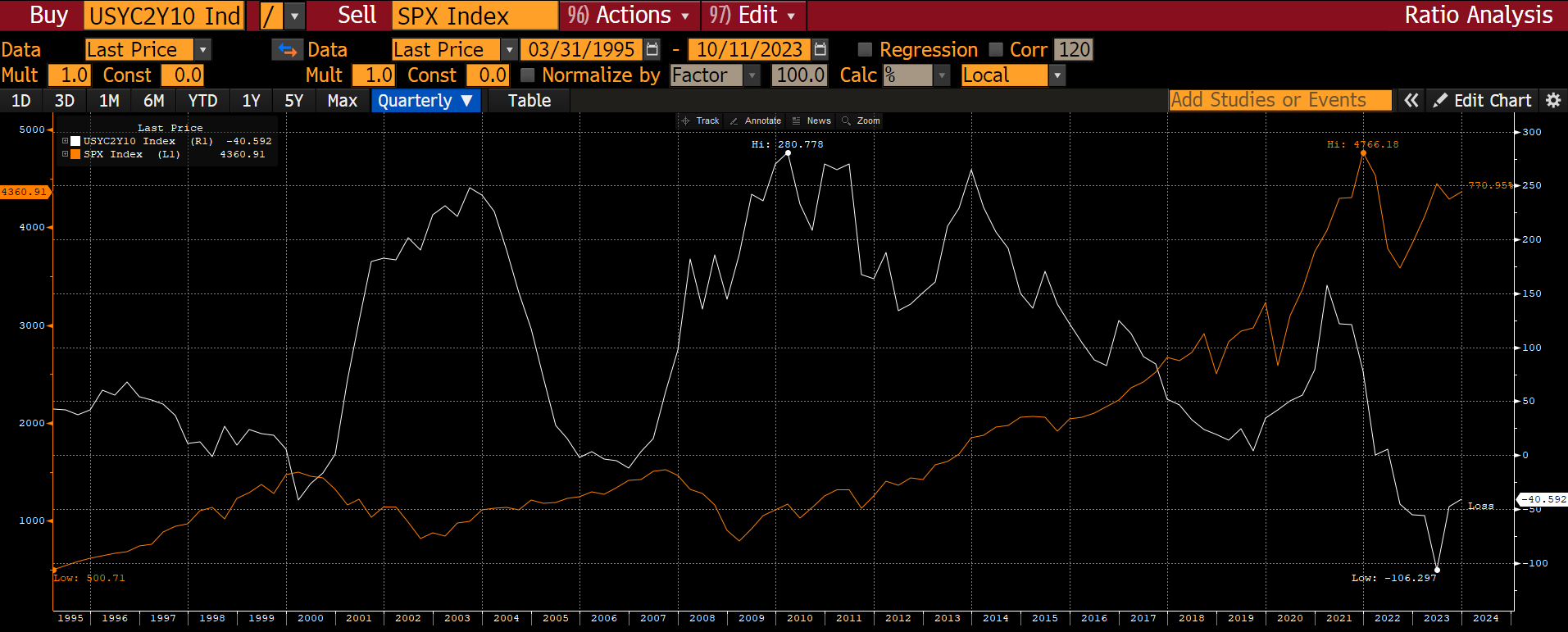

Lastly, QT – most central banks are trying to reduce the huge balance sheets that they have created since the GFC. This leads us to the third scenario, a hard landing. The r-word will have to be mentioned in this case. – let me take you 9-12 months back in time. PMIs started to indicate more than just slowdowns, surveys like the IFO (yes they matter) did the same. Usually, these indicators predict what will happen 6-9 months ahead. All got ignored. Still happening as the music seems to be playing – as this time all is different – again! So, where are we now? We are facing historic levels of government bond issuance while deficits are blowing out. That while only the BoJ is still in QE and not QT mode (and once this changes and it will, wait for the headwind of the Japanese repatriation trade of trillions of assets invested outside of Japan). Yields are therefore to stay higher for longer and something is going to break sooner than later on back – it is all a function of the yield after all in the end. Those high yields are starting to be fairly attractive compared to especially equity yields. It’s a relative world as always! Risk premiums for equities have only risen for small caps so far though. Interestingly, when Treasuries rally, equity investors generally still seem to think this is a risk-on rather than risk-off sign (who’s usually smarter here?!). The R-trade is on in my mind. Long Treasuries (and usually when the curve starts to steepen from negative levels, this is when equities start to come off), long defensive bond proxies (yes, I am still forever puffing bubbles – check those old articles from May and July). Europe clearly seems to face a recession, the U.S. is definitely showing cracks and China has huge problems (India is the new China, but it will take time that India’s commodity hunger replaces that of China). Some graphs that I think are worth highlighting below.

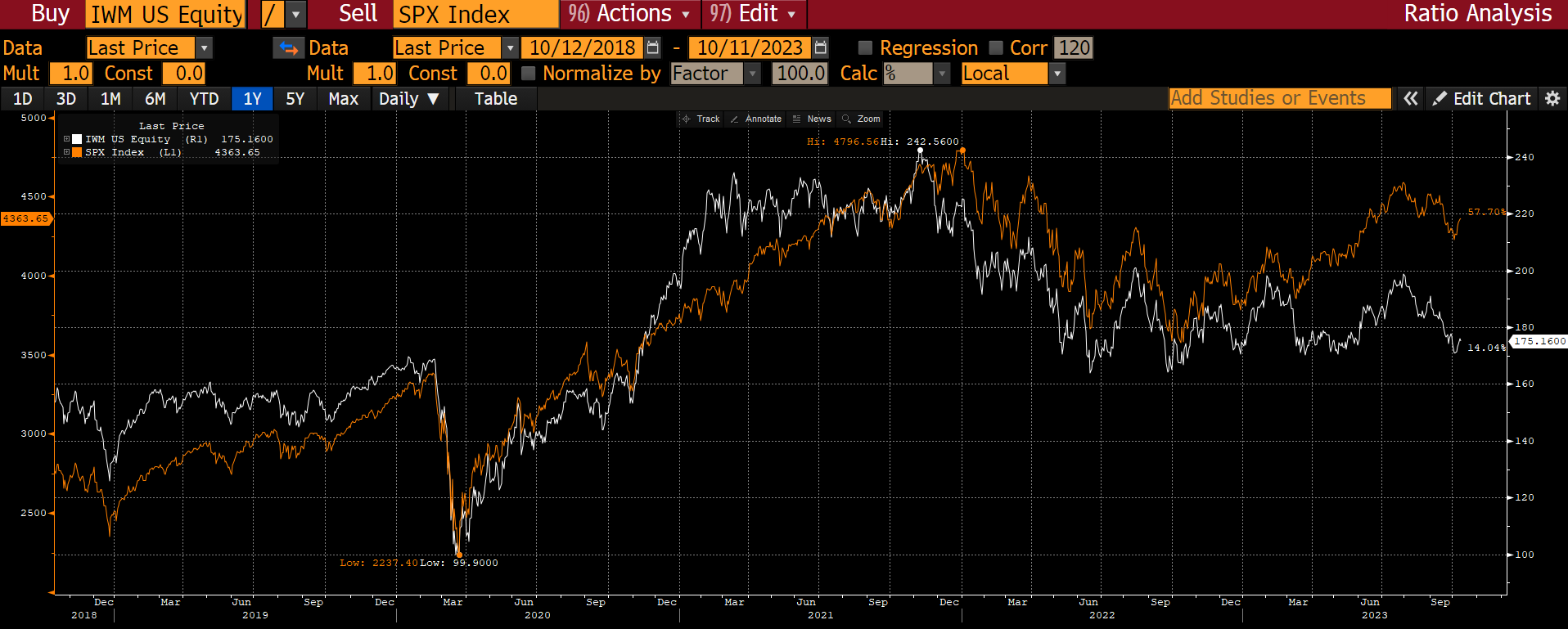

Small Caps vs Large Caps in the U.S.:

DAX vs German Manufacturing PMI:

S&P 500 vs yield curve – when the steepening starts, equities come off.

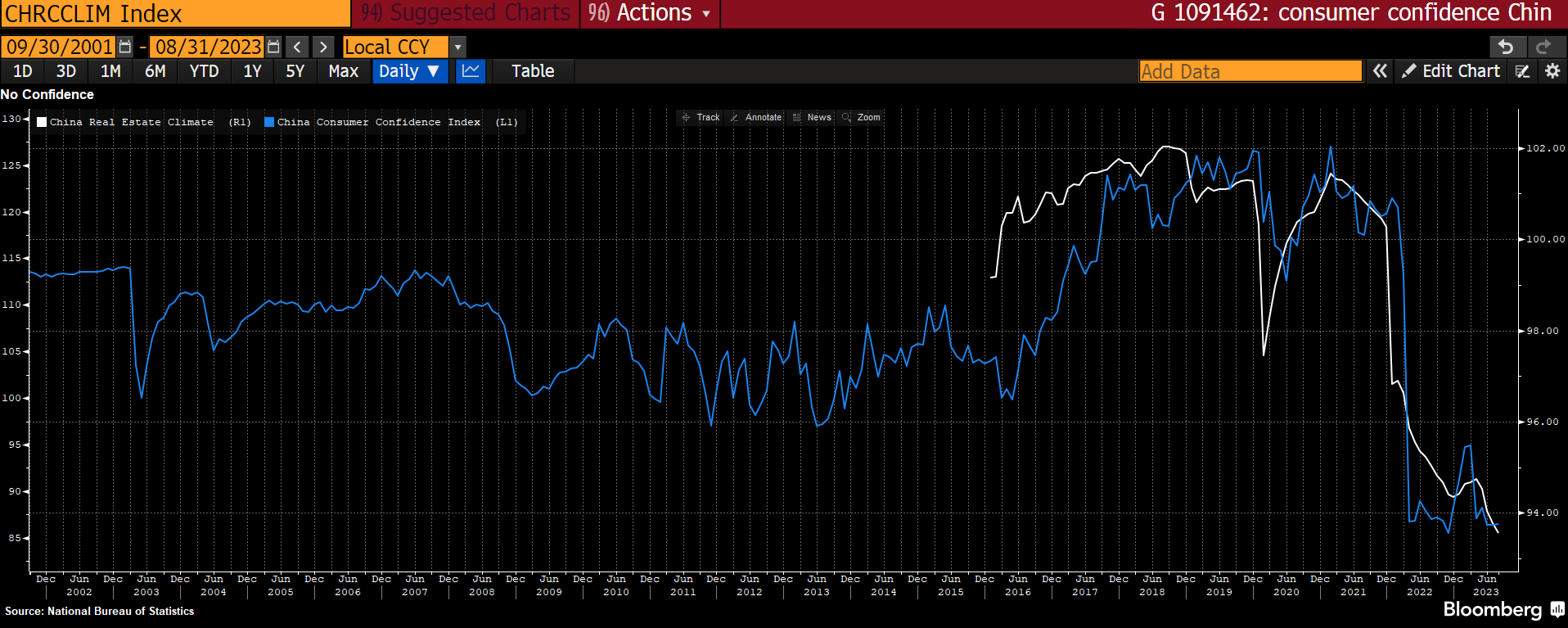

Chinese consumer confidence vs China real estate health – see the wealth effect:

Credit card spending soft according to Citi stats. -11% last month according to a FT article.