The simple narrative is the following. EM bond yields on average show close to zero risk premiums vs DM bond yields. This means, buy DM over EM bonds. Makes sense from a risk reward perspective and the hard currency appeal for EM investors. Now, DM bond yields are higher than equity earnings yields and also dividend yields. U.S. government bond yields at ca. 5% for the short-term and the 10- year maturities. Corporate bonds with even higher yield to maturities. These are equity like returns guaranteed for periods of time – we have not had that for decades. What risk premium to you demand for your equity investment usually and especially in this kind of environment?! This in a market that faces a lot of headwinds still (I will spare you the details as I have mentioned these headwinds and risks in most of my emails, posts and trading thoughts). DM government bonds should benefit from the recession trade, too. In a market where the buy and hold equities narrative has not worked recently. In a market that lacks conviction by equity investors that struggle with liquidity as well. Why not just buying into guaranteed returns? I get it, if rates rise further, there are still downside risks for bonds and not all of us want to buy bonds and hold them till maturity (there would be even bigger downside risks for equities in my mind if yields keep rising though). The level of returns offered to me in fixed income markets now are very appealing – it is as usual a relative world after all. The big rotation trade is here, buy bonds, sell equities. Especially as there are signs that inflation is falling. Some supporting charts and graphs below.

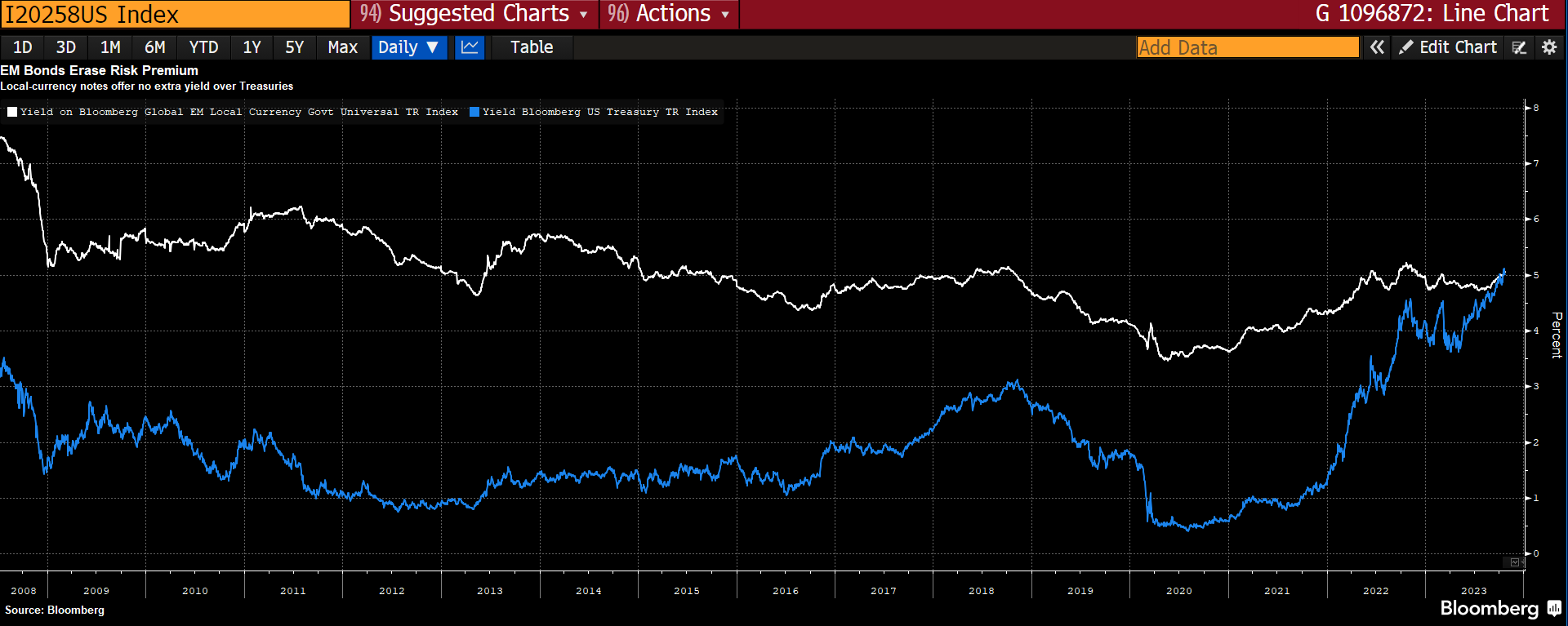

EM bond yields vs DM bond yields (Bloomberg):

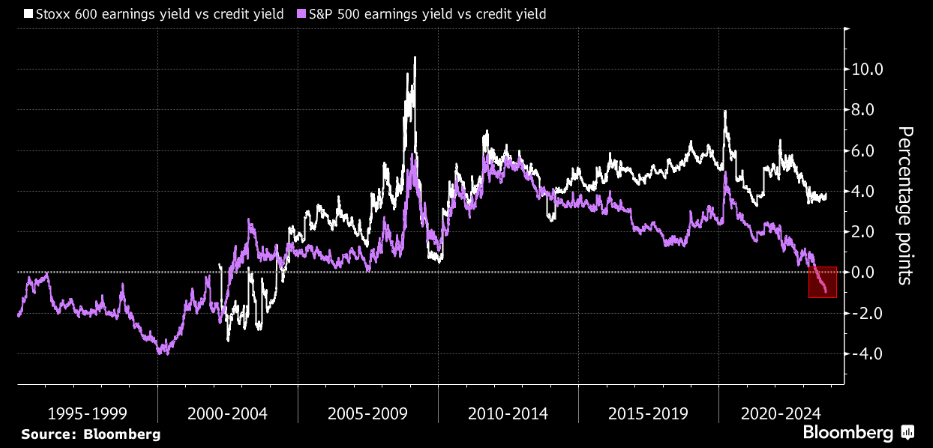

Equity earnings yield vs credit yield (Bloomberg):

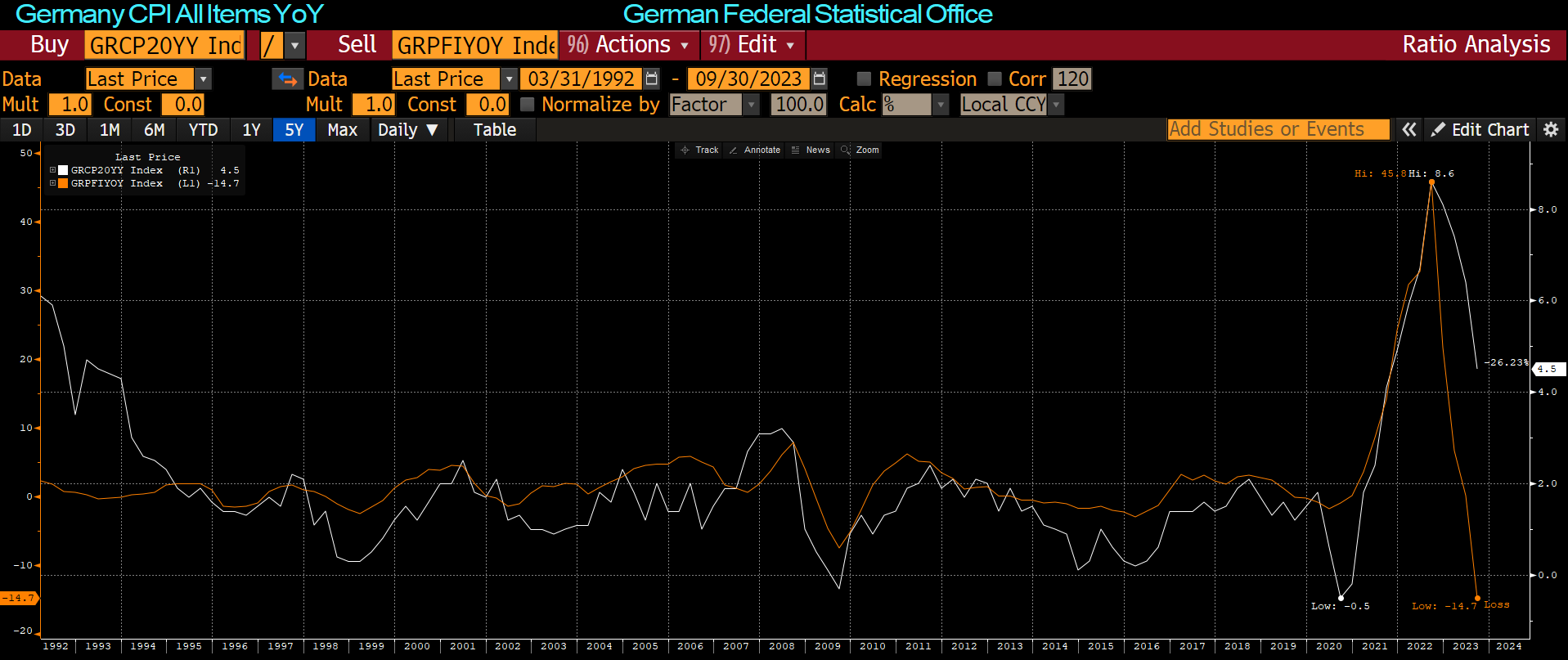

German PPI is leading the CPI (Bloomberg):

High yield equity yields (FT):

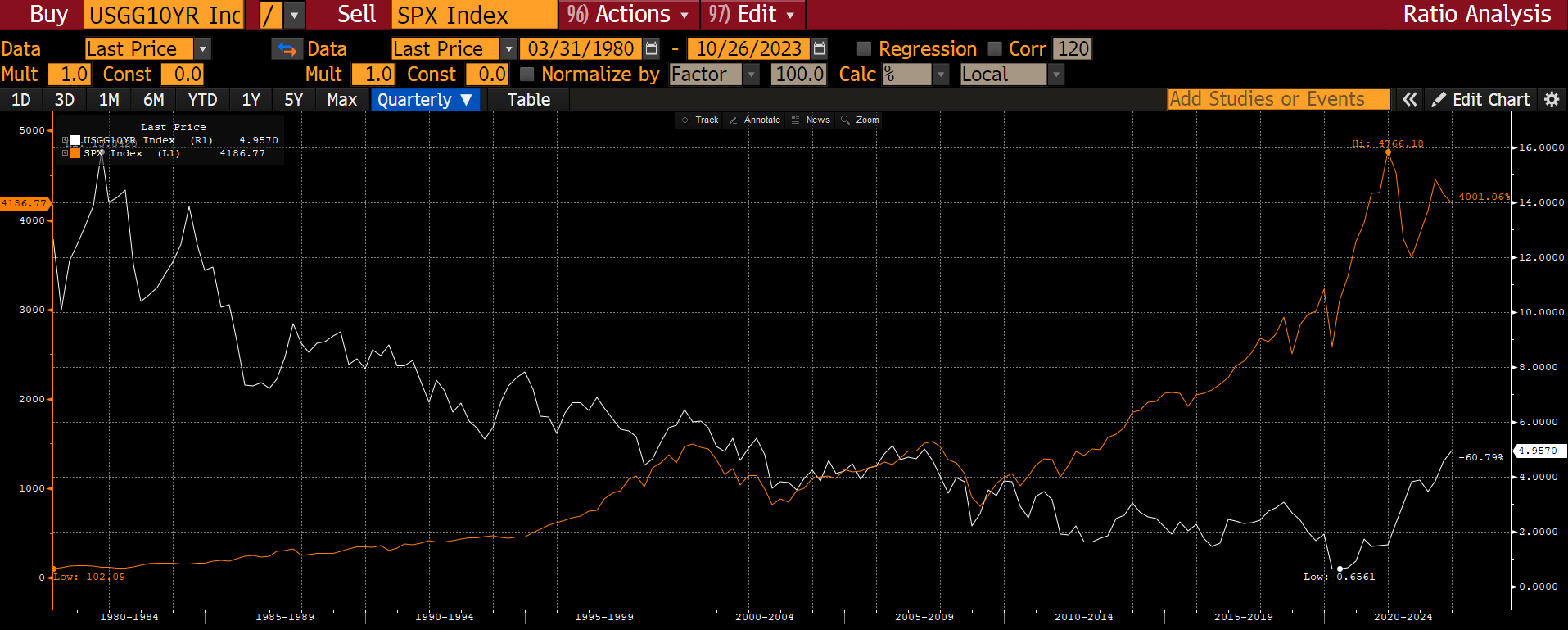

S&P500 vs U.S. 10yr yield since 1980. Everything is a function of rates (Bloomberg).

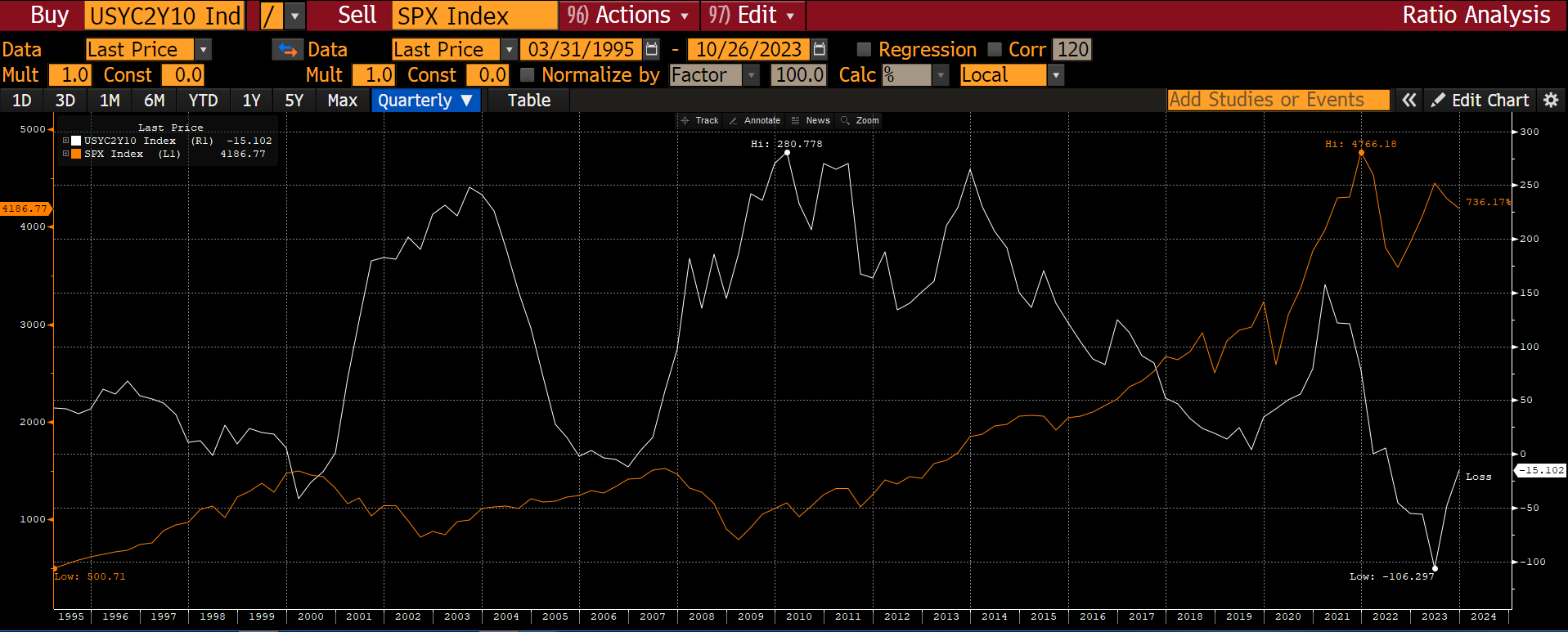

Equity markets sell off when the curve finally steepens again (Bloomberg).