Going into the second quarter and searching for conviction, I like to look at the bigger picture. What are in my mind important drivers for markets currently? In a nutshell and keeping it rather simple, below some food for thought on this.

Living in South Africa (SA), I will start with the mighty Greenback. The USD is trending lower due to U.S. rates peaking relatively, BRIC countries pushing for more trade in their own currencies and of course also due to positioning. This is fairly supportive for emerging market (EM) assets & commodities in general, also as an example for the likes of Anheuser-Busch due to EM revenues and USD debt. The chart on monthly basis below shows the long-term trend for the USD has changed.

South Africa is a China proxy. Hence understanding what is happening in China is important for investors. China is definitely recovering! Recent PMIs are supporting this view. Add the below graph (source Bloomberg) showing massive credit demand in China. This should be fairly positive for commodities, no? What is the read for SA? "Growth" expectations are low for SA currently, sentiment is very bearish. Contrarian long in the making?!

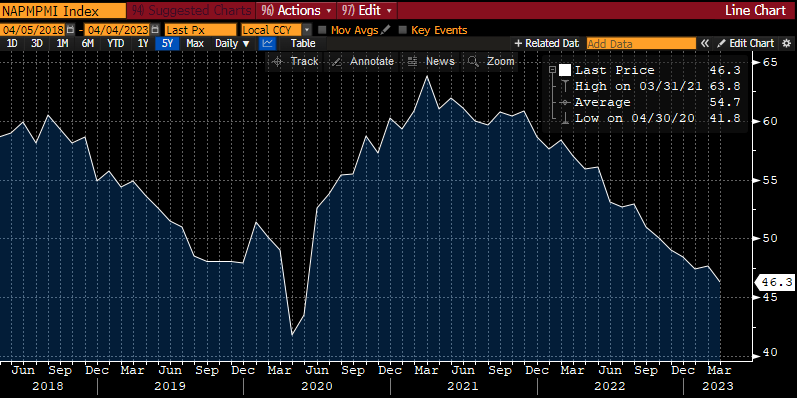

Over to developed markets (DM). That part of the world faces a rather sharp slowdown. Below the U.S. ISM Manufacturing. Similar graphs could be shown for German PMI, German IFO, etc. An earnings recession is likely. Think margins, demand, etc..

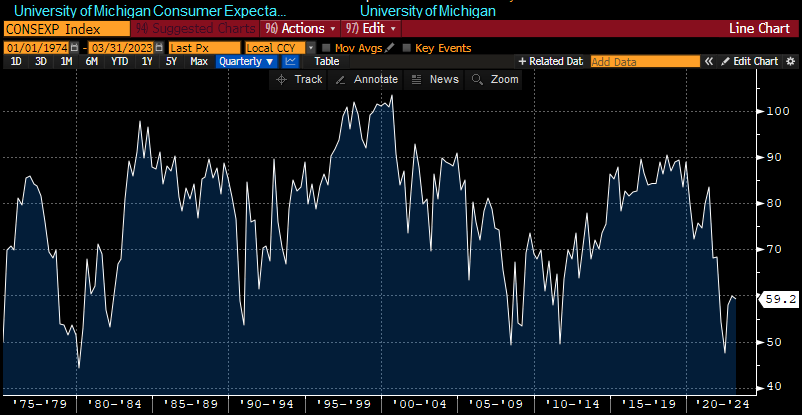

More particularly regarding the DM view, the U.S. consumer starts to show cracks. Credit card debt levels at record highs, housing markets are negatively impacting the wealth effect. This in my mind a negative for luxury especially (Yes, really!). Below the University of Michigan consumer expectations.

What else to consider? While a lot of people are calling peak inflation, a recovery in China, rising oil prices, the ongoing Russian war against the Ukraine and most importantly fiscal support globally and wage inflation likely mean inflation is sticky and staying at high levels. While some central banks might be close to the last rate hikes, this does not mean the market is right in pricing cuts. I think rates will stay higher for longer. Nevertheless, markets are playing the peak view right now and I have to respect that. Next data point will be the NFP print this Friday, imagine a miss here…USD weaker, commodities stronger?!

What other risks do we have to take into consideration? Commercial real estate risk is huge globally, this impacts banks especially in the U.S. currently. There is a tightening of credit conditions overall as a consequence. Add that there is risk the next shoe to drop will be VC & PE portfolios. Bottom-line, a slowing U.S. economy is China’s Achilles heel as exports will slow on back. We need China stimulating its own growth. Looks like we are seeing the latter.

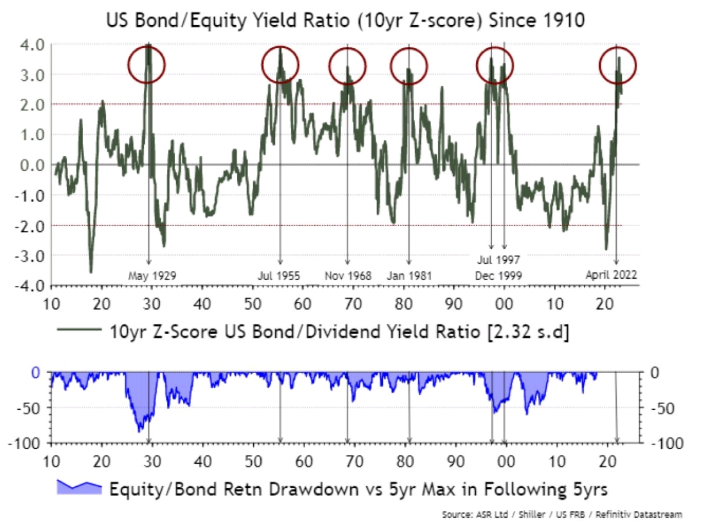

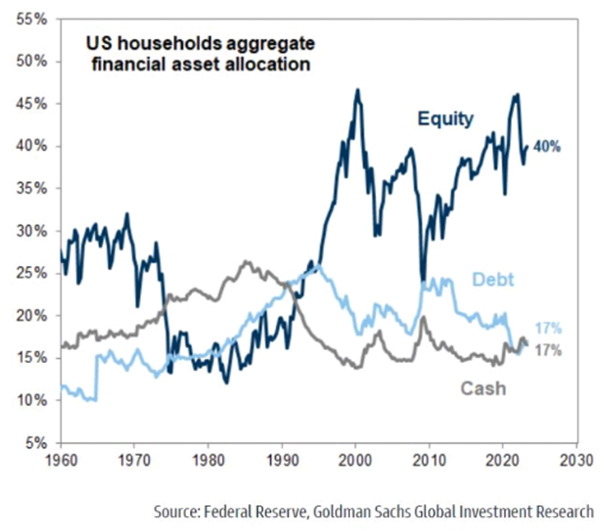

What are the biggest headwinds for equities as an asset class going forward? Asset allocation is a big one. Bond yields > EQ yields. There should be a massive shift from equities into bonds, especially considering overall positioning. Below graphs are supporting this view. (Source for below graphs: ASR Ltd., Shiller, Refinitiv Datastream, Federal Reserve, GS Research).

Last one to monitor are Japanese yields. Inflation is starting to become a problem for Japan, too and the BoJ is the last central bank still in QE mode. A change of this policy and rising yields on back (especially when happening too fast) will mean risk of repatriation of some of the estimated $3-4trillion of investments Japanese hold outside of Japan.

Enjoy the upcoming holidays!