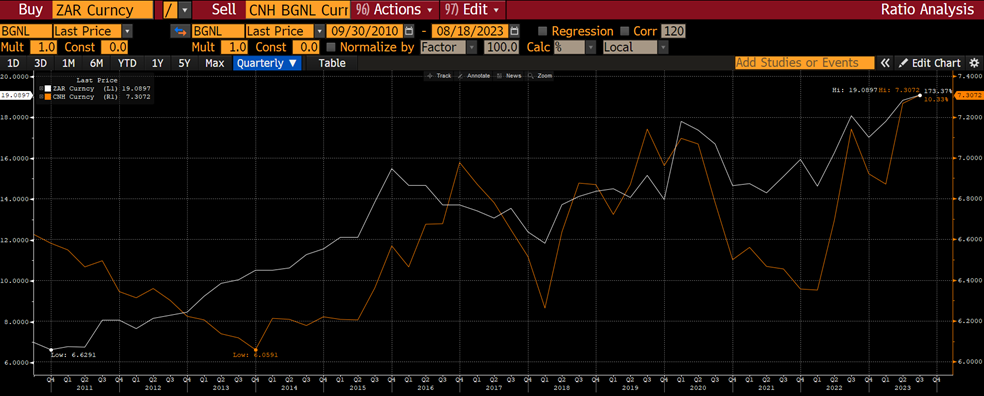

Let’s start with South Africa (SA) being a China proxy. – see the Rand vs. Yuan below – quite correlated over time. We are an economy that sells raw materials, 60% of SA’s exports are commodities – mainly iron ore, PGM (platinum group metals), gold, diamonds and coal. China for decades has been the main driver for industrial commodity demand and SA benefited from that tailwind. Unfortunately, SA has not used the tailwinds it had, the money has not been invested into infrastructure. We all know what happened.

China’s steel demand has been driven by building infrastructure and also by its factories that produce for the world. One of the biggest part for China’s steel demand though has been China’s property market, consuming close to 300 million metric tons of steel bars per year. That’s ca. 30% of China’s total steel consumption p.a., or ca. 15% or the world’s annual steel consumption. We all know what is happening in China’s property market now and this time I won’t mention all the other implications this has for consumer confidence (LUXURY!), wealth effect and so on. This time I focus purely on the read for SA. 52% of SA’s iron ore exports go to China and ca. 22k people are directly employed in SA’s iron ore sector. Imagine China’s demand slows down significantly just purely on lower demand from the property sector, not even thinking about the world slowing down and less demand overall.

Over to the PGM sector. The world is changing and in Europe and China particularly electric vehicles are taking over. Believe it or not! This trend is unstoppable – thing is that the current batteries use ZERO (0%) of the PGM metals while cars that use diesel or petrol are the major driver for PGM demand (catalysator usage). A structural headwind for one of South Africa’s largest industries. Demand for jewelry and dental fillings are small compared to this. A massive problem for SA – ca. 172k people are directly employed in the sector. Only the green hydrogen economy will be the next positive catalyst for the sector and that is in optimistic scenarios at least 5 years away from now – when that’s coming though, there is not enough platinum on this planet btw. Cyclicals remain cyclicals.

What does that mean for the SA PGM sector? Structural demand headwinds for the time being until the hydrogen economy becomes a reality.

While I mentioned employment, the far more negative implication of these two factors (China & electric cars) are the read for the SA tax revenues. The Mining sector contributes ca. 40% to SA’s corporate tax collections. This is important for our views regarding the Rand, SA bond yields and also economic growth.

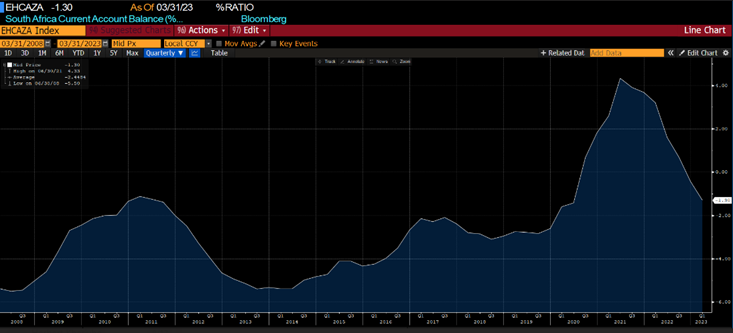

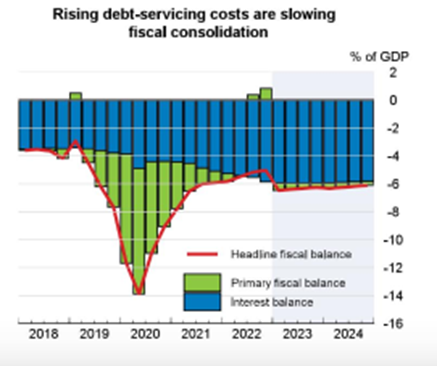

Some graphs below (current account deficit and debt servicing cost), sources Bloomberg and OECD.

Obviously I do not want to finish this comment on a negative note! If we see SA’s CPI coming in below estimates next week, markets might quickly start to talk rate cuts (I disagree until we see the U.S. cutting) and that will translate into some relief for consumers – unfortunately that would also weaken the Rand. Never easy.

Have a good weekend all!