Bottom-line: We outline market implications of the South African elections in this note, focusing on asset class performance rather than political views.

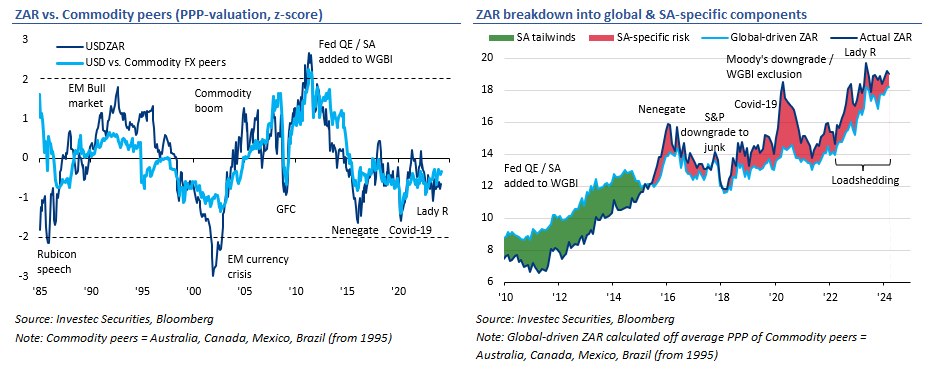

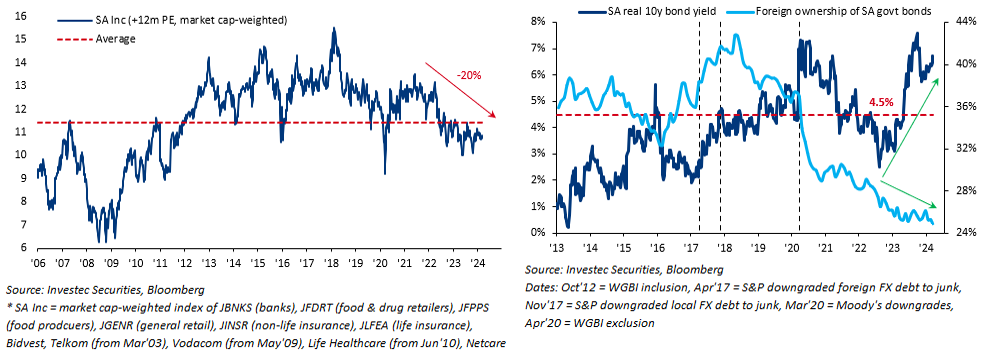

Backdrop: domestic assets are cheap and underowned … SA Inc trades at a +12m PE of just 10.7x; foreign ownership of bonds reached a new low of 24.9% despite soaring real yields. Breaking down ZAR into its global & SA-specific components shows ~ZAR1/USD of additional SA risk priced in at spot (vs. ZAR1.50 during last year’s Lady R newsflow, ZAR2 at Nenegate, ZAR4 when peak covid fear coincided with the exclusion of SA bonds from the WGBI).

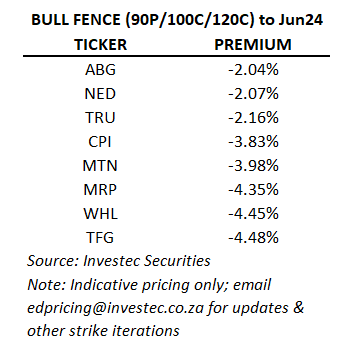

Bull case: ANC loses enough votes to require a coalition with a sizeable multi-party charter. A sense of urgency from the ANC on key issues combined with oversight from coalition members could see investors price in a reform ‘high road’ with USDZAR < 17.50 and a 20-30% broad based rally in SA Inc (bull fences on key SA stocks with strikes at 90 / 100 / 120 cost ~2-4.5% out to Jun’24).

Coalitions: Who the ANC forms a coalition with is more important than the actual percentage of votes they achieve; smaller coalition partners = smaller ZAR & SA Inc rally; left-wing coalition = ZAR blowout. Longer term equity performance requires at least a few checkboxes from the local reform list to be ticked, or for global factors to drag SA higher (Fed rate cuts / China stimulus).

Trades

- USDZAR fence with strikes at 16.00 / 17.00 / 21.82 (19 Sep’24 expiry) Client sells 16.00 put (to help lift the upper bound while keeping overall structure at zero-cost), buys 17.00 put, sells 21.82 call

- Bull fences on SA Inc stocks with strikes at 90 / 100 / 120 (Jun’24 expiry)

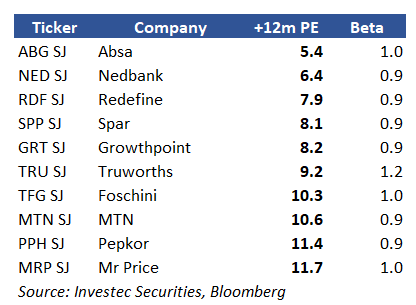

- Stock screen: Investec Buy-rated stocks with +12m PE < 12x, Beta > 0.9

Scenarios

Our scenarios assume that the ANC would win the biggest share of votes but would likely need to form a coalition to achieve an overall majority vote. Who the ANC forms a coalition with is more important than the actual percentage of votes they achieve (the percentages in parenthesis are a rough guide only).

- ANC majority (>50%, no coalitions) … Status quo maintained. ANC could lose control of another key province (along with the Western Cape). Ramaphosa becomes the only ANC president to serve two full terms. Debatable whether this means reform speeds up, or whether it just continues at its frustratingly slow pace.

- ANC-led coalition with one/a few small political parties (ANC 45-50%) … ANC loses enough votes to spark a sense of urgency on at least key issues like Eskom & Transnet.

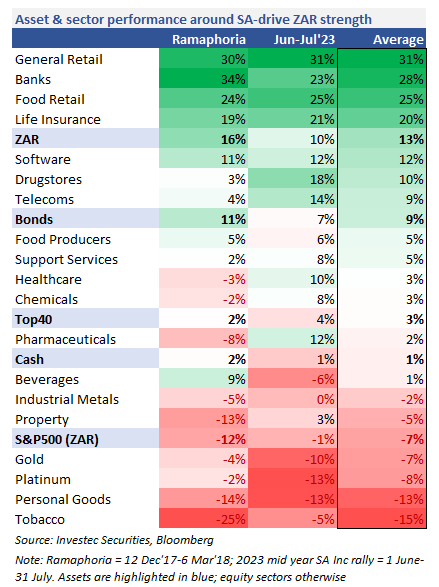

1 & 2 would be fairly standard for South African elections in that ZAR weakens into the elections amidst a tug of war between leftist policy rhetoric and more pragmatic official statements … ZAR & SA Inc breathes a sigh of relief when the worst case doesn’t play out … but then settles back into its longer term trend (chart below).

3. ANC coalition with the Multi-Party Charter (DA, IFP, FF Plus, ACDP, ActionSA + other small parties), or just the DA (ANC 40-45%) … Does increased oversight from coalition members with a larger share of the vote mean investors factor in a reform ‘high road’? Perhaps.

Similar to 1 & 2, but bigger moves. In the case of a big SA Inc rally, history says that retailers and banks outperform but the rally would be broad based rather than concentrated in the quality stocks.

4. ANC coalition with the EFF / MK (ANC <40%) … A necessary evil for the ANC if their share of the vote is low (say, 40% or less) and a DA-led coalition garners enough votes to be able to challenge the incumbent ruling party.

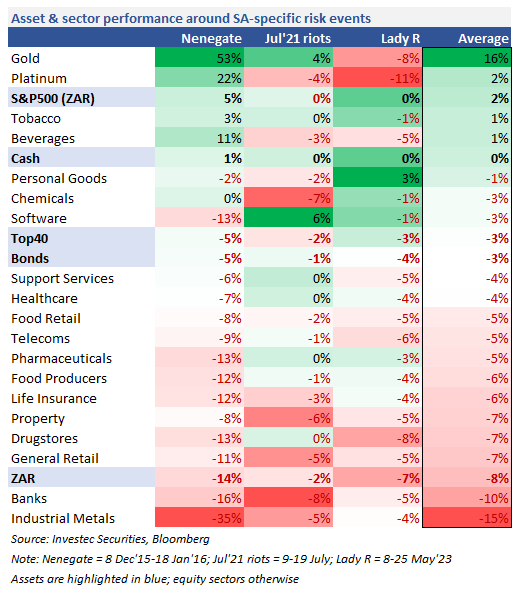

Elevated risk of leftist policies and unstable provincial governments would be priced in via a sharp depreciation in ZAR & a sell-off in SA Inc. It’s tough to find a historical anlaogy but we use periods of heightened SA-specific risk as a guide to sectoral performance.

Unloved SA Inc

The election outcome is just one puzzle piece in a bigger picture of cheap, underowned domestic SA assets (charts below).

- Equities … SA Inc trades at a +12m PE of 10.7x (20% below the highs set during the post-covid rally). Since 2012, this basket has only traded near current levels during periods of crisis

- Bonds … Foreign ownership of SA bonds reached a new low of 24.9% despite soaring real yields

2023 seemed to mark an inflection point in the way investors, especially offshore, look at South Africa. Record high loadshedding, Transnet inefficiencies, FATF greylisting, some corporate slip ups … collectively this has seen the shortlist of quality SA stocks shrink further, and there was a combined outflow of ZAR500bn from SA equities & bonds. 2024 has been somewhat of a continuation of this with an outflow of ZAR68bn from equities & bonds YTD.

Valuations alone don’t often drive rallies but off such low levels, any incremental positives could spark a sudden rebound that’s larger than most investors expect. Longer term performance requires at least a few checkboxes from the bull case to be ticked – improved loadshedding with a clear path to this ending by early ’25, cost & efficiency wins at Transnet under their newly appointed CEO, SARB cuts rates to stimulate growth, China/global growth drags SA higher, consumer spending gets a boost from ‘two pot pension’ withdrawals, SA removed from the FATF greylist, more corporate action / buybacks / consolidation.

Risks: Inclusion of India’s government bonds in JP Morgan’s EM indices from Jun’24 sees an estimated USD2-3bn outflow from SA bonds, Eskom / Transnet woes continue, SARB & Fed both delay rate cuts, US elections see a stronger USD (and/or renegotiation of AGOA), Chinese policy stimulus disappoints.

Best,

Nadeem