There’s lots of talk about yield curves these days. Investors, borrowers and analysts all closely watch the curve. Some even want to ride the curve. Imagine that.

But, what the heck is a yield curve?

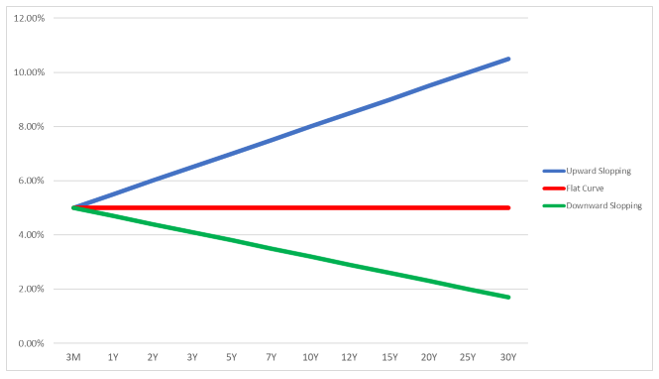

Ah! It’s just a picture of interest rates out to say, 30 years. Like a polaroid snapshot. Click. And there you have it. Interest rates frozen at a point in time.

Source: Investec Corporate and Institutional Banking

So, there will be an interest rate for 3, 6 and 9 months…all the way out to 30 years. And then all these points are joined up by a line or curve. And that’s a yield curve. Bold and beautiful.

Sometimes curves are flat and very boring. This would be when 3 months rates are more or less the same as long rates e.g. 10 year rates. At other times these curves can be breathtakingly steep, e.g. when 10 year rates are say 4% higher than 3 months. This is a steep upward sloping or positive yield curve,

The opposite is also true. Yield curves can be downward sloping or negative, for instance when 10-year rates are much lower than 3 month.

So what. Who cares…you ask.

Well, the shape of the yield curve tells a story. And we all love stories, especially investors and borrowers. These guys always need to know where interest rates are going. And no one knows. Sure, economists have their views and forecasts, but they are just that, forecasts.

That’s why yield curves are so exciting. Because these curves are not forecasts, but are the market’s actual expectations of what interest rate are going to do.

Why is this the case…?

This is so, because investors who buy government bonds (debt) expect (or demand) to earn a certain interest rate for lending to the Government over various periods. Similarly, for investors who place funds with banks for various terms.

Now, these investors, as you can imagine are shrewd guys. And they would want to earn rates based largely on how they feel about economic growth and inflation. And how this might affect central banks’ interest rates.

Because these investors would expect to earn a higher fixed rate from lending (or investing) for longer periods, yield curves are usually upward sloping.

Investors view short-term rates out to 12 or 18 months, as what will happen to central bank policies in the near term e.g. how will the central bank adjust borrowing costs like the repo rate. (And therefore, also prime and Jibar).

The reason why people get so excited about the yield curve these days, is because historically it has been a good predictor of the start of a recession.

How can this be?

Well, when an economy is slowing, investors start to lower their inflation expectations. And, therefore also what they expect to earn on 10-year and 30-year bonds.

These rates then start to drift down towards the shorter maturities, such as 3 months and 2-year bonds. The buyers of these bonds feel there is less need for central banks to raise their borrowing costs in the future.

And just like that…the yield curve starts to flatten. It is this flattening, which can give a recessionary signal, especially if the yield curve becomes downward sloping or inverted. An inversion of the yield curve has preceded every US recession for the past half century.

The yield curve steepens during periods of low economic growth, where governments use low interest rates to encourage spending and boost economic activity. (This happened following the 2008 financial crisis. And earlier this year following the pandemic recession).

The reason for this steepening is that investors expect higher rates in the future, because the economy becomes stronger from lower rates which in turn may speed up inflation. Eventually the cycle reverses and the central bank would have to raise rates to encourage saving over spending.

Okay. So, now you know what a yield curve is. But, how do you ride the curve. Well, as an investor you could buy a 5-year bond and fund it with overnight or 3-month funds. Just like that.