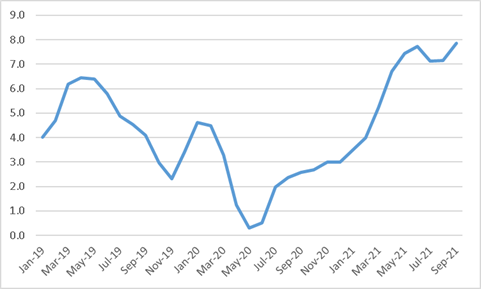

Producer price inflation in September accelerated by 7.8% from 7.2% in the previous month. The outcome was well ahead of Bloomberg consensus forecasts of 7.3%. While base effects contributed to the acceleration, price increases were broad based. E.g., Prices of machinery and equipment and computer equipment increased 2.6%m/m and chemicals, rubber and plastic products (1.1% m/m). There is a substantial number of manufactured goods that have recorded double-digit price increase compared to 2020, e.g., Rubber (+15.6%), metal,s machinery, equipment, and computing equipment (+10.8%), structural and fabricated metal products (+14.9%). Prices of base metals goods are up by 44.1% and plastic goods by 22.2%. Higher fuel and diesel prices have also exerted upward pressure on the PPI. When energy is excluded from the PPI, prices have increased by 6.6%.

Intermediate goods inflation has continued to accelerate, reaching 19.5%y/y ib September compared to 8.6% at the beginning of the year. However, when the prices of basic metals are excluded from intermediate prices, then prices are 14.5% higher. Producer price inflation reflects the global supply-side shortage, the surge in commodity prices, the weaker exchange rate, and rising electricity prices. Agriculture PPI remains sticky, rising by 9.6%y/y from 8.6%. The outcome warns of significant pipeline pressures. The pass-through from higher input prices have not yet been reflected in the CPI, partly because services inflation remains muted but also because of relatively weak demand with the output gap negative. However, today’s PPI will undoubtedly leave the MPC with some sense of unease.

Figure 1 PPI inflation