Another CPI inflation surprise

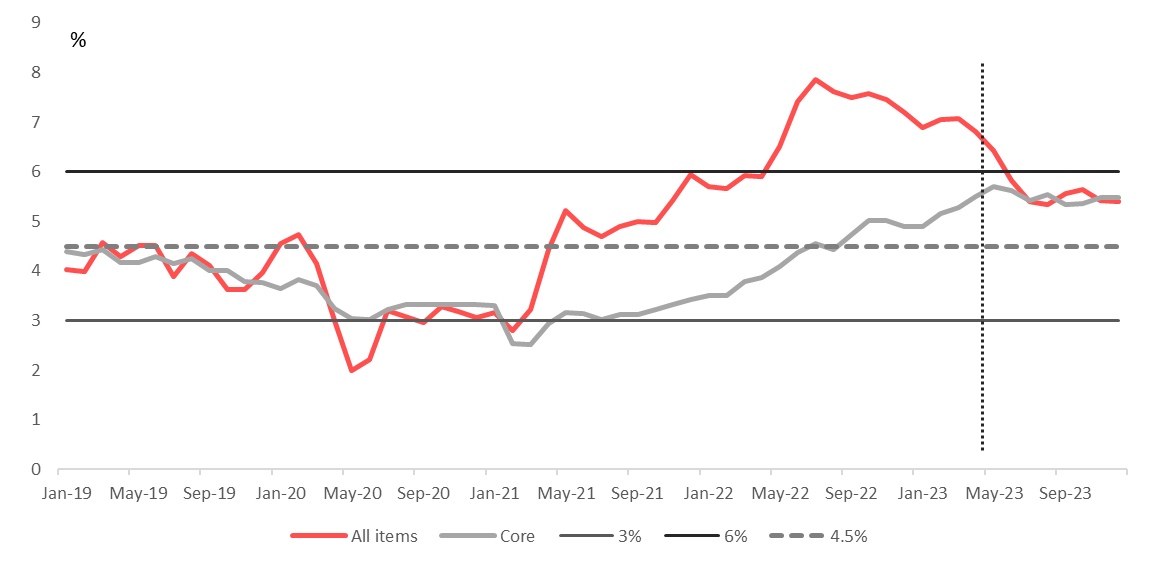

Inflation accelerated for the second consecutive month in March, rising from 6.9% to 7.1%. The outcome exceeded ICIB's forecast of 7.0% and Bloomberg's consensus of 6.9%. Core CPI inflation was unchanged at 5.2%.

What happened?

- Food and fuel prices continue to drive headline CPI inflation higher.

- Food price inflation accelerated from 14.0% to 14.4%. and is now at the highest level since the early 2000s. The monthly rate of increase of 1.04% has yet to show signs of moderating and was in line with a 14-month average (Jan 22 to Feb 23) of 1.06%. The most significant increases were recorded for the following:

- Bread and cereals (+0.9%vs 14m ave of 1.6%).

- Dairy and eggs (2.0% vs. ave of 0.9%) as prices of cheese surged by 6 – 10%m/m;

- Vegetables (+3.8% vs. ave of 1.3%) with significant monthly increases for beetroot (+14.3%), broccoli (+7.4%), tomatoes (6.1%), peppers (+6.2%), cucumbers (+6.7) and potatoes (+5.0%). Onion prices declined by 2.3%m/m but are 45.0% higher than a year ago.

- Sugar, sweets and desserts (1.6% vs ave of 1.1%) and other food products +0.9% vs ave of 0.8%).

- Protein prices have started to stabilise, and declines were recorded for specific cuts of sirloin, pork, mutton, and chicken (fresh) whereas the price of hake increased by 4.7%).

- Food price inflation accelerated from 14.0% to 14.4%. and is now at the highest level since the early 2000s. The monthly rate of increase of 1.04% has yet to show signs of moderating and was in line with a 14-month average (Jan 22 to Feb 23) of 1.06%. The most significant increases were recorded for the following:

- Fuel price disinflation was reversed as petrol and diesel prices increased by 122c/l and 30c/l, respectively. Fuel prices are 4.5% higher than in the same month in March when Russia's invasion of Ukraine resulted in a 295c/l increase in the pump price. Public and private transport consequently increased prices over the month but base effects resulted in a moderating in the annual rate of increase to 8.4% (P: 10.4%) and 14.5% (P: 15.8%).

- The difference in prices in March 2022 and March 2023:

March 2022 March 2023

Brent spot: $112/bbl $79/bbl

USDZAR: R14/96/$ R18.26/$

Diesel crack spreads: $20.6/bbl $21/5/bbl

Gasoline crack spreads: $12/bbl $16/bbl

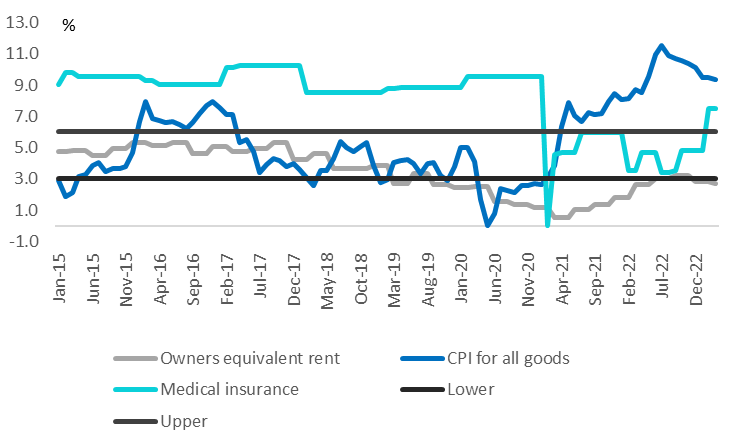

- Core CPI inflation, closely monitored by the SARB for pass-through effects from higher input costs, was unchanged at 5.2%. March is a large survey month, including measuring homeowner's equivalent rent, actual rentals, and education. The housing category remained an important anchor of services inflation, with both categories recording a softening in price increases from 2.9% to 2.7% and 2.8% to 2.7%. Education, however, recorded more meaningful increases. Primary and secondary tuition fees rose from 4.4% to 6.1% whereas tertiary education fees increased from 4.2% to 5.3%. The weaker rand and a surge in printing paper prices resulted in prices of books, newspapers and stationery rising from 4.4% to 10.2%y/y. Categories, where a moderation in price increase was evident, are package holidays (6.4% from 10.6%) and hotels (+4.8% from 6.1%).

Outlook

- The SARB revised its headline CPI inflation forecast to 6.0% from 5.4% in 2023. The 4Q23 average was raised from 4.6% to 5.3%, and the balance of risks remains on the upside. Several issues bear close monitoring:

- A key challenge is the risk of elevated inflation (driven by food and fuel) feeding into higher inflation expectations. The BER's 1Q inflation expectation survey continued to be revised higher.

- SA's output gap is very small and has recently moved to zero because of the electricity constraint (the difference between actual and potential growth) which implies that demand (even if weak) in excess of supply could absorb price increases.

- EM and SA's ability to attract foreign capital inflows in the context of (1) higher DM global neutral policy rates as inflation is also stickier in Europe, the UK and the US and (2) an anticipated current account deficit with weaker terms of trade.

- While the disinflation process has been slower than expected, headline CPI inflation is expected to make a more convincing decline in coming months and 2Q23 could average 6.4% from 7.0% in 1Q23. Base effects will be a key driver. Food price inflation is expected to remain sticky until May before it could start to moderate in 2H23. In a call with Wandile Sihlobo from Agbiz hosted by Ayan, Wandile noted the following:

- For April, we will likely see the continuation of the tail-end effects of the high grain prices of last year. If sustained, the current relatively cheaper grain prices will filter mainly in the year's second half. There is a lag between three and five months between farm and retail prices of some products. Other product prices that could remain elevated in the near term are fruits and vegetables. The unfavourable weather conditions over the past few months disrupted production; hence, some vegetable product prices picked up in recent months. But this will be a temporary blip and should also soften in the year's second half.

- The impact of load-shedding may also influence prices for the next few months. The mitigating measures businesses are currently making to improve power supplies, along with the diesel rebate announced by the Finance Minister, should bear fruits later in the year.

- Positively, global agricultural commodity prices are softening. If the rand/dollar exchange rate remains relatively strong, this will soon be a reality in South Africa, with a lag at the retail level. Notably, South Africa had a favourable agricultural season following adequate rainfall. The 2022/23 summer grains and oilseeds production is estimated at 19,6 million tonnes, up 5% year-on-year. Red meat prices, which have started to soften, should continue to moderate in the coming months, as we already see that continuous trend at the farm level. In essence, South Africa's consumer inflation food price outlook for the year's second half is reasonably better. The key drivers of the expected moderation will be meat, grain-related products, vegetable oils and fruits, which comprise roughly two-thirds of the consumer inflation food price basket. The base effects also support a view of a softening pace to levels around 7- 8% y/y in 2023 (from 9,5% in 2022).

- The anticipated moderation in headline CPI inflation from 2H23, however, does not appear to be factored in by trade unions with some insisting on wage increases of 15% despite very challenging operating environment and pressure on margins (especially in the food industry).

- The MPC, which meets again from 23 to May 25, remains data dependent. The outcome of March's CPI inflation print has likely strengthened the case for a 25bp rate hike. April's CPI will be available, and we expect a moderation to 6.8%. The FOMC meets on May 3 and the market is currently pricing in a 22bp rate hike and bias of 5bp for another rate hike in June. The FOMC will not provide an update of its SEP forecasts but will consider the latest CPI, jobs, inflation expectation and consumer spending data. A key dynamic is whether the Fed could signal a pause.

- SA's FRA market repriced the probability of rate hikes after the CPI print from 100% of a 25bp to 80% of a 50bp. ICIB expects a 25bp rate hike, which should be the peak as base effects should become more prominent at the July MPC meeting.

Fig 1 Headline and core CPI inflation

Source: StatsSA, ICIB

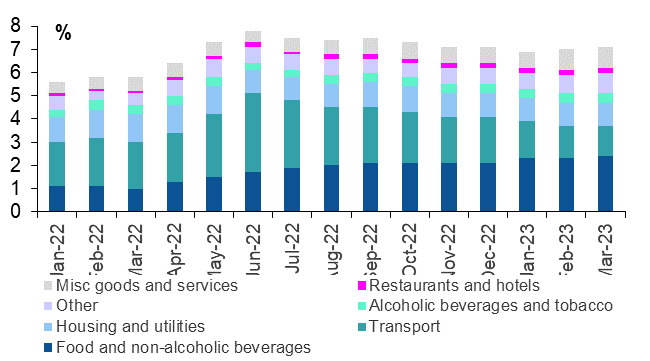

Fig 2 Contribution to headline CPI inflation: Food remains elevated with high monthy fuel price increases

Source: StatsSA, ICIB

Fig 3 Services – medical insurance and owners equivalent vs goods price inflation

Source: StatsSA, ICIB

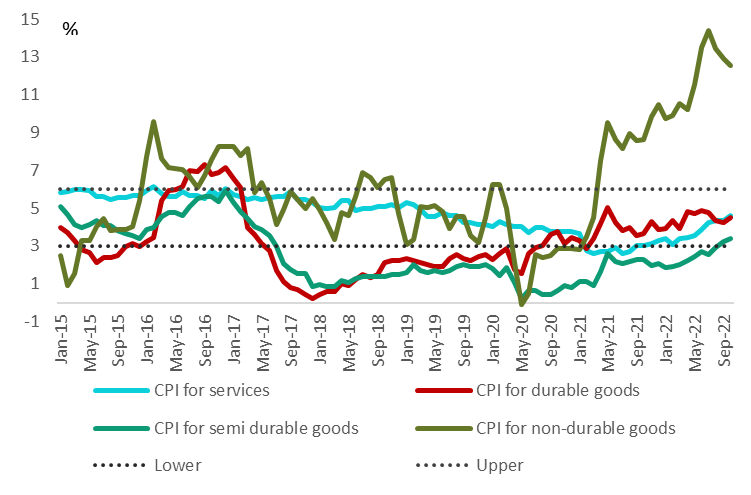

Fig 4 CPI for services, semi-durables, durable and goods

Source: StatsSA, ICIB