August's CPI inflation rate came in well below consensus market expectations and ICIB's forecast of 4.9% and 5.0%, respectively, at 4.7% from 5.4% in the previous month. This was the third consecutive month of downward surprises. Core CPI inflation also remained well contained, moderating to 4.7% from 5.0% (F: 4.9%). However, property taxes were not measured in many metros/municipalities because of new valuation roles, so August's inflation rate has an upside risk. July's CPI inflation rate, including property taxes, could have been ~4.9%.

The key drivers of inflation in July were utility rates, with annual increases at municipal level for electricity, water, property and sanitation rates. There was also volatility risk associated with food price inflation, although we have anticipated a moderation from elevated levels.

Reasons for the moderation:

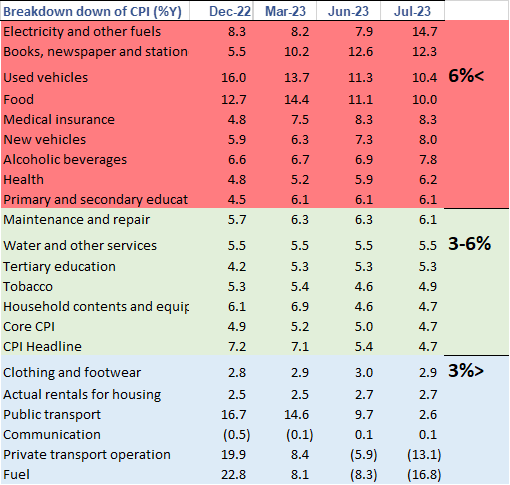

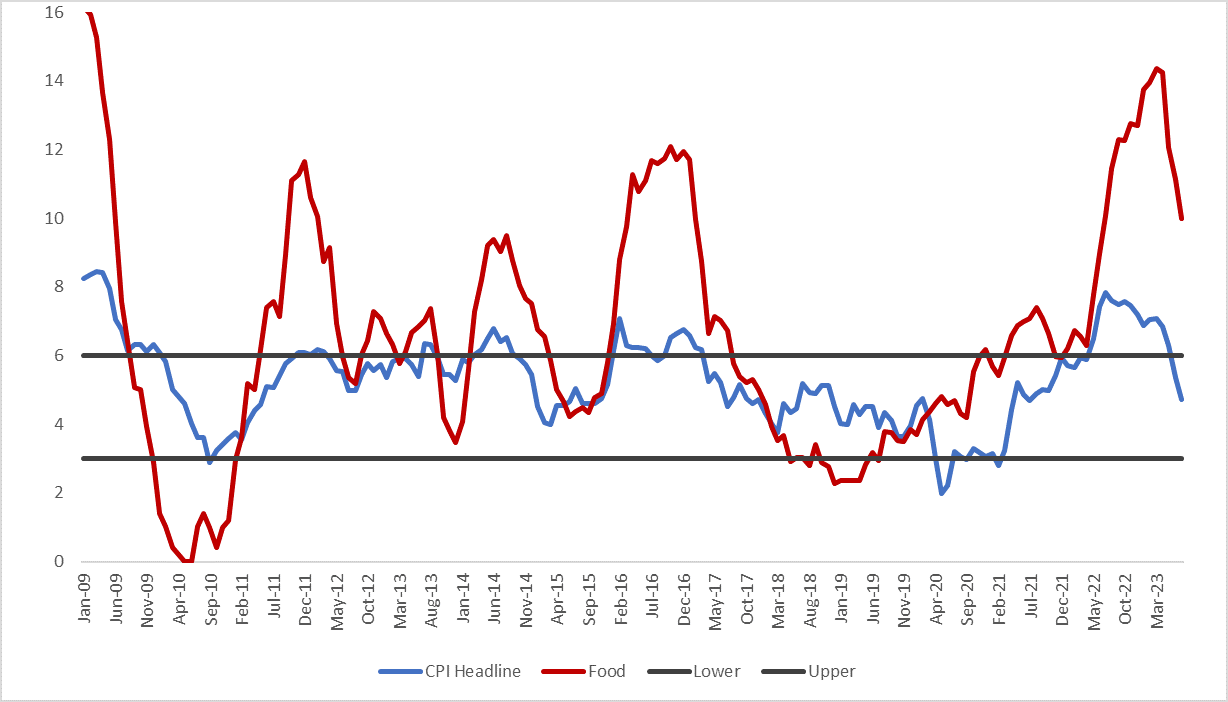

• Base effects were expected to lower the annual rate of increase in inflation. This was evident in a decline in food price inflation from 11% to 10.1% and below ICIBs forecast of 10.3% over the month; food prices increased by 0.2%, below the six month average of 0.9%. A decline in protein prices by 0.5%m/m was the main driver due to beef and processed meat specials.

• Utility rates increases:

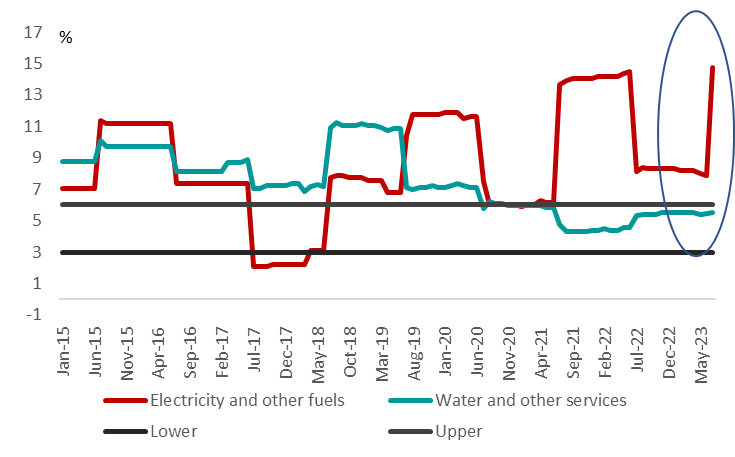

o The annual water and electricity tariff increase came in well below our forecasts. Water and other services tariffs were 4.7% higher over the month (F: 9.3%) and electricity tariffs 14.6%m/m (16%). The "other services" in the water sub-category include property tariffs, which will be measured in August. Electricity tariffs have been measured in the large measures, with a few small municipalities measured in August, which will not make much difference.

July's core CPI inflation data nonetheless shows a moderation in price increases in products linked to domestic demand, such as non-alcoholic beverages (6.5% vs. 8.8%y/y), package holidays (4.3% vs. 4.3%), and restaurants and hotels (5.2% from 5.6%), are moderating. But the rand's depreciation continues to be passed on in new vehicle prices (8.0% from 7.3%) and price increases of books, newspapers and stationery remains high at 12.3% (from 12.6% in June to 10.3% in May).

Inflation outlook: July's CPI inflation is expected to have been the trough until March 2024. We forecast August's CPI inflation rate to rise to 5.0% and September's can accelerate to ~5.5%, on account of a material increase in fuel/diesel prices before returning to 5.1% year-end.

Outlook for interest rates: Considering the exclusion of property taxes, the outcome of today's core CPI inflation rate strengthens the view that the rate hiking cycle has peaked. However, recent developments such as the increase in the oil price, the renewed depreciation of the rand, and the trajectory of inflation for the remainder of 2H23 will likely keep the messaging from the MPC hawkish, as cost-push pressures remain elevated. Thus, it would be premature for the front-end of the FRA curve to invert and pricing in rate cuts before 1Q24.

Fig 1: Headline and food price inflation

Fig 2 Utiltiy rates: Electricity and water, other services (which is likely to bounce to 9% in Aug)

Fig 3: Annual rate of change in prices of sub-categories

Note that water and other services will accelerate to ~9.0% in Aug