Not a unanimous hold

The MPC’s decided to keep the repo rate unchanged at 8.25% for the first time since November 2021, when the first of a total of 475bps rate hikes were delivered. The rate hiking cycle was characterised by meaningful upward revisions to the inflation forecast as many of the upside risks to the inflation forecast, transpired.

The context of July’s interest rate meeting was more constructive compared with May’s politically driven turbulence, which sparked a ~7% selloff in the ZAR (currently trading at R17.96/$). Global inflation has also moderated, although sticky core inflation led to various DM central banks hiking rates in June. The MPC’s decision, however, was not unanimous, with two of the five members in favour of a 25bps rate hike.

Implied rates have repriced ahead of the meeting

Market reaction was slight. Implied policy rates have repriced rate expectations since a more benign US June headline and core CPI prints (3.0% and 4.8% respectively) and South Africa’s June print of 5.4%. FRA rates assigned a 30% probability of a 25bps rate hike and the decision not to hike elicited a decline of ~5bps in the belly of the curve.

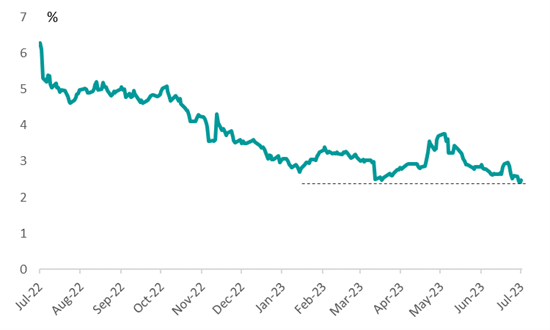

FRA rates out to January 2024 are trading 3bps above the 3m JIBAR rate of 8.50%, with a 25bps rate cut priced in for July 2024. ICIB concurs with the inversion and is of the view that a mild rate-cutting cycle could commence late in 1Q24. However, fiscal risks are expected to become more pronounced in coming months, with June’s exchequer account and revenue receipts published on 28 June, providing more insight into funding pressures. We expect the SAGB yield curve to steepen.

Hawkish pause

Our interpretation of the MPC statement and Q&A session was that the MPC kept its options open to resuming rate hikes, should the balance of risk assessment that remains “serious to the upside”, lead to a deviation of the projected inflation path.

Balancing act

The MPC’s decision was balanced between an improvement in inflation outcomes, the inflation projection and that policy is “restrictive, consistent with elevated inflation expectations and the inflation outlook” and “serious upside risks” to inflation. The risks include the following:

- Inflation expectations remained elevated in the BER’s 2Q23 inflation expectations survey (of importance is the extent to which inflation expectations will respond to the moderation in headline inflation in 3Q23’s survey)

- Persistence of tighter global financial conditions as G3 interest rates will remain high. This remains challenging in the context of attracting external financing to finance the current account deficit.

- Tight oil/demand-supply dynamics (2023 average oil price assumption of $81/bbl)

- Elevated food price inflation of 11% in June and a higher risk of El Nino that could lead to drier weather conditions in 2H23

- High cost of doing business due to load-shedding and logistics crisis and the acceleration in July’s municipal electricity tariffs.

- Uncertainty around the direction of food and fuel prices implies considerable risk attached to the forecast for average salaries.

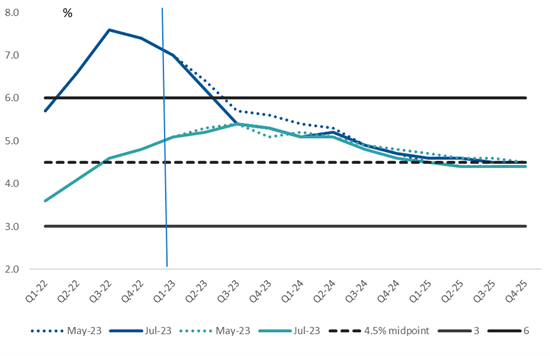

Inflation forecast: The headline CPI inflation forecast was revised to 6.0% (6.2%) and 5.0% (5.1%) in 2023 and 2024, and unchanged at 4.5% in 2025. Small changes were made to food and fuel price forecasts, with electricity unchanged at 11.6%, 13.4% and 10.9% over the forecast period. Food price inflation is expected to remain elevated but lower at 10.6% from 10.8% in 2023 but raised to 5.2% from 5.0% in 2024. The assumption for the fuel price larger at -3.1% in 2023 from 02.0%. The forecast for core CPI inflation has witnessed a slight improvement and revised to 5.2% (5.3%) and 4.9% (5.0%) in 2023 and 2024 (unchanged at 4.5% in 2025).

GDP forecast: The SARB made a small upward revision to its 2023 GDP forecast from 0.3% to 0.4% because of less load shedding in 2Q23. But left the growth forecast unchanged at 1.0% and 1.1% in 2024 and 2025. The output gap is closed at zero, showing no upward or downward pressures to inflation.

Figure 1 - Headline and CPI inflation forecast: May vs July

Source: SARB, ICIB

Figure 2 - R2032/3m JIBAR rate spread

Source: Bloomberg, ICIB