Key dynamics to monitor in the October MTBPS

- The MTBPS presented by the Minister of Finance on 28 October 2020 (after National Treasury requested a postponement from the 21st of October) will be preceded by President Ramaphosa’s Reconstruction and Revival growth plan presented to a joint sitting of parliament on Thursday, 15 October. These events will test the credibility of government’s commitment to fixing South Africa’s national finances against the backdrop of recent progress made in executing the anti-corruption strategy - also a critical growth enabler.

- The economic growth plan should provide a broad outline of the various facets of the growth strategy, with finer details left for the MTBPS to address. However, to establish credibility given skepticism about government’s competency and ability to execute, timelines would be expected.

- The ability to execute the economic plan to lift the growth trajectory is key for government to be able to embark on a fiscal consolidation plan, which requires confidence to lift private sector fixed investment and consumer spending.

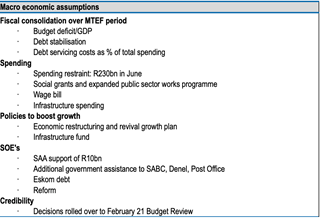

- The MTEF framework will be extended to F23/24. The key focus is on government’s commitment to push through what have always been politically challenging decisions. These include (1) plans for debt stabilization, (2) the expenditure framework, and (3) the public sector wage stance, and (4) SOE reform in the context of increasing efficiency of spending.

- The expenditure dynamics will be influenced by the debate around the pace of reducing government spending over the MTEF framework. In the current fiscal year, we expect an increase in spending as the President’s economic support package of R500bn announced in April 2020 had not been fully included in the June 2020 Supplementary budget. The MTEF framework demands a trade-off between (1) reducing spending required for debt stabilization and (2) continued strong growth in government consumption spending to support aggregate demand. We think there is more of a leaning towards the latter which implies a larger borrowing requirement over the MTEF period.

- On the spending side, zero-based budgeting has been implemented to reassess the MTEF spending framework. National Treasury’s forecast of fiscal metrics in June 2020 was premised on the active scenario which factored in R230bn of spending cuts in F21/22 and F22/23. ICIB’s baseline forecast is that government will not be able to adhere to the active scenario, which makes the credibility of the growth strategy and its efficient execution that much more critical. The Minister of Finance is expected to announce elements of fiscal consolidation but it appears likely to be softer than the active scenario assumption.

- The outlook for the budget deficit over the MTEF period feeds into the sovereign risk premium and government borrowing costs. The large government deficit is overwhelming the domestic savings industry and more contractual savings could be directed to funding the infrastructure programme. Foreign saving flows are therefore critical to supplement domestic savings.

- Announcements about tax increases are likely to feature only in the February 2021 Budget Review. June 2020 indications were that taxes will be raised to generate an additional R5.0bn, R10bn, R10bn and R15bn over the MTEF period. But this forms part of a broader tax debate in the context of South Africa’s direct taxes already being at the high end relative to the rest of the world.

Figure 1 | Checklist

Source: ICIB

Expectations F20/21: Larger budget deficit but bond supply unchanged

- Main budget deficit is forecast to increase from 14.5% of GDP to 15.3% and the consolidated budget deficit from 15.6% to 16.6% of GDP. Main reasons are a downward revision to GDP growth and additional spending.

- Spending could be raised by R20bn to R40bn allocated to SOE’s and social grant/expanded public works programme.

- Revenue receipts are expected to be left unchanged.

- Main budget deficit raised from R710bn to R740bn.

- Bond supply is expected to remain unchanged.

- Bond outlook: We leave our 10yr SAGB yield forecast at 9.30% for end-2020 and expect the long-end of the curve to remain range bound.

Risk to the yield forecast: To the downside in the event of earlier expenditure constraint.