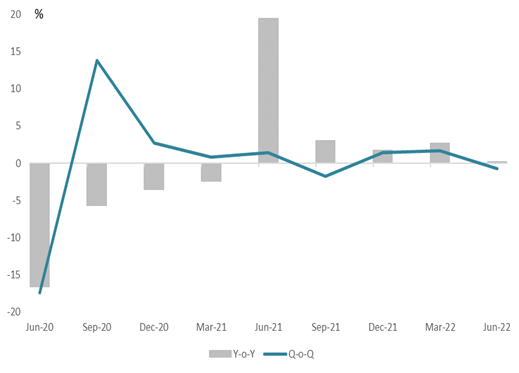

2Q 22 q-o-q: -0.7% vs ICIB F-0.9% and Bloomberg consensus -0.8%

2Q 22 y-o-y: +0.2%

1Q 22 Revision: 1.7%q-o-q (P1.9%); 2.7%y-o-y (P3.0%)

H1 22 y-o-y: 1.4%

2021: +4.9%

2022 F: 1.9%

Key takeaways

- GDP outcome for 2Q 22: South Africa's GDP contracted by 0.7% q-o-q (seasonally adjusted but not annualised) from a revised 1.7% q-o-q (1.9%) in the previous quarter. The outcome was in line with market expectations and slightly better than ICIBs forecast of 1.0%. The economy was 1.7% below the pre-pandemic level in 4Q 19.

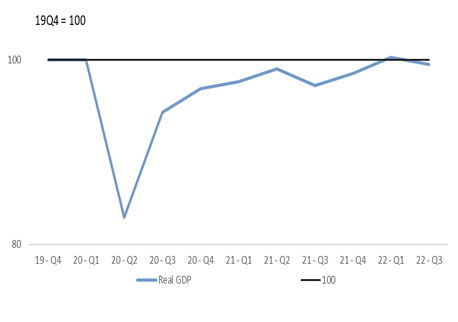

- The level of the economy was 0.5% below pre-Covid 19 levels in 4Q 19. However, the SARB views the negative output gap as relatively small in the context of potential GDP growth below 1%, owing to the electricity constraint.

- The contraction in economic activity was caused by (1) slower global GDP growth, i.e., China's GDP contracted by 2.6%q-o-q owing to a protracted Covid-19 lockdown in Shanghai, and (2) SA specific factors such as the April KZN floods which damaged infrastructure (and exports) and intensification in load shedding (by June 2022, load shedding has reached 91% of 2021 intensity).

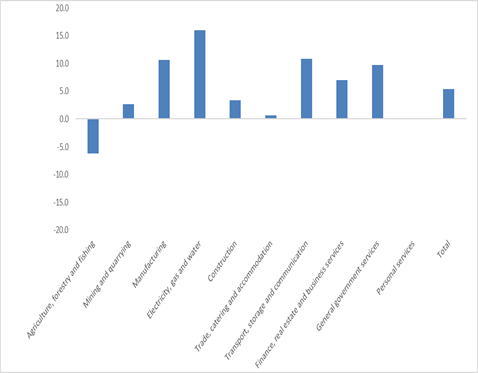

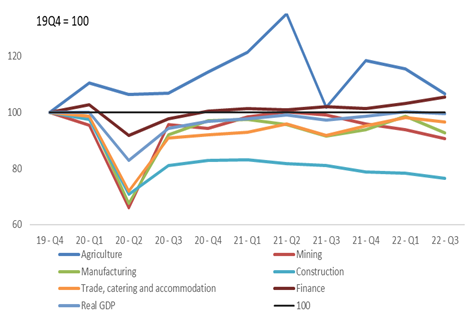

- Production side impacted by lower agricultural, mining and manufacturing production: As expected, output in the primary and secondary sectors was very weak, contracting by 5.1% and 4.8%q-o-q, respectively. The services sector remained relatively firm, supported by lifting Covid-19 restrictions. However, wholesale and retail trade contracted (-1.5%q-o-q), although there was a strong rebound in inventory held by the retail sector. A decline in government spending of 1.4%q-o-q was ascribed to a reduction in employment numbers (although the LFS survey showed an increase in community employment linked to the government's job creation programme). The finance industry continued to record positive growth (+2.4%q-o-q), driven mainly by financial intermediation, insurance, and pension funding and activities (reflected in credit extension). The transport sector (mostly road) because of the operational challenges facing Transnet rail network (+2.4%q-o-q).

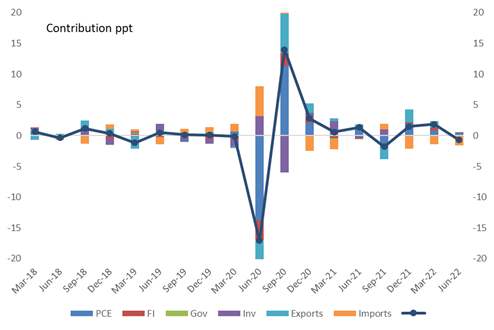

- On the expenditure side, there has been a moderation in the key drivers of GDP growth post the Covid-19 lockdown, namely household spending, and exports. Household spending increased by 0.6% q-o-q in Q2, compared to 1.2% and 3.0% in the previous two quarters, with services recording positive growth. The growth rate in exports slowed to 0.3%q-o-q (previously 3.8 and 8.3%), on account of global factors, compounded by rain damage to infrastructure transporting goods to Durban harbor. Where we expected a significant drawdown in mining and manufacturing levels, restocking took place in the sector. This probably bolstered an increase in import volumes (rising by 5.6%q-o-q from 5.1% previously) and the transport sector.

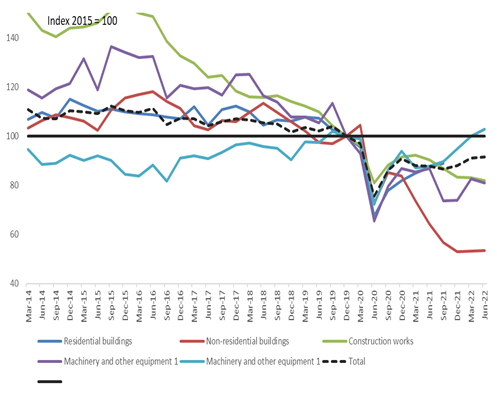

- Fixed investment increased for the third consecutive quarter, growing by 0.5%q-o-q (previously 3.4%). Fixed investment by private businesses continued to increase (+0.8%q-o-q from 3.9%), whereas investment by public corporations and general government contracted. The breakdown of fixed investment showed that construction activity has contracted for the fifth consecutive quarter, which is a function of the government dynamics. The Minister of Finance stated that the MTBPS is looking to allocate more funds to infrastructure spending, which probably includes transfers to Transnet. Whereas we expected more activity in residential buildings, the industry contracted for the second consecutive month (-4.7%q-o-q from -1.8% previously). Machinery recorded positive growth (+2.9%q-o-q from 5.4%), ascribed to an increase in maintenance capital.

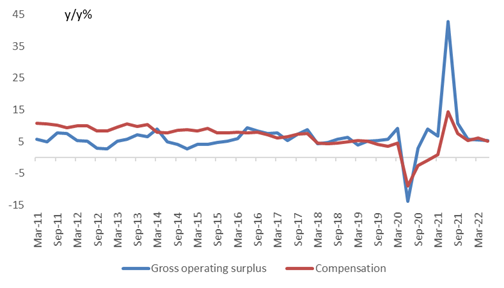

- The gross operating surplus (a proxy for the industry's profitability) has moderated, rising from 6.2% to 5.6%. However, base effects played a meaningful role (i.e., increasing by 42.9% in Q2 21 as activity started to normalize after 2020 severe lockdown restrictions and mining companies' revenues were bolstered by a surge in commodity prices). Compensation increased by 5.1%y-o-y from 5.2%, indicating a deterioration in real disposable income.

What we are watching: On 7/9 and 8/9, the BER publishes its Q3 business and consumer confidence surveys. After deteriorating in Q2 22, we expect consumer confidence to remain low because of high inflation (steep petrol price increase and rising interest rates). The outcome of business confidence will be interesting, as the survey was conducted after President Rampahosa announced meaningful reforms to the energy sector. We will also assess how strong the rebound in economic activity is after the Q2 contraction, i.e., manufacturing production in 8/9 for July.

Figure 1 Real GDP (q-o-q and y-o-y % change)

Source: StatsSA

Figure 2 Real GDP in 4Q 21 was 1.7% below pre-Covid Q4 2019 levels, but the negative output gap is small on account of very low potential GDP

Source: StatsSA, ICIB

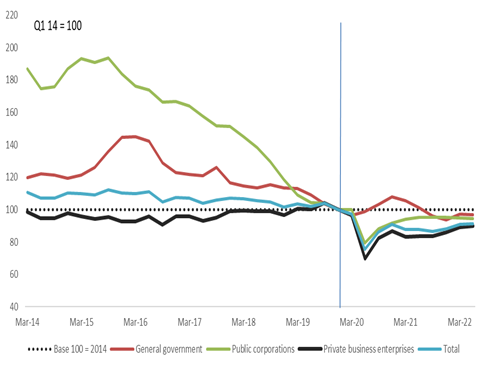

Figure 3 GDP production – Finance and agriculture the only two sectors which have returned to levels above pre-Covid

Figure 4 Expenditure contributors to growth in 2021: Household spending and exports

Figure 5 Private sector fixed investment is recovering from a very low base

Source: StatsSA, ICIB

Figure 6 Breakdown of fixed investment – machinery recovering

Source: StatsSA, ICIB

Figure 7 Compensation and gross operating surplus (GOS)

Source: StatsSA, ICIB

Figure 8 Industry breakdown of GOS