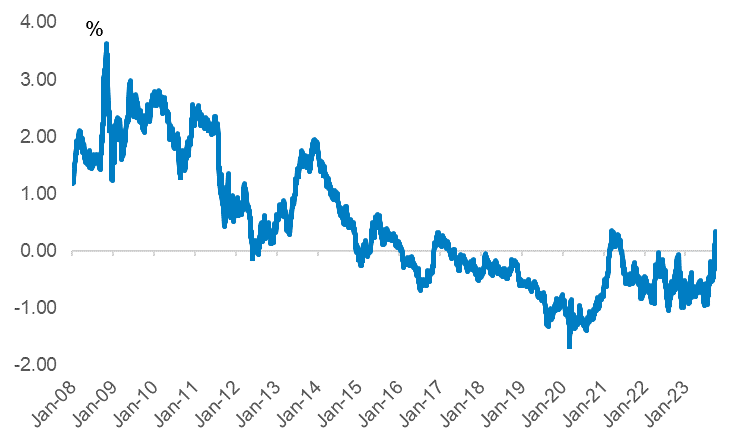

The selloff in US Treasury yields in September extended into October (Fig 1), leading to a further depreciation of the USD index of 2.6%. The note provides a high level overview of the drivers, as the rise in longer-dated US Treasury yields also contains a non-economic component, leading to an increase in the term premium required by investors to hold longer-dated maturities. EMFX and sovereign bond yields have risen, and short rates have repriced.

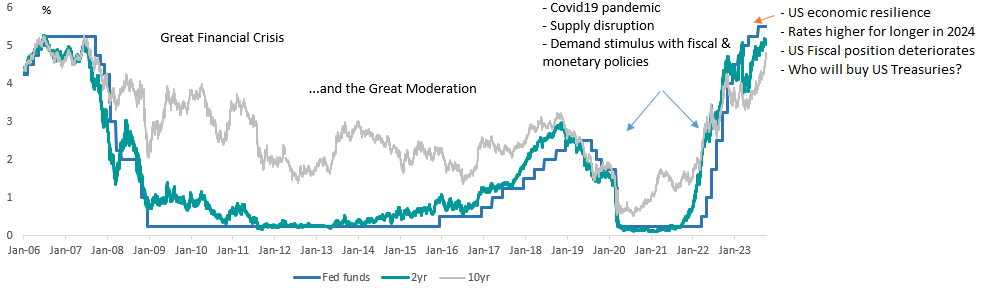

Fig 1 US Treasury yields have returned to 2007 levels

Source: Investec CIB

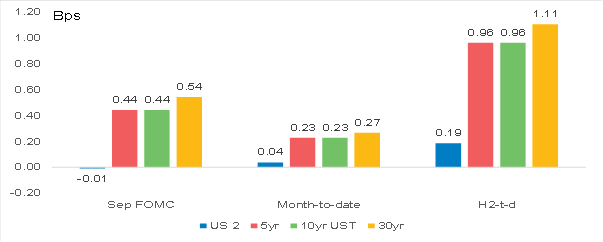

Fig 2 Rise in US Treasury yields from pre-September FOMC, month-to-date and H2-t-d

- The rise in shorter-dated US Treasury note yields, such as the 2y yield, has been more muted, rising by 19bps to 5.08% from mid-2023. The selloff has mainly been in the mid-long and long-end of the curve, where the 10y yield has increased by 23bps in October (and a total of 96bps since mid-2023) to 4.81%. The slope of the 2vs10yr curve has become less inverted, with the spread narrowing from 108bps to 28bps.

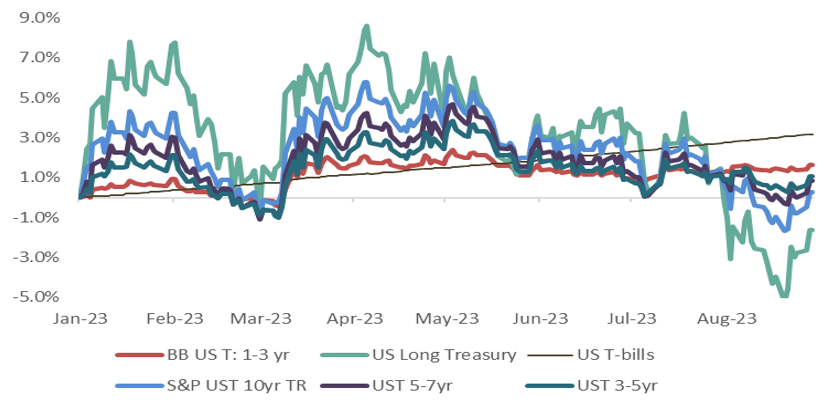

Fig 3 Selloff in yields has resulted in total returns on 10 to 30-year segments of the curve to be flat to negative

Source: Investec CIB

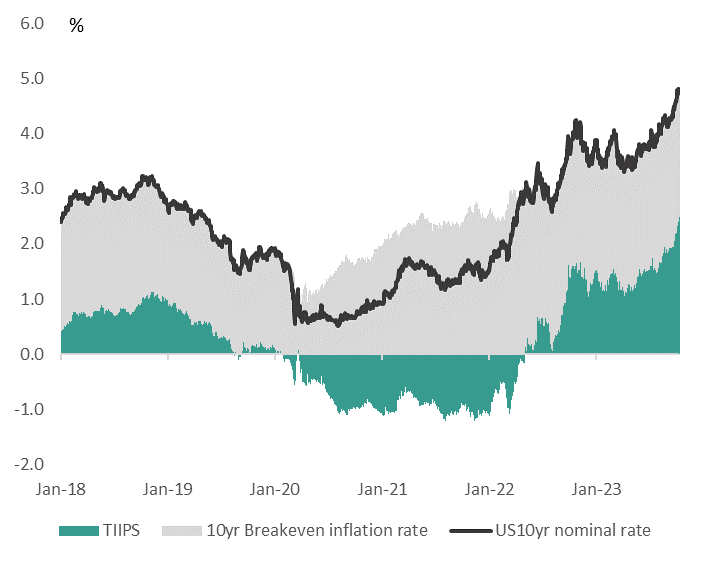

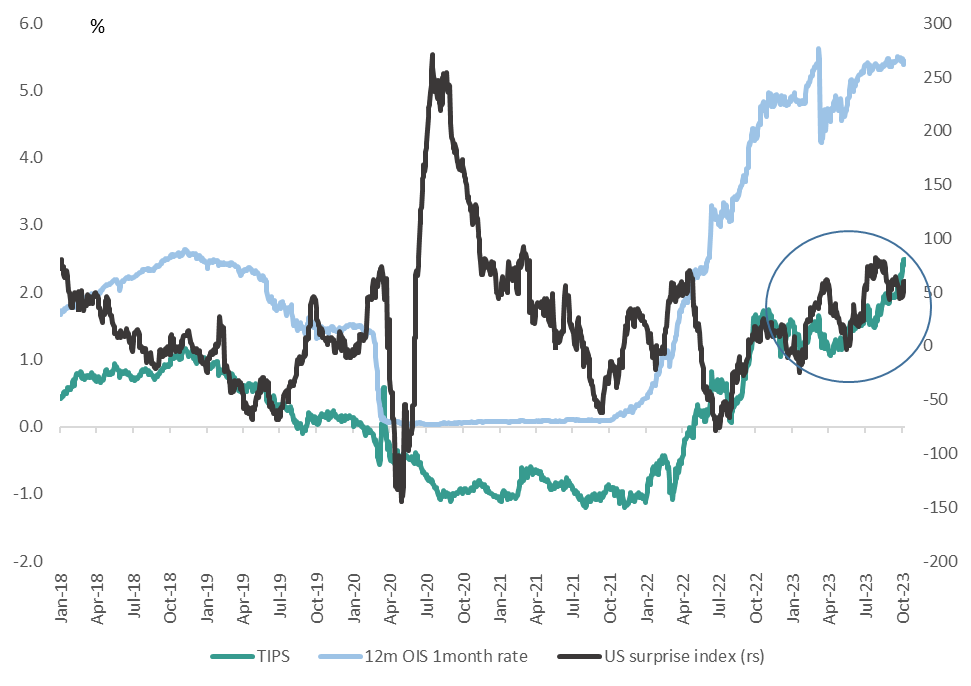

Fig 4 Composition of 10yr US yield: Rise in the real TIPS yields behind the rise in nominal yields

- The rise in the 10y yield can be attributed to an increase in the real component of the nominal yield, which is determined by growth and economic surprises. The stronger than expected outcome of Friday's nonfarm payroll report saw the 10y yield rise to 4.9% before settling at 4.81%. The Atlanta Fed GDPNow model estimated real GDP in Q3 23 (q/q and saar) at 4.9% from 2.1% in 2Q, well above trend growth at ~2.0%. However, growth is expected to moderate in 4Q as student loan repayments have restarted in October.

Fig 5 Term premium has risen as investors require a higher spread to hold a 10yr US Treasury note

- The increase in the term premium can be attributed to non-economic factors, which we discuss below.

Drivers of the repricing of longer dated US Treasury yields

- Resilience in the US economy is making the "last mile" in returning inflation to the target of 2% more difficult.

- Deterioration in fiscal health leads to an increase in US Treasury supply. At the same time, demand is impacted by the Fed's QT, higher non-US core sovereign yields, and US bank demand is affected by unrealised losses.

Fig 6 US economy remains more resilient – raising the real rate in US10y

- The reacceleration in US GDP growth in 3Q, which has resulted in an upward movement in the surprise index (black line), has led to an increase in the real yield (green line). Added to this has been a revision of the Fed's 2024 dot plot, which shows that monetary policy could remain more restrictive for longer, as the median rate forecast expects the Fed funds target to be cut by only 50bps from a previously expected 100bps rate cut. The implied OIS spread, however, expects a 100bp rate cut.

- The resilience of the US economy, notwithstanding a total of 525bps rate hikes, has sparked a debate about how restrictive US monetary policy is. The neutral Fed Funds target rate, or r*, is seen to be at 2.5% (Fig 6.2). This is an important dynamic as the direction influences the yield curve's slope. A catalyst for the repricing of longer dated US Treasury yields was in July and September when the FOMC held the Fed funds target rate at 5.50% but interpreted it as a "hawkish pause".

- Why is the US economy so resilient in the face of 525bps rate hikes? Larry Summers flagged two issues:

- Firstly, households have fixed mortgage rates and have not been impacted by the rise in mortgage rates to nearly 8%. US house price growth has moderated to 3.1%y/y from almost 20% in 2022 due to a shortage in house supply. Rising house prices have supported the wealth effect and consumer spending. For new home buyers, housing affordability has declined to levels below the index's inception in 1989.

- Fiscal policy has remained stimulative, with fiscal transfers followed by the Inflation Reduction Act. The latter is a misnomer as it is essentially legislation to invest in energy security and climate change, with a price tag of $783bn.

What are we watching

- Incoming data for 4Q. A moderation in GDP growth could lead to some moderation in the real yield component of the 10y yield, indicating that the 10yr yield at 4.75% could be "toppish."

- US financial conditions have tightened on account of the higher US Treasury yields. However, the yield adjustment has been abrupt as opposed to more gradual. A Fed rate hike in November is therefore not conclusive.

- A renewed increase in geopolitical risk. The involvement of Iran in Hamas's attack on Israel and possible sanctions by the US, has raised the oil price from $83/bbl to ~$88b/ll. Supply dynamics will be the key driver in coming months.