The two important US data releases feeding into the FOMC meeting, scheduled for September 21, are jobs and inflation data. This week the market repriced its terminal rate hike expectations to 4% in 2023, following Fed Chair Powell's hawkish Jackson Hole speech last Friday. The focus on today's August jobs data was therefore, if the September FOMC meeting could see a 50bp or 75bp rate hike, feeding into the unfolding debate about a hard or soft landing of the economy in 2023.

The July labour market report was more or less in line with consensus expectations. The key focus, however, was on an improvement in the labour force participation rate. A poor improvement post-Covid has been a contributory factor to the supply of jobs exceeding demand, in turn leading to upward pressure on wage increases. The increase in average hourly earnings remained high, rising by 5.2%, but has been flat over four consecutive months after accelerating by 5.5% in January 2022

Key takeaways

- The economy created 315 000 jobs in August. The outcome was slightly ahead of consensus forecasts of 298 000 but a moderation from a robust 526 000 increase in July. 528 000. Historical data revisions show a reduction of 107 000 over the previous two months.

- The average number of jobs created per month over the past 14 months remains elevated at 507 000 per month. This has raised the total amount of nonfarm jobs back to 152.7m, which is ahead of 512m, which ahead of pre-Covid level highs of 152.5m.

- The unemployment rate increased from 3.5% to 3.7% and 5.3% from 3.6%, aided by the increase in the labour force participation rate (from 62.4% to 62.1%). This suggests more people are returning to the labour market, which could help to contain wage increases. The number of vacancies continues to exceed the labour supply, i.e., for every unemployed person, there are 1.87 jobs available, although this has moderated from 2 times in April 2022.

- Another key focus point is whether wage pressures are subsiding. The average hourly earnings have remained flat at 5.2% since April.

Market reaction

The market reacted positively to the outcome in the context of risk-off sentiment fanned by Powell's Jackson Hole speech. Before the labour market report, the S&P tumbled by 3.3% (currently +0.3%), 2yr US Treasury yields rose to 3.50% from 3.39%, the highest since 2007 (now at 3.44%) and 10yr US Treasury yields from 3.04% to 3.25% (below a June high of 3.47% and currently at 3.23%). The DXY reached its highest level this week since 2002 before yielding 0.3% after the report. Risk-off sentiment has hit EM FX very hard this week, with the ZAR depreciating from R16.88/$ to a low of R17.30/$ today (currently R17.19/$).

Following the labour market report, a 75bps rate hike at the September FOMC meeting remains live. The next crucial data point is August's CPI print, scheduled for 13/9. Headline CPI inflation is expected to continue its descent from 8.5%, on a further retreat in gasoline prices and possibly airfares and secondhand car prices. However, the direction of core CPI inflation, at 5.9%, will be closely monitored. The key dynamic is that the battle against inflation is likely to continue as the Fed has stressed its commitment to return inflation to its 2% target. The market is pricing in a probability of 85% that the Fed funds rate could be raised by 75bp on 21/9. These dynamics are important for the MPC, which announces South Africa's rate increase on 22/9. MPC members are keeping a close eye on SA interest rate differentials with G3 countries, as EM FX has come under increasing pressure as the Fed turned more hawkish. The FRA curve is pricing in a 75bp and 50bp rate hike at the September and November MPC meetings, which I think is too high (base case: a total of 75bps, worse case, 100bps).

What we are watching next week:

Global

5/9 EZ PMI Services , China Caixin PMI services

Announcement of new UK PM

6/9 US ISM, Australia RBA interest rate decision +50bp

8.9 ECB interest rate decision: the market is expecting 75bps

7/9 Fed Beige Book (reading of general economic activity)

China's exports and imports:

9/9 China PPI and CPI

South Africa:

7/9 Q2 22 GDP (F: Bloomberg consensus: -0.5%q/q, ICIB -0.9%)

BER business confidence 3Q: Could more positive news flow related to the energy plan start to lift confidence?

8/9 Q2 Current account balance (1.2% of GDP from 2.2%)

Manufacturing production (July)

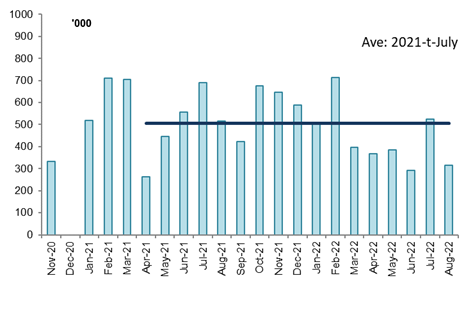

Figure 1 US created a surprise 315 000 jobs in August vs. 14m monthly ave of 506 000

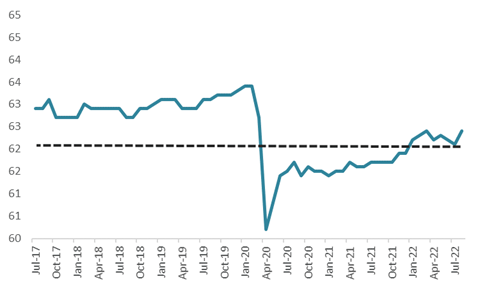

Figure 2 Labour force participation rate has ticked higher

Figure 3 Wage increases flat at 5.2%

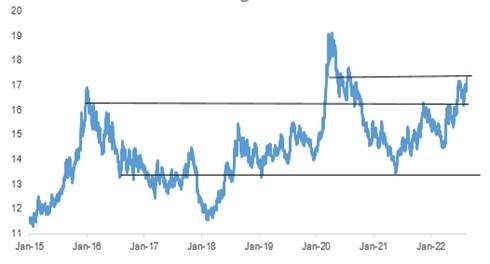

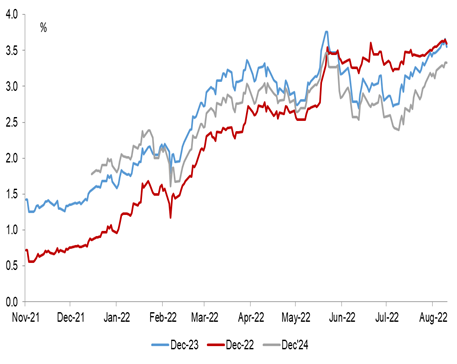

Figure 4 Repricing 2023 Fed rate expectations (blue line)

Figure 5 S&P (robust earnings growth vs concern of 2023 earnings recession),

Brent spot has declined, leading to a decline in headline CPI inflation