Strengthening our Industrial Tech & Services team

Investec is pleased to welcome Matthias Odrobina as Managing Director of our European Business Advisory and a senior member of the global sector team covering Europe, UK, Africa, the US and Asia with impartial advice on cross-border transactions.

Matthias brings deep sector expertise across industrial technology (particular focus on smart industries, B2B software and digital transformation).

He has 20 years of experience as a trusted partner to boards and owners on mergers, acquisitions, divestitures, financings, and buyouts, with a particular focus on the industrial sector, B2B software, and business services.

Contact: Matthias Odrobina

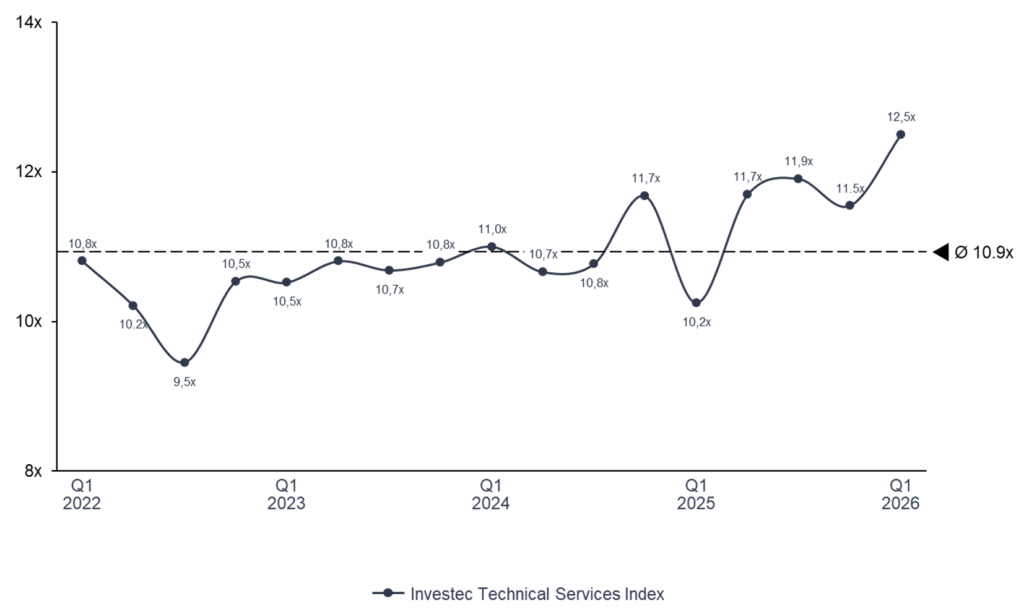

Sector multiples have reset above the long-term median – but the index average masks the real story.

The Technical Services Index is trading at 12.5x EV/EBITDA in Q1 2026, +1.6x above the long-term average of 10.9x and +2.3x above Q1 2025.

Investors are no longer pricing technical services as a single cyclical block. After three years of selective re-rating, the market has unbundled the index into four distinctly priced narratives – power, project execution, recurring service quality, and engineering scarcity – andthe spread between them is at its widest of the cycle.

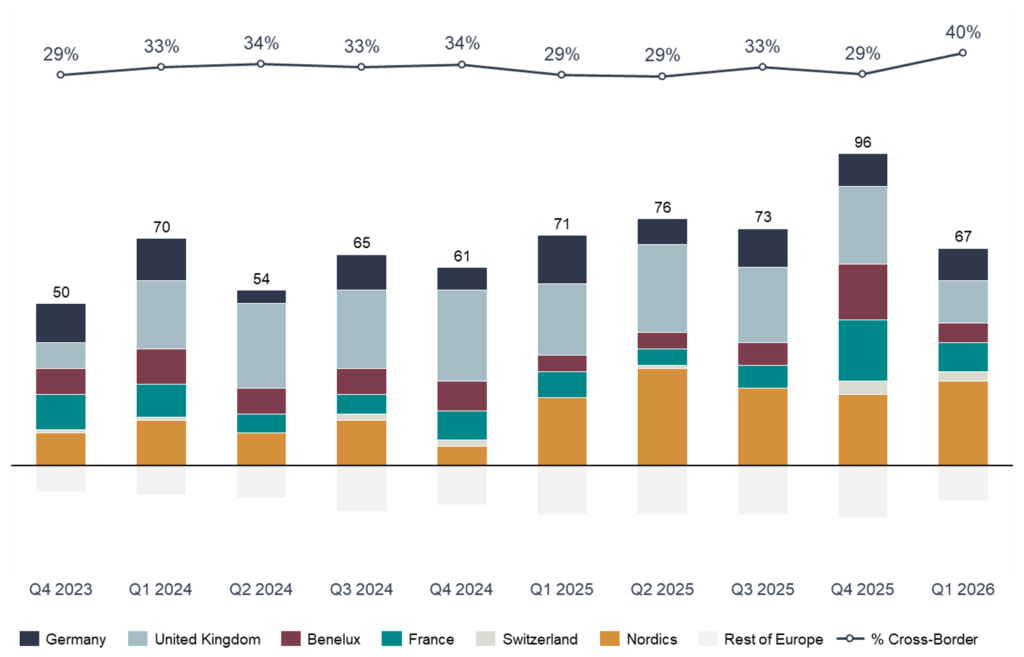

Resilient deal volumes (67 European transactions in Q1) and a step-up in cross-border participation (40%, vs. low-30s through 2025) confirm that buyer appetite remains intact, but selectivity has sharpened materially.

What’s behind the re-rating

The index has rebuilt steadily since the Q4 2022 reset, but the path has not been linear. Multiples held in a narrow band through 2023–24 as investors worked through the rate-shock repricing, then accelerated through 2025 as backlog visibility, energy-transition capex and the AI infrastructure build-out translated into earnings upgrades – not just multiple expansion. The current premium to long-term mean is being underwritten by delivered earnings, not narrative. That distinction matters for what comes next.

The market is rewarding service models that combine recurring revenues, mission-critical exposure and demonstrable margin expansion – and applying a clear discount everywhere else.

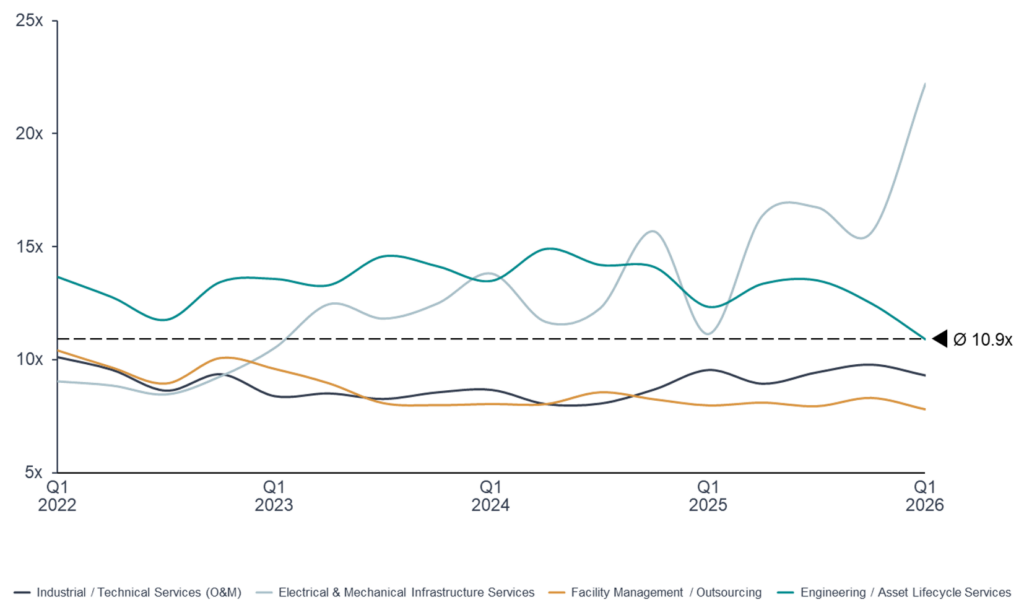

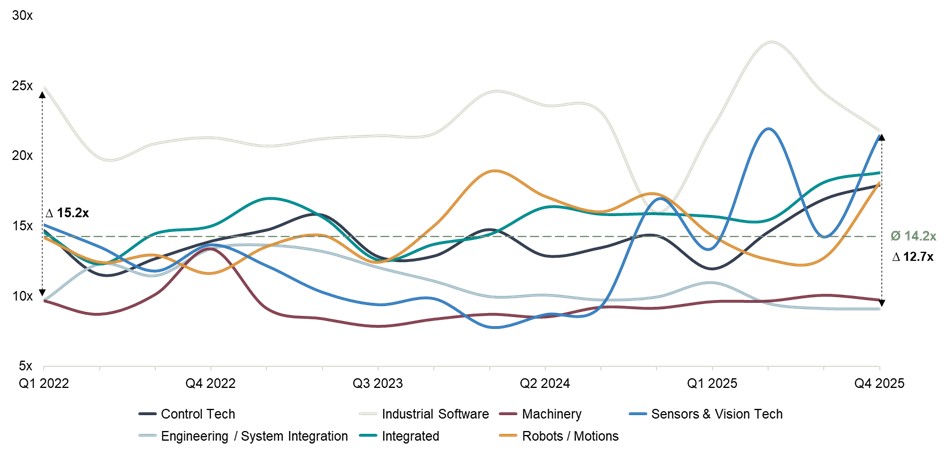

EV/EBITDA: Segment comparison Q1 2022 – Q1 2026

The segment trades broadly in line with the index, supported by a clear and increasingly consistent strategic playbook across the leading platforms.

- Margin ambition has reset structurally upwards across the multi-technical platforms – medium-term EBITA targets now cluster in the 8–9% range, a step-up from the 6–7% delivered through the prior cycle, and forward 2027E multiples already compress to ~8.6x as the market underwrites delivery

- Portfolio repositioning toward energy transition, data centre and pharma end-markets is a segment-wide strategic priority, replacing legacy oil & gas and general industrial exposure

- Bolt-on M&A remains the primary growth engine – leading platforms are deploying capital at a pace materially above prior cycles, supplied by a still-fragmented European mid-market

- Pricing power has shifted to providers as labour scarcity in skilled trades has changed the negotiating dynamic on outsourced industrial maintenance contracts

- Mission-critical backlog mix is rising – multi-technical service contracts are increasingly anchored in regulated, safety-critical infrastructure, lifting the recurring component of revenue

Investors are paying for delivery on stated margin paths and continued M&A optionality. Tolerance for execution slippage is limited.

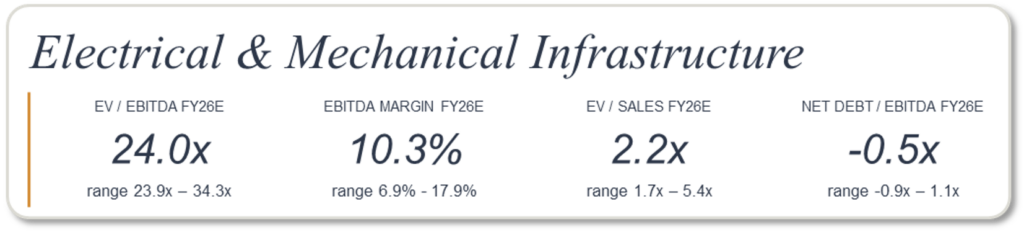

The standout segment of the cycle, with a valuation premium of ~16 turns versus Facility Management – pricing structural exposure to the most concentrated capex super-cycle in industrial services.

- Combined backlogs across the cohort have grown +34% year-on-year, with hyperscaler-driven data centre work the fastest-growing pocket and electric grid build-out providing a multi-year secondary leg

- Customer mix has pivoted decisively toward technology buyers across the cohort – hyperscaler and data-centre work is now a meaningful share of new awards across the cohort, with the most exposed names having moved from a structurally limited share of revenue to majority technology exposure inside two years

- Capacity expansion is the segment’s strategic priority – both physical capacity and contracted labour pools through master service agreements are being scaled materially across the cohort to convert record backlogs

- Selective M&A in specialty electrical and mechanical adjacencies is reinforcing premium positioning rather than diluting margin

- Margins are at or near cycle peaks and balance sheets are increasingly net cash, providing optionality without near-term re-leveraging risk

The risk is asymmetric: 24.0x embeds a multi-year continuation of current capex trajectories. Historical analogues from prior pauses suggest 30–50% multiple compression within weeks of any confirmed inflection. Investors are paying for backlog duration, not cycle-stage normalisation.

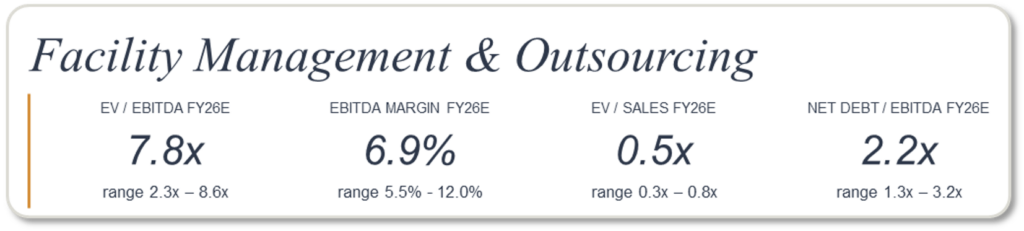

The structural laggard of the index – but the discount is becoming differentiated, and that bifurcation is the more important development.

- The segment-level discount reflects genuine fundamentals – lowest aggregate growth (4.8% in 2025/26), thinnest margins (6.9%) and highest leverage (2.2x net debt/EBITDA)

- Mix shift away from manned services toward technology-enabled and compliance offerings is the defining strategic playbook for the leaders

- Balance-sheet discipline through systematic capital return – sustained buyback programmes and progressive dividends – is increasingly part of the equity story

- Selective M&A in higher-margin adjacencies is repricing the leaders – security technology, integrated workplace technology, compliance and TIC services have transacted at multiples well into the teens

- Evidence of strategic delivery is accumulating at the leading end of the segment – long-stated medium-term margin targets are being hit, technology mix is now meaningfully contributing to profit pools, and contract pipelines have expanded materially through the most recent reporting cycle

- The laggards have validated the discount – material guidance downgrades among segment incumbents, including organic growth resets to near-flat and margin reductions of more than 100 basis points within a single fiscal year, reinforce the case for selectivity

Buyers are paying up for technology mix and recurring contract quality. Pure manned-services exposure remains comprehensively discounted.

The most strategically coherent segment in the index, and the one where M&A is most actively reshaping the peer set.

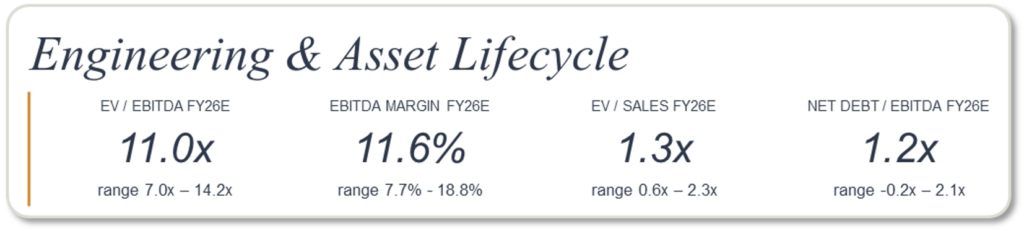

- Three converging structural advantages underpin the premium – highest aggregate margins in the index (11.6% segment median FY26 EBITDA, with the upper quartile delivering 17–18%), multi-year backlog visibility through long-cycle programmes, and direct exposure to scarce specialist verticals

- Scarce-vertical exposure is the primary valuation driver – nuclear new-build and refurbishment, water infrastructure, grid and energy transition, and defence

- Strategic acquirers are paying materially for energy positioning – recent transactions in energy-transition consulting have priced at 14–15x pre-synergy EBITDA, well above the wider segment average

- A margin-convergence story is playing out across the leading end of the segment – platforms with publicly stated medium-term Adjusted EBITDA targets in the 17–20% range are now at or within 100 bps of those targets

- Capital allocation is broadening from M&A-only toward buybacks as platforms approach their margin targets, signalling cycle maturity at the leading end

Premium pricing of scarce specialist capability and disciplined margin convergence at the leaders will drive most of the stock selection within Engineering through 2026.

M&A activity – selectivity, scale, and the rise of cross-border

Q1 2026 confirmed two of our central theses on the European deal market. First, transaction volumes have remained resilient at 67 deals – broadly in line with the four-quarter average – despite higher financing costs, indicating that strategic and sponsor capital deployment is now structurally embedded rather than cycle-dependent. Second, and more importantly, cross-border participation rose to 40%, materially above the c.33% trailing pattern of the past two years.

The cross-border step-up reflects two reinforcing dynamics. Strategic acquirers – particularly those repositioning toward power, energy transition and nuclear – are reaching across borders to acquire specialist capability that cannot be built organically at the required pace. Sponsors, in parallel, are increasingly comfortable underwriting multi-jurisdictional roll-up theses where local-champion platforms can be combined into pan-European leaders. Recent benchmark transactions in the period – including a $3.3bn engineering acquisition disclosed at 14.5x pre-synergy EBITDA and a c.€4bn sponsor recapitalisation in European facility management at an estimated 12–13x – confirm both the depth of capital available and the multiples that scale platform assets continue to command.

For owners, this matters concretely: competitive tension in well-run sale processes is increasing, and the buyer universe for premium assets is materially larger today than in any year since 2021.

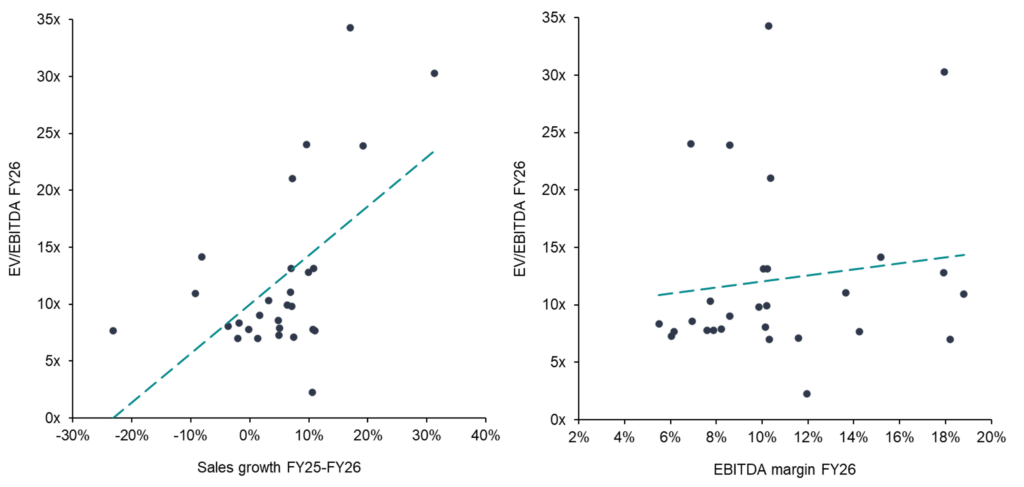

Investors reward profitable growth

The two charts make the underwriting model of today’s market explicit. Forward sales growth tracks tightly with FY26 trading multiples – each percentage point of expected growth corresponds to roughly half a turn of EV/EBITDA – while FY26 EBITDA margin shows no meaningful relationship at all. Read together, the pattern confirms what the segment commentary has set out: the market is paying for visible, contracted growth, with margin acting as the qualifier that separates underwritten growth from narrative growth, not as a primary driver in its own right.

What this means for owners and investors

For entrepreneurs, the message is sharper than at any point in the past three cycles. Premium valuation outcomes are increasingly driven by recurring revenues, demonstrable margin resilience, and the ability to articulate strategic relevance within a defined value chain – not by aggregate growth. Top-line CAGR alone no longer commands a premium. Buyers are dissecting revenue mix, contract duration, and end-market exposure with substantially more discipline than they applied during the 2021 peak.

For investors and strategics, selectivity is paramount. Scaled platforms with clear consolidation theses, recurring service exposure, and defensible end-market positions continue to attract the deepest pools of capital and the highest exit multiples. Generic exposure – to construction cyclicality, to manned-only services, to government-revenue concentration, to mid-cycle margin levels – is being systematically discounted.

In today’s market, valuation premiums are not driven by growth in isolation. They are driven by visibility, resilience and strategic scarcity – and the index dispersion at the close of Q1 2026 is the clearest evidence yet that buyers are pricing accordingly.

The Investec Technical Service Index tracks daily developments across the technical services landscape, covering sectors such as Maintenance & Repair, Installation & Commissioning, Engineering Services, Asset Management and Field Services. The index includes valuations, growth projections, profitability margins and other key metrics. You can find more information on our website and specific industry insights in our latest Industrial Services Report.

Investec has a senior team in Technical Services, who are experienced experts in selling, buying, and financing businesses. If you have questions and would like to know more about valuations, buyer activity and current opportunities in the market – please get in touch: [email protected], [email protected], [email protected]

Michel Degryck, Managing Partner, has been recognised by MergerLinks by Datasite among the Top Investment Bankers in France!

A well-deserved recognition of his leadership and long-standing commitment to clients.

Behind every successful transaction lies trust, judgement and long-term relationships.

Explore the rankings: Top Investment Bankers in France FY 2025

The European building automation industry is undergoing a period of structural transformation. A traditionally fragmented, owner-managed market is increasingly giving way to a capital-backed platform ecosystem. M&A is no longer merely opportunistic but has become a core strategic tool for vertical integration, scaling expertise, international expansion, and value creation. Leading providers such as Siemens, Johnson Controls, Schneider Electric, and Trane Technologies dominate the market with integrated solutions and digital service portfolios. Mid-sized companies and platform providers such as VDK Groep, Elevion, and Konzmann complement the market with regional strength and specialized technical expertise. Drivers in a market expected to nearly double by 2034 include energy efficiency, regulation, digitalization, AI, and smart building technologies. Private equity is a powerful catalyst for market transformation, driven by buy-and-build strategies, software margin potential, and demand secured by regulation. M&A activity remains high due to fragmentation, technology needs, and international expansion goals.

For owners of private companies, this gives rise to clear strategic priorities: digitalization and cloud/AI technologies should be consistently expanded, service- and lifecycle-oriented business models strengthened, positioning sharpened, and organizational structures made scalable. Sustainability is also emerging as a key competitive and valuation factor.

Digitalization shifts value creation and creates new revenue models

The building automation industry is undergoing a profound transformation that is increasingly shaped by software, data, and services. Even though traditional hardware still plays a role, growth is clearly shifting toward digital solutions. Energy management software, cloud-based BMS, subscription models, and AI-powered optimization systems, in particular, are experiencing high growth rates. Wireless retrofits and cloud-based analytics are also gaining importance and ensuring that recurring revenue accounts for an ever-larger share of total revenue.

At the same time, digitalization significantly improves earnings quality. Digital and data-driven services generate substantially higher margins than the installation business. Providers that combine AI, IoT, and automation consistently achieve above-average EBITDA margins. At the same time, predictive maintenance enables both efficiency gains for customers and the introduction of performance-based compensation models. In addition, service and maintenance contracts have a stabilizing effect on the business model: they smooth out the volatility caused by economic fluctuations in the construction and modernization market. Regulatory frameworks also contribute to investment security and long-term planning.

Consolidation is accelerating

The M&A market in building automation is increasingly characterized by consolidation. The highly fragmented landscape of small and medium-sized providers offers attractive opportunities for strategic buyers seeking, above all, digital expertise—for example, in areas such as cloud architectures, AI technologies, or cybersecurity. These capabilities are becoming essential for remaining competitive and offering integrated, scalable solutions.

Companies with a high proportion of software or proprietary BMS systems also achieve higher EBITDA multiples, as software is not only more scalable but also generates more stable and predictable cash flows. Due to regulatory drivers and the increasing focus on energy efficiency, building automation is considered a particularly resilient industry.

In addition, regional expansion strategies are coming more into focus. North America and Europe remain key markets, but APAC in particular is gaining increasing importance due to high growth rates. Cross-border transactions are on the rise as companies increasingly pursue technological differentiation and geographic scaling in tandem.

Trane Technologies: Expanding digital capabilities through M&A

Trane Technologies provides a striking example of strategically driven investments. With the acquisition of BrainBox AI in 2025, Trane acquired a leading provider of autonomous HVAC optimization based on deep learning. Its technology enables energy savings of up to 25% and CO₂ reductions of up to 40%. The acquisition serves to strengthen Trane’s own digital capabilities and further develop the company’s decarbonization strategy. It also opens up or strengthens vertical markets such as hotels, healthcare, offices, retail, and airports, and unlocks potential for results-oriented service and SaaS models.

Also in 2025, Trane acquired a 49% stake in Kieback & Peter, a European specialist in smart building automation with proprietary hardware and software, service expertise, and a strong presence, particularly in the German market. The investment improves Trane’s access to an established BMS platform such as Qanteon and expands its own HVAC capabilities to include high-quality control and automation systems and lifecycle service business.

Overall, these investments strengthen Trane’s business model on multiple levels: they increase the share of recurring revenue, improve margins through software and AI services, enable extensive up- and cross-selling opportunities, and deepen customer loyalty through long-term service and SaaS contracts.

Private equity as a catalyst for market disruption

Private equity firms are playing a central role in the transformation of the building automation industry. Thanks to attractive market dynamics—including stable annual growth of 8–12%, demand underpinned by regulations, and a high proportion of recurring revenue – the sector is among the preferred investment areas. PE investors are increasingly relying on buy-and-build strategies, in which regional installation and automation companies are consolidated into larger platform groups. The goal is to realize economies of scale, optimize procurement and processes, and expand digital capabilities and software expertise.

The funds’ value creation strategies often include the digitalization of existing business models, the development of proprietary software stacks, and the expansion of the portfolio to include energy management and smart building services. By focusing on predictable cash flows from service and maintenance contracts, PE investors create stable, high-growth platforms.

At the same time, PE-financed platform groups significantly increase the pressure for innovation on traditional market participants. They drive the professionalization of software- and AI-based business models, thereby accelerating the structural transformation of the entire industry.

Success agenda for private business owners

- Prioritize digitalization: Investments in cloud-based BMS, AI-driven systems, and energy management increase enterprise value and EBITDA multiples.

- Strengthen a service-oriented business model: Expanding recurring revenue streams (maintenance, monitoring, software subscriptions) enhances stability and appeal to buyers and investors.

- Sharpen strategic positioning: Differentiation through specialization (e.g., healthcare, industry, energy efficiency) improves M&A options.

- Make the organizational structure scalable: Standardized processes, integrated IT systems, and modular service offerings facilitate integration by strategic buyers and PE platforms.

- Leverage sustainability as a competitive advantage: ESG expertise is increasingly becoming a decisive factor in acquisition decisions, particularly in light of European regulations.

Investec has a senior team in the Technology & Services sectors, who are experienced experts in selling, buying, and financing businesses.

If you have any questions or would like to learn more about building or industrial automation, company valuations, buyer activity, and current market opportunities, please contact us: [email protected],[email protected], [email protected], [email protected]

After the 2022–2023 reset, Industrial Technology valuations have rebuilt decisively, with the sector trading at 16.7x EV/EBITDA in Q4 2025 — clearly above the four-year average of ~14.2x and ~17% ahead of prior year. But the headline multiple is not the story. Dispersion remains the defining characteristic of the market: Industrial Software, Control Tech, Robots / Motions, Sensors & Vision Tech and Integrated Conglomerates command high-teens to low-20s multiples, driven by double-digit growth, expanding margins and recurring revenue, while Machinery and Engineering/SI trade at a structural discount, weighed down by single-digit to low-teens EBITDA margins, volatile project economics and disproportionate Automotive exposure. The business model and the customer base together determine where a company sits in that range — not the sector label.

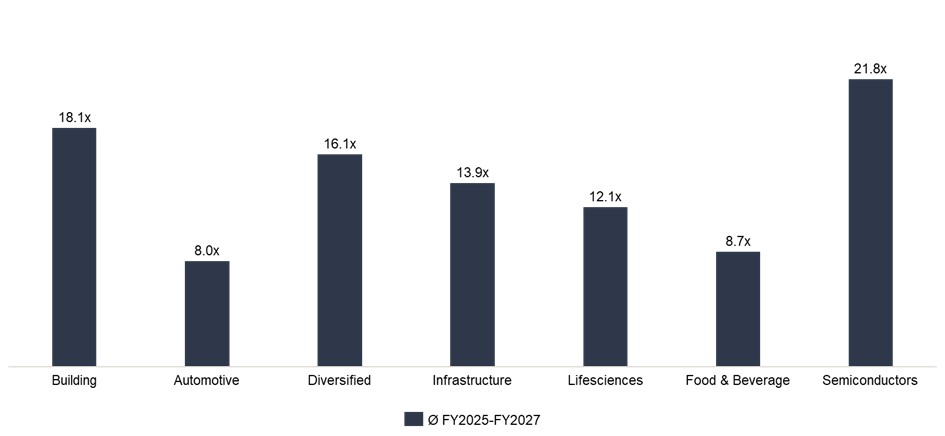

Our growth-vs-profitability analysis confirms what the multiples already imply: investors reward both dimensions equally. Companies delivering above-average sales growth and EBITDA margins above 25–30% consistently sit at the top of the valuation range — those that underdeliver on both fall below 8x regardless of what they call themselves. End market exposure has emerged as an equally decisive factor: sub‑sectors tied to Semiconductors (~21.8x) and Building‑related applications (~18.1x) benefit from structurally non‑deferrable, often regulation‑driven capex, with Diversified and Infrastructure exposures trading in the mid‑teens; Automotive‑ and Food & Beverage‑heavy segments sit closer to 8x, a discount that the revenue model alone cannot overcome.

For entrepreneurs and sponsors, the implication is direct: premium multiples in Industrial Technology are increasingly reserved for software‑enabled, automation‑driven models with durable margins, recurring revenue and a customer base that treats technology as operational necessity — not for cyclical exposure or thematic labels alone.

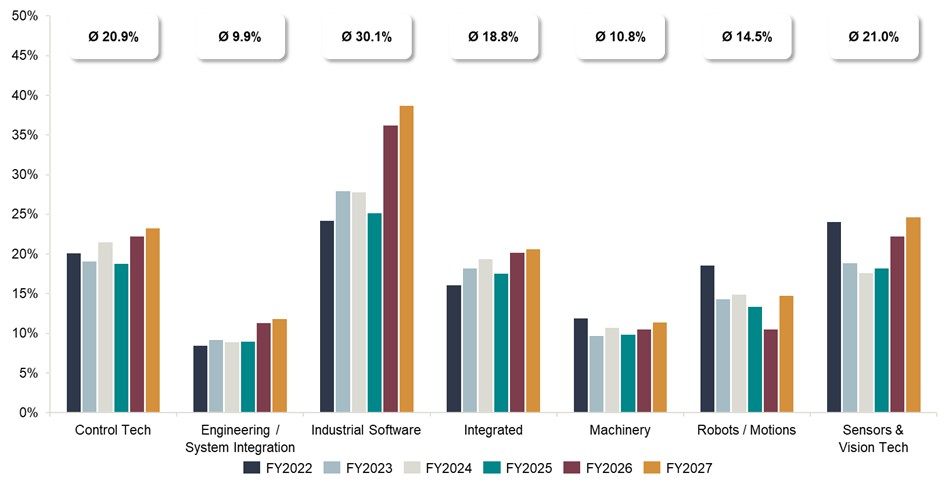

EV/EBITDA: End market comparison Ø FY2025-FY2027

Our end‑market analysis shows that valuation is now as much about where you sell as what you sell.

- The new framework splits the universe into Building, Automotive, Diversified, Infrastructure, Lifesciences, Food & Beverage and Semiconductors, each with a distinct “lane” of mid‑cycle multiples.

- At the top, Semiconductors and Building command high‑teens to low‑20s EV/EBITDA, reflecting non‑deferrable, mission‑critical capex; Automotive and Food & Beverage sit closer to 8–9x, despite similar business models in some cases.

- Diversified and Infrastructure names form the middle of the range, anchoring the overall sector multiple but masking a clear two‑speed market underneath.

EV/EBITDA Development by sub-sector: Q1 2022 – Q4 2025

The sector has rebuilt to a healthy level — but the headline multiple masks a structural divide.

- Valuations have normalised at 16.7x EV/EBITDA in Q4 2025, ~17% above the prior year and clearly above the four-year average of ~14.2x. Six of seven sub-sectors currently trade at or above their historical averages.

- The spread tells the real story: Industrial Software at 21.8x, Engineering/SI at 9.1x — a gap of over 12x. Buyers are paying for business models and end market exposure, not sector labels.

- It’s a two-speed market: software-enabled sub-sectors serving non-cyclical end markets like Semiconductors, Building, Infrastructure and Lifesciences command teens to low-20s multiples, while hardware-intensive, project-based segments with heavy Automotive or Food & Beverage exposure cluster around 8–9x.

- Within our peer set, companies with comparable margins and similar recurring revenue shares trade 3–5x apart when their end market mix diverges — a Control Tech platform serving Building end‑markets commands a structurally different multiple than one with equivalent economics but dominant Automotive exposure. End market quality is not a secondary factor — it is a primary valuation driver in its own right.

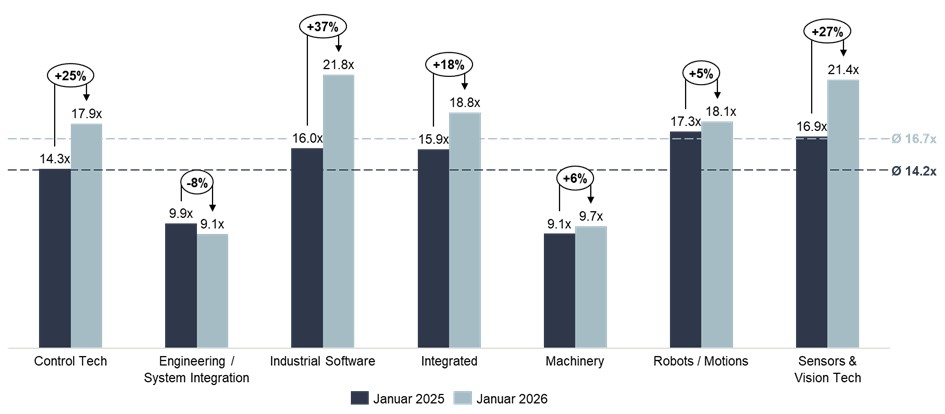

EV/EBITDA: YoY comparison 01/2025 – 01/2026

The re-rating is concentrated in software-rich models serving structurally growing, non-cyclical end markets.

- Industrial Software (+37% to 21.8x), Sensors & Vision Tech (+27% to 21.4x) and Control Tech (+25% to 17.9x) show the strongest momentum — driven by AI-embedded automation and IIoT adoption in Semiconductors, Building and Infrastructure, where capex is non-deferrable and regulation enforces technology investment.

- Integrated Conglomerates (+18% to 18.8x) benefit from diversified portfolio breadth — spanning automation, software, electrification and industrial infrastructure — and growing exposure to Building and Semiconductor end markets, where secular demand provides a durable multiple floor.

- Engineering/System Integration (−8% to 9.1x) is the only sub-sector with negative momentum — high Automotive concentration compounds the structural disadvantages of a project-based model: limited pricing power, high execution risk and cyclical order intake.

- Machinery (+6% to 9.7x) and Robots/Motions (+5% to 18.1x) appear relatively stable for now, though the divergence between them reflects the difference between predominantly Automotive-exposed equipment businesses and automation platforms increasingly deployed in Food, Logistics and general manufacturing. While EV platform transitions and battery production ramp-ups may create selective re-rating catalysts for Automotive-exposed players, the broader segment discount is unlikely to compress meaningfully without a structural shift in OEM procurement behaviour and margin-sharing dynamics.

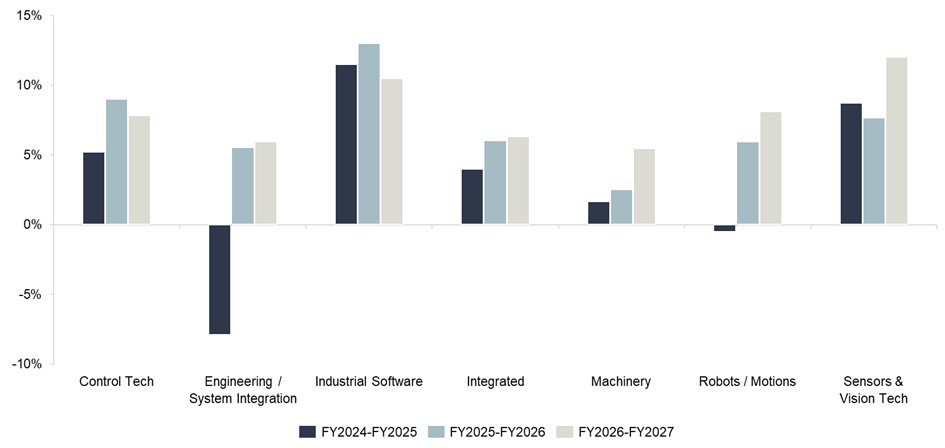

Revenue growth in % by sub-sector: 2024 – 2027E

Growth quality matters as much as growth rate — end market determines how sustainably it compounds.

- Industrial Software and Sensors & Vision Tech are leading at 10–12% p.a. through 2027, driven by data, analytics and workflow-automation spend in Pharma, Healthcare and Semiconductors.

- Control Tech and Robots/Motions form the second tier at 6–9%, supported by automation intensity across non-cyclical end markets: pharma filling lines and logistics automation are structurally less sensitive to macro headwinds than Automotive capex.

- Engineering/SI recovers from −8% to mid-single-digit growth, but this is largely deferred Automotive projects catching up — not a structural improvement. As long as Automotive dominates the order book, top-line recovery does not translate into re-rating.

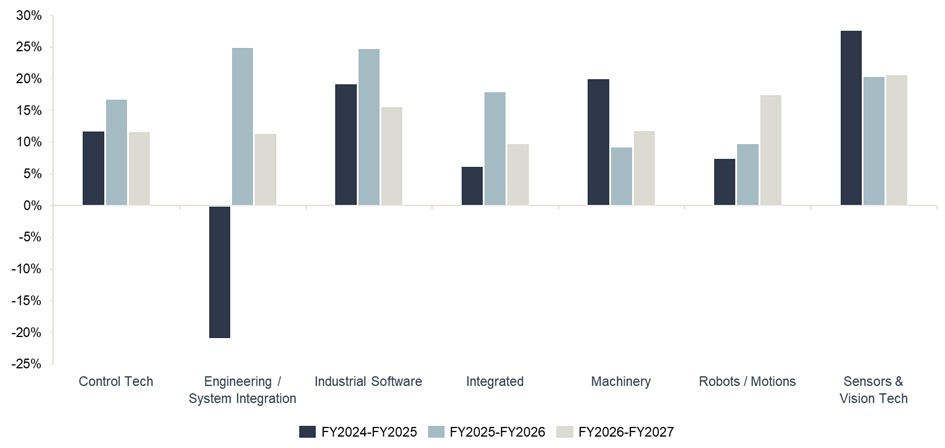

EBITDA growth in % by sub-sector: 2024 – 2027E

Scalable profitability — not just top-line growth — is what the market is pricing.

- Industrial Software delivers ~20% EBITDA growth transitioning to ~16% — a healthy maturity curve where initial operating leverage converts into durable profitability, reinforced by Pharma and Healthcare customers who sustain higher pricing than industrial OEMs.

- Robots/Motions accelerates to ~17% EBITDA growth by FY2027, driven by Logistics and Food automation demand — a clear signal that software economics are increasingly visible in the P&L as the platform mix shifts away from Automotive assembly.

- Engineering/SI swings from −21% to +10%, driven by restructuring and improved project selection — not structural margin expansion. The recovery remains fragile as long as Automotive dominates the order book and OEM pricing dynamics compress margins at renewal.

EBITDA-margin by sub-sector: 2022 to 2027E (in %)

The margin gap between sub-sectors is the root cause of the valuation spread — and end markets explain much of it.

- Industrial Software improves from 24–28% toward ~40% by FY2027 (Ø 30.1%) — best-in-class software economics, further supported by end markets where customers treat software as mission-critical infrastructure and accept premium pricing accordingly.

- Sensors & Vision Tech (Ø 21.0%), Control Tech (Ø 20.9%) and Integrated Conglomerates (Ø 18.8%) sustain robust margins through diversified product portfolios, IP-rich platforms and strong aftermarket revenue — reinforced by Food, Pharma and Semiconductor end markets where downtime costs and regulatory requirements structurally strengthen pricing power.

- Engineering/SI and Machinery at ~10% average reflect a structural constraint that goes beyond the business model: Automotive OEMs systematically compress supplier margins through competitive tendering, volume pressure and cost-down programmes — creating a margin ceiling that is difficult to break without a fundamental shift in the customer base.

- Robots/Motions (Ø 14.5%) is the most asymmetric opportunity — despite today’s relatively stable multiples, it has a hybrid margin profile today but a clear trajectory toward software economics as platform deployment shifts from Automotive assembly toward Semiconductors, Logistics and Healthcare automation.

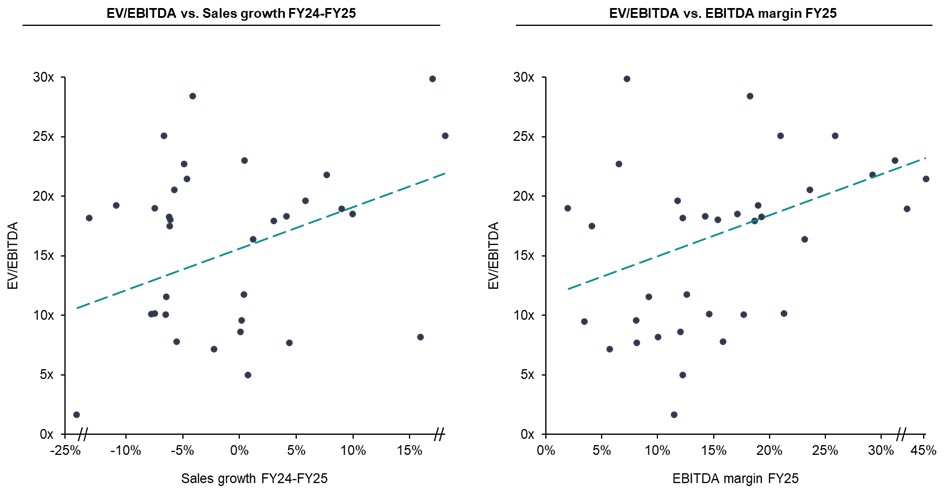

Correlation analysis – Industrial Technology

In Industrial Technology, investors reward profitable growth. Both dimensions matter equally.

- The scatter plots show a clear positive slope for both EV/EBITDA vs. sales growth (FY24–25) and EV/EBITDA vs. EBITDA margin (FY25) — and both correlations are broadly comparable in strength.

- Companies combining above-average growth with EBITDA margins above 25–30% typically trade above 20x. Double underperformers — negative growth and low margins — fall below 8x, regardless of sector label.

- End market quality acts as a third, implicit factor: companies in defensive, non-cyclical end markets show lower earnings volatility and higher margin persistence — which is visible in the upper tail of both scatter plots and directly translates into multiple resilience.

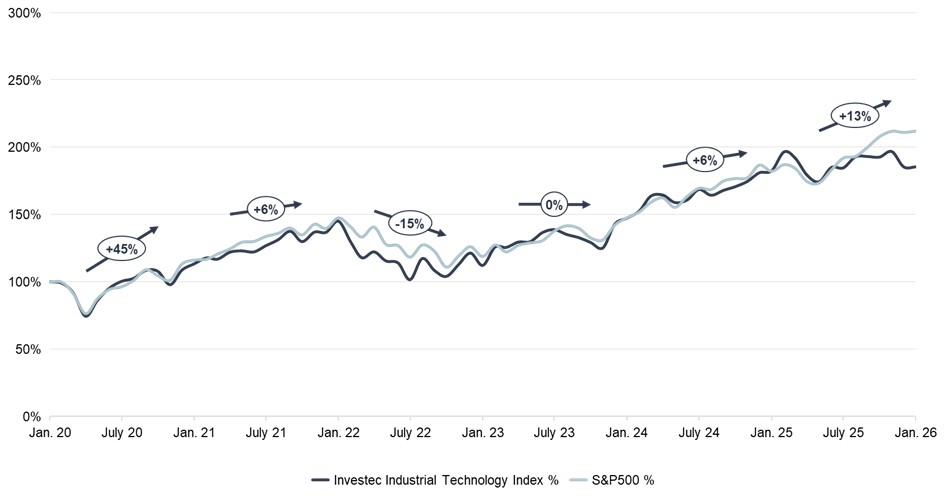

Investec Industrial Technology Index vs. S&P 500

High correlation, moderate underperformance — and the right conclusion is not what it appears.

- The Investec Industrial Technology Index has tracked the S&P 500 closely across all major market phases since 2020 — COVID crash, 2021 recovery, 2022 rate correction, and the 2023–2025 rally.

- On a total return basis since January 2020, the index has underperformed the S&P 500 by ~25–30 percentage points — a gap that largely reflects the absence of high-multiple software pure-plays from the Industrial Technology peer set, not structural sector weakness.

- For private markets practitioners, the index comparison provides useful context but limited actionable signal. M&A returns are ultimately generated through operational value creation at the asset level — and that is precisely where Industrial Technology’s fragmented, margin-rich landscape creates the most compelling opportunities.

What does this mean in practice?

The data points above converge on a clear set of priorities for both sides of the transaction:

For entrepreneurs & owners

- Premium multiples require three things simultaneously: a software-enabled recurring revenue model, high-teens EBITDA margins with demonstrated persistence, and an end market mix dominated by structural non-cyclical demand — Pharma, Healthcare, Building, Semiconductors.

- The next 24 months should be used to build recurring revenue, improve EBITDA conversion, and actively diversify the customer base away from Automotive — each of these directly converts into exit valuation.

For investors & strategics

- The most powerful value creation lever available today is end market transformation: pivoting Automotive-heavy assets toward Pharma, Semiconductors and Healthcare can unlock a 6–8x multiple differential that is measurable, quantifiable and accessible through targeted add-on strategy.

- Robots/Motions offers the most asymmetric profile: entry at hardware multiples, exit potential at software multiples as platform deployment shifts toward non-cyclical, high-margin end markets. Integrated Conglomerates, meanwhile, provide portfolio resilience and multiple stability — their diversified exposure across end markets and business models makes them a natural anchor allocation rather than a re-rating play.

Sector exposure without an end market and model filter delivers average returns, not outperformance — selectivity is the only viable strategy in the current environment.

The Investec Industrial Technology Index tracks daily developments in sectors such as Control Tech, Industrial Software, Integrated Providers, Engineering, Machinery, Vision Tech & Robots/Motions. The index includes valuations, growth projections, profitability margins and other metrics. You can find more information on our website and specific industry insights in our latest Systems Integration Report.

Investec has a senior team in Industrial Technology, who are experienced experts in selling, buying, and financing businesses.

If you have questions and would like to know more about valuations, buyer activity and current opportunities in the market – please get in touch: [email protected], [email protected], [email protected]

European chemicals companies continue to attract strong acquisition interest, with specialty and innovation-driven businesses commanding the highest valuations.

Large international chemical companies remain highly active in M&A, targeting businesses that offer differentiated technologies, specialty products, or access to new markets. This sustained demand creates a competitive environment for high-quality assets.

For financial investors, the fragmented market structure – combined with innovation-driven growth and sustainability trends – continues to create attractive opportunities to build larger specialty chemicals platforms.

Western Europe and the Benelux remain a highly attractive region for both global acquirers and private equity investors, driven by strong industrial ecosystems, innovation capabilities, and export-oriented business models.

Please contact Marleen Vermeer or Thom Deckers to access our full Chemicals Sector M&A Insight Report exploring the key trends, market dynamics, and valuation benchmarks shaping the European market.

A day full of inspiration and intensive exchange

On 16 September 2025, Investec Advisory together with FINANCE Think Tank co-organised Dealsourcing 2025 in Frankfurt/Oberursel. With over 1,000 industry experts from M&A, private equity and corporate finance, it is one of the largest events in the German corporate finance community.

Pressure to sell or investment crunch: what is driving financial investors?

In the opening plenary session, Ervin Schellenberg, Managing Partner Investec Advisory together with Matthias Weidner, Head of Business Development DPE Deutsche Private Equity, made a clear statement on the current market situation: “Those who need to sell will sell. Those who still have time will first work on optimising their business.” This quote illustrates the current bifurcation of the market: On the one hand, there are companies that have to sell due to pressure, and on the other, there are companies that are optimising their processes and business models before engaging in transactions.

Holger Truckenbrodt, Partner Investec Advisory said: „Great opportunity to get in contact with new potential business partners that weren’t on my radar screen so far.”

In addition to the plenary session, Investec Advisory organised two well-attended workshops:

Is the next wave of M&A coming in healthcare services?

Matthias Holtmeyer, Managing Partner Investec Advisory, discussed the question of whether the healthcare sector is facing a new phase of consolidation and what opportunities and risks investors can expect. A big thank you to our panelists Martin Spirig, Partner at Invision, Ingmar Wegner, Managing Partner at CONVALES, and Dr Thomas Willaschek, Partner and specialist lawyer for medical law at Luther Rechtsanwaltsgesellschaft.

Modern Food – an M&A niche with great potential

Jürgen Schwarz, Managing Partner Investec Advisory led the session, providing exciting insights into the current M&A trends in the food sector from the perspective of manufacturers and investors. A big thank you to our panelists Carsten Hackel, CFO Germany Nestlé, Andreas Holtschneider, Partner PAI Partners, Godo Röben, Supervisory Board & Advisory Board for Plant-Based Foods, and Fabio Ziemssen, Partner Zintinus.

Both sessions addressed highly topical issues and offered not only exciting insights, but also the opportunity to engage directly with industry leaders.

The focus for Investec Advisory was on exchanging ideas with clients, partners, and new contacts. Many of our conversations showed that personal networks are key to success, particularly during challenging market phases. The event provided an opportunity for us to share our expertise, shed light on key market issues and engage in valuable discussions with partners and clients.

We would like to thank all our panelists, contributors and the Deal Sourcing team for the intensive exchange and look forward to Dealsourcing 2026.

Click below for the Aftermovie:

How a professional dialogue is now moving companies forward

Interview with Thorsten Gladiator, Managing Partner of Investec about how a professional dialogue is now moving companies forward:

- Why companies should entertain a professional dialogue with their investors and lenders?.

- What other challenges are companies facing?

- As a financial expert and transaction specialist what advice do you have for companies when dealing with debt and equity investors?

- Giving an example.

This video answers these questions and give you an idea and overview in a few minutes.

Finding the right type of capital and investor to help grow your business

Our team has a long track record of successfully raising equity and debt capital and has the necessary expertise and networks:

- Raising capital to support business growth

- Securing capital from private equity and/or other Investors to support MBO/MBI projects

- Securing capital from private equity and/or other investors to manage changes in the shareholding structure (such as supporting the buyout of one or more shareholders and the reallocation of equity shares)

- Project financing: supporting companies in realizing essential investments or working capital

- Refinancing: supporting companies in reorganizing/reducing their debt burden

We’re pleased to announce a further expansion of our international M&A advisory business with the integration of Capitalmind Switzerland into the Investec brand.

The Swiss team, lead by Markus Decker and Thomas Ellenberger, is proud to join Investec, reinforcing our shared commitment to delivering tailored M&A advice and solutions.

It’s an important milestone for our team and clients, strengthening our presence and capabilities across Europe.

This latest acquisition underscores our commitment to expanding our advisory business, where we now have 300 M&A professionals based across 17 offices globally, and complements the growth of Investec’s integrated offering in Switzerland, which includes private banking, wealth management and direct lending.

“By uniting our M&A professionals accross Europe, we are able to bring fresh ideas and tailored solutions to clients in Switzerland and internationally.”

– Markus Decker, Managing Partner of Swiss office

“This acquisition deepens our Swiss presence and enhances global collaboration, connecting clients to international and local investment opportunities.”

– Jonathan Arrowsmith, Head of Investment Banking, Investec

All our Swiss team members:

Markus Decker, Thomas Ellenberger, Yanik Costa, Dr. Miró Feller, Tim Graber, Kai Kiesinger, Lorenzo Mattei, Luca Stalder and Gabi Korolnyk

Learn more:

Switzerland | Investec Advisory

We at Investec Advisory together with FINANCE Think Tank, are delighted to co-host DEALSOURCING2025 – the leading networking event for the German Corporate Finance community – on 16 September 2025 in Oberursel, near Frankfurt. It is one of the largest events in the German corporate finance community, with over 1,000 participants from the fields of M&A, financing, and restructuring.

Highlights in the opening plenary: “Pressure to sell or Investment crunch: What is Driving Financial Investors?”

Our Managing Partner Ervin Schellenberg and Matthias Weidner, Head of Business Development DPE Deutsche Private Equity will discuss the key question in the opening plenary session.

Workshop 1 at 11:00 am: Is the second M&A wave coming in Healthcare Services?

Matthias Holtmeyer, Managing Partner at Investec Advisory, invites visionaries Martin Spirig, Partner at Invision, Ingmar Wegner, Managing Partner at CONVALES, and Dr Thomas Willaschek, Partner and specialist lawyer for medical law at Luther Rechtsanwaltsgesellschaft, to an expert panel to discuss whether the next wave of M&A activity in healthcare services is coming.

Workshop 2 at 15:30 pm: Modern Food – an M&A niche with great potential

Jürgen Schwarz, Managing Partner at Investec Advisory, invites visionaries Carsten Hackel, CFO Germany at Nestlé, Andreas Holtschneider, Partner at PAI Partners, Godo Röben, Supervisory Board & Advisory Board Member for Plant-Based Foods, and Fabio Ziemßen, Partner at Zintinus, to an expert panel discussion on the question of M&A potential in the modern food sector.

We look forward to a day full of knowledge-sharing, fresh ideas, and new connections.

More on the programme: www.dealsourcing.de

Date: Tuesday, 16 September 2025

Location: Dorint Hotel Frankfurt/Oberursel, Königsteiner Str. 29 61440 Oberursel

Investec is proud to announce that our French team is awarded as one of the Best Investment Bank – LBO Small to Mid Cap with a Silver Award at the recent Sommet des Leaders de la Finance in Paris.

Organised by Décideurs Corporate Finance, this event recognises excellence in corporate finance and highlights the work of professionals who lead complex and strategic transactions.

We warmly thank our teams for their dedication, and our clients for their continued trust.

Helen Lucas | UK

Jonathan Harvey | UK

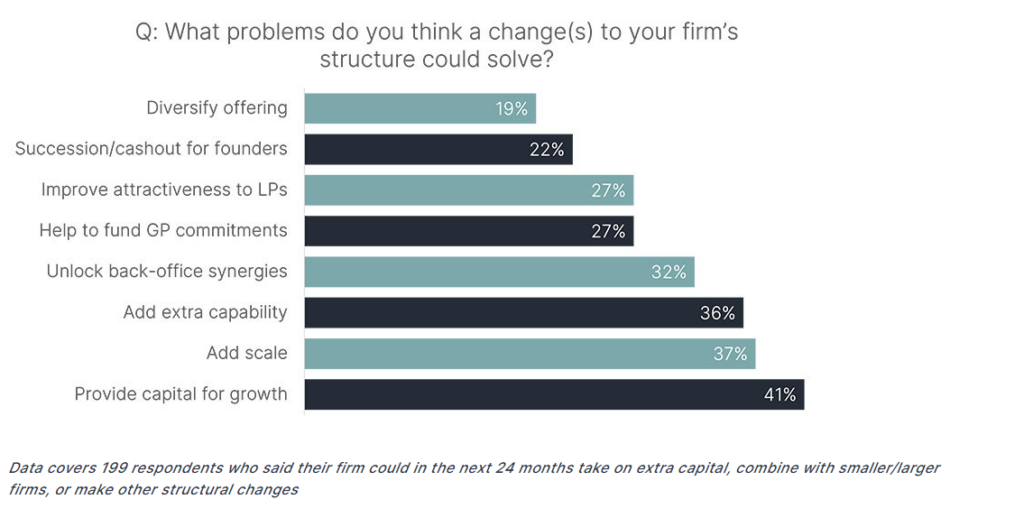

Our 14th report comes at a crucial time for the industry, as GPs get back to the business of selling portfolio companies and raising new funds.

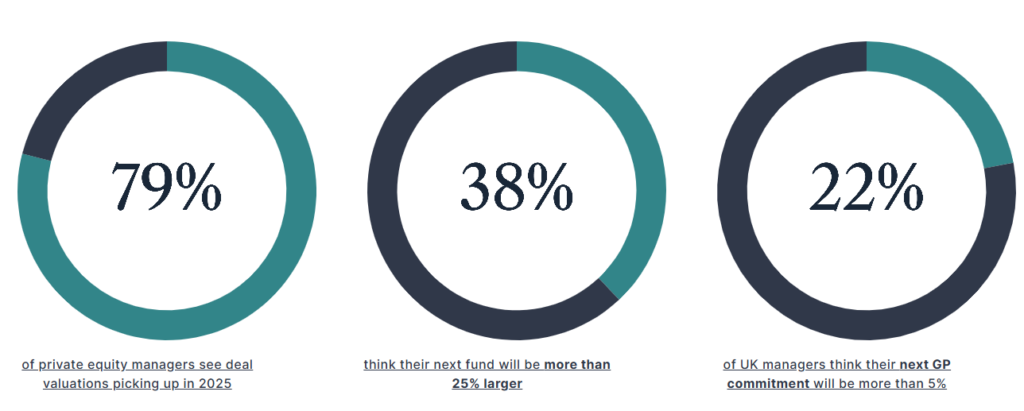

2024 was a tough year for private equity and the overriding view from our survey of 253 general partners (GPs)* is that 2025 will be different.

Our findings show an industry which, despite challenges over the past few years, is resilient, adaptable, and anticipating a more favourable period ahead.

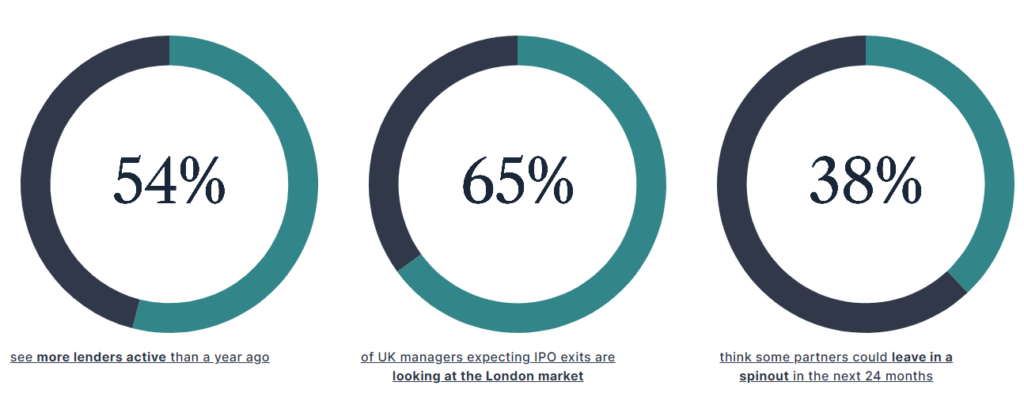

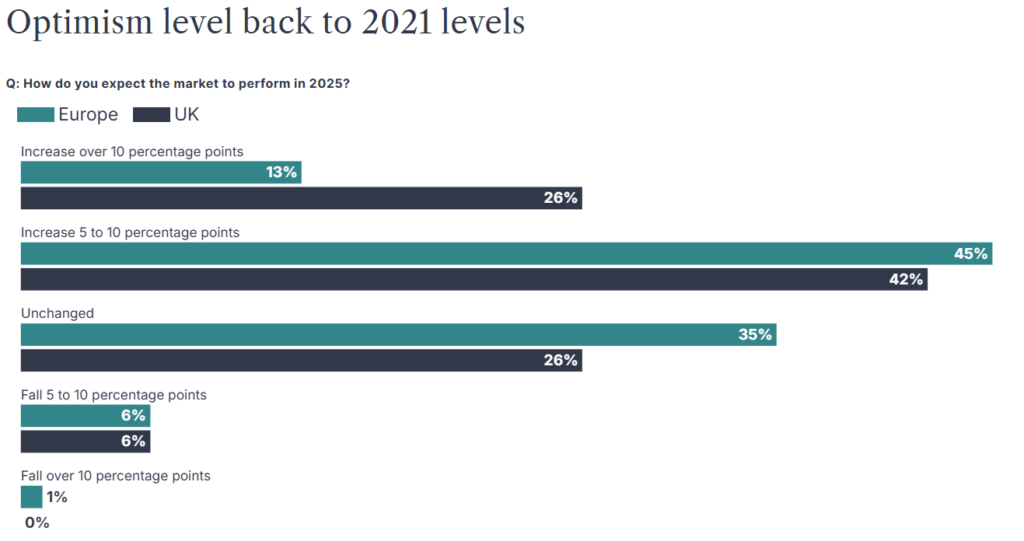

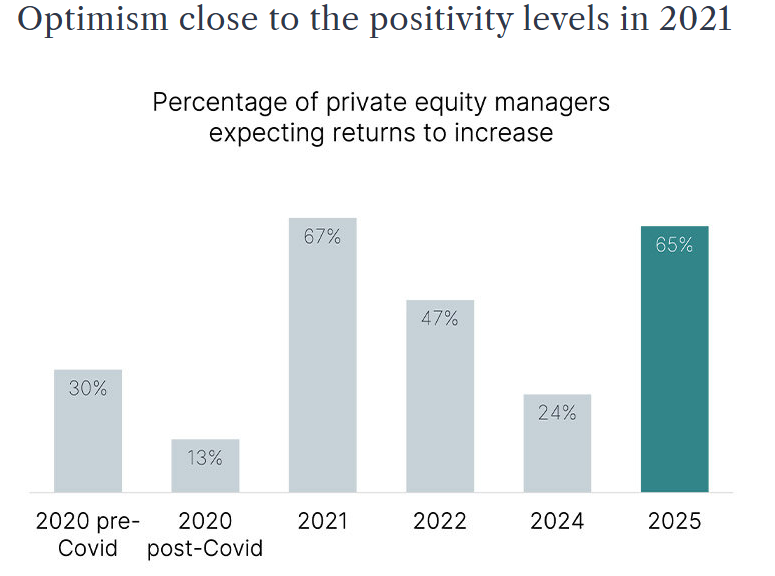

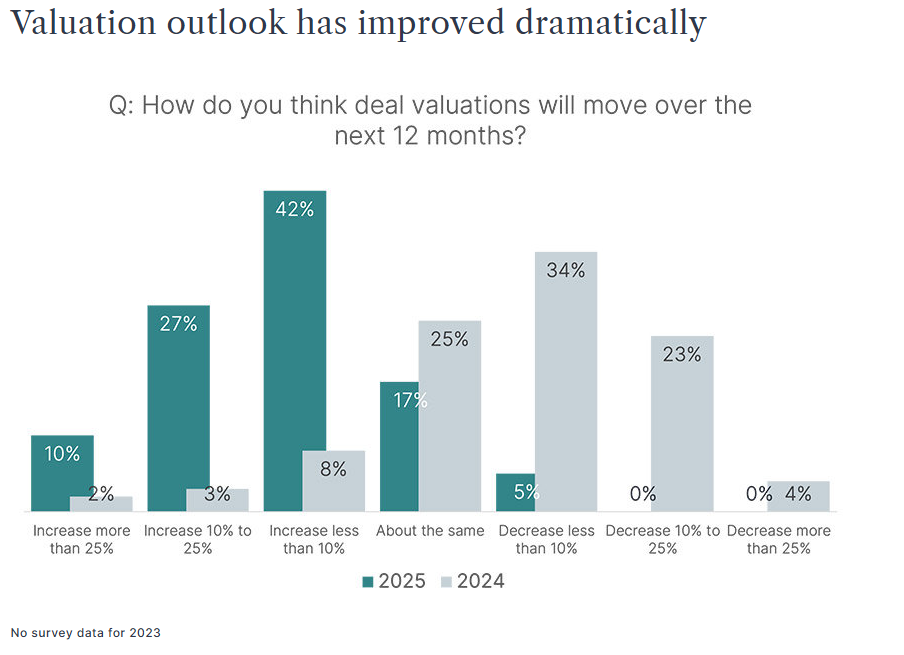

Four in five GPs expect deal valuations to increase in 2025 as interest rates come down, helping to clear exit bottlenecks and accelerate investors’ distributions. The outlook for returns is also brighter, with improvements registered across geographies and fund sizes. Close to two thirds (65%) of investors see returns improving in 2025, up from only 24% in 2024.

Dealmakers still must navigate ongoing geopolitical and macroeconomic risk, as trade tariff tit-for-tats continue and conflicts in the Middle East and Ukraine remain unresolved. It is a complex market, but the backdrop for M&A is better than it was a year ago.

Jump to a section:

Future fundraisings

GP commitments

New world of debt

Innovations and exits

GPs at a crossroads

Future fundraisings

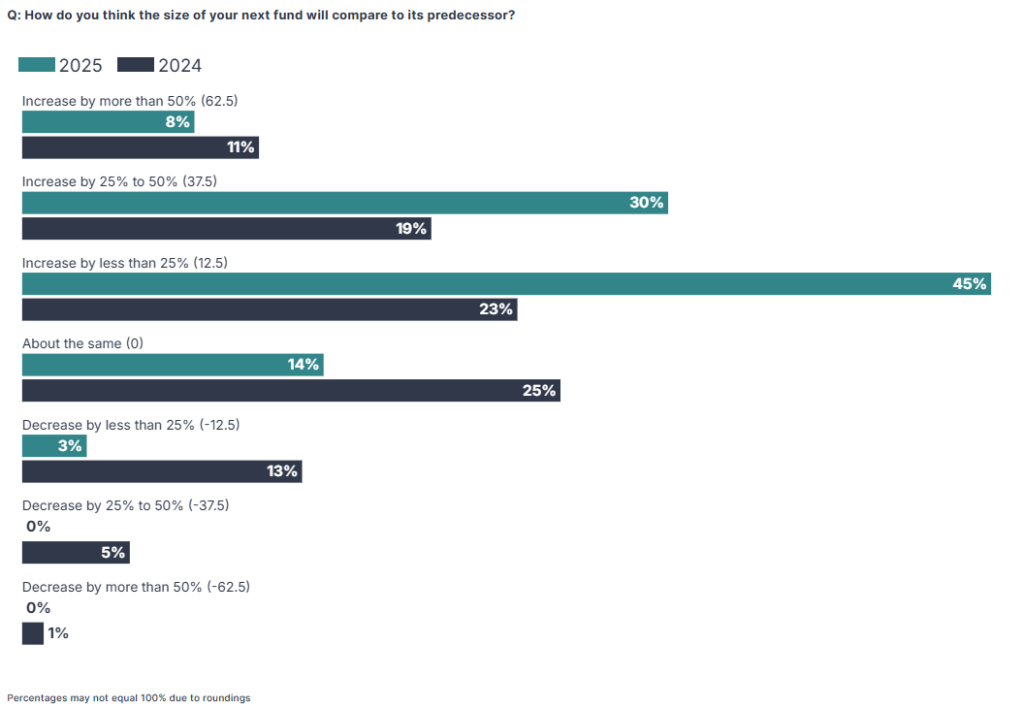

In 2024, 21% of respondents expected a down raise for their next fund: the 2025 research shows only 3% anticipating the same scenario.

There is also a large cohort of super-optimists – 38% expect their next raise will be a blockbuster increase of 25% or more over their previous fund.

Limited partners (LPs), however, are expected to remain highly selective in 2025. In 2024, according to PEI figures1, the ten largest funds to close in 2024 all secured more than $10 billion and absorbed more than a fifth of total fundraising allocations while a Coller Capital LP survey2 showed that the top focus for 98% of investors is that a new manager has a team with a strong track record.

Our survey findings tie in with this theme – close to a third of respondents (31%) expect an increasing number of GPs to move into wind-down. However, this does not mean the opportunity for new managers has passed; just 26% agreed that “very few new GPs will be launched”.

Although fundraising conditions are improving, LPs continue to consolidate GP relationships, focusing on managers of scale and mid-market specialists with differentiated investment strategies and exceptional returns.

Fundraising optimism surges

Jump to a section:

Deal valuations

GP commitments

New world of debt

Innovations and exits

GPs at a crossroads

GP commitments

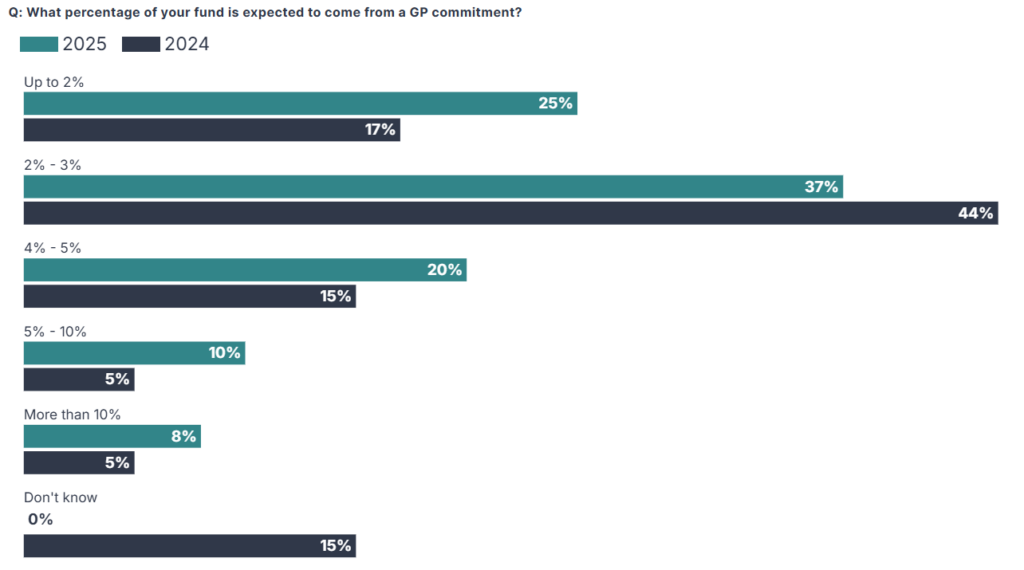

The survey shows GPs are planning to up their commitment from the typical 2% to 3% to strengthen alignment with investors and boost fundraising momentum.

- One in five GPs expect to commit 4-5% of their next fundraise.

- One in ten expect their next commitment to be 6-10%.

- 8% expect to commit more than 10% in 2025.

Managers are taking a blended approach to financing these higher commitments including existing resources, reinvesting carried interest and external debt, which is gaining favour. Most are using two options to fulfil their obligations, with 13% expecting to use three options.

Where are commitments highest?

The findings reveal interesting regional variations when it comes to GP commitments.

UK managers are more likely to be asked for a big commitment: 22% were asked for more than 5% versus just 8% of managers in Europe. Managers in France, meanwhile, seem to be asked for a particularly slim commitment, with more than half expecting to be asked for less than 2%.

Overall, a significant minority of investors expect to up commitments in the future.

Jump to a section:

Deal valuations

Future fundraisings

New world of debt

Innovations and exits

GPs at a crossroads

New world of debt

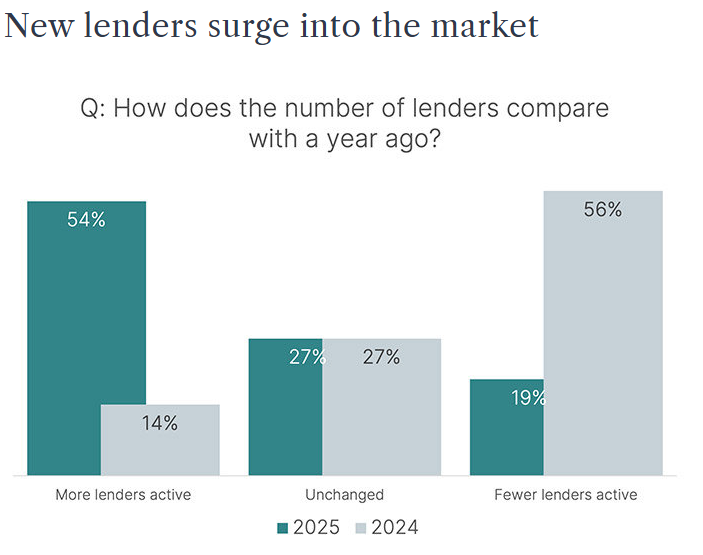

Debt markets are open for business with a substantial number of new lenders entering the market to provide GPs with enhanced financing optionality.

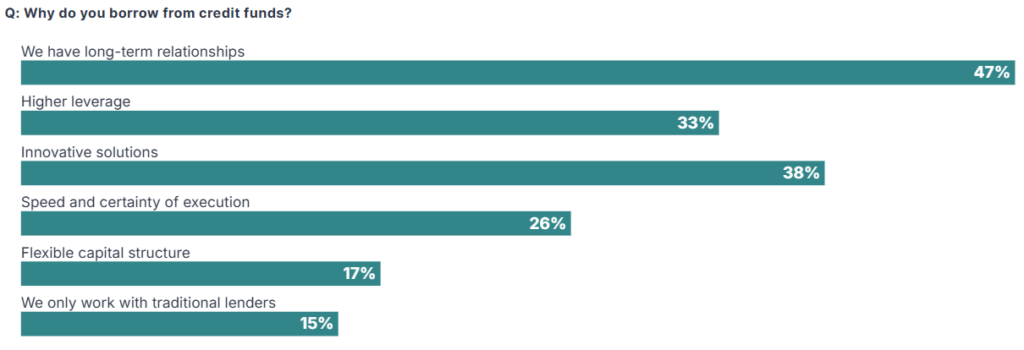

More than half (54%) of GPs say they will have new lenders to work with in 2024. This marks a shift from last year’s findings, when 56% of respondents saw a contraction in new lender activity. The majority of GPs who took part in our survey are working with credit funds and the top three reasons cited for working with a private credit included higher leverage levels and innovative financing solutions.

UK managers are hopeful that increasing competition will result in looser terms, with 54% of UK managers reporting either private debt narrowing margins or terms loosening generally. Outside of the UK, however, GPs are more cautious, with only 35% forecasting looser terms.

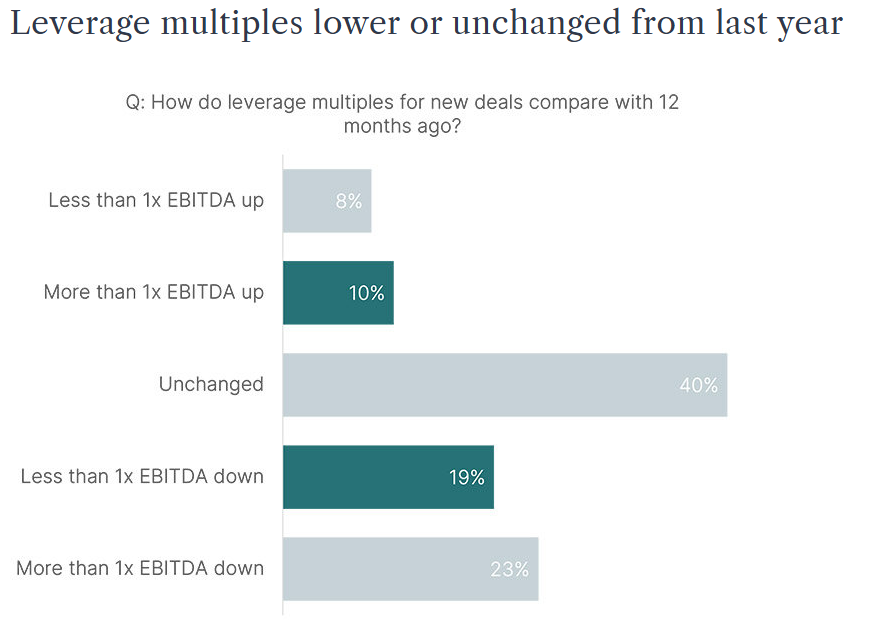

Despite these expectations, lenders are remaining disciplined. Well over a third of respondents (43%) report that leverage multiples have lowered from a year ago.

Competition is fierce for trophy assets in certain sectors, and these companies will be able to negotiate more favourable terms, but lenders will be highly selective.

Interest rates may have come down, but the risk-free rate remains elevated when compared with recent years, making additional leverage costly to service. Debt is available (European leveraged loan issuance climbed by more than 90% in 20243 and private debt managers have $126.4 billion of dry powder available to invest4), but the survey findings on leverage multiples show that capital structures remain relatively conservative.

Covenant flexibility

Even as interest rates have come down, GPs have still had to work hard to protect portfolio companies.

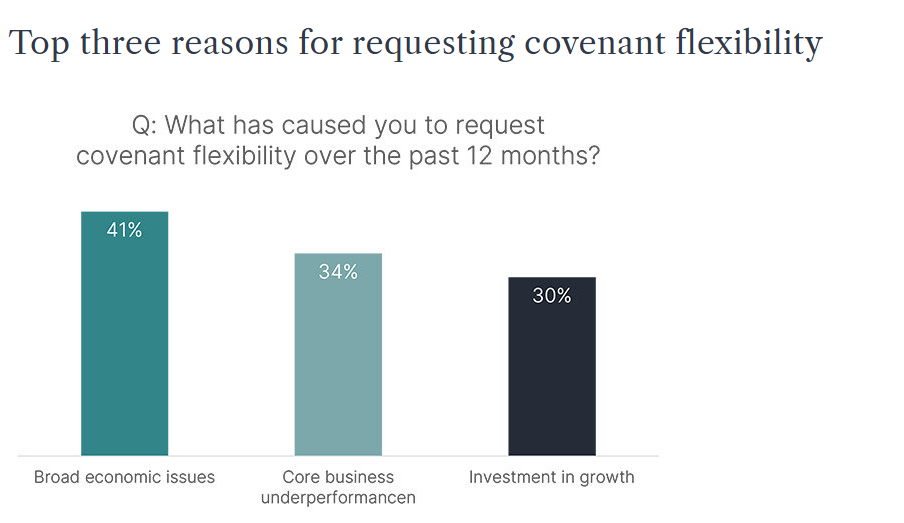

Some 87% of respondents say they have gone to lenders to request covenant flexibility for one or more portfolio companies. Broad economic issues (cited by 41%) and business underperformance (cited by 34%) are the main reasons for requesting flexibility.

Interestingly, close to a third of respondents (30%) have requested covenant flexibility to fund growth as GPs hold some portfolio companies for prolonged periods.

“We will always be open to a conversation about covenant flexibility. If a business is growing and wants to re-lever, or the sponsor wants to hold an asset for longer, loosening covenants can have a positive impact on supporting growth.” – Helen Lucas, Co-Head of UK Origination, Direct Lending, Investec

Lending landscape

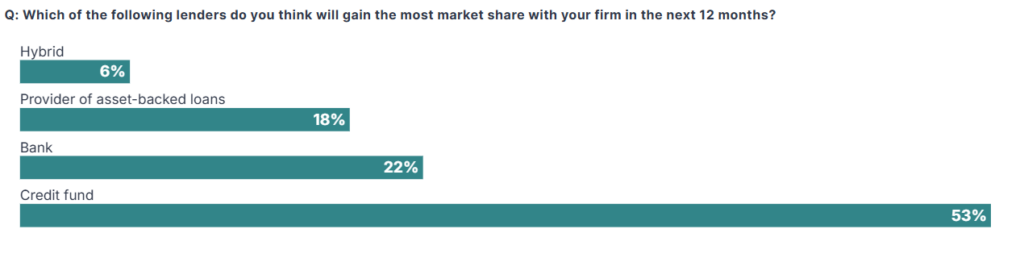

As more lenders entered the private equity space, there has also been increased use of some newer debt products. Innovation continues; survey respondents expect ESG-linked lending, fund-level finance and asset-based lending to increase market share.

Around half of the respondents expect credit funds to do more business with their firm during the year, but banks remain highly competitive; almost a quarter (22%) say they expect to place more lending with banks in the next 12 months. Hybrid capital is gaining particular traction for smaller managers with assets of $250m or less, with a quarter of these saying this type of lender will gain the most market share at their firm in the next year.

NAV lending

Net asset value (NAV) finance has proven particularly popular with managers in an environment where liquidity has been constrained.

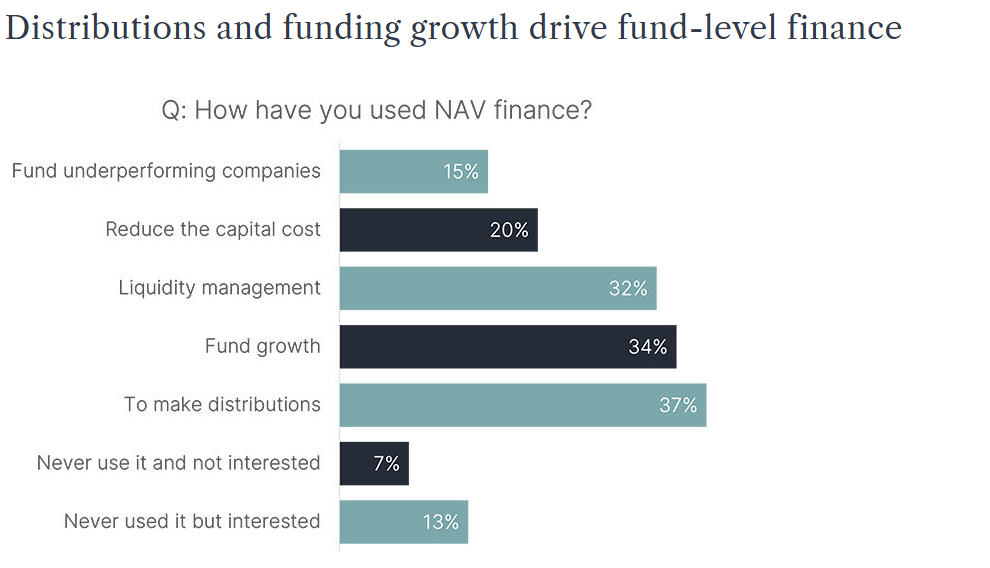

Four in five GPs said they used NAV finance in the last year, with distributions the most-cited use case (37%).

Uptake of NAV finance looks set to continue accelerating, with two thirds (65%) of respondents who had not used NAV finance previously saying they were interested in taking up NAV loans.

Deployment and operations

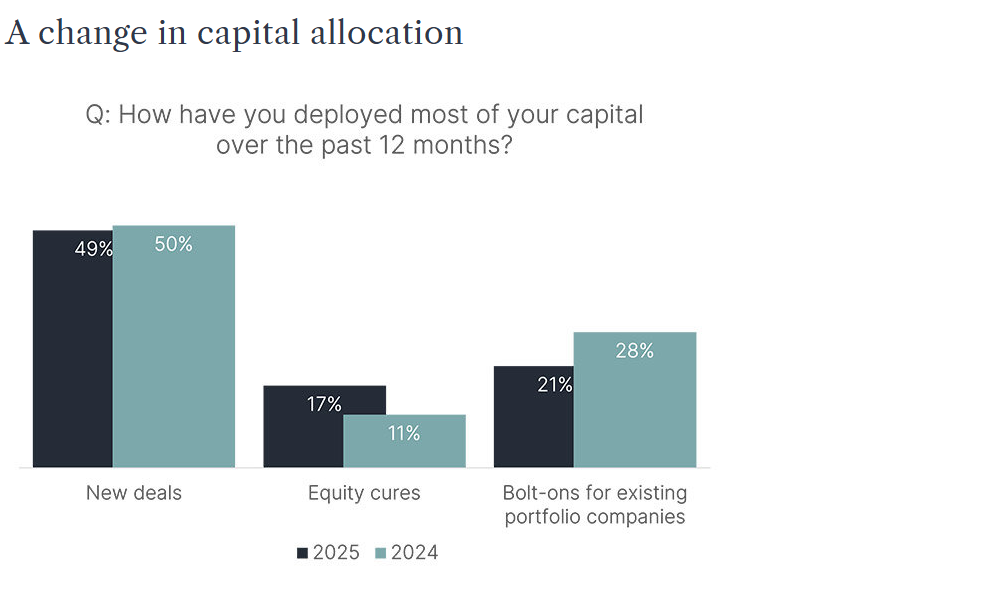

Less than half of GPs (49%) have deployed most of their capital in new deals during the past 12 months, with just over a fifth (21%) focusing efforts on smaller bolt-on acquisitions to support buy-and-build portfolios – down from 28% in our previous survey. An increase in the number of GPs deploying most of their capital in equity cures – up to 17% from 11% last year – further highlights the tough backdrop for managers during the past year.

The improving outlook means that the next 12 months should be more favourable for deployment. Somewhat surprisingly, the public-to-private outlook is mixed and not much changed from last year despite low stock market valuations, most notably in the UK5. Some 50% say they expect to look at more public-to-privates but 40% expect to look at less.

Big-ticket take-private deals during 20246 have ensured that P2P remains on the managers’ radars and may result in activity in this area.

“Private equity managers are ready to deploy, but it is taking much longer to originate deals. GPs will be forming relationships with management teams up to three years ahead of a formal process. During the last two years we have seen a number of processes fall over, and it does take time to rebuild before businesses come back to market.” – Kate Gribbon, Head of Financial Sponsor Coverage & Origination, Investec

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

Innovations and exits

GPs at a crossroads

Innovations and exits

One of the single biggest challenges for private equity managers through the rising interest-rate cycle has been to sell portfolio assets at valuations that deliver adequate returns.

In tepid IPO and M&A markets, GPs often opted to sit tight rather than offload assets at lower-than-hoped-for multiples. Hold periods remain above long-term averages, with the backlog of private equity-backed companies sitting at record levels7.

This has had repercussions on fundraising – slowing distributions to LPs have limited their ability to allocate to new funds.

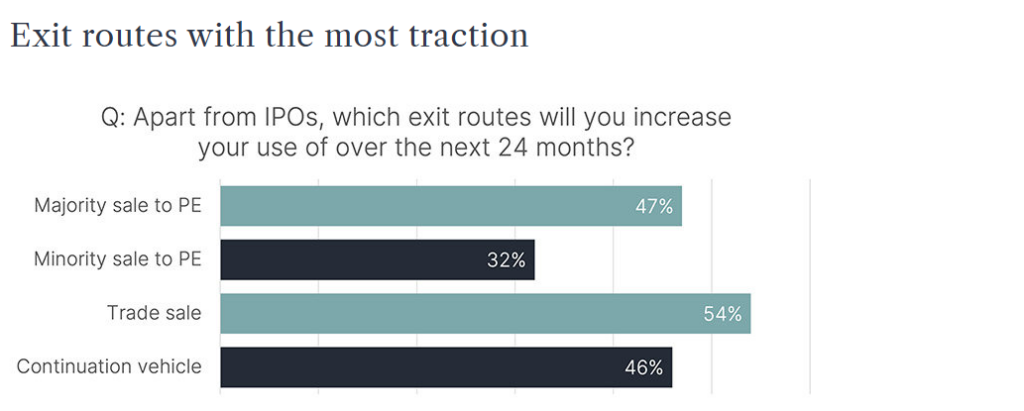

Managers looking at exits will explore all options to crystallise returns, with the survey findings ranking expectations for different exit routes in a narrow band.

More than half of GPs (54%) think trade sales will be the busiest exit route during the next 24 months. But after a long barren spell the IPO is back in the frame again, with the typical manager optimistic that two portfolio companies could be an IPO candidate over the next two years.

The squeeze on other exit routes meant there has been greater use of continuation vehicles which are here to stay as a mainstream exit path: more than 40% of GPs say a continuation fund will be an exit option they are more likely to use in the next 12 months.

The UK IPO question

Private equity-backed portfolio company IPOs haven’t always been crowd-pleasers, particularly on UK markets8, but the survey findings show managers warming to the UK stock market – albeit with some reservations.

Some 65% of UK managers who expect to list a portfolio company in the next two years consider the UK a potential venue – although they will also look at other venues such as Amsterdam or New York.

The size of the manager and portfolio is a factor in stock market selection. Larger managers with bigger assets to float think a UK IPO is less attractive, indicating that larger IPOs are considered more challenging for UK public markets.

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

New world of debt

GPs at a crossroads

GPs at a crossroads

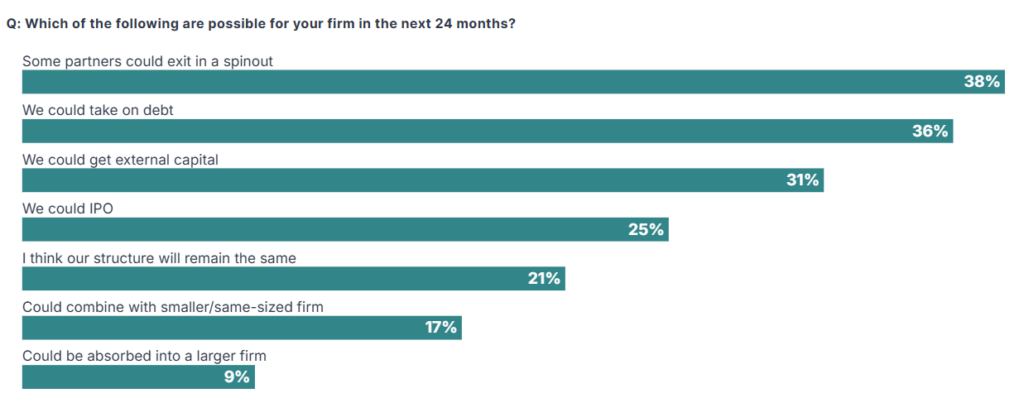

According to Pitchbook figures, GP-to-GP M&A reached record highs at the end of 20249 and the survey points to a long runway of further deals, with 79% of respondents expecting some kind of change to their firm’s structure.

In addition to GP consolidation deals, new teams are forming in spinouts and minority stake investment is proliferating.

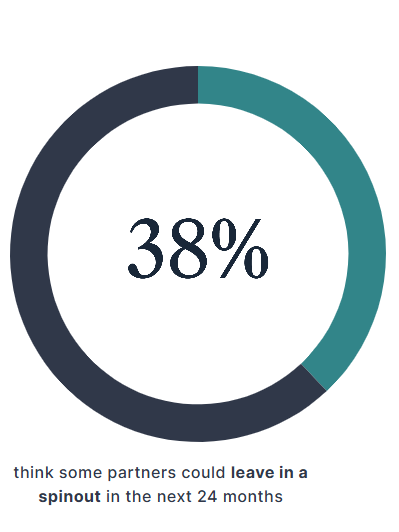

Indeed, 38% of GPs say some partners could leave their firm via a spinout in the next 24 months. This is reflective of a tougher fundraising environment, particularly for smaller managers with assets under management (AUM) below $1bn, where spinouts are more likely as junior partners explore other options when fundraisings stall.

Getting ready to capture growth

Historically, the main driver for taking on third-party capital or merging with another firm was likely to unlock liquidity and facilitate succession. While this reason was selected by 22% of respondents, the majority see a transaction as a tool to provide capital for growth or expand service lines and scale.

Ideally, twice as many managers say they would like to be the acquirer rather than target in a consolidation scenario.

What is also worth noting is that when it came to continuation vehicles, our survey showed that 40% of GPs think there will be more single-asset continuation vehicles over the next 24 months and over 25% thought they are likely to become more specialised. Single-asset continuation vehicles allow GPs to remain invested in a prized portfolio company and could potentially lead to a spin-out by a manager.

Jump to a section:

Deal valuations

Future fundraisings

GP commitments

New world of debt

Innovations and exits

* Demographic info

This report is based on 253 responses to an online survey conducted between 7 January and 22 January 2025. Respondents were sourced from a prequalified panel and no PE firm was represented more than once.

178 were based in the UK, 75 in Europe including 22 in Germany, 14 in Spain and 11 in France. Some 34% of respondents were investment directors, other eligible job titles were CFO, VP of finance, director of finance, principal and manager of finance/investments.

Footnotes:

2 https://www.collercapital.com/41-barometer-winter-2024/

4 https://www.muzinich.com/opinions/corporate-credit-outlook-2025-private-markets

6 https://www.ft.com/content/ec9aa2ae-f56a-4373-8c4b-88effc01a25d

7 https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report

9 https://pitchbook.com/news/articles/blackrock-hps-purchase-record-year-gp-consolidation

Our French team is recognised as the one of the most active firm in LBOs, M&A and Debt Advisory

We are delighted to announce that our French team has been recognised as one of the most active firm in LBOs, M&A, and Debt Advisory by CF News, a leading French publication in Private Equity and Corporate finance.

The team has achieved the following rankings:

- #4 in the LBO segment

- #5 in the M&A Small & mid cap (€50 million to €250 million deal value)

- #5 in Debt Advisory

Under Michel Degryck‘s leadership, the French team of 40 cross-sector professionals has continued to deliver results for clients in a challenging environment, delivering tailored and high-quality solutions to entrepreneurs, family businesses, corporates and private equity firms.

“This recognition reflects the trust our clients place in us and the unwavering commitment of our team. We remain dedicated to providing innovative solutions tailored to their strategic challenges.”

— Michel Degryck, Managing Partner, Investec Advisory France

Navigating Market Crosswinds Through Strategic M&A

The M&A market for industrial system integrators is currently experiencing decreased deal activity due to global uncertainty. Buyers have become more cautious, prioritizing strategic acquisitions in key end-markets and technologies.

Private equity firms remain highly active, leveraging buy-and-build platforms. With strong capital positions, strategic positioning in key end-markets and technologies, players are well-placed to capitalize current market crosswinds through M&A.

Ongoing consolidation, underscores the sector’s long-term potential for scalable growth.

Ervin Schellenberg, Managing Partner Investec

This report provides an overview of valuations, transactions, buyers, etc. in the European industrial systems integrator market.

To access and read the full report click here

Investec announces the appointment of Michael Eriksen as Head of Nordic M&A in support of its strategy to significantly grow its presence in Europe. Michael brings over 25 years’ experience as an M&A advisor to companies in the Nordics.

In his new role, Michael will focus on identifying and pursuing growth opportunities for clients, in line with Investec’s 25-year track record as a trusted M&A advisor to clients globally, particularly in Europe. Investec provides tailored M&A advice to clients, many of whom operate in the mid-market across a wide range of sectors, helping them achieve their growth objectives.

In 2023 Investec acquired a majority interest in Capitalmind and, with effect from today, completes its transition to the Investec brand.

“Companies across multiple sectors in the Nordics are actively seeking opportunities to expand beyond their borders. Michael’s established relationships and expertise will be invaluable as we enhance our M&A advisory capabilities in the region. At the same time, we are committed to bringing our broader expertise to the Nordics, including leveraged finance and fund solutions for private equity, such as GP financing, continuation funds, and NAV facilities.”

Jan Willem, Managing Partner and Board Director of Investec Continental European Advisory BV (ICEA)

“The Nordic region is a dynamic and expanding market. I firmly believe that Investec, with its strong client focus and comprehensive banking capabilities, is ideally positioned to capitalise on the opportunities that lie ahead.”

Michael Eriksen, Head of Nordic M&A

Case Study

Aqseptence Group, a global leader in autonomous water and filtration technology, equipment and system solutions specialising in water treatment and liquid/solid separation, has attracted Oaktree, a leading global investment manager, as an investor.

Oaktree’s investment and expertise will provide Aqseptence Group with the necessary resources to continue to grow and innovate to best serve existing and new markets.

Interview with Baldassare La Gaetana, CEO of Aqseptence Group and Ervin Schellenberg, Managing Partner of Investec, taking us through the process and decision making of Oaktree’s majority investment in Aqseptence in a short video:

- What is the Aqseptence Group? Why a new shareholder?

- What is your sector and investor perception? – Opinion Ervin Schellenberg

- Why is it important to work with an M&A advisor? – Opinion Baldassare La Gaetana

- How was the collaboration with Investec?

For nearly 25 years, Investec has been assisting its clients in reaching their strategic goals, whatever it takes, whether it’s by securing a strategic business, or maneuvering and winning a competitive auction process:

We are particularly adept at advising on the following situations:

- Acquiring (family-owned) companies, groups, or other mid-market companies

- Acquiring subsidiaries or business units from (international) corporates, including carve-outs

- Acquiring businesses from a founder/(majority) shareholder, including succession

- Acquiring shares owned by a private equity firm, family office or other investors

Designing and executing such transactions is what our team does on a daily basis. To ensure success, our team also leverages its extensive experience and unique capabilities, which include: deal intelligence, tactical, technical and project management skills, negotiation skills, and an understanding of the personal interests/sensitivities of relevant stakeholders.

Investec France awarded Best Investment Bank 2024 in LBO Small to Mid cap with a Golden Award, during the last awards ceremony of the Finance Leaders Summit (Sommet des leaders de la Finance) of Décideurs Leaders League, which took place on 29 May in Paris.

Congratulations to all our teams for their hard work , and many thanks to our clients for their trust and support.

Winners 2024 – Finance Leaders Summit

The Rheingau Music Festival is one of the largest music festivals in Europe and organises over 170 concerts every year throughout the region from Frankfurt and Wiesbaden to the Middle Rhine Valley.

Unique cultural monuments such as Eberbach Monastery, Johannisberg Castle, Vollrads Castle or the Wiesbaden Kurhaus as well as picturesque vineyards are transformed every summer into concert stages for stars of the international classical music scene and interesting up-and-coming artists from classical music and jazz to cabaret and world music.

In over 30 years, the Rheingau and its festival have become a centre of attraction for music enthusiasts from all over the world in a unique interplay of culture and nature, music, enjoyment and joie de vivre.

Investec is delighted once again to sponsor the Rheingau Music Festival 2024 and invites you to join us from 22 June to 7 September 2024!

A special feature this year? For the first time, there will be two opening concerts: Traditionally, the festival opens in the Eberbach Monastery, followed by another opening concert in the Kurhaus Wiesbaden. This year’s focus artists are also particularly outstanding: violinist Christian Tetzlaff, cellist Anastasia Kobekina, pianist Bruce Liu and jazz saxophonist Candy Dulfer.

Once again this year, various themes and focuses will ensure a varied and exciting programme. Under the motto “Spot on: Hollywood”, the world of film music comes to life in twelve concerts. Under the motto “Brazil!”, the contrasts and beauties of the country will be explored musically. The programme is also dedicated to the works of Antonín Dvořák and a true classic: Vivaldi’s “Four Seasons”.

The stages of the 37th festival season will be graced by numerous stars from the worlds of classical and pop music. Highlights include star pianist Lang Lang, singers Álvaro Soler, Max Mutzke and Max Giesinger, violinist Anne-Sophie Mutter, opera singer Rolando Villazón and entertainer Eckart von Hirschhausen.

Investec has been a committed sponsor of the Rheingau Music Festival for more than 15 years. This long-standing partnership is characterised by our deep appreciation for the arts and a strong connection to local culture. We look forward to experiencing a rousing summer full of music together with you again this year.

You can view the detailed program here.