Key takeouts

- Eskom debt restructuring to be discussed with investors with no additional guidance from National Treasury.

- Additional financial support to Eskom of R10bn over and above the R23bn announced in February 2019, increasing the total financial assistance to R161bn.

- Limited fiscal consolidation over the MTEF period shows a rising debt to GDP trajectory out to F26/27.

- National Treasury has announced the intention to target a primary balance of zero by F22/23, excluding financial assistance to Eskom. This is premised on additional spending cuts of R150bn over the MTEF period which requires a reduction in the compensation bill.

- The user pay principle for E-tolls will be retained.

- The MTBPS is short on detail regarding the amount by which taxes could be raised and spending could be cut in F20/21 to reduce the budget deficit and reinstate fiscal consolidation. Spending cuts will be determined by the outcome of discussions with trade unions to rein in the wage bill.

- Treasury bill, ILB and SAGB issuance could remain unchanged notwithstanding the increase in the F19/20 borrowing requirement from R239.5bn to R394.2bn (mainly because of the increase in the main budget deficit from R255.0bn to R324.3bn). The size of the weekly TB auctions was raised in April from R8.2bn to R11.2bn and bond supply in August from R1.5bn to R5.5bn. However, the risk of National Treasury being unable to implement cuts in the compensation bill from F20/21, could lead to an increase in the size of both the weekly ILB and SAGB auctions of approximately R600m each.

- The risk of a change in Moody’s rating outlook from stable to negative has increased to above 50%.

Receive Focus insights straight to your inbox

Fiscal consolidation plans looks they were again postponed until the February 2020 Budget Review

The key focus points of the MTBPS have been (1) fiscal consolidation over the MTEF period in the context of stabilising SOEs; (2) the debt trajectory and (3) Eskom’s debt restructuring. Our key take away is that the MTBPS was short on specific detail mainly because some of the key decisions required to enhance growth and reduce spending, are political.

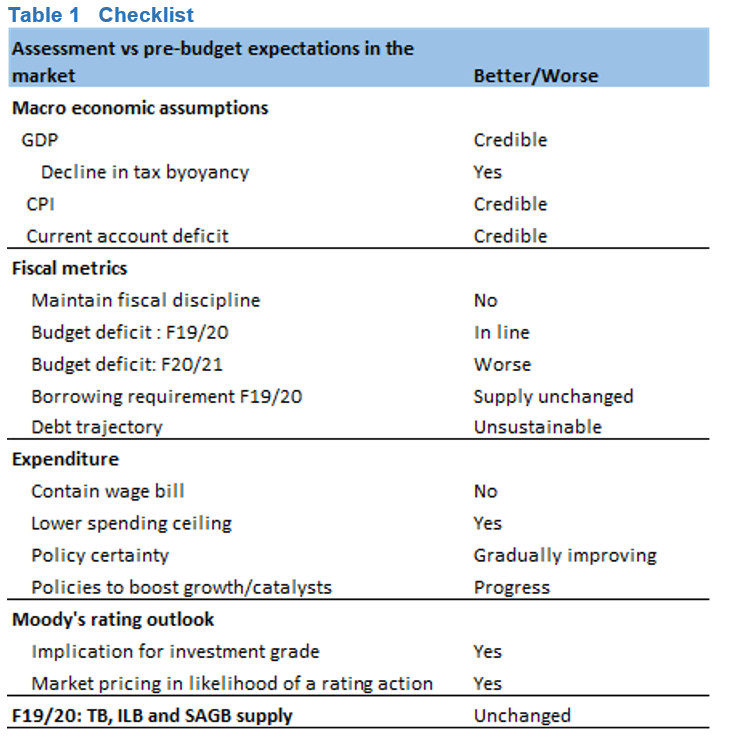

The gradual deterioration in South Africa’s fiscal metrics of the past few years, has accelerated in F19/20 which has been reflected in an increase in the main budget deficit of 4.7% of GDP to 6.2% and in F20/21 from 4.5% to 6.8% of GDP. National Treasury’s ability to stabilise a rising debt to GDP trajectory by containing the primary deficit to around 0.5% of GDP by raising taxes, has also become constrained as the tax burden on households has become onerous. The Minister of Finance has indicated that more tax increases can be expected in F20/21, over and above the R10bn already penciled into the base line forecast.

Figure 1: Political will needed to reduce the budget deficit

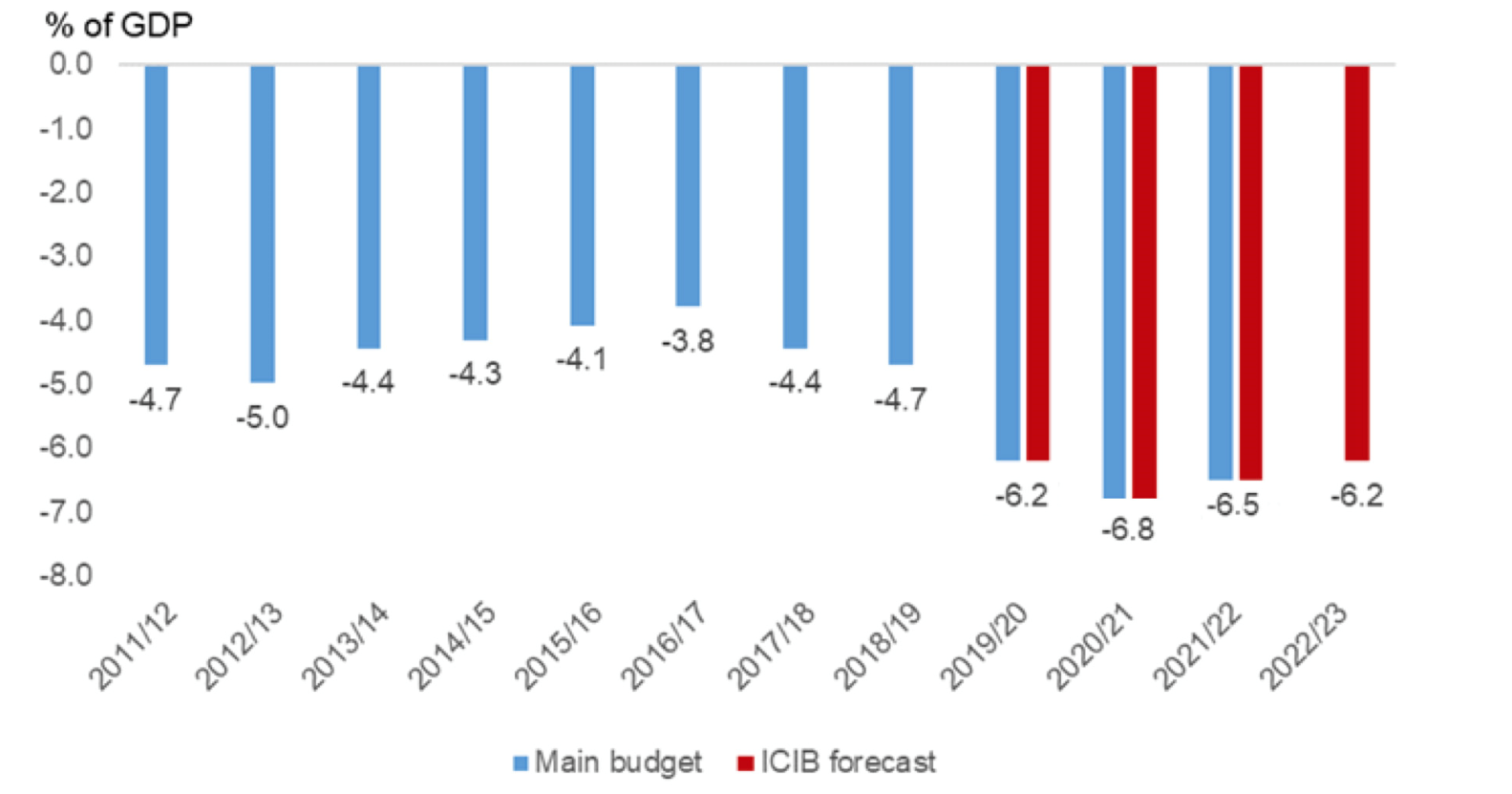

Lower nominal GDP and tax buoyancy forecasts: The persistent slowdown in nominal GDP growth and a decline in tax buoyancy have been the main reasons for the growing shortfall in revenue receipts, estimated to rise to R82bn in F20/21. The tax buoyancy assumptions for F19/20 and F20/21 have been reduced from 1.31 and 1.17 to 1.08 and 1.09. These are more reasonable and lowers the downside risk to the revenue forecast in the coming year. We think assumptions of a quick of turnaround at SARS have been moderated. Added to these is a more realistic nominal GDP forecast, averaging 6.1% over the MTEF period compared to the previous forecast of 7.4%.

Figure 2: Capacity for tax increases to stabilise the budget deficit has declined – Tax increase vs revenue shortfalls

Reducing the expenditure ceiling without reducing the compensation bill: The government’ emphasised its commitment to fiscal consolidation in the MTBPS by lowering the expenditure ceiling. In our MTBPS Preview, we added government’s financial assistance to Eskom. However, National Treasury deems the assistance as spending on financial assets, whereas the expenditure ceiling is comprised of non-interest spending excluding the skills development levy on the main budget. Spending cuts of approximately 1.4% of non-interest expenditure over the MTEF period has been announced with a reduction in municipal and provincial conditional grants, goods and services and capital spending. These measures help to contain real growth in non-interest spending by 0.5% p.a. compared to 1.4% when Eskom is included.

Guidelines to contain spending has been announced: These include salaries for Cabinet, premiers and MECs which could be adjusted downward; the cost of official cars will be capped at R700 000 VAT inclusive; a new cell phone dispensation will cap the amount claimable from the state; all domestic travel will be on economy class tickets; and payment for subsistence and travel for both domestic and international trips will be cancelled.

Lowering public compensation has not been factored into the

spending trajectory: In February, National Treasury penciled in a reduction in the wage bill of more than R20bn to be achieved through voluntary retrenchments. A slow uptake has resulted in the removal of this (totaling R20bn) in the expenditure forecast. Reducing the wage bill will now form part of broader discussions with trade unions of which more clarity could emerge in February 2020. Added to this is a fresh round of public sector wage negotiations that will kick off in 2020 for F21/22. The reconfiguration of government with a smaller cabinet, announced in the June 2019, and considerable overlap and duplication by the nearly 250 government departments, is progressing at a very slow pace.

Financial assistance to smaller SOEs: The growth in public sector debt has been contained in F19/20 mainly due to larger on-balance sheet government financial assistance. In F19/20, R13.0bn had been set aside in the contingency reserve for financial assistance to smaller SOE’s. Of this, R10.8bn has been transferred of which SAA received R5.5bn, SABC R3.2bn, Denel R1.8bn and SA Express R300m. SAA requires a further R9.2bn due to its inability to repay debt of R9.2bn guaranteed by the government. The Minister of Finance stated in the MTBPS speech that SAA “is unlikely ever to generate sufficient cash flow to sustain operations in its current configuration. Which then begs the question: how long are we going to be on the flight path? Forever? I think not”.

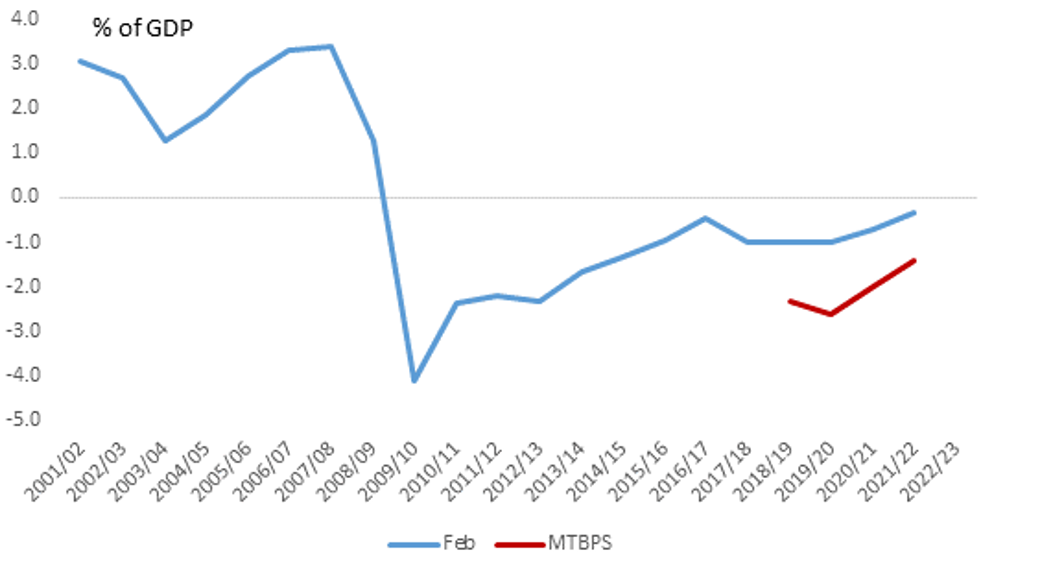

A target for reducing the primary deficit has been suggested to

stabilise the rising debt to GDP trajectory: The debt trajectory in the MTBPS rises to more than 80% of GDP in F26/27. A consolidation of the deficit on the primary deficit is critical and the MTEF forecast shows the deficit narrowing from 2.6% in F20/21 to 1.4% in F22/23. National Treasury has proposed a target for the primary balance of zero in F22/23 for non-interest spending and excluding financial assistance to Eskom. However, this is contingent on a reduction in spending of nearly R150bn and by implication, the compensation bill.

Figure 3: Primary deficit – Spending cuts needed to reduce the primary budget deficit in order for the rising debt trajectory to stabilise.

What to watch out for in November:

- President Ramaphosa’s new growth plan and the five-year Medium Term Strategic Framework;

- Moody’s rating review (1 November)

- Investment summit (5-7 November)

More detail is expected on the Infrastructure Fund and the pipeline of strategic projects.

Key topics

You may also be interested in

Fund Finance

Corporate Finance and Advisory

We are a leading corporate house with an international presence. Our sound advice across sectors will help you grow your business.

Corporate Borrowing

Fund Finance

Corporate Finance and Advisory

We are a leading corporate house with an international presence. Our sound advice across sectors will help you grow your business.

Corporate Borrowing

Browse further in