The ongoing conflict in the Red Sea and escalating tensions in the Middle East are making daily headlines across the globe. Let us not forget that the Transnet issues continue to negatively affect our economy. Geopolitical and trade tensions could well lead to unforeseen scenarios playing out and potentially disrupting global trade in one way or another.

We will continue to work very closely with all our partners and service providers, to ensure that all your shipments are delivered as efficiently as possible.

The impact of the following key factors needs to be continually assessed and considered:

- Equipment and capacity challenges

- Disruptive sailing schedules

- Red Sea situation and geopolitical landscape

- Transnet

- Rate increases

Sea freight update

The sea freight market continues to experience volatility and the situation in the Red Sea is creating further headaches for the market. However, the full impact of the situation has not been completely realised yet. It is estimated that 80% of containerships that transit through the Suez Canal for various trades have diverted their routings via the Cape of Good Hope. Not only does this impact their transit times, operations, and costs, but it also means that additional capacity and equipment is tied up in transit for longer. This is creating capacity and equipment imbalances which also leads to additional surcharges being implemented.

On the local front, Transnet’s port and rail operational performance remains a hindrance to our economy. There has been a slight improvement in terms of reducing the number of vessels at anchorage, but the vessel waiting times at anchorage and berthing delays are still not acceptable. It must be noted that the weather conditions have not be favourable the past few weeks and this has had an impact on the port operations. It will still take weeks if not months for the situation to improve.

Red Sea closure no benefit to SA

Denys Hobson talks to Moneyweb's Simon Brown about the issue of shipping companies avoiding the Red Sea, and whether there are opportunities locally or risks to supply chains.

Capacity:

The market is expecting an additional 2.83Mteu of newbuild container ship capacity to be delivered in 2024 in addition to the 2.34Mteu capacity added in 2023. Global capacity is clearly not an issue, however the current situation in the Red Sea, the pre-Chinese New Year shipping period and port congestion (c.5.8% of global fleet according to Marine Traffic) across numerous ports globally is creating an imbalance in capacity and equipment availability on various trades.

We anticipate that the imbalance will be rectified over time as carriers and shippers adjust to the current disruptions being experienced, but keeping in mind that should tensions in the Red Sea and Middle East region escalate, disruptions to global markets and trade routes could be severely impacted.

For the time being, the EU/Mediterranean-Asia trade is the most significantly impacted trade route, and the full impact is yet to be felt. Vessel bunching across EU and Asian ports can also be expected which may force carriers to re-route cargo or create bottlenecks at ports which could reduce equipment availability in multiple regions and hence have a direct impact on South African trade. Carriers will also be implementing blank sailings post the Chinese New Year as export volumes decline. Some carriers are fully booked up until the start of the Chinese New Year.

Sailing schedules:

Shipping lines continue to face challenges in maintaining their schedules, and the delays to vessel arrivals and departures across our South African ports have contributed to the erratic carrier lead times and routings on all trade routes servicing South Africa. Severe weather conditions in Central and North China have also disrupted vessel schedules on the South African trade route. Feeder services across the Asia market have also been impacted and in cases resulted in transshipment delays.

Port operations in Port Louis, Mauritius were also recently affected by Cyclone Belal. This will affect transit times for cargo originating in Mauritius or transiting via Port Louis to South Africa. The number of vessels at anchorage changes daily. Durban port has seen the biggest decline in terms of number of vessels at anchorage and the average number of days at anchorage fluctuates between 7-14 days across the container terminals.

Cape Town port has experienced an increase in the number of vessels at anchorage with the average waiting time between 5-10 days.

Coega is less congested and waiting times for vessels at anchorage is down to two to three days on average. Vessel discharging and container upliftment from terminals is still taking longer than expected across all ports which is adding an extra three to seven days to the total lead time.

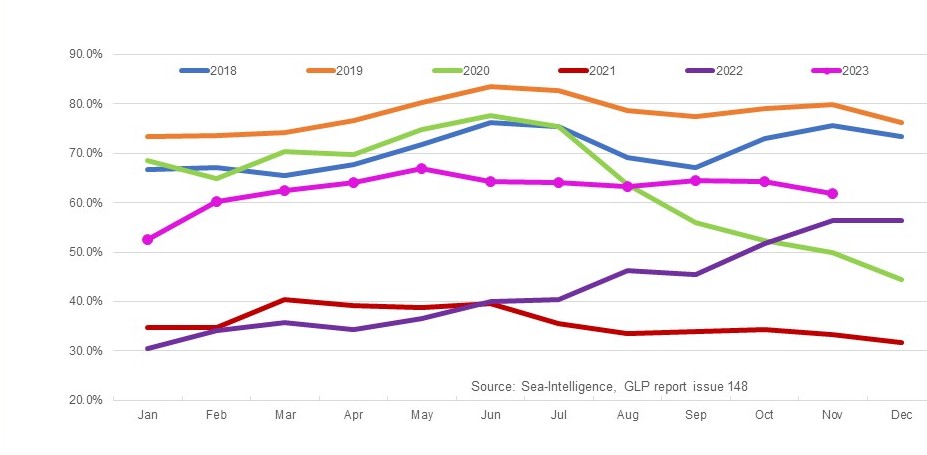

Global schedule reliability declined at 61.9% according to the latest Sea-Intelligence report. The average delays for late vessel arrivals increased slightly to 5.02 days. We expect schedule reliability to decline further in the coming weeks.

See graphs below.

Figure 1: Global Schedule Reliability

Figure 2: Global Average Delays for Late Vessel Arrivals

Freight rates:

Rate levels have increased on the Far East trade to South Africa as expected. We anticipate rates to soften post the Chinese New Year period. Our rates from Europe to South Africa have decreased since December 2023. Shipping lines have kept their port congestion surcharges into South Africa and these will remain in place while shipping lines still battle with congestion across the South African ports. Carriers could possibly increase local landside charges such as container turn-in fees because of the impacts caused by Transnet’s operational constraints.

Air freight update

The market has remained relatively stable with a few disruption reports over the past few weeks. Unfavourable weather conditions across Europe for example caused disruptions to flight schedules and carrier operations.

There has yet to be a significant impact on the airfreight market following the attacks on vessels in the Red Sea region and subsequent sea freight capacity constraints and longer voyages for trades impacted by this. The market is expecting that the effects of the Red Sea situation on global trade will soon spill over into the airfreight market and with this demand for airfreight will increase as so will rate levels.

Transit times:

There have been delays to cargo moving from Europe because of severe weather conditions. In general service levels and lead times remain consistent. The picture could change should demand for airfreight pick up dramatically because of disruptions to the sea freight market.

We are encouraging clients to provide their required arrival dates in advance for us to offer optimal routings and rates to meet their requirements.

Freight rates:

Spot rates have increased on the Asia trades with the pre-Chinese New Year rush. One would have expected freight rates to increase across other trades as well, but sufficient available market capacity has meant that rate levels remained relatively flat. Fuel prices could increase with the current conflicts in the Middle East, and this will push freight rates higher.

As your logistics partner, we remain fully committed to offering you import solutions that support your business needs. We have a strong international network for both air and sea modes which we leverage to ensure that we continue to offer you the best viable solutions for your business. We are aware that current market conditions are volatile and challenging, and we remain dedicated to serving and working with you during these times.

Partner with Investec

Optimise your import business with an end-to-end logistics and inventory finance solution.

As your logistics partner, we remain fully committed to offering you import solutions that support your business needs. We have a strong international network for both air and sea modes which we leverage to ensure that we continue to offer you the best viable solutions for your business. We are aware that current market conditions are volatile and challenging, and we remain dedicated to serving and working with you during these times.

Comprehensive offerings to support your business growth

Our working capital finance is designed to boost and free up cash for optimising or growing your business. We offer a number of tailored financing solutions to suit your business needs.

We provide financing for the purchase of stock and services on terms that closely align with your working capital cycle. For importers, our fully integrated solution provides a single point of contact for the end-to-end management of your imports, including order tracking, the hedging of foreign exchange risk, the physical supply of product, and the provision of a consolidated landed cost per item on delivery.

Funding the needs of your business by leveraging your balance sheet (debtors, stock, and other assets) to provide you niche asset-based lending or longer-term growth funding to assist you in growing your business and creating shareholder value.

Niche funding for the purchase of the productive assets and other capital requirements needed to grow your business. We alleviate the requirement for the upfront capital investment in these assets.

Browse further in