Following mass layoffs during the Covid-19 pandemic, both the global aviation and shipping industry are struggling to recruit enough staff to cope with increased consumer and traveller demand, particularly over the summer holiday season in Europe and the US.

In the air freight industry, the resultant flight cancellations and endless passenger queues have sparked travel chaos across Europe as holidaymakers seek to make up for lost time. Labour shortages are also wreaking havoc in the sea freight industry, and several European ports are grappling with strike action that’s causing serious bottlenecks.

Sea freight update

The sea freight market continues to be hampered in various forms which pushes the time frame out for a return to stability. Labour shortages and strike action in countries such as Germany and Belgium for example have reduced operational capacity and efficiency within the region. This has caused bottlenecks for cargo handling facilities, trucking and rail services as well as impeded on the carriers’ ability to offer reliable services.

Importers on the Far East trade have reason to smile as rate levels continue to gradually decline. Demand for capacity has not been as strong as anticipated post the lifting of the strict China Covid lockdown regulations. Some regulations remain in place which is still affecting trucking services in parts of China as well as cross-border movements between China and Hong Kong.

The USA, South America and Middle East trades remain a headache. A lack of capacity and schedule reliability continue to cause shipments to be delayed and lead times are very inconsistent.

Labour negotiations between the relevant stakeholders for the USA West Coast shipping ports have not been concluded yet and there is a commitment not to stop operations at this point. Similarly in Germany, a contract agreement has also not been reached yet between the German port employers and the German labour union.

Capacity

Capacity availability from Europe is the most constrained and carriers have been experiencing strong demand for automotive and chemical products. Most carriers are fully booked weeks in advance with very limited spot capacity available. A higher number of port omissions due to congestion has also contributed to the capacity pressures.

Capacity availability from China and South-East Asia is relatively stable at this stage and demand forecasts for the rest of July. We do expect demand to increase through August and September as we approach the Chinese Golden Week beginning of October.

The USA East Coast trade has been affected by port congestion due to the shift in outbound and inbound cargo movements from the West Coast. Inland trucking and rail bottlenecks have delayed cargo movements to the ports resulting in bookings not being utilised and therefore creating a roll-over pool for future sailings. The booking lead time has extended with some carriers being fully booked for four weeks in advance.

Port congestion around the globe continues to be a major driving force in capacity being tied up.

We encourage bookings to be made well in advance of the required shipment dates and factor in longer lead times.

Despite the challenging environment, we have, in general, managed to consistently secure space through our extensive global network. With our expanded global network, we have gained access to additional capacity which strengthens our service offering to our clients.

Equipment imbalance

There are pockets of equipment shortages in areas of Europe, India and at times in parts of China. The biggest challenge facing carriers is their ability to reposition equipment to container yards due to the trucking capacity being impeded.

Sailing schedules

Global scheduling reliability has improved ever so slightly but remains below 40%. The European trade has been the most unstable in recent times and we have seen some carriers making frequent changes to their schedules. Vessel berthing delays and transshipments remain an issue. Vessel sailings have also been delayed on the Far East trade due to severe weather conditions. We can expect further delays as we approach the typhoon season.

Cape Town port continues to experience a high number of omissions, especially on the European trade. Booking time sensitive cargo to Coega instead of Cape Town is an alternative option on both the USA and European trades.

Freight rates

The elevated fuel prices have pushed both trucking and freight rates upwards most trades. Capacity constraints have driven market rates up on the European and South America trades. Middle East and Turkey rates also remain elevated, and the majority of bookings are only accepted on a spot basis.

Rate levels have softened on the Far East trade and there is likely to be further softening of rates for the second half of July. Should demand start picking up again for August then we can expect carriers to push through increases.

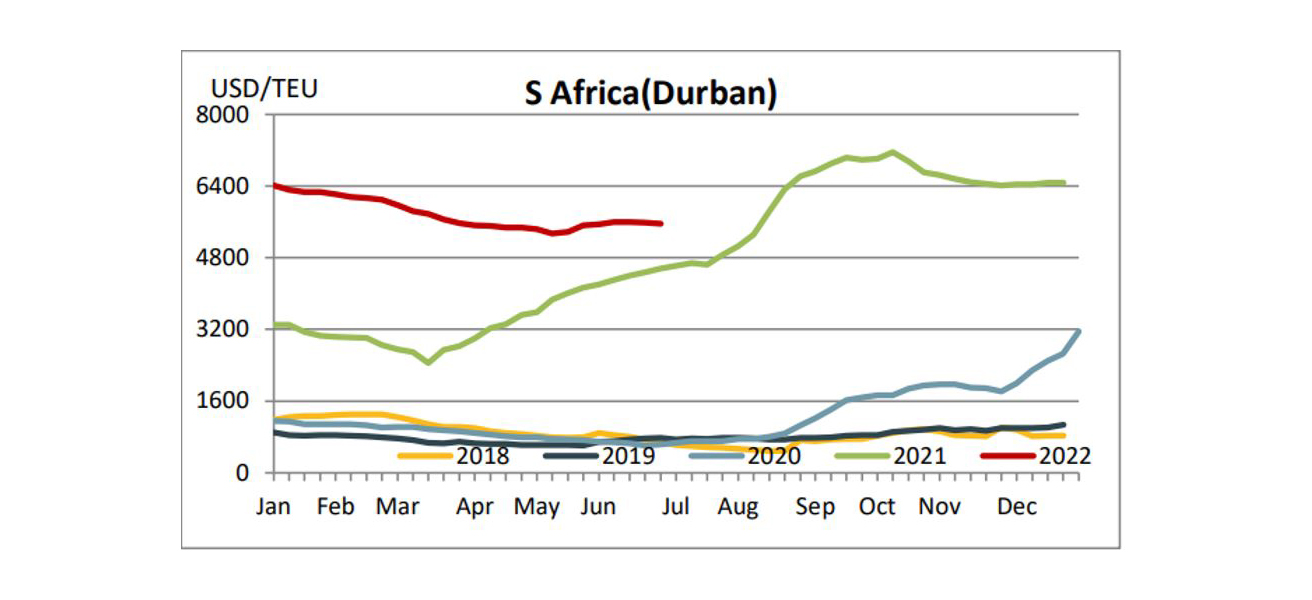

SCFI (Shanghai Container Freight Index)

The below graph demonstrates the freight rate movement per TEU ex-China to South Africa

Chinese Golden Week

The Chinese Golden Week takes place from 1-7 October 2022. We anticipate demand for capacity to increase in the weeks leading up the Golden Week. Carriers are likely to implement blank sailings in the first one to two weeks post Golden Week which will reduce capacity on this trade for the month of October. Bookings need to be made in advance to ensure orders ship on time.

Air freight market update

The airfreight markets for the USA and Europe are battling with labour shortages and a significant number of flights have been cancelled. Air Cargo News recently published this article highlighting the reasons behind the flight cancellations. Schiphol and Heathrow have also been battling with disruptions.

Passenger demand typically increases around this time of the year as the USA and European countries enter their summer holiday period. This tends to impact airlines available cargo capacity as preference is given to passenger cargo.

Capacity

The situation is relatively stable on the Far East trade. Cargo handling and trucking services have improved, but there is still pressure on trucking capacity from South China into Hong Kong which has resulted in cargo movement delays.

We expect disruption to capacity because of the high number of flight cancellations within the European trade. Freighter capacity from the USA remains a challenge with cargo being routed via Europe or the Middle East.

Our airfreight network enables us to continue offering flexible solutions that meet our clients’ import requirements.

Transit times

Some airlines are struggling with reliability and lead times will be extended with the current labour and trucking constraints, and the high number of flight cancellations.

We encourage you to provide your required arrival dates in advance for us to offer you optimal routings and rates to meet your requirements.

Freight rates

Rates remain at elevated levels with airline fuel surcharges and increasing handling and trucking costs driving total costs upwards. The weakening of the Rand is also adding to landed costs increasing.

With our expanded network we are well positioned to offer a variety of options to meet our clients airfreight requirements.

Get Focus insights straight to your inbox

Comprehensive offerings to support your business growth

Our working capital finance is designed to boost and free up cash for optimising or growing your business. We offer a number of tailored financing solutions to suit your business needs.

We provide financing for the purchase of stock and services on terms that closely align with your working capital cycle. For importers, our fully integrated solution provides a single point of contact for the end-to-end management of your imports, including order tracking, the hedging of foreign exchange risk, the physical supply of product, and the provision of a consolidated landed cost per item on delivery.

Funding the needs of your business by leveraging your balance sheet (debtors, stock, and other assets) to provide you niche asset-based lending or longer-term growth funding to assist you in growing your business and creating shareholder value.

Niche funding for the purchase of the productive assets and other capital requirements needed to grow your business. We alleviate the requirement for the upfront capital investment in these assets.

Browse further in