Global Economic Overview – July 2024

Global markets watch inflation dynamics as more central banks ease policy. Despite cooling global price pressures, there are still risks to inflation, such as rising food prices and elevated shipping costs. Economies, except for China, remain resilient to higher interest rates.

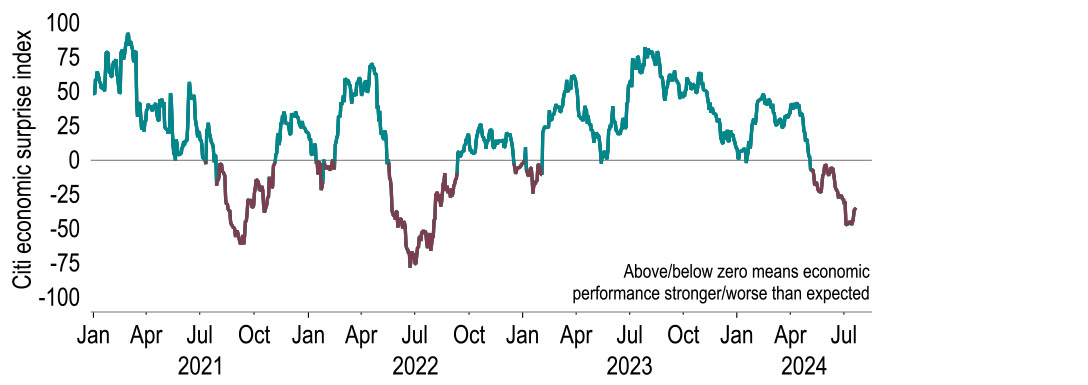

Outside of political developments, global markets are still attentive to inflation dynamics as a greater number of central banks transition towards policy easing. Although global price pressures have cooled, there are still upside risks to the inflation outlook, such as from rising food prices as extreme weather hits harvests and elevated shipping costs. But broadly, economies continue to be resilient to the higher level of interest rates – China is an exception to this where interest rates are low, yet the economy is struggling. Our global growth forecasts remain at 3.2% for 2024 and a touch lower for 2025, also at 3.2%.

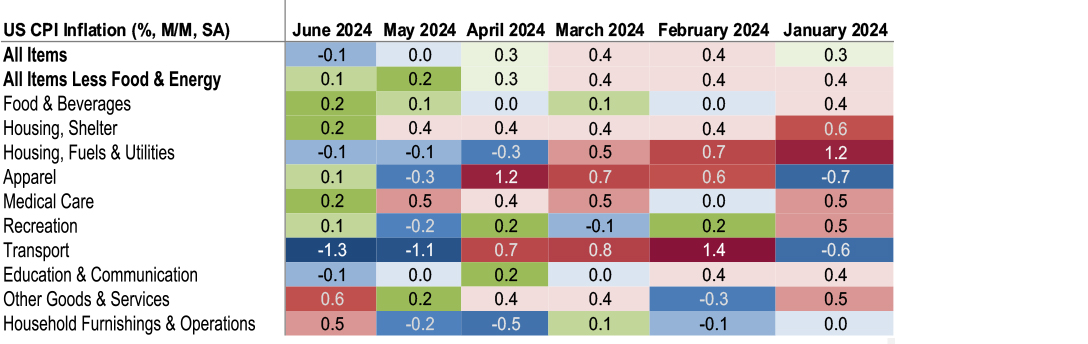

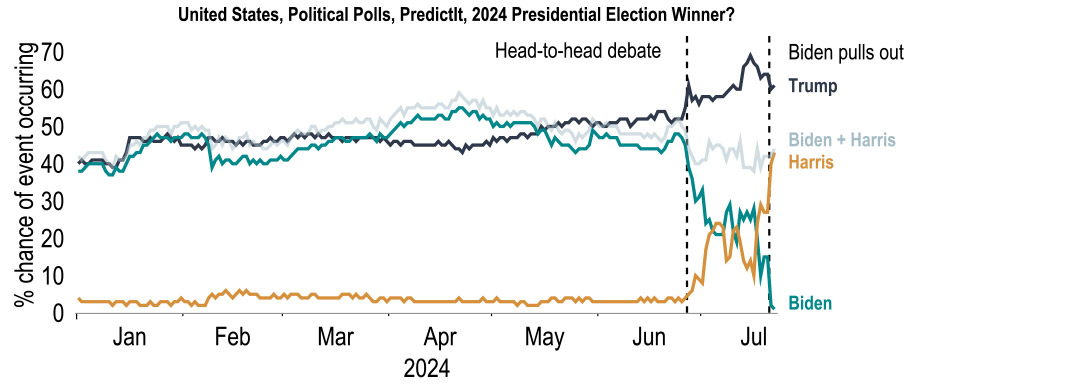

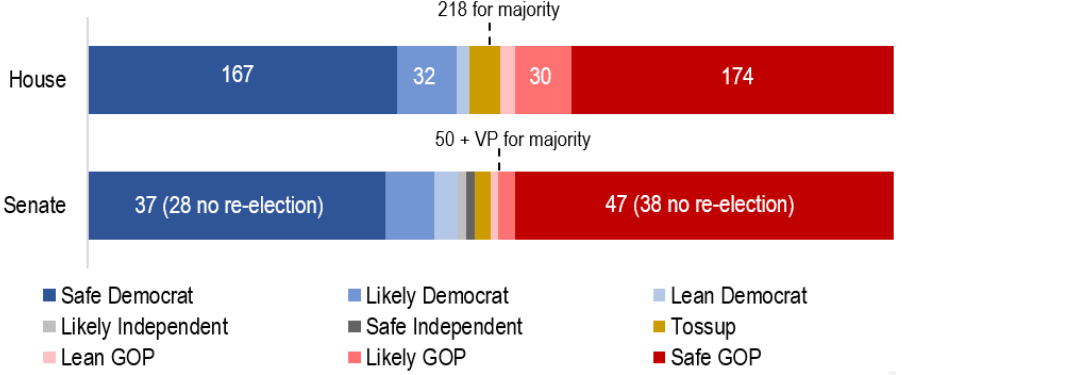

Political developments have overshadowed macro news in the US in recent weeks. Current VP Kamala Harris looks set to be the Democratic nominee to take on former President Trump on 5 November. With polls currently pointing to a tight race between the pair, given the uncertainty we are conditioning our forecasts on an unchanged policy stance post-election for now. However, considering the range of potential outcomes (regarding both the Presidency and the make-up of Congress) there are wide risks to these forecasts. From a monetary policy perspective, we maintain our call that the Fed will first cut rates in September, with recent CPI data supporting that position. A Trump presidency and a clean sweep of Congress could result in a higher rate profile moving forward though if Mr Trump enacts fiscally expansive and protectionist policies.

July’s ECB meeting saw policy kept on hold following its first rate cut in five years in June. As to future policy easing, September’s meeting has been described as ‘wide open’ and is our base case assumption for a second cut in rates, whilst our end year Deposit rate forecasts stand at 3.25% (2024) and 2.25% (2025). Much will depend on the data, and whilst we note that some wage readings have moved higher, this does not necessarily preclude further interest rate cuts given that elevated wage growth this year is already embedded in the ECB’s baseline scenario. As for the economy, we expect a recovery this year driven by an improving household income backdrop, but we are also encouraged by some signs that credit conditions are improving. This should help boost investment, which has been depressed in recent years. Our 2024 and 2025 GDP forecasts stand at 0.7% and 1.6%.

Attention has swung towards what the new Labour government will do with its huge majority. We do not yet know its precise fiscal rules or the date of the Budget, but we still judge that modest tax rises will be necessary in the short-term to fund higher spending commitments. We doubt that this will shift the dial on the monetary policy outlook. Longer-term its key aim is to raise GDP growth to 2.5% p.a., possibly initially by getting people back into the workforce, then by raising labour productivity growth. The UK has been something of a pariah in recent years and if the government is anywhere near successful in delivering higher growth, this could benefit various UK asset classes, including equities. We have therefore upgraded our view of sterling, which we now expect to rally to $1.32 by end-year and $1.35 by end-2025.

For more information contact our economists

Philip Shaw

Chief Economist

I head up the Economics team for Investec in London after joining in 1997. I am a regular commentator on the economy and financial markets in the press and on TV. I graduated with an Economics degree from Bath University and a master’s in Econometrics from the University of Manchester. I started my career in the Government Economic Service at the Department of Energy before joining Barclays as an economist/econometrician.

Ryan Djajasaputra

Economist

In 2007, I joined Investec as part of the Kensington acquisition, before joining the Economics team in 2010. I provide macroeconomic, interest rate and foreign exchange analysis to Investec Group and its corporate clients. After graduating with a Bachelor’s degree in Economics from UWE Bristol.

Lottie Gosling

Economist

I joined the London Economics team at Investec as a graduate in September 2023. I graduated with a Bachelor’s degree in Economics from the University of Bath with a year-long placement working as an Economic Research Analyst at HSBC.

Ellie Henderson

Economist

I joined Investec in February 2021 as part of the London Economics team, providing economic advice and analysis for the company and its clients. Before joining Investec I worked as an economist for Fathom Consulting, where I predominantly focused on China research. I hold a Bachelor’s degree in Economics from the University of Surrey, as well as a Master’s degree in Economics from Birkbeck, University of London.

Sandra Horsfield

Economist

I am part of the London Economics team, having joined in 2020, providing macroeconomic analysis and advice to the Investec Group and its clients. I hold a Bachelor’s and a Master’s degree in Economics, both from the London School of Economics. I have over 20 years’ experience as a financial markets economist on the buy and sell side as well as in consulting.

Philip Shaw

Chief Economist

I head up the Economics team for Investec in London after joining in 1997. I am a regular commentator on the economy and financial markets in the press and on TV. I graduated with an Economics degree from Bath University and a master’s in Econometrics from the University of Manchester. I started my career in the Government Economic Service at the Department of Energy before joining Barclays as an economist/econometrician.

Ryan Djajasaputra

Economist

In 2007, I joined Investec as part of the Kensington acquisition, before joining the Economics team in 2010. I provide macroeconomic, interest rate and foreign exchange analysis to Investec Group and its corporate clients. After graduating with a Bachelor’s degree in Economics from UWE Bristol.

Lottie Gosling

Economist

I joined the London Economics team at Investec as a graduate in September 2023. I graduated with a Bachelor’s degree in Economics from the University of Bath with a year-long placement working as an Economic Research Analyst at HSBC.

Ellie Henderson

Economist

I joined Investec in February 2021 as part of the London Economics team, providing economic advice and analysis for the company and its clients. Before joining Investec I worked as an economist for Fathom Consulting, where I predominantly focused on China research. I hold a Bachelor’s degree in Economics from the University of Surrey, as well as a Master’s degree in Economics from Birkbeck, University of London.

Sandra Horsfield

Economist

I am part of the London Economics team, having joined in 2020, providing macroeconomic analysis and advice to the Investec Group and its clients. I hold a Bachelor’s and a Master’s degree in Economics, both from the London School of Economics. I have over 20 years’ experience as a financial markets economist on the buy and sell side as well as in consulting.

Get more FX market insights

Stay up to date with our FX insights hub, where our dedicated experts help provide the knowledge to navigate the currency markets.

Browse articles in

Please note: the content on this page is provided for information purposes only and should not be construed as an offer, or a solicitation of an offer, to buy or sell financial instruments. This content does not constitute a personal recommendation and is not investment advice.