27 Apr 2022

Aviation Market Snapshot - Q1 2022

Market insights

-

Steady, but still non-linear global recovery

The demand recovery of 2021 has continued into the first quarter of 2022, with positive trends emerging across most regions. The strong economic growth forecast in 2022 is anticipated to drive further air traffic recovery. Governments have growing faith in Covid-19 vaccinations, which has resulted in the progressive relaxation or elimination of travel restrictions in many markets. This also entails that Omicron-related flight cancellations have become less prevalent, and industry optimism has further increased. Bouncing back to pre-pandemic levels of global traffic by 2023-24 feels a more achievable target than it did six months ago (and that target was already an improvement on previous projections, which had looked towards a 2024-25 recovery horizon).

In terms of regional differences, North Atlantic and intra-European markets continue to strengthen and improve the recovery pattern. However, demand in Asia keeps lagging due to strict Covid-related government policies, in particular China which is showing no sign of altering its severe border policies. Airlines in most regions have been faced with the short-term challenges of Omicron’s impact on their workforce, with longer-term challenges including increasing staff levels across the industry. In the US, for instance, airlines are already being forced to pare back capacity expansion due to staff shortages (Delta Airlines and United Airlines).

-

Impact to aviation of sanctions and war in Ukraine

Sanctions targeting the Russian economy and its commercial aviation sector entail that Western aircraft leases be terminated by 28 March 2022. At the start of the conflict there were 980 aircraft in the Russian fleet, of which 515 were leased from international lessors. Lessors have so far repossessed circa 70 aircraft at airports outside Russia. Several Russian airlines, including Aeroflot and S7, have halted international flights to avoid seizure of their airplanes. Given that only a limited number of the leased aircraft are likely to be available in the near-future, the impact on lease rates and values is likely to be limited. Apart from the loss of the Russian market to place aircraft in, only a limited number of the leased aircraft are likely to be made available in the short term, with a similar number of OEM aircraft on order to airlines in the region that will need re-placing in the next 18 months.

-

Europe in particular is nearing pre-pandemic levels of flying on the back of pent-up demand

In European markets, success stories include Ryanair, which carried more passengers in March 2022 than pre-pandemic (the first time that a major European airline has done so) with predicted load factors returning to 90% by June 2022. Data from IATA and Eurocontrol show a growing recovery in Europe as a whole, which is approaching pre-pandemic levels of capacity and demand. Also positive is that the risk of another Covid variant or crisis is no longer hampering airlines from gearing up for the summer. Europe’s largest airlines, including EasyJet, IAG, Lufthansa and Ryanair, plan to fly at or near their pre-pandemic European capacity peak during the summer.

There are some caveats, nonetheless, when analysing the aviation recovery in Europe. Despite the optimism, long-haul travel, particularly to Asia, remains below pre-pandemic levels. The Ukraine war and higher energy prices are likely to have a medium-term negative impact. Sector-wide issues will emerge if the conflict rises energy prices to a level at which they affect consumers’ purchasing power and raise airlines’ fuel costs.

Derek Wong, Head of Aviation Debt Fund

“As travel restrictions continue to ease in the key US and European markets, consumer spending is shifting from goods to experiences including travel. Coping with the resurgent demand is becoming a challenge for some airlines, airports and related infrastructure. As new aircraft deliveries and lessor trading pick up momentum, demand for debt financing will grow across the aircraft age spectrum. Aircraft backed debt is an attractive space to deploy capital and Investec continues to structure transactions that provide a premium in risk adjusted returns.”

Trends

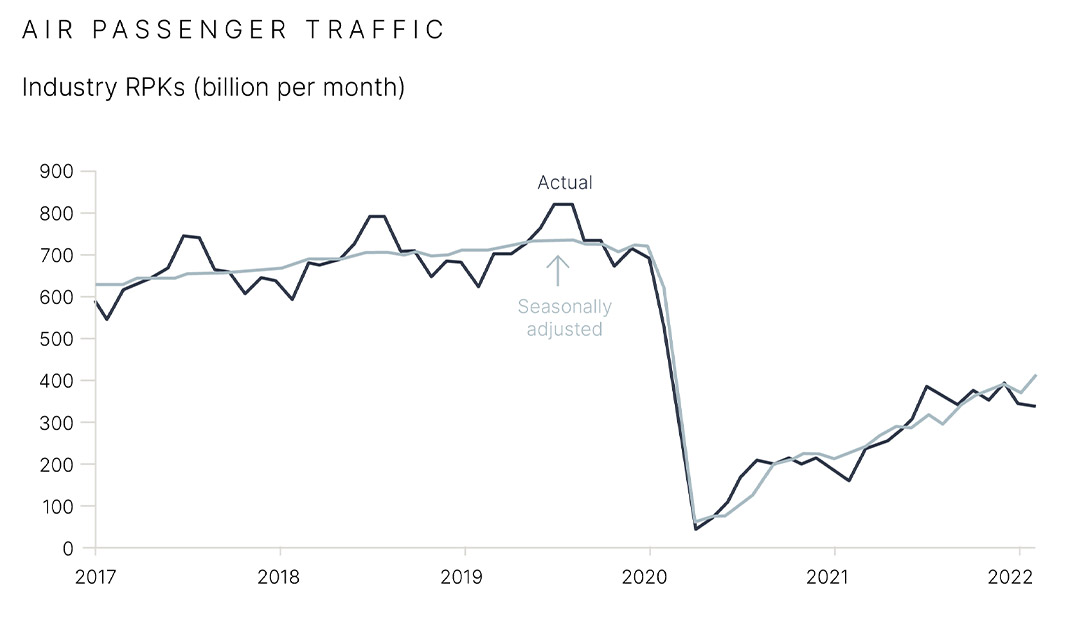

Global air travel continued to recover in February, with Omicron proving less of a burden on countries outside of Asia and the war in Ukraine not having had a major impact of global air traffic data to date. According to IATA reports, air traffic, as measured by Revenue Passenger Kilometres (RPKs), an indicator of global passenger demand, grew by 115.9% YoY, but were only 54.5% of the levels seen pre-pandemic in February 2019.

Sources: IATA Economics, IATA Monthly Statistics

Domestic air travel has seen RPKs move up 60.7% YoY in February, 78.2% of pre-pandemic levels in February 2019. The performance of key domestic markets was mixed across regions. In the US, RPKs were 112.5% above February 2021 and only 6.6% below February 2019 levels. Australia continues its upwards trajectory albeit from a low base. Japan has been negatively impacted by the spread of Omicron and government advice to limit travel, resulting in RPKs only 35.1% above February 2021. Domestic Chinese RPKs are due to drop in March following localised lock-downs and travel restrictions to contain Covid outbreaks.

International air travel recovery continues to gather momentum, driven by growing vaccination rates and a relaxation of travel restrictions in many regions. RPKs rose 256.8% YoY in February, but are only 40.4% of pre-pandemic February 2019.

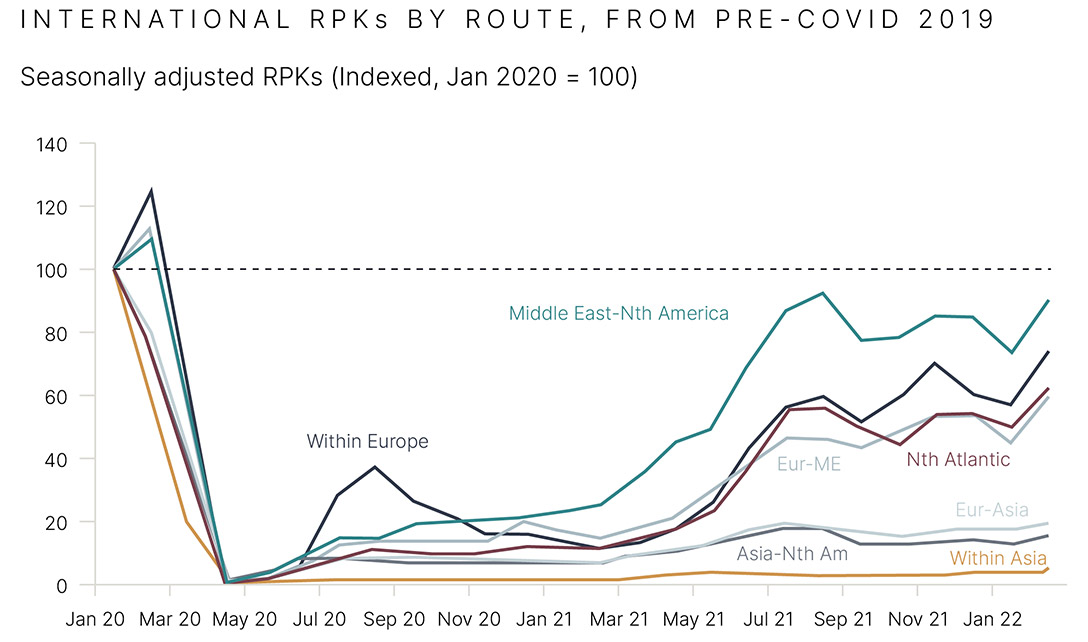

Regionally, European airlines performed best YoY, as the impact of the war in Ukraine has been relatively limited so far outside of Russia and countries neighbouring the conflict. Ticket sales suggest the fall in customer confidence was modest and rebounded quickly. Latin America, North America and the Middle East all posted significant gains YoY. In Asia the recovery remains slow, with RPKs 88% below February 2019 levels. The recent news of easing travel restrictions in many countries in the region (South Korea, Vietnam, Thailand, Singapore, New Zealand etc.) is positive.

Source: IATA Economics, IATA Monthly Statistics by Route

IATA noted a more optimistic outlook for air travel after 2 years of severe Covid-related disruptions. Global Covid infections have declined and hospitalisation rates remain low, which has alleviated the strain on economies and healthcare. More countries have started to ease international travel restrictions, including some in the long closed Asia Pacific region. Bookings have rebounded quickly when restrictions have lifted. However, the China market has soften following localised lockdowns and travel restrictions.

Asia is gradually reopening after two years of some of the world’s toughest travel restrictions. Singapore is the latest country to relax its Covid protocols, from 1st April, fully vaccinated passengers will not need to take a test on entering Singapore, nor will they be required to quarantine. However, passenger pre-departure tests are still required. Unvaccinated passengers can transit through Singapore as long as they meet the entry requirements of their destination country.

The war in Ukraine, rising inflationary pressures and increases in jet fuel costs will negatively affect the recovery. Ukraine and Russia accounted for 0.8% and 1.3% of global air traffic respectively. The closure of Russian airspace to European and US carriers will lead to delays, expensive re-routing and cancellations. However, the significance of Europe-Asia and North America-Asia diminished during the pandemic due to boarder closures in Asia.

Pre the Russia-Ukraine war the IMF forecast global GDP growth of 4.4%. IATA forecasts a ~1% reduction in GDP growth because of the war. Russia and Ukraine are both large exporters of energy, precious metals, wheat, and other commodities, however combined they account for less than 2% of global GDP. Most major economies have only limited trade exposure to Russia (US 0.5%, China 2.4%).

Rising jet fuel prices are increasing pressure on fuel costs coupled with additional challenges from rising infrastructure costs and staff shortages in the US. During 2021, jet fuel increased 68% YoY, as demand increased with easing lockdowns while OPEC supply remained constrained. In the US airlines are optimistic ahead of the Northern hemisphere summer that strong pent-up demand will enable them to pass on increases in fuel costs to the consumer without impacting demand. European airlines are utilising hedging strategies and increasing fares via fuel surcharges on long-haul flights.

Kroll Bond Rating Agency (KBRA) reported in the quarter, that whilst aircraft lessors’ revenues remain under pressure there were strong signs of improvement in 2021 as the sector started to recover from the worst effects of the pandemic. KBRA noted that airline rent-deferral requests fell in 2021, cash collection rates improved and the Asset-Backed Securitisation market returned at speed with $9.2 billion of issuances in 2021. KBRA ‘remains cautious’ on airlines short to medium-term credit fundamentals, but notes that lessors continued to absorb the remaining disruptions to cash flow through their strong liquidity and access to capital markets. During 2021, lessors issued $35 billion of senior unsecured bonds up from $25 billion the previous year, and there was a significant rise in non-bank lending to airlines and lessors.

During the quarter, Airbus reported that it expects to deliver 720 aircraft, up from 611 in 2021. Airbus acknowledged that bottlenecks affected production in 2021 and that a tight labour market, snarled logistics and an increasing cost of raw materials would affect 2022. To achieve the goal, production rates will be raised across the board. The biggest and most challenging ramp-up will be for the A320 family, planned to rise to 65 aircraft per month by the middle of next year. To help achieve this, the company is making all its production sites capable of assembling the A320. At 31 December 2021, Airbus’s backlog stood at more than 7,000 aircraft (10 years of production at current rates).

Air cargo’s long growth run slowed in January impacted by Omicron affecting crew scheduling and operations. The war in Ukraine poses a greater threat, with the closure of Russian airspace to airlines from most of Europe and North America. Re-routing is causing longer flight times and coupled with increasing fuel prices is effecting the economic viability of certain routes. However, shipping too is being affected by the war with reports of ships stuck at anchor as Russian and Ukrainian sailors leaving their posts and delays at ports as the content of containers are checked for goods defying sanctions. Russian and Ukrainian seafarers make up 14.5% of the global shipping workforce (International Chamber of Shipping Feb-2022).

How has the market responded?

- During the quarter, IATA reported that the Global Airline share price index started 2022 positively, rising 5.8% to mid-January driven by investor confidence that the Omicron variant will result in fewer hospitalisations and less disruptions to previous variants. Nevertheless, the airline stock index remains ~30% below pre-crisis levels.

- The war in Ukraine has dampened activity by both issuers and investors in the capital markets. Across the existing aircraft lessor ABS market, there are 30 transactions with exposure to Russian or Ukraine. The majority of the exposure is to Aeroflot and Rossiya, in addition to regional carriers such as Ural and S7. While aircraft in Ukraine are being taken out of the country, the Russian aircraft may prove very difficult to recover and could significantly impact the value of transactions with higher exposure levels.

- In April, the Portuguese government announced that it plans to inject a further EUR990m into flag carrier TAP in 2022. The funds are part of the airline’s EUR3.2bn rescue package approved by the EU in 2020. The airline received EUR1.2bn of public funds in 2020 and a further EUR998m in 2021.

- In April, Lufthansa Group announced that it has boosted its liquidity with a EUR2bn revolving credit facility. The facility, which will be available for three years with two one-year extension options, is unsecured and provided by a syndicate of international banks. It replaces existing bilateral credit lines of ~EUR0.7bn, thereby increasing the airline’s potential liquidity by EUR1.3bn.

- Recent debt capital market deals, include:

- 22 February, Vietjet Air priced VND3.0tn notes due in 2025. The issuance has a coupon of 3.500% and is unrated.

- 18 February, China Aircraft Leasing Group (CALC) priced RMB1.2bn notes due in 2024. The private placement issuance has a coupon of 4.400%.

- 13 January, Wizz Air priced €500m notes due in 2028. The issuance has a coupon of 1.000% and rated BBB- and Baa3 by Fitch and Moody’s respectively.

- 11 January, Singapore Airlines priced $600m notes due in 2029. The issuance has a coupon of 3.375% and is unrated.

- Whilst capital market activity has slowed, we expect airlines and lessors to return in due course, especially for issuers located in those areas recovering quicker from the impact of Covid and unaffected by the war. We expect the bifurcation of the market to continue with spreads staying low for strong carriers and significantly above pre-Covid levels for the rest of the market.

Investec Aviation Debt Funds

$5 bl

7-year

25+ people

Strong alignment of interest

Proven track record

Find out more about Aviation finance from Investec

Investec co-invests in all managed platforms, with strong technical capabilities and a proven track record in originating, releasing and remarketing aircraft.

Disclaimer

This presentation and any attachments (including any e-mail that accompanies it) (together “this presentation”) is for general information only and is the property of Investec Bank plc (“Investec”). It is of a confidential nature and all information disclosed herein should be treated accordingly.

Making this presentation available in no circumstances whatsoever implies the existence of an offer or commitment or contract by or with Investec, or any of its affiliated entities, or any of its or their respective subsidiaries, directors, officers, representatives, employees, advisers or agents (“Affiliates”) for any purpose.

This presentation as well as any other related documents or information do not purport to be all inclusive or to contain all the information that you may need. There is no obligation of any kind on Investec or its Affiliates to update this presentation. No representation or warranty, express or implied, is or will be made in relation to, and no responsibility or liability is or will be accepted by Investec or its Affiliates as to, or in relation to, the accuracy, reliability, or completeness of any information contained in this presentation and Investec (for itself and on behalf of its Affiliates) hereby expressly disclaims any and all responsibility or liability (other than in respect of a fraudulent misrepresentation) for the accuracy, reliability and completeness of such information. All projections, estimations, forecasts, budgets and the like in this presentation are illustrative exercises involving significant elements of judgement and analysis and using the assumptions described herein, which assumptions, judgements and analyses may or may not prove to be correct. The actual outcome may be materially affected by changes in e.g. economic and/or other circumstances. Therefore, in particular, but without prejudice to the generality of the foregoing, no representation or warranty is given as to the achievability or reasonableness or any projection of the future, budgets, forecasts, management targets or estimates, prospects or returns. You should not do anything (including entry into any transaction of any kind) or forebear to do anything on the basis of this presentation. Before entering into any arrangement, commitment or transaction you should take steps to ensure that you understand the transaction and have made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances, including the possible risks and benefits of entering into such a transaction. No information, representations or opinions set out or expressed in this presentation will form the basis of any contract. You will have been required to acknowledge in an engagement letter, or will be required to acknowledge in any eventual engagement letter, (as applicable) that you have not relied on or been induced to enter into engaging Investec by any representation or warranty, except as expressly provided in such engagement letter. Investec expressly reserve the right, without giving reasons therefore, at any time and in any respect, to amend or terminate discussions with you without prior notice and disclaim hereby expressly any liability for any losses, costs or expenses incurred by that client.

Investec Bank plc whose registered office is at 30 Gresham Street, London EC2V 7QP is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority, registered no.172330.