14 Jul 2023

Aviation Market Snapshot - Q2 2023

- Domestic air traffic exceeds pre-pandemic levels

- Post-pandemic airline consolidation in Europe

- Aircraft orders at Paris Air Show increase production backlog

China’s reopening boosts domestic aviation and gives the global air-passenger market a lift

Key market insights

Domestic air traffic exceeds pre-pandemic levels

Following the gradual lifting of travel restrictions in China in January 2023, domestic capacity has increased and passenger numbers have also risen. In April, both Chinese domestic ASKs and RPKs exceeded pre-pandemic levels, with the growth forecast to continue. In turn, this enabled the global domestic air passenger market to exceed pre-pandemic levels by ~3% in April.

Europe sees post-pandemic airline consolidation

The impact of the global pandemic on the financial health of airlines has affected regional competition and encouraged consolidation. In Europe in February, IAG agreed a €400m deal for Air Europa, pending anti-trust approval. In May, the Lufthansa Group announced that it had reached agreement – subject to regulatory approvals – to acquire a 41% stake in Italy’s ITA Airways for €325m, with an option to buy the remaining shares at a later date.

TAP Portugal is another big acquisition target in Europe. TAP’s solid 2022 operating results coupled with its network to Brazil, the world’s 12th-largest economy, has attracted interest from all three of the European full-service carrier groups. TAP’s market share of the flights between Europe and Brazil at c.30% is almost twice that of LATAM’s 15%. TAP also has the third-largest share (10%) of flights from Europe to Latin America, behind Iberia (13%) and Air France (11%). In June, the Portuguese Government, which owns TAP, announced that keeping Lisbon’s airport hub and safeguarding TAP’s strategic roles for Portugal will be a key condition of the airline’s upcoming privatisation. Lufthansa group, Air France-KLM and IAG have all shown an interest.

Strong aircraft orders at the Paris Air Show increase production backlog

Approximately 1,000 orders and LOIs, of which 600 were firm, were announced at the recent Paris Air Show. This is clearly great news for the two major OEMs. Airbus has the majority share at 78% and, out of those 825 orders, 500 were A320neo aircraft for Indigo in India. If you add Air India’s 450 Boeing and Airbus orders, the number of orders placed outside India is minimal.

The backlog of over 13,000 aircraft will take around 10 years to deliver at recent production rates. This solidifies the in-production aircraft types for both OEMs and will help retain values over the long term, but the challenge now is how to cut the current backlog down to less than a seven year horizon.

The airframe OEMs have published their plans to ramp things up – Airbus is opening new production lines – but the engine OEMs haven’t made the same commitment. The shortage of materials and labour is not going to be resolved in the short term because many of the precious metals traditionally come from Ukraine and Russia, so it is likely that airframes will continue to pile up at assembly lines while they await engines.

The new generation narrow-body engines – CFM LEAP and PW GTF – have both suffered major in-service reliability issues and much less time on-wing than was originally anticipated. Both OEMs have managed to improve their products and have ongoing reliability upgrades, but it remains to be seen whether all Life Limited Parts (LLPs) in those engines will ever reach their target design life.

CFM LEAP orders have traditionally exceeded those for the PW GTF, but recent orders have seen a rise in GTF- powered A320 aircraft, which will see them account for approximately 40% of the market. The improvements have clearly restored industry faith in the engines, but many of the latest Airbus orders do not yet have an engine selection. The airlines and lessors are still waiting to see which engine performs best before committing. This doesn’t just mean on-wing performance; it also includes the OEMs’ ability to manufacture and deliver the engines on time.

Prefer to download the report?

Strong aircraft orders at the Paris Air Show increase production backlog

Approximately 1,000 orders and LOIs, of which 600 were firm, were announced at the recent Paris Air Show. This is clearly great news for the two major OEMs. Airbus has the majority share at 78% and, out of those 825 orders, 500 were A320neo aircraft for Indigo in India. If you add Air India’s 450 Boeing and Airbus orders, the number of orders placed outside India is minimal.

The backlog of over 13,000 aircraft will take around 10 years to deliver at recent production rates. This solidifies the in-production aircraft types for both OEMs and will help retain values over the long term, but the challenge now is how to cut delivery times down to less than seven years.

The airframe OEMs have published their plans to ramp things up – Airbus is opening new production lines – but the engine OEMs haven’t made the same commitment. The shortage of materials and labour is not going to be resolved in the short term because many of the precious metals traditionally come from Ukraine and Russia, so it is likely that airframes will continue to pile up at assembly lines while they await engines.

The new generation narrow-body engines – CFM LEAP and PW GTF – have both suffered major in-service reliability issues and much less time on-wing than was originally anticipated. Both OEMs have managed to improve their products and have ongoing reliability upgrades, but it remains to be seen whether all Life Limited Parts (LLPs) in those engines will ever reach their target design life.

CFM LEAP orders have traditionally exceeded those for the PW GTF, but recent orders have seen a rise in GTF-powered A320 aircraft and they now account for approximately 40% of the market. The improvements have clearly restored industry faith in the engines, but many of the latest Airbus orders do not yet have an engine selection. The airlines and lessors are still waiting to see which engine performs best before committing. And this doesn’t just mean on-wing performance; it also includes the OEMs’ ability to manufacture and deliver the engines on time.

Significant aircraft orders from the likes of Indigo and Avolon at the Paris Air Show point to the long-term growth of the aviation industry. The sector is expected to return US$10 billion in profits in 2023 but the headline figure hides disparities between regions and carriers.

Derek Wong adds: “Therefore, Investec remains selective in deploying capital. We are also watching out for macro headwinds such as slower GDP and trade growth, higher interest rates and various forms of labour and supply-chain constraints. On a more positive note, we have seen airline demand for additional capacity translate into lease extensions, robust lease rates and firmer aircraft values. Investec’s strategy will continue to focus on capturing opportunities with strong carriers and liquid in-demand aircraft types.”

The resurgence of global airline traffic is resulting in increased demand for narrow-body aircraft, which, coupled with the slow production rates of new aircraft, is causing market values and lease rates for current-generation aircraft to improve each month.

David Louzado adds: “India is leading the way in new aircraft orders, but can the OEMs overcome their supply-chain and labour-market problems in time to meet the demand, and can they synchronise their efforts accordingly?”

Trends

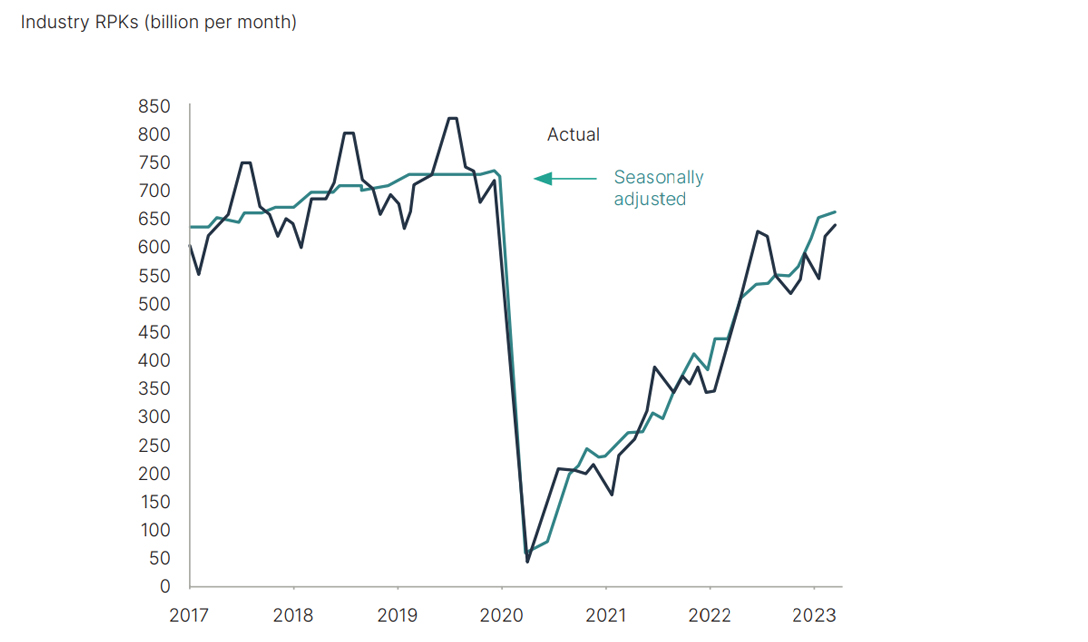

Global air travel continued its recovery in April and numbers are now 90% of pre-pandemic levels. Air traffic measured by Revenue Passenger Kilometres (RPKs), an indicator of global passenger demand, grew by 46% YoY to April 2023. Capacity, as measured by Available Seat Kilometres (ASKs), increased 40% YoY, with industry-wide passenger load factors trending at near pre-pandemic levels (81%) for the month.

Air Passenger Traffic (RPKs)

Sources: IATA Sustainability and Economics, IATA Monthly Statistics

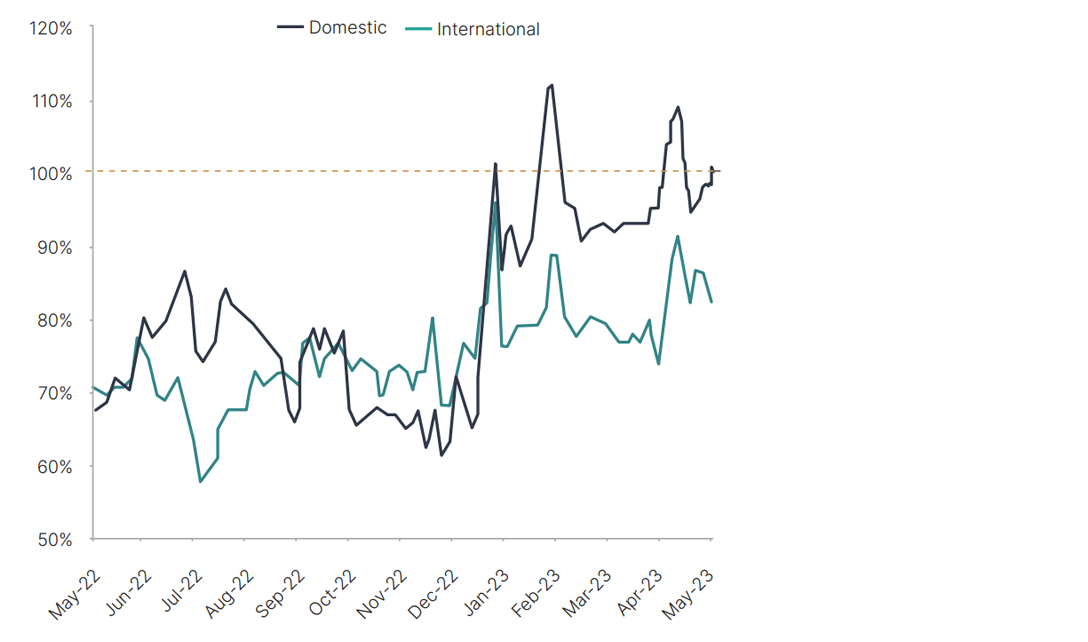

Passenger ticket sales by day of travel, % share of same day in 2019

Sources: IATA Sustainability and Economics, DDS

Global ticket sales were boosted by the Labour Day holidays in China between 29 April and 3 May. Domestic ticket sales peaked in April at 11% ahead of pre-pandemic levels, while international ticket sales were only 8% below 2019 levels. IATA noted that the ticket-booking data continued to project a positive outlook for the upcoming months.

Domestic air travel has now in aggregate fully recovered, with RPKs 3% ahead and ASKs 6% ahead of April 2019 levels. The growth was widespread, with all IATAs reporting regions surpassing pre-pandemic levels. April was also the first time that Asia Pacific carriers achieved domestic growth above 2019 levels. Indeed, China has rapidly restored capacity and domestic RPKs exceeded pre-pandemic levels by 6%. However, with capacity in China up 21% compared with April 2019, load factors are modest at 74%.

International air travel has continued its steady growth trajectory. Globally, traffic grew 48% YoY to April 2023 and is now 84% of pre-pandemic levels. The annual growth in ASKs in April was 38%, resulting in international load factors increasing to 81% (1 ppt less than pre-pandemic levels). With the gradual reopening of China, carriers in Asia Pacific continue to drive this growth, with RPKs in the region nearly tripling during April. Traffic within Asia is also showing positive momentum, reaching 56% of pre-pandemic levels. Passenger flow between Europe and North America has remained consistently high and exceeded pre-pandemic levels for the fourth consecutive month.

Global Air Traffic versus pre pandemic April 2019

(as measured by RPKs)

90%

103%

84%

81%

Airline financial performance

At a global level, IATA is forecasting that the industry will generate a net profit of USD9.8 billion in 2023, with a modest 1.2% net profit margin. Financial performance across regions remains divergent and continues to be led by North America. The US is followed by Europe and the Middle East, which are also forecast to be profitable in 2023. Airlines have adapted to changing travel habits post-pandemic by increasing frequencies on the weekends and deploying more premium cabin seating. In addition, airlines have simplified their fleets to improve cost management and they are also benefitting from the falling price of jet fuel, which has continued its downward trend from April 2022.

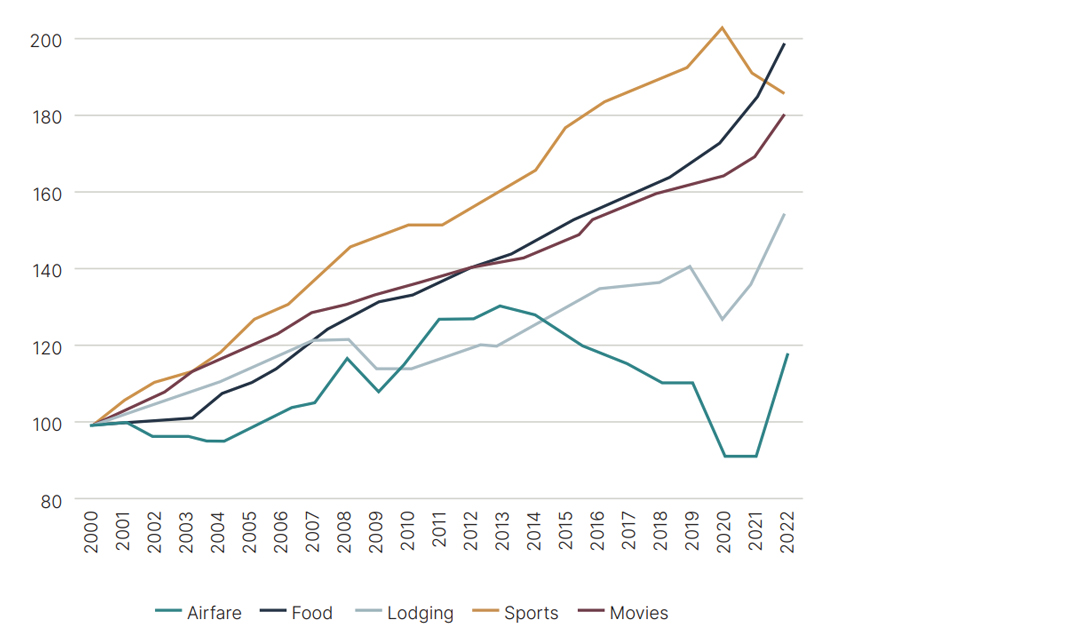

Airfares have been driven up in many jurisdictions by inflation and pent-up demand exceeding capacity. However, when compared with other leisure categories over the last 22 years, the increase is less pronounced (see graph below).

Airfare price increases versus other categories

Index (2000 = 100)

Sources: US BLS

How has the market responded?

In early April, Airbus announced that it would open a second A320 assembly line in Tianjin, China. This will double Airbus’s production capacity in China, bolster its footprint in a crucial market and sidestep potential geopolitical risks. The assembly line is forecast to begin operations in late 2025 and will position Airbus to capitalise on expected market growth driven by a rapidly emerging middle class (forecast at 5.3% annually in China and 9.0% in neighbouring India until 2041). The new Chinese site should help Airbus reach its goal of delivering 75 A320 and A321 aircraft per month in 2026 (up from 43 per month in 2022). The current order backlog stands at ~7,300 aircraft.

On 10 May, Go Airlines (India) Ltd was granted bankruptcy protection, marking the most significant bankruptcy of an Indian airline since Jet Airways in 2019. The low-cost carrier, recently rebranded as Go First, was plunged into financial crisis early in 2023, driven by what it called ‘faulty’ Pratt & Whitney engines that grounded around half of its 54 A320neo fleet. Alvarez & Marsal has been appointed to take over management with immediate effect. The bankruptcy complicates matters for lessors, many of whom have filed requests with India’s aviation regulator for the return of approximately 40 aircraft after rental payments were missed.

In May, following a significant recovery of the aviation market in the wake of the pandemic, Bain Capital announced that it was targeting a November initial public offering for a A$1 billion re-listing of Virgin Australia. The sale is expected to enable Bain to recover most of its original investment while still retaining a majority stake. Australia’s second-largest carrier entered voluntary administration in April 2020 with A$6.8 billion of debts to stakeholders.

Founded in 2021, start-up Global Airlines is the world’s newest long-haul airline and is aiming to begin operations in the spring of 2024. The company attracted headlines during the quarter with an announcement that it has entered an agreement to buy an additional three A380s, bringing its fleet to four aircraft. The airline is planning to refit them before returning them to service.

In June, the European Commission announced that it had decided to include aviation activities within the EU Taxonomy regime as transition activities for their ‘potential contribution to climate change mitigation’. The criteria to be embedded in the EU Taxonomy will focus on incentivising the development of zero-emission technologies and the manufacturing and uptake of latest-generation aircraft to promote fleet renewal. The criteria will also incentivise the adoption of sustainable aviation fuels (SAF), increasing the percentage of SAF uptake by five points to 15% by 2030. The European Commission noted that: “Together, they can help mitigate emissions from aviation to a significant degree before transformative zero-emissions technologies become market-ready and become economically viable alternatives. The criteria will also be reviewed periodically, every three years as for any transitional activities under the Taxonomy Regulation.”

In June, Fitch Ratings assigned a neutral outlook to the global aircraft leasing sector. Improved airline operating performance boosted by pent-up post-pandemic demand was offset by ongoing macroeconomic challenges. According to agency estimates, Fitch-rated aircraft lessors issued $6.2 billion of unsecured debt at a weighted average coupon of 5.6% in the first half of 2023. The agency noted that “activity is expected to increase despite a rise in rates and market volatility, as aircraft lessors address $19.8 billion in term debt maturities and $24.1 billion in expected capex in the next 12 months”.

In late June, Boeing reported that around 90% of 737 Max aircraft owned by Chinese carriers had resumed commercial operations. China grounded all Boeing 737 Max aircraft following the fatal crash in Ethiopia in March 2019. State-owned China Southern Airlines was the country’s first carrier to resume flying the 737 Max in January 2023. Since then, Chinese airlines have been gradually reintroducing the model back into operations. In April 2023, China’s aviation regulator published a revised report that Boeing views as a key step to resuming 737 Max deliveries to Chinese carriers.

Recent debt capital market deals, include

- 13 April, TrueNoord Aviation secured a $275m 5-year senior secured term loan to finance a portfolio of 31 regional jet and turboprop aircraft, with a margin of +315 bps over SOFR.

- 2 May, Avolon issued a $750m 5-year senior unsecured note. The issuance has a coupon of 6.380% (+300 bps) and was rated BBB-, Baa3 and BBB- by Fitch, Moody’s and S&P respectively. The notes will be used for general corporate purposes.

- 16 May, BOC Aviation issued a $500m 5-year senior unsecured bond. The bond has a coupon of 4.500% (+120 bps) and is priced at 99.439 cents for an all-in yield of 4.627%. It was rated A- by both Fitch and S&P. Proceeds will be used for general corporate purposes.

- 21 May, China Airlines issued a NT$2.65bn senior unsecured note. The 5-year note has a fixed rate of 1.900% and will be used to refinance debt.

- 24 May, Griffin Global Asset Management issued a $1.0bn senior notes financing package, including $400m of 3yr senior notes with a coupon of 7.75% (+373 bps) and $600m of 5yr senior notes with a coupon of 8.0% (+421 bps). Both the corporate and the dual-tranche are rated BB and BB- by Fitch and S&P, respectively. Proceeds from Griffin’s debtssuance will be used to partially repay the company’s $2bn warehouse facility and to fund general corporate purposes.

- 2 June, China Aircraft Leasing Tianjin issued a RMB1.5bn 3-year low-carbon transition note. The issuance has a coupon of 3.850% and will be used for aircraft purchases.

- 12 June, United Airlines issued a $1.32bn EETC. The transaction was a single tranche deal rated A3 and A by Moody’s and S&P, respectively. It has a final maturity of 12.6 years, an average life of 9.5 years and a 5.800% coupon with a T + 207 bps spread.

- 19 June, Japan Airlines issued a JPY20bn 10-year sustainability development goal-linked note. The issuance has a coupon of 1.200%.

Jet fuel market update

Brent Crude continued its descent from the highs of last summer into the start of this year, but found a floor around $70 per barrel and has drifted sideways since March. The market has been surprised by the failure of sanctions to inhibit Russian output, and Chinese demand has not picked up as quickly as had been expected, both of which were negative for prices. To counter this, OPEC+ members have taken measures to cut output to stabilise the market, preventing Brent from dropping below 70 $/b and enabling it to continue moving sideways. The burden of cuts has fallen mainly on Saudi Arabia though, particularly on its extra 1 mb/d cut (around 1% of global supply and 10% of Saudi output), which has now been extended to the end of August. This raises questions over the resolve of OPEC+ to manage the market and the risk of Saudi Arabia throwing the towel in on its voluntary cuts. Indeed, the Saudis could increase output to compete for market share even though sharp falls in prices would likely follow.

However, forecasters such as the International Energy Agency continue to expect demand – driven by Asia – to increase over the second half of the year. Some of these forecasts suggest that the market could be heading for a significant deficit. If this does happen, then Saudi Arabia will be able to unwind its cuts and take the pressure off OPEC+. If demand does not rebound significantly, then Saudi Arabia may need to extend its additional cut beyond August, or get other OPEC+ members to share the pain. The trajectory of demand over the coming weeks may prove decisive.

Callum Macpherson, Head of Commodities

Brent Front Contract

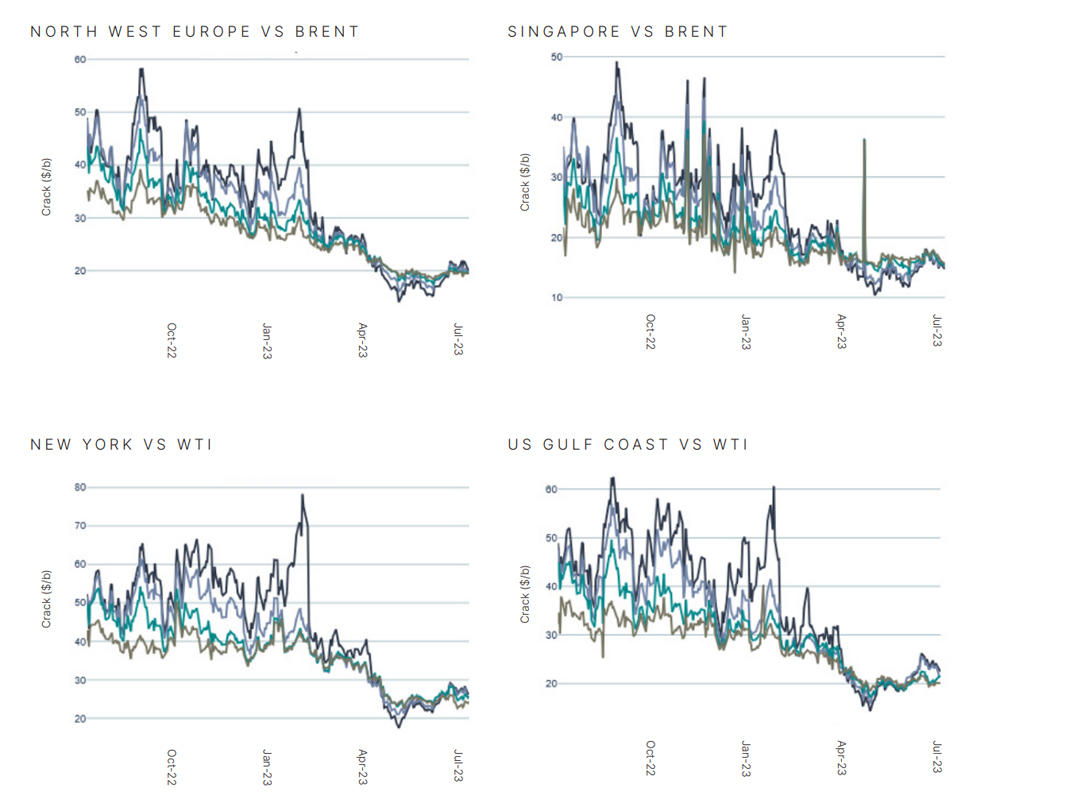

Disruption to Russian output last year led to dramatic increases in the premium of jet fuel prices over crude (the crack spread). The premium steadily dissipated into this year as logistical juggling enabled oil trade flows to be rerouted so that Russian crude and refined products could continue to reach world markets. The spread reached its low point in April and May at levels that were comparable with those seen before the invasion of Ukraine. However, they have started to rise again lately as jet fuel is expected to be a significant element of demand growth this year, especially in Asia.

Global jet crack spreads

Source: Invstec, Bloomberg

2022 Aviation Debt

Investec Arranged and closed over US$550m

Investec Aviation Finance

$10 billion

7 years

25+ people

Disclaimer

This presentation and any attachments (including any e-mail that accompanies it) (together “this presentation”) is for general information only and is the property of Investec Bank plc (“Investec”). It is of a confidential nature and all information disclosed herein should be treated accordingly.

Making this presentation available in no circumstances whatsoever implies the existence of an offer or commitment or contract by or with Investec, or any of its affiliated entities, or any of its or their respective subsidiaries, directors, officers, representatives, employees, advisers or agents (“Affiliates”) for any purpose.

This presentation as well as any other related documents or information do not purport to be all inclusive or to contain all the information that you may need. There is no obligation of any kind on Investec or its Affiliates to update this presentation. No representation or warranty, express or implied, is or will be made in relation to, and no responsibility or liability is or will be accepted by Investec or its Affiliates as to, or in relation to, the accuracy, reliability, or completeness of any information contained in this presentation and Investec (for itself and on behalf of its Affiliates) hereby expressly disclaims any and all responsibility or liability (other than in respect of a fraudulent misrepresentation) for the accuracy, reliability and completeness of such information. All projections, estimations, forecasts, budgets and the like in this presentation are illustrative exercises involving significant elements of judgement and analysis and using the assumptions described herein, which assumptions, judgements and analyses may or may not prove to be correct. The actual outcome may be materially affected by changes in e.g. economic and/or other circumstances. Therefore, in particular, but without prejudice to the generality of the foregoing, no representation or warranty is given as to the achievability or reasonableness or any projection of the future, budgets, forecasts, management targets or estimates, prospects or returns. You should not do anything (including entry into any transaction of any kind) or forebear to do anything on the basis of this presentation. Before entering into any arrangement, commitment or transaction you should take steps to ensure that you understand the transaction and have made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances, including the possible risks and benefits of entering into such a transaction. No information, representations or opinions set out or expressed in this presentation will form the basis of any contract. You will have been required to acknowledge in an engagement letter, or will be required to acknowledge in any eventual engagement letter, (as applicable) that you have not relied on or been induced to enter into engaging Investec by any representation or warranty, except as expressly provided in such engagement letter. Investec expressly reserve the right, without giving reasons therefore, at any time and in any respect, to amend or terminate discussions with you without prior notice and disclaim hereby expressly any liability for any losses, costs or expenses incurred by that client.

Investec Bank plc whose registered office is at 30 Gresham Street, London EC2V 7QP is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority, registered no.172330.