Back To Reality

08 September 2020

Globally the Covid rollercoaster continues with India and Brazil at the top, and numbers rising in France and the UK.

4 min read

08 Sep 2020

The housing market is helping to lead the UK’s recovery. No doubt there is some pent-up demand from buyers who were stalled by Covid, as well as the much-reported exodus from city centres (especially by renters who now see the possibility of remote working from a pleasant location funded by rock-bottom interest rates). 66,300 mortgages were approved in July, well ahead of expectations. Nationwide’s House Price Index recorded a 3.7% rise over the year to August, while the Land Registry’s version rose 2.9% (although this was only to May).

August’s Non-Farm Payrolls saw an addition of 1,371,000 jobs, slightly more than forecast and well above a pessimistic “whisper” number that was doing the rounds. The Unemployment Rate ticked down from 10.2% to 8.4%, which remains well above European equivalents owing to the latter’s use of furlough schemes. Average Hourly Earnings growth, which peaked at 8% y/y, has fallen back to 4.7%. While presenting some return to the more normal 3-3.5% seen pre-Covid, it still illustrates tougher conditions for less skilled workers who have lost jobs in greater numbers.

Headline price levels fell into deflation territory in August across the euro zone, coming in at -0.2% y/y (-0.4% m/m). The Core rate stayed above water at 0.4%, but that was still the lowest reading since the inception of the euro (1999). No doubt there are short-term effects such as discounts to get people shopping again, but the numbers suggest that the ECB might have to up its game (even more) at the next meeting.

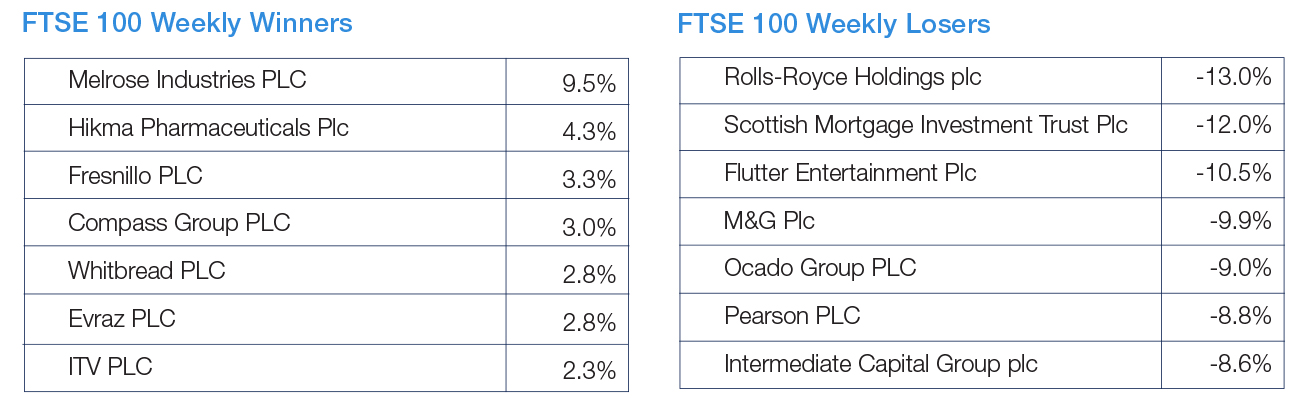

Source: FactSet

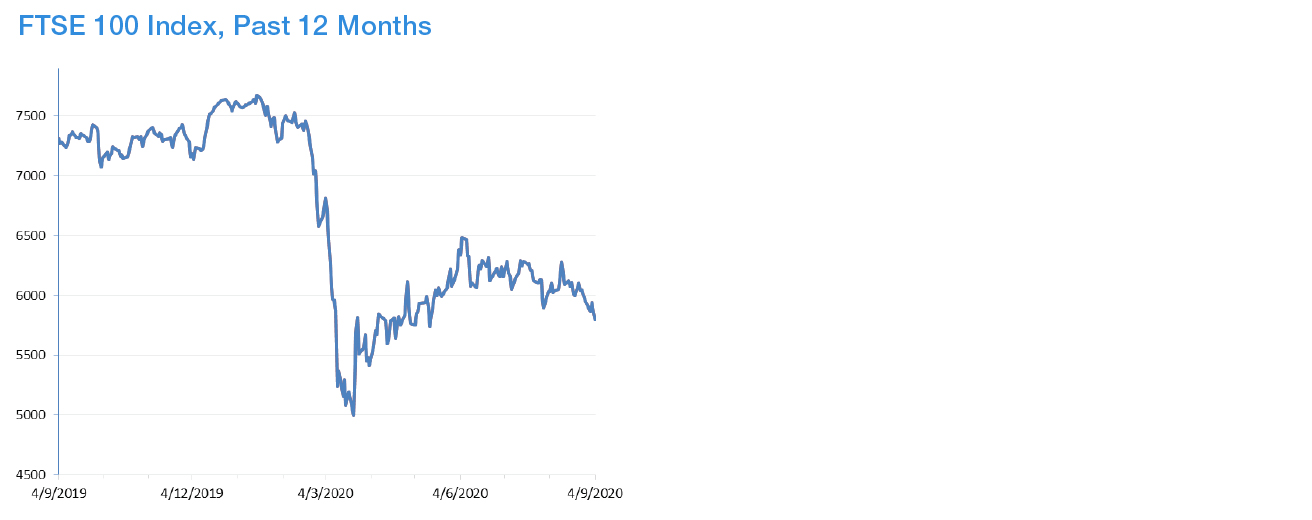

Source: FactSet