Bond Yield Resurrection

08 March 2021

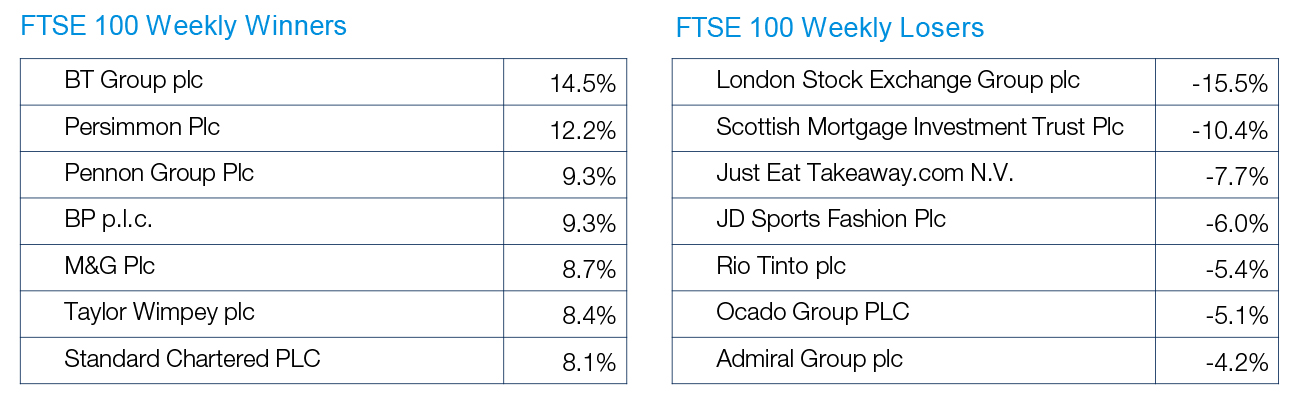

All roads lead back to the bond market at the moment, as it again proves its power over pretty much every other asset class.

5 min read

08 Mar 2021

With the Budget taking centre stage last week, there was a dearth of new economic data. Only the Nationwide House Price Index caught the attention, showing a gain of 6.9% y/y. Not sure anyone would have predicted that a year ago, but record low interest rates and the Stamp Duty holiday have boosted demand, along with a shift from urban centres and a desire for larger houses and gardens to accommodate home offices and unschooled children. Bank of England Governor Andrew Bailey, in a speech today, followed the tone of other central bankers in promising continued monetary accommodation. The MPC ‘does not intend to tighten monetary policy at least until there is clear evidence that significant progress is being made in eliminating spare capacity and achieving the 2% inflation target sustainably'.

Non-Farm Payrolls rose by more than expected in February. A net 379k jobs were created, against an expected number of 200k, and January’s figure was revised higher too. The Unemployment rate ticked down a tenth to 6.2%. Wage growth of 5.3% remained strong, although still reflects the fact that it is lower paid workers who have borne the brunt of Covid when it comes to the employment market.

Full employment has never materialised in the euro zone. Even pre-pandemic the unemployment rate only got as low as 7.3%, before bouncing to 8.7% thanks to Covid. Of course, that figure would have been a lot worse had it not been for furlough-style arrangements such as Germany’s “Kurzarbeit” scheme. The figure has now fallen back to 8.1%, and should continue to drop as economies re-open.

We have seen the first evidence of what will happen to economic data once we start to compare it with last year’s (lack of) activity during lockdowns. China’s Exports (+60.6%y/y) and Imports (+22.2%) were higher than forecast in February. There still appeared to be plenty of external demand for *working from home* goods, as well as PPE related to Covid. Import values were boosted by higher commodity prices.

Source: FactSet

Source: FactSet