Caution, Not Fear

20 September 2022

It’s difficult to judge when exactly markets will bottom out, but within the next six months looks plausible.

4 min read

20 Sep 2022

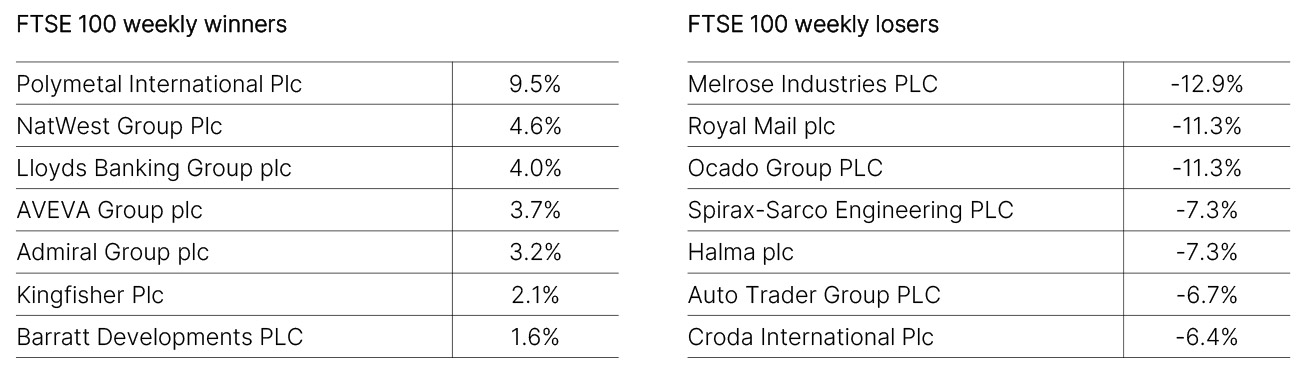

Welcome to our Economic Highlights, bringing you market updates from across the UK, US, Europe and China, as well as the FTSE weekly winners and losers.

UK Retail Sales for August made pretty grim reading. The 1.6% month-on-month drop in volumes (consensus -0.5%) suggests that the economy might already be in recession. The fall more than reversed the upwardly revised 0.4% month-on-month rise in July. Sales volumes fell in every major category and the Office for National Statistics (ONS) reported that high prices were prompting households to rein in their spending. This echoes the fall in consumer confidence to its lowest level on record in August. Fuel sales fell 1.7% despite a sharp 6.2% month-on-month decline in fuel prices in August. Admittedly, these data related only to spending on goods and not on services such as hospitality, which have fared considerably better since the removal of Covid restrictions. Nonetheless, it is hard to escape the conclusion that cost-of-living pressures may be catching up with consumers’ spending patterns. The Bank of England will be watching closely when it decides how much policy tightening is needed to bring price pressures under control.

Core CPI (stripping out the more volatile food and energy elements) jumped 0.6% month-on-month, a pick up from July’s 0.3% reading and 0.3% ahead of market expectations. This meant that the year-on-year rate increased from 5.9% to 6.3%, 0.2% ahead of expectations. The headline reading of 8.3% year-on-year did soften slightly from July’s 8.5%, but it too was 0.2% ahead of expectations. Some comfort could be taken from the hourly earnings figure, up 5.2% year-on-year, which was unchanged from July and in-line with expectations. Even so, the upside surprise cemented expectations of a 75bp rise in the Fed Funds rate at this week’s meeting, with a full 1% not ruled out. Jobless claims, headline Retail Sales and the Empire Manufacturing survey were all better than expected, although the Philadelphia Fed survey missed forecasts as did other interpretations of Retail Sales. When it comes to hard economic data, we are back in the “good news is bad news” phase, and strong data means a more restrictive Fed.

Eurozone industrial production contracted by a larger-than-expected 2.3% month-on-month in July following a 1.1% increase in June. Capital goods and durable consumer goods led the decline. The outlook for the European economy remains poor. Rising electricity prices are hurting European manufacturing, with companies including ArcelorMittal, Ferroglobe and other heavy energy-consuming businesses announcing plans to shut down temporarily some of their operations, warning that high costs are denting competitiveness. Now that the Nord Stream 1 pipeline is “indefinitely” shut down, further energy supply disruptions are in the offing. Eurozone demand is weak and sentiment is dismal. The forward-looking Manufacturing PMI new order-to-inventory measure augurs poorly for future manufacturing activity and industrial production. Decelerating Chinese and ex-Eurozone global growth momentum pose another headwind to industrial production in the Euro Area. Meanwhile, inflationary pressures are compelling the European Central Bank to tighten policy amid a weakening economic backdrop.

Industrial Production, Retail Sales and Fixed Asset Investment for August all beat expectations, although Home Prices and Residential Property Sales remained weak. Maybe there are tentative signs that stimulus measures are having an effect, although there remains a great deal of scepticism about whether the government will feel compelled to be much more aggressive right now. There is a widely held opinion that the leadership will be more focused on sorting out existing structural problems (notably in the real estate sector) than unleashing a new wave of strong growth, which would probably require further debt creation. At least now we know the date of the National Party Congress, which will begin on Sunday 16 October. The world is looking for some policy pointers, especially regarding the “zero-Covid” policy, which continues to constrain activity.

The information in this document is for private circulation and is believed to be correct but cannot be guaranteed. Opinions, interpretations and conclusions represent our judgement as of this date and are subject to change. The Company and its related Companies, directors, employees and clients may have positions or engage in transactions in any of the securities mentioned. Past performance is not necessarily a guide to future performance. The value of shares, and the income derived from them, may fall as well as rise. The information contained in this publication does not constitute a personal recommendation and the investment or investment services referred to may not be suitable for all investors. Copyright Investec Wealth & Investment Limited. Reproduction prohibited without permission.

Member firm of the London Stock Exchange. Authorised and regulated by the Financial Conduct Authority.

Investec Wealth & Investment Limited is registered in England.

Registered No. 2122340. Registered Office: 30 Gresham Street, London EC2V 7QN.