Exit Strategies

06 April 2020

Investors decisions can be dictated by the current situation and the weight of their portfolio.

5 min read

06 Apr 2020

We are finally beginning to see the effects of COVID-19 in “hard” economic data. 470,000 worker have registered for Germany’s Kurzarbeit scheme, which allows companies to retain employees with financial assistance from the government. Last year that initiative attracted just 1,300 applicants per month, on average. In the UK, 950,000 people registered for Universal Credit in the two weeks to 30th March. A normal number would be around 100,000. Norway reported a 10% jump in unemployment in just two weeks.

But of all of this was merely an appetiser for the US Weekly Jobless Claims. These jumped from the previous week’s shocking record number of 3.3 million to an astounding 6.65 million. That’s 10 million people losing their jobs in just two weeks, or around 6.5% of the non-farm workforce. That would take months during an ordinary recession, and underlines the severity of the economic shock. The US unemployment rate could be over 10% already. A normal indication of a recession is rise of 0.5% from the low!

PMI data from China suggest a recovery, notably in Manufacturing. Last week’s Caixin PMI jumped from 40.3 to 50.1, so back into expansion territory. But PMI surveys are bound to be more imprecise than normal in the current environment, as they are based on a blunt question – are things better or worse than last month? They also fail to differentiate whether supply chain lengthening is a good thing (excess demand) or a bad thing (deficient supply). Very much the latter currently.

Latest UK data today is as bad as one might have expected. GfK Consumer Confidence posted a record fall from -9 to -34; Car Registrations down 44.4% (m/m) in March, and 31% YTD (y/y). Construction PMI fell from 52.6 to 39.3. Plenty more of this to come. Some things, such as cinema attendance, will be down 100%.

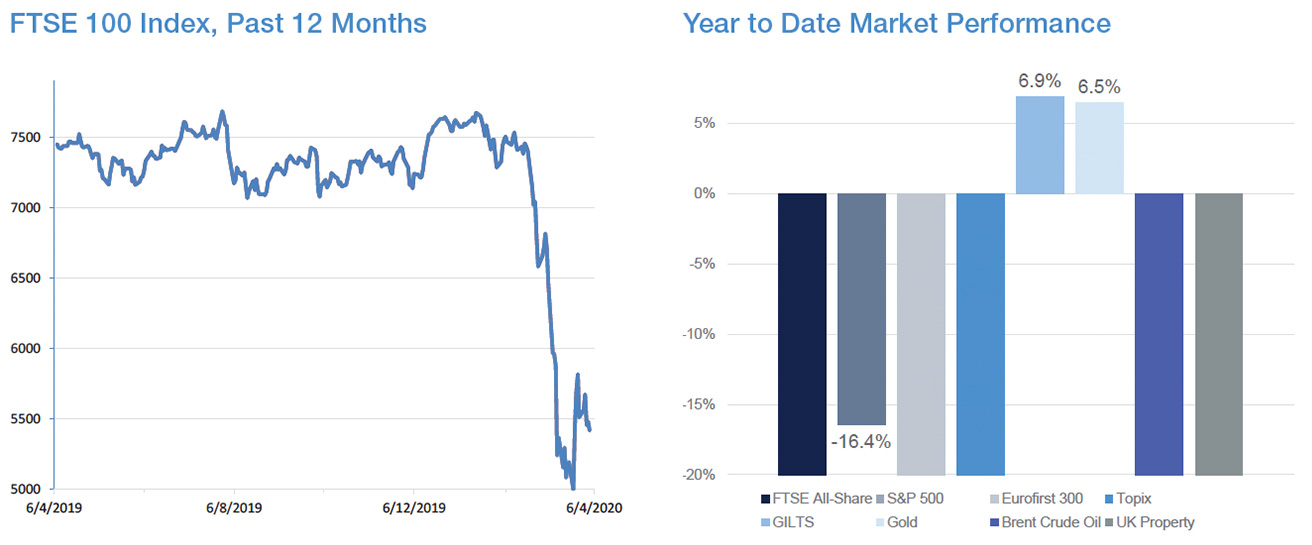

Source: FactSet

Source: FactSet