Eye of the Storm

01 August 2022

The snapshot view is that inflation is close to peak levels and that a recession is more likely in Europe than the US.

4 min read

01 Aug 2022

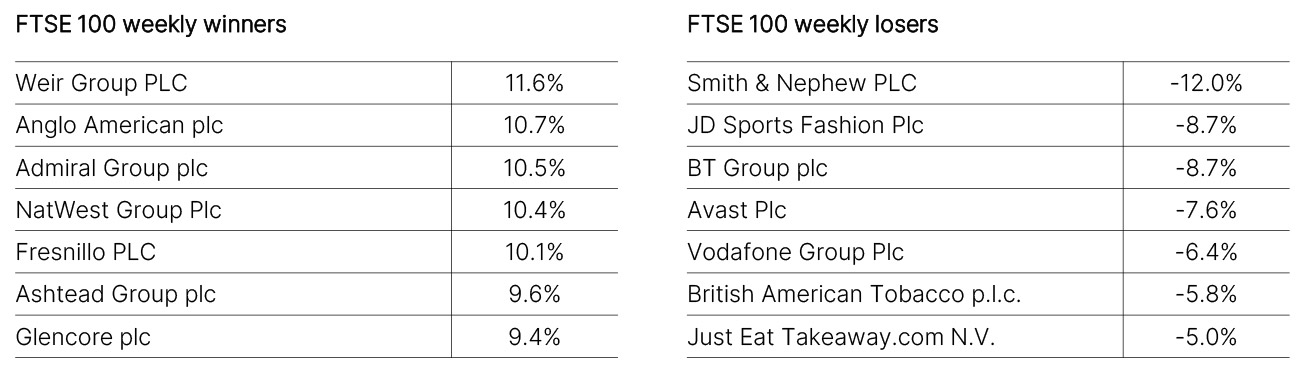

Welcome to our Economic Highlights, bringing you market updates from across the UK, US, Europe and China, as well as the FTSE weekly winners and losers.

Another large rise in unsecured borrowing in June remains difficult to interpret: rampant animal spirits, or forced borrowing to keep up with rising prices? The £1.8bn rise in consumer credit in June (forecast £1bn) was larger than the £0.9bn gain in May and the pre-pandemic average of £1.1bn. The increase suggests that non-retail spending may be continuing to hold up a bit better than retail spending (we learnt last week that retail sales volumes fell by 1.2% quarter-on-quarter in Q2). The £1.5bn rise in cash sitting in households’ bank accounts was much smaller than the £5.2bn rise in May and the 2019 average monthly rise of £4.6bn, which suggests that households are also reducing their savings to cope with higher prices. There was further evidence that higher interest rates are curbing housing market activity. The 63,726 of mortgage approvals in June was less than the 65,681 approvals in May and the pre-pandemic average of 65,700. The average new mortgage rate has now risen by 65bps (from 1.5% in November to 2.15% in June).

The Federal Reserve duly delivered its second successive 0.75% increase in interest rates at July’s meeting, and will now be able to sit on its hands and watch the data roll in until September. That’s because it has effectively abandoned “forward guidance” and will now move back to being more “data dependent”. Markets interpreted this as “dovish”, reducing expectations for the peak of the rates cycle by around 0.10% and also bringing that peak forward to December 2022 (not long ago it was in 2024).

Maybe the committee already knew that the following day’s GDP report would show a second successive quarter of declining output, thus putting the US into a “technical recession”. However, given that this was largely a function of a reversal of past inventory building and because consumption remained positive, the National Bureau of Economic Research (which rules on such matters) is unlikely to make it official. Even if overall output is decelerating, the Fed’s members’ minds will be exercised by an unwelcome stickiness in employment costs as well as in its favoured inflation measure, the PCE Core Deflator. The latter ticked back up to 4.8% year-on-year against expectations of remaining flat at 4.7%. Initial Jobless Claims (weekly data) continue to tick up, with the four-week rolling average of new claims having risen from a trough of 170k in April to 249k. So some of the heat is coming out of the labour market, but not enough to ease the tightness substantially.

Second quarter GDP data revealed a slightly better growth picture. Growth was recorded at 0.7% quarter-on-quarter (vs +0.2% expected). France, Italy and Spain all helped to drive the momentum, with tourism a key factor. Reports suggest that Americans are back in force thanks to the strength of the dollar against the euro. Of the big countries, Germany was the laggard, with no growth in output. Figures published alongside GDP showed another push higher in Euro area HICP inflation in July to 8.9% from 8.6%. However the ECB will be as concerned, if not more so, about the continued rise in core inflation (which strips out volatile food, energy and alcohol and tobacco prices), which firmed to 4%, a new record high for the euro era. On this evidence, the European Central Bank will have to consider a second successive 0.5% rate rise in September.

The latest Manufacturing PMI data show that the economy continues to struggle in the face of rolling lockdowns as a result of the country’s zero-Covid policy. The “official” number dropped from 50.2 to 49.0 (forecast 50.3), suggesting a contraction in output, while the Caixin version (collated by the Caixin media company) fell from 51.7 to 50.4 (forecast 51.5), which hardly suggests much in the way of growth. It’s hard to see these readings changing dramatically for the better without some radical policy shift, and one is not expected this side of the autumn’s National Party Congress, for which we still await a form date. Stimulus remains half-hearted, largely aimed at shoring up the real estate sector rather than boosting overall demand. The government has not officially abandoned its 5.5% GDP growth target for this year, but its absence from communications suggests that its demise has been acknowledged privately.

The information in this document is for private circulation and is believed to be correct but cannot be guaranteed. Opinions, interpretations and conclusions represent our judgement as of this date and are subject to change. The Company and its related Companies, directors, employees and clients may have positions or engage in transactions in any of the securities mentioned. Past performance is not necessarily a guide to future performance. The value of shares, and the income derived from them, may fall as well as rise. The information contained in this publication does not constitute a personal recommendation and the investment or investment services referred to may not be suitable for all investors. Copyright Investec Wealth & Investment Limited. Reproduction prohibited without permission.

Member firm of the London Stock Exchange. Authorised and regulated by the Financial Conduct Authority.

Investec Wealth & Investment Limited is registered in England.

Registered No. 2122340. Registered Office: 30 Gresham Street, London EC2V 7QN.