FAITal Attraction

22 March 2021

Inflation, Duration and Rotation.

5 min read

22 Mar 2021

February's public finance figures were slightly better than expected. The overall deficit was £19.1bn. Tax receipts, perhaps surprisingly, held up reasonably well at £63.2bn, but expenditure remains well above historical levels thanks to Covid (£72.6bn vs £67bn in 2020). Furlough payments remain a huge burden, amounting to £74.4bn in the current fiscal year. One thing to note, though, is that the current deficit numbers do not take into account the expected losses on bank loans that have been guaranteed by the government. The Office of Budget Responsibility currently projects losses of £27bn for the various schemes. On a brighter note, Consumer Confidence indices rose in response to the vaccine rollout, the new re-opening timetable and the Chancellor's generous budget.

Recent clear recovery trends in US data series have become more mixed. Last week saw disappointing readings for Retail Sales, Industrial Production, Housing Starts and Jobless Claims. Citi's Economic Surprise Index has fallen from 92 at the beginning of March to 41, the lowest level we have seen since the recovery started in Spring 2020. Some of the latest shortfall might have been caused by the snowstorms in Texas in February, and so we will wait to see if there has been a bounce in March. One effect of weaker bond markets, though, is to push up mortgage rates, with the 30-year national average now at 3.32%, up from 2.82% in early February. That might well dampen some of the activity in the housing market.

Precious little fodder in the EU last week, with most of the focus on poor vaccine distribution and tighter social restrictions in several countries. Generally, though, sentiment surveys suggest that people are willing to look through current impediments, and this was reflected in a nice jump in the latest ZEW survey of economic growth expectations, which rose from 69.6 to 74. Meanwhile February's inflation reading was confirmed at 1.1% y/y.

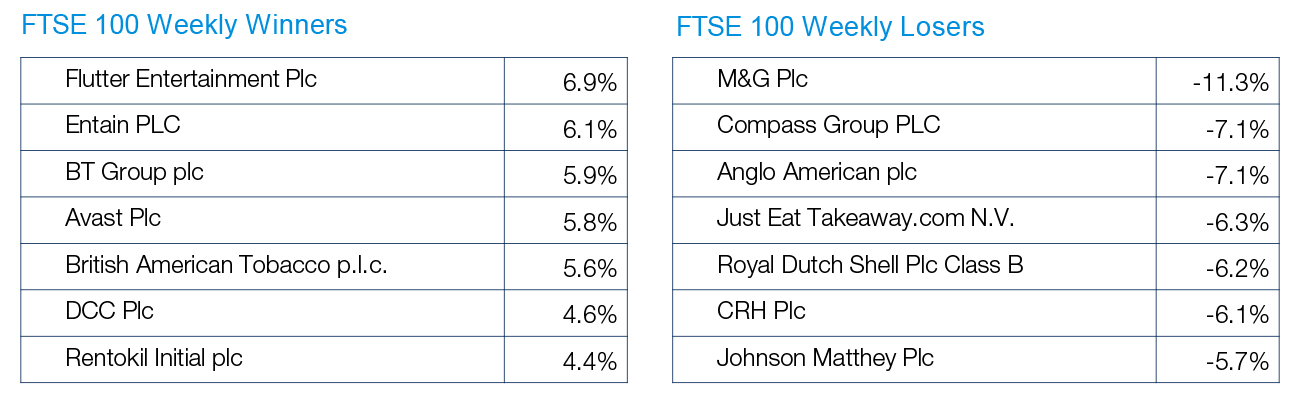

Source: FactSet

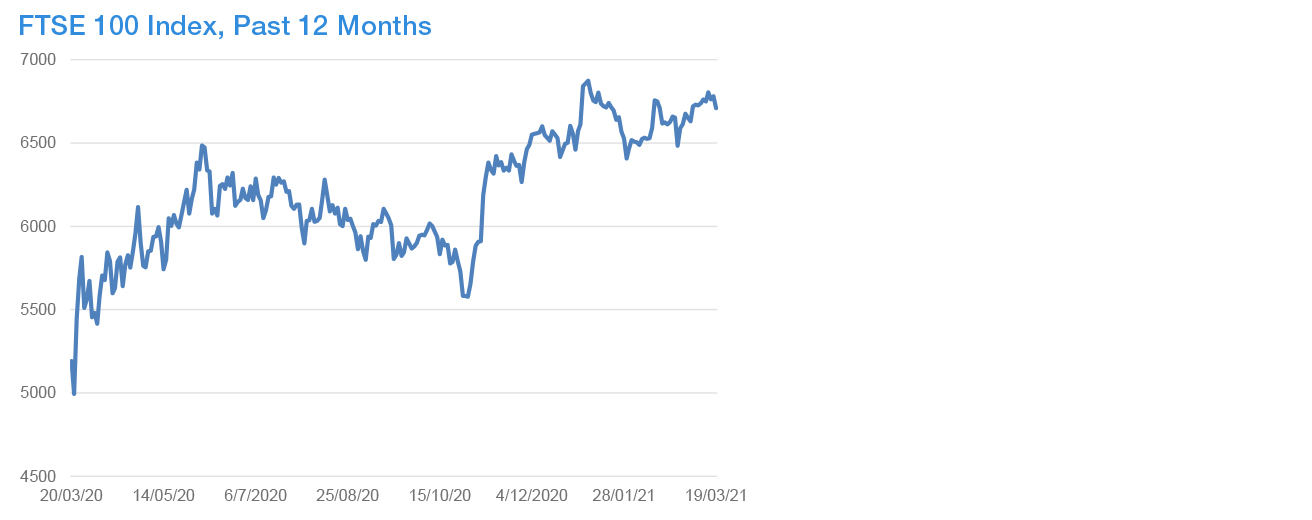

Source: FactSet