For want of a nail

12 October 2021

Companies with strong long-term relationships with their suppliers tend to have a sustainable competitive advantage.

5 min read

12 Oct 2021

A dearth of key data last week allows us to focus on comments from two members of the Bank of England’s Monetary Policy Committee (one of whom is the Governor). They both suggest that an interest rate rise is coming sooner rather than later due to inflationary pressures. More importantly, they also highlight the risk of embedded expectations of persistently higher inflation in the future. This could lead to a classic wage/price spiral, invoking fears of the 1970s. Investec Bank forecasts a 0.15% rise in February (to 0.25%) followed by a 0.25% rise in August. Futures markets now place a 50% probability on the first rise coming as soon as December.

Although the 194,000 gain in non-farm payrolls in September was a disappointment relative to the expectation of half a million, the market appeared to view it as strong enough for the Fed to begin tapering its asset purchases next month, especially following upward revisions to the two previous months’ data. This view is supported by all our economics research providers, including Investec Bank. But the combination of slowing growth and worsening labour shortages leaves the Fed in a quandary. The Covid-19 Delta variant was largely to blame for the shortfall, with the leisure, hospitality and education sectors all below expectations. Growth in manufacturing employment was a bright spot. The labour force fell by 183,000, which is worrying when people are supposed to be returning to employment now that certain benefits are rolling off. It remains 3 million below its pre-pandemic level. Consequently, the unemployment rate dropped from 5.2% to 4.8% (with the caveat that this does come from a different survey). Wage growth continued to be strong, with the annual rate rising to 4.6% and a record-high share of small firms planning to raise compensation.

Retail sales in August came in below expectations thanks to the Delta variant. Growth of 0.3% month-on-month (m/m) was better than the downwardly revised -2.6% in July, but below the expectation of +0.8%. Year-on-year growth is now flat. We are beginning to see downgrades to gross domestic product (GDP) growth expectations, with JP Morgan, for example, cutting its forecast for 2021 from 5.4% to 5.1% and 2022 from 5.2% to 5%. Recovery from the Delta variant is a positive force but more than offset by rising energy costs and supply chain disruption. But still, these are growth numbers that investors would have once salivated over.

Slim pickings here too. Much of the world’s focus remains on real estate giant Evergrande, with no resolution to its financial difficulties yet forthcoming. Asset sales (such as a stake in a listed bank) are being undertaken to provide cash to pay interest due and fulfil immediate debt repayment schedules. Still, there seems to be no way that the companies’ full liabilities can be covered. We, and the market, continue to expect an orderly unwind to be presided over by the government to avoid destabilising both the financial markets and the social situation. But risk appetite will be diminished and growth will be reduced as the speculative construction model of real estate development is constrained.

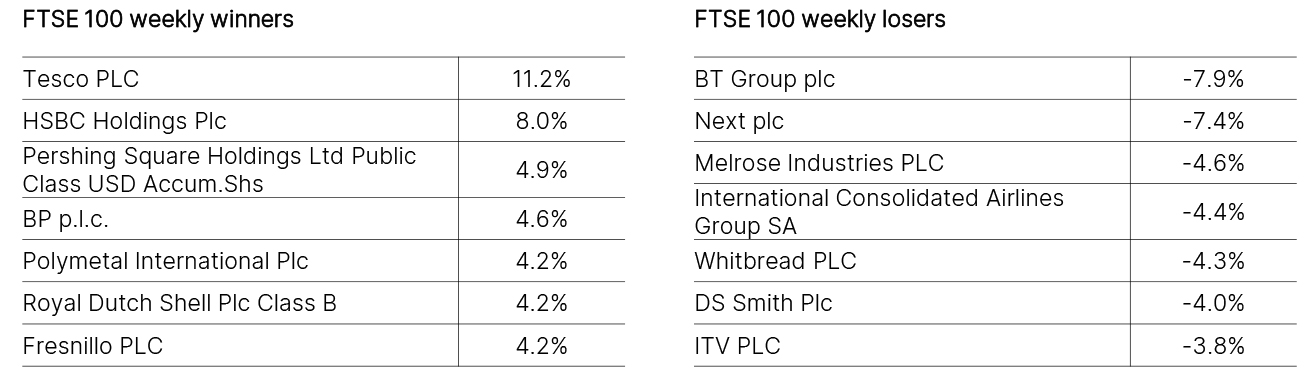

Source: FactSet

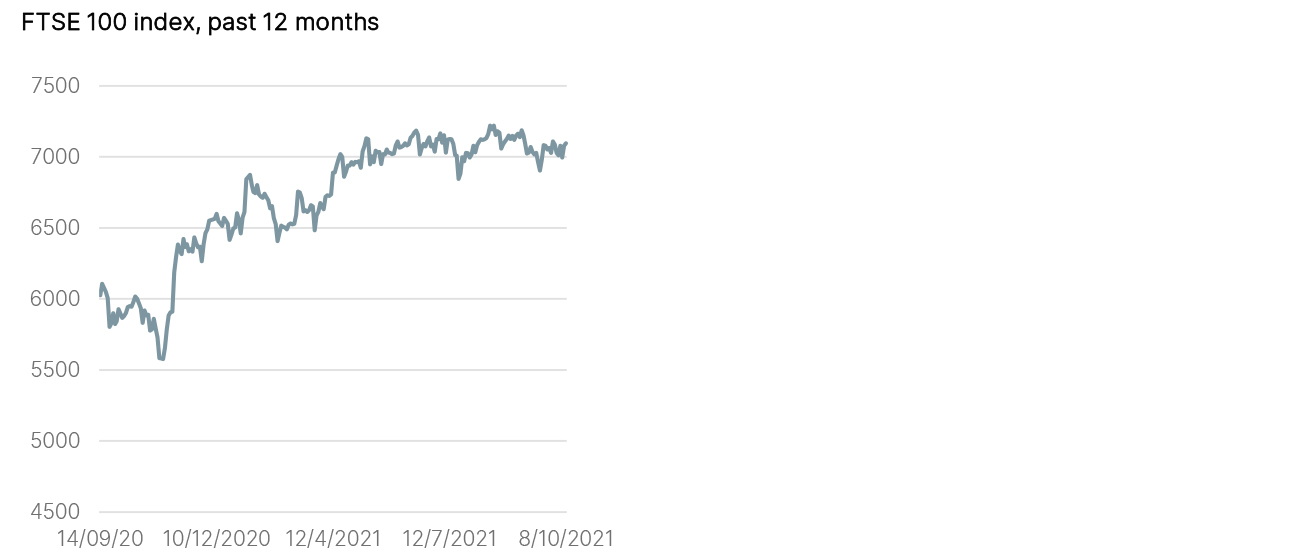

Source: FactSet