Hallelujah!

09 November 2020

Election results and vaccines, and the impacts of both.

4 min read

09 Nov 2020

The latest Markit/CIPS Purchasing Manager surveys revealed a slight deceleration in the UK even before we entered the latest lockdown in England. Construction (53.1 vs 56.8) and Services (51.4 vs 52.3) readings both slipped lower in October, although remained in growth territory. Manufacturing, which is also less affected by Lockdown 2.0, did manage to accelerate from 53.3 to 53.7. Government support remains crucial to maintaining growth as further job losses accrue (for example, John Lewis announced 1,500 job losses last week).

The US economy added 638k jobs in October (est 600k). Service sector jobs represented 783k, the bulk of which were in leisure and hospitality (271k), professional and business services (208k) and retail (104k). The headline rate of unemployment dropped to 6.9% (est 7.7%). This extends the recovery in the US labour market, with 12 million jobs re-added to the market since April’s nadir, although that still leaves the total level of payroll employees 10 million down on pre-COVID levels.

Eurozone Retail Sales declined 2% m/m in September as holidaymakers headed home and restrictions increased against the background of rising Covid cases. But the year-on-year growth of 2.2% is more encouraging, as savings and fiscal stimuli support consumption.

Both the Manufacturing (53.6 vs 53) and Services (56.8 vs 54.8) PMI readings accelerated in October, as China continued to weather the Covid storm better than any other major country.

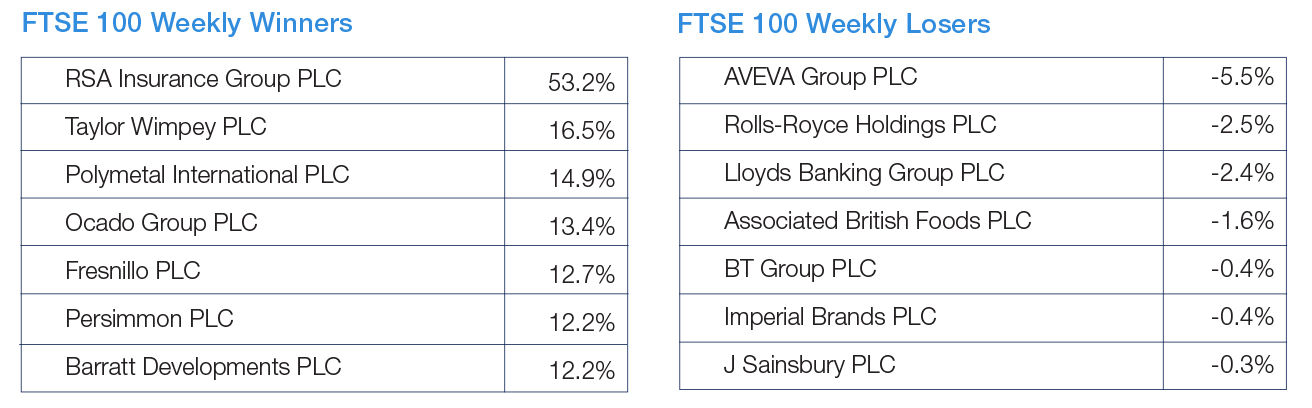

Source: FactSet

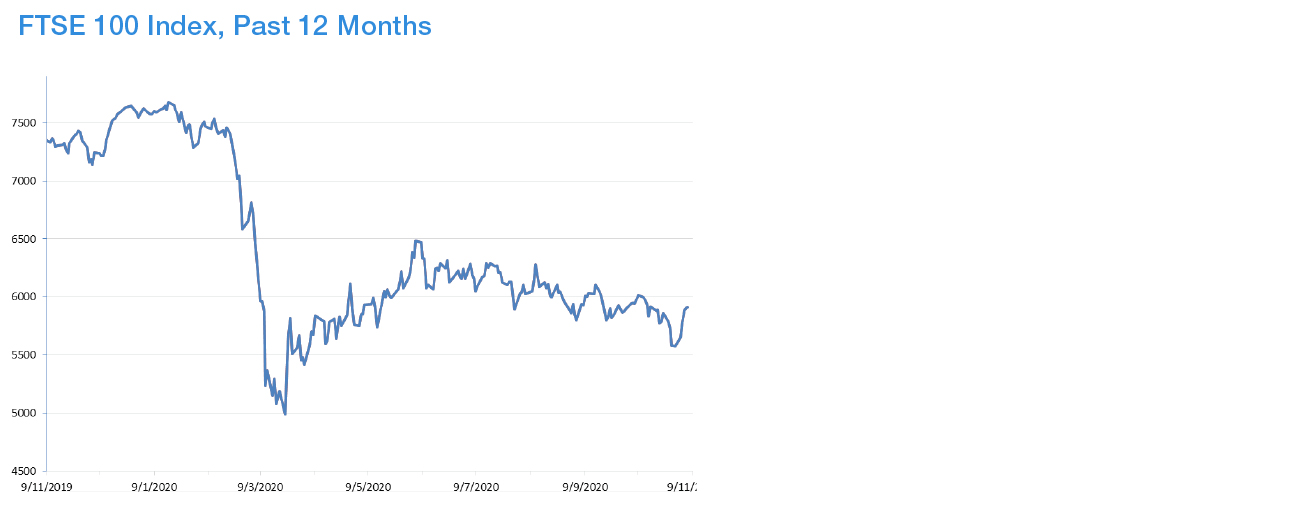

Source: FactSet