Information Overload

25 July 2023

The bar appears to be set reasonably low for the current earnings season, although that might turn out to be misleading.

5 min read

25 Jul 2023

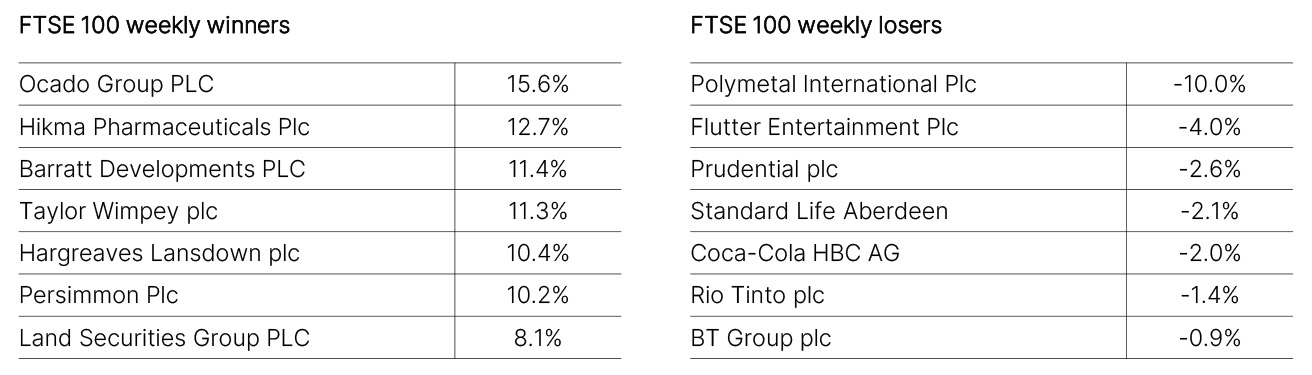

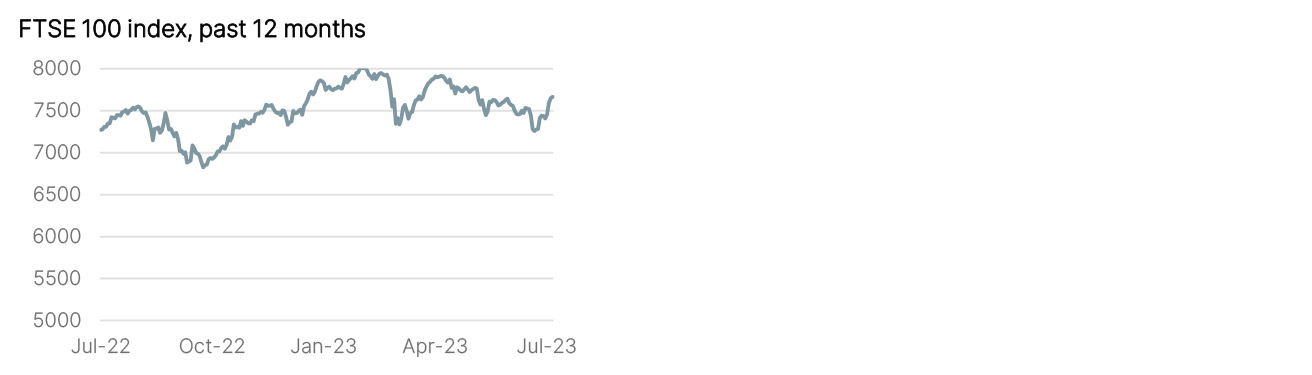

Welcome to our Economic Highlights, bringing you market updates from across the UK, US, Europe and China, as well as the FTSE weekly winners and losers.

Inflation cooled faster than expected in June, ending a four-month run of higher-than-expected prints. Headline CPI inflation was recorded at 7.9%, down from 8.7% in May (versus a 8.2% forecast). Although falling fuel prices were a significant drag on the headline measure once again, there were also encouraging signals from the stickier core measure, which excludes food and energy. After the annual rate unexpectedly accelerated in May, there was a dip down in June to 6.9% from 7.1%, again lower than estimates of 7.1%. The fall was aided by an easing in restaurant and hotel price inflation, likely assisted by softer food and energy price pressures, as well as lower furniture and household good prices. But lower inflation seems to come with slowing activity. The composite Purchasing Manager survey slid by 2.1 points to 50.7, marking a six-month low, with both services and manufacturing in retreat. And with private sector firms passing on higher wage costs, there was a further increase in average prices charged in July, although at the slowest pace since February 2021.

Data continues to show a remarkably resilient economy. Retail Sales grew by 0.6% month-on-month in June, against an expected rate of 0.3%. Weekly Jobless Claims remain subdued at 228k. After some remarkably strong housing data in May, there was a bit of a reversion in June, which was not entirely unexpected. Housing Starts dropped by 8% month-on-month and Existing Home Sales by 3.3%. With the 30-year mortgage rate still above 7%, the stock of existing houses is not going to be as actively traded as in the past. But household formation should continue to support new builds.

Revisions to eurozone first quarter GDP left growth unchanged rather than down by 0.1%. This means that Europe is no longer officially in a recession (following a Q4 2022 fall of 0.1% in economic activity), however marginal that might be. But the economy remains weak, as evidenced by the latest PMI survey data. The Manufacturing index hit a new low of 42.7, with Services falling from 52.0 to 51.1. The Composite reading of 48.9 (down from 49.9) does say “recession”. The European Central Bank is still talking about two more 0.25% interest rate increases to come, in its bid to maintain credibility in its fight against inflation, but the market is becoming less certain by the day.

It’s still “wait and see” time in China. With no new data following the latest GDP numbers, everyone is on tenterhooks for some sort of announcement from the government on the subject of stimulus measures, to boost confidence. But these will not be the “borrow to build” incentives we have seen in the past. The real estate sector is still working through its accumulated pile of debt and the focus is on completing existing projects rather than starting new ones. The key will be in trying to get consumers to release some of their savings into the domestic market, which could involve the provision of stronger social safety nets or even the some form of cash handouts. With youth unemployment running north of 20%, the government will be motivated to act at some point owing to the risk of social unrest.

The information in this document is for private circulation and is believed to be correct but cannot be guaranteed. Opinions, interpretations and conclusions represent our judgement as of this date and are subject to change. The Company and its related Companies, directors, employees and clients may have positions or engage in transactions in any of the securities mentioned. Past performance is not necessarily a guide to future performance. The value of shares, and the income derived from them, may fall as well as rise. The information contained in this publication does not constitute a personal recommendation and the investment or investment services referred to may not be suitable for all investors. Copyright Investec Wealth & Investment Limited. Reproduction prohibited without permission.

Member firm of the London Stock Exchange. Authorised and regulated by the Financial Conduct Authority.

Investec Wealth & Investment Limited is registered in England.

Registered No. 2122340. Registered Office: 30 Gresham Street, London EC2V 7QN.