Just The Time Of Year

21 September 2021

It’s fair to say that there is no end of things to worry investors at the moment, and we are watching them carefully.

4 min read

21 Sep 2021

August inflation data surprised on the upside, with the headline Consumer Price Index moving from 2.0% in July to 3.2% (f/c 2.9%). Around 90bps of this increase was due to base effects as we start to lap the “Eat Out to Help Out” discount from this time last year. Other highlights included a 5.9% increase in hotel prices, reflecting the strong staycation theme. We have almost certainly got another full percentage point of higher inflation to come, with a 0.7% contribution from higher utility prices in October and another 30bps from clothing base effects in November, leaving the UK well on track for mid-4% inflation by the year end. However, even if this scenario plays out it is well telegraphed and is unlikely to cause the BofE to rethink its “transient” take on the current inflationary impulse.

Friday saw the release of the monthly University of Michigan Sentiment Survey, and, in the end, it was a bit of a damp squib, with only marginal changes from the August survey. The overall measure of sentiment edged up from 70.3 to 71, with the level still well down from a recent high of closer to 90. The impact of higher prices for homes, cars and durable goods is still cited as the main reason for this. The all- important inflation expectations component was little changed. The 1-year-ahead measure crawled up from 4.6% to 4.7%, suggesting that consumers see the current spike as being prolonged for at least that long. On the other hand, the 5-10-year expectation held steady at 2.9%, although still well above its pre- pandemic range of 2.3%-2.6%. Earlier in the week, official Consumer Price data for September showed little change from August, with a headline rate of 5.3% (vs 5.4%).

Little by way of economic data to report from Europe, and so we turn to politics, as we enter the final leg of the German Federal elections. Olaf Scholz and the SDP remain comfortable leaders in the polls, with 26% of the vote versus 21% for the CDU. Herr Scholz set out his terms for a coalition partner over the weekend, with taxing the rich and raising the minimum wage as non-negotiable policies. That’s the way politics is going in many Western democracies.

The latest data from China missed expectations on most fronts, with Retail Sales in August increasing only 2.5% (f/c +7.0% vs July’s +8.5%) as the latest round of Covid restrictions took their toll. Industrial data was also weaker than expected, with output growth of 5.3% down from 6.4% in August (f/c +5.8%). The latest industry to be subject to tighter regulation was Casinos in Macau, leading to sharp share price falls in affected stocks.

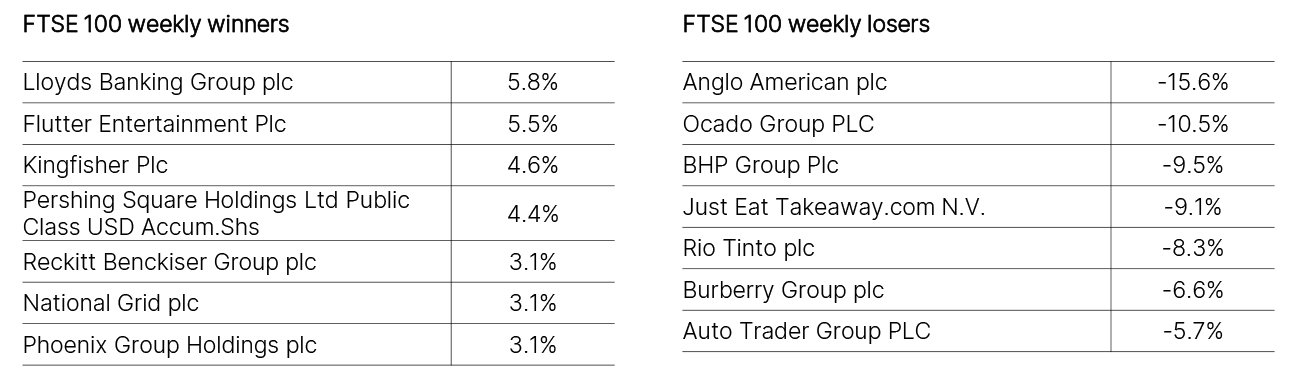

Source: FactSet

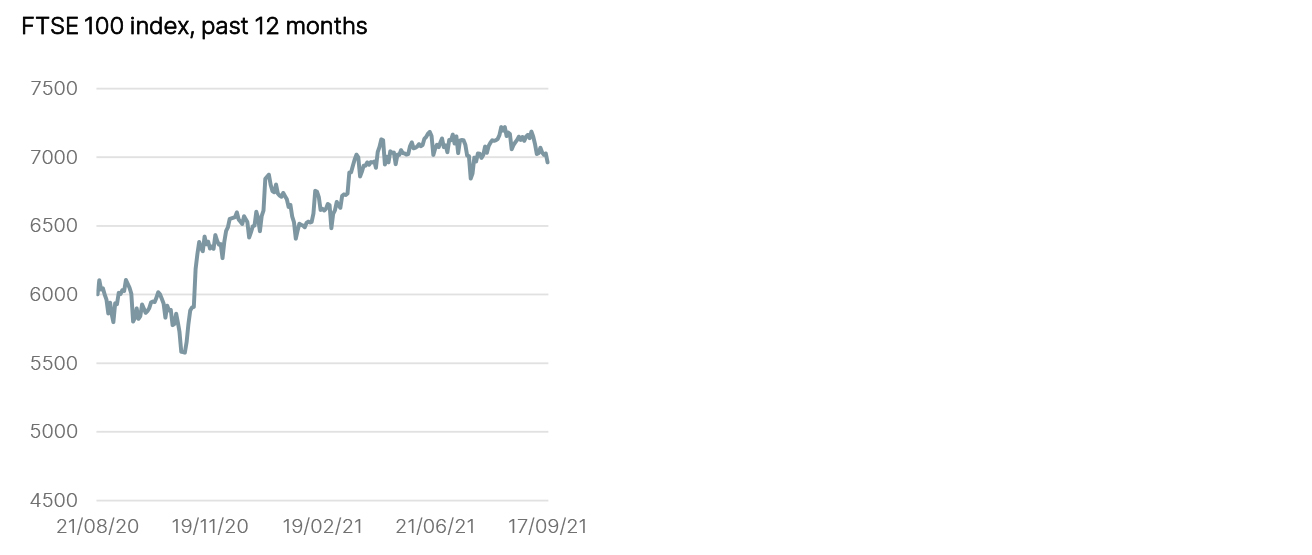

Source: FactSet