Swiss CoCo Pops

21 March 2023

Following troubles at SVB and Credit Suisse, the market has been pretty sanguine about the risk of increased loan losses for various reasons.

5 min read

21 Mar 2023

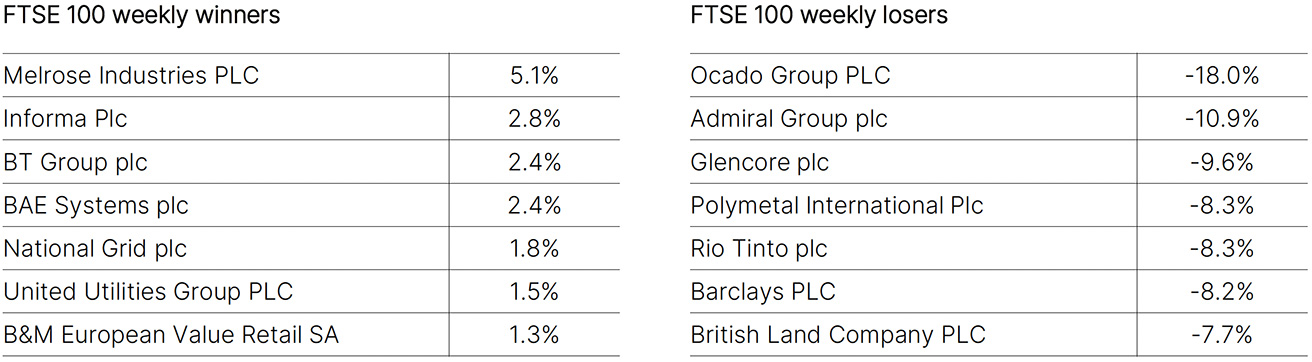

Welcome to our Economic Highlights, bringing you market updates from across the UK, US, Europe and China, as well as the FTSE weekly winners and losers.

The UK labour market remains resilient. The unemployment rate held steady at the low level of 3.7% in the three months to January, confounding the consensus forecast for a tick up to 3.8%. The change in the number of unemployed compared to the previous quarter was negligible (+5k), despite the participation rate for those aged 16-64 nudging up to 78.7%. Although this is 0.4%pts higher than at its trough, participation remains the Achilles heel of the UK economy: it is merely around the levels spring of 2022 and still a long way below the pre-pandemic level of 79.8%. This contrasts with the experience of the Euro area, which has seen participation rise above pre-pandemic levels, and also that of the US, which is now close to that point. On the employment side, there was a quarterly rise of 65k in the three months to January, equating to 0.2% growth. A fall of 14k in the number of full-time employees was more than offset by rising self-employment (+92k) and part-time employment (+88k). Vacancies remain extremely high relative to the number of people that are unemployed, pointing to ongoing tight labour market conditions. Wage growth eased from December’s 6.0% to 5.7% in the three months to January (as expected), and regular (ex-bonus) pay growth nudged down from 6.7% to 6.5% (consensus 6.6%), as slightly slower growth in the private sector (7%, vs 7.3% in December) more than outweighed faster growth in public-sector regular pay growth (4.8% after 4.3%). Nonetheless, the wedge between the two remains noticeably wide. At a time when the jobs market is very tight and pay growth falls short of inflation, pressures for a catch-up in public sector pay growth look likely to persist.

February’s CPI figures were almost bang on consensus. The headline index rose by 0.4% on the month, resulting in a moderation in the annual rate of inflation to 6.0% from 6.4%. The ‘core’ rate ( excluding food and energy) climbed by a touch more than expected on the month at +0.5%, compared with consensus forecasts of 0.4%. The annual rate however was on consensus, slipping marginally to 5.5%. The details were a bit of a mixed bag. Shelter costs increased strongly again, by 0.8% on the month, despite the weakness of the housing market. Meanwhile, food costs posted a month-on-month gain of 0.4%, but the annual pace moderated for the sixth month in a row, to 9.5% from 10.1% in January. The price of second hand cars and trucks fell by 2.8% on the month – the change on the year now stands at -13.6%. The month-on-month data suggests that while headline inflation will continue to fall, it might yet not fall as fast as the Fed would like to its 2% target. The Fed would be more inclined to be more hawkish on policy, were it not for events in the banking sector.

Last week’s meeting saw the European Central Bank (ECB) stick to its very well telegraphed 50bp increase in all its key rates, meaning that the Deposit rate now stands at 3.00%, the Main refinancing rate at 3.50% and the Marginal lending rate at 3.75%. Justification for sticking to the planned 50bps increase in rates was firmly placed on inflation being expected to remain too high for too long. It is core inflation that continues to trouble the Governing Council (GC) given its still elevated level: HICP inflation ex-food, energy, alcohol and tobacco recorded a new high in February at 5.6%. President Lagarde herself noted that the GC was not seeing a lot of improvement in this space. Despite the recent financial market troubles the desire to address inflation remained front and centre, with the ECB’s executive board only proposing the policy option of a 50bps increase. Madame Lagarde revealed this proposal was supported by a very large majority, with only three or four dissenters who had preferred to wait for the uncertainty over banking developments to clear rather than disagreeing with the decision per se.

The 3.5% year-on-year increase in retail sales in January and February followed two consecutive months of declines at the end of last year and marked the strongest gain in a year. Notably, restaurant and catering sales (the only service sector category in the report) jumped by 9.2% year-on-year following a double-digit drop in December. Meanwhile, sales of consumer goods increased by a more moderate 2.9%. The relative strength of the rebound in demand for services versus goods is consistent with the gradual reopening of the economy. Industrial production growth slowed from 3.6% year-to-date year-on-year in December to 2.4% in February – slightly below expectations of a 2.6% increase. And although fixed asset investment accelerated from 5.1% year-on-year to 5.5% year-on-year, the overall increase conceals an ongoing deceleration in private investment growth, which at 0.8% year-on-year in February is the slowest growth in over two years. Additionally, property investment continued to contract, though the pace of decline moderated to -5.7% year-on-year. We continue to believe that China’s total economy has recovery momentum, although this will be led by consumption and not the speculative building and investment booms we have seen in the past.

The information in this document is for private circulation and is believed to be correct but cannot be guaranteed. Opinions, interpretations and conclusions represent our judgement as of this date and are subject to change. The Company and its related Companies, directors, employees and clients may have positions or engage in transactions in any of the securities mentioned. Past performance is not necessarily a guide to future performance. The value of shares, and the income derived from them, may fall as well as rise. The information contained in this publication does not constitute a personal recommendation and the investment or investment services referred to may not be suitable for all investors. Copyright Investec Wealth & Investment Limited. Reproduction prohibited without permission.

Member firm of the London Stock Exchange. Authorised and regulated by the Financial Conduct Authority.

Investec Wealth & Investment Limited is registered in England.

Registered No. 2122340. Registered Office: 30 Gresham Street, London EC2V 7QN.