The Epilogue

19 December 2022

The majority of commentators are in the camp that sees economies weakening earlier and faster in the New Year.

5 min read

19 Dec 2022

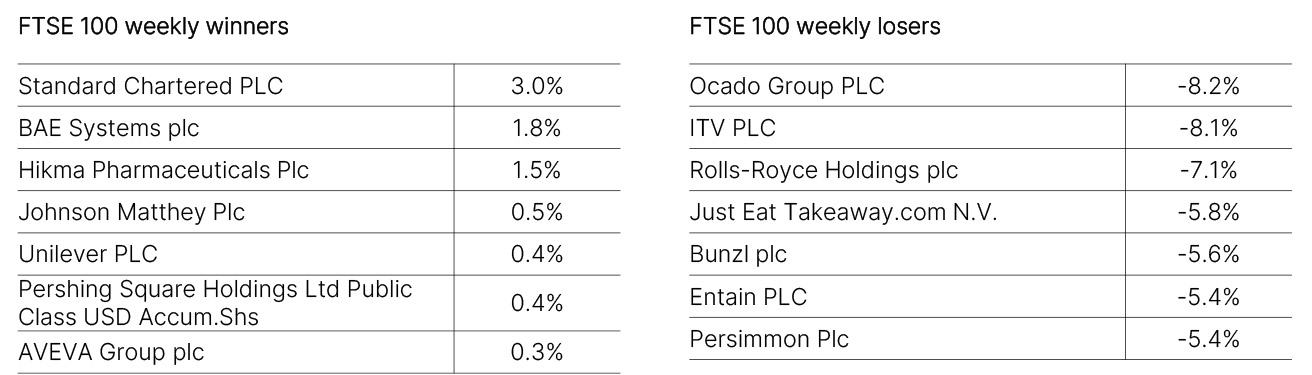

Welcome to our Economic Highlights, bringing you market updates from across the UK, US, Europe and China, as well as the FTSE weekly winners and losers.

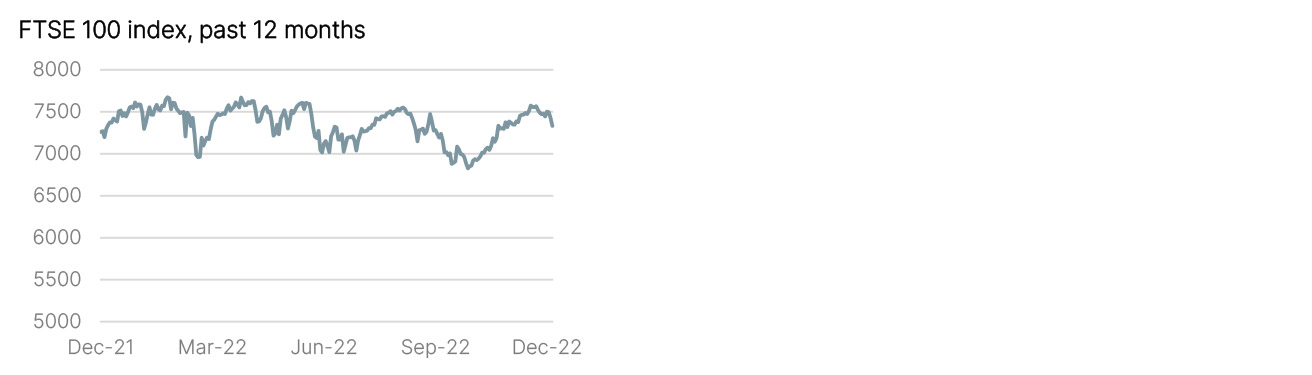

This week’s economic section will focus mainly on last week’s key central banks meetings. The Bank of England's Monetary Policy Committee voted to raise the Bank rate by 50bps to 3.50%, as expected. Once again the vote was split, and this time three ways. Resident doves Silvana Tenreyro and Swati Dhingra voted for no change, while known hawk Catherine Mann preferred a second 75bp increase. The minutes of the meeting noted that although the economy was slowing, some indications suggested that it was more resilient than expected and that it was unclear when the labour market would loosen, although the Bank of England’s own agents’ observations were that the labour market had started to loosen. The committee concluded that labour market conditions overall remained very tight. Indeed members stressed that ex-bonus private sector pay growth had strengthened and was some 0.5% above expectations at the time of the Bank’s Monetary Policy Report last month (not to mention wage demands in the private sector). And so the policy battle seems to be between weaker demand and higher wages, which could readily be described as “stagflation”. The Bank is erring on the side of caution in favour of capping inflation at the expense of the economy for now. Market expectations reflect that, with the Bank rate expected to peak at 4.5% or so next summer.

The Federal Open Market Committee (FOMC) raised rates by 0.5%, down from 0.75% increases at each of the previous four meetings. Most of investors’ attention, however, was on the new dot plots to see what had changed in the Committee’s thinking since the last publication in September. These duly showed a new expected peak in the Fed Funds rate at 5.1% (up from 4.6%) and that is expected to be the rate at the end of 2023. Moreover, only two of the dots indicated a policy rate below 5%, indicating the FOMC was close to unanimous that policy would not need to be eased in H2 next year. Cuts in calendar 2024 from the peak are projected to be only 100bp, though there is a wide range of opinion among the 19 FOMC members about where rates will end 2024: one member suggests rates will be still at peak, while one other thinks rates will have fallen by 200bp. There were updated forecasts for both GDP and inflation next year, with growth still positive but now projected at only 0.5% versus 1.2% back in September. Still no recession in their outlook, although if unemployment does rise to 4.6% as they forecast, that is a jump (from the low of 3.5%) that has never not led to recession in the past. Perhaps surprisingly, their expectation for core inflation increased, from 3.1% to 3.5%, in contrast to the better-than-expected CPI numbers released the day before. Clearly there is a desire within the Fed to sound hawkish, in the hope of suppressing consumer spending through the threat of tighter policy; what might make the Fed loosen policy in H2 (as markets predict) is either a much weaker economy or a faster decline in inflation. What is less contentious is that the next Fed meeting in February will contain another rate increase, but whether it’s 25bp or 50bp will be influenced by the next couple of months. Policy therefore does remain data dependent. Interest rate futures continue to show that the market thinks the Fed is bluffing, with forward rates pricing in 4.4% by December 2023.

Again as expected, the European Central Bank (ECB)'s Governing Council raised its key benchmark rates by 50bps, taking the Deposit rate to 2.00%. However, the Council noted that it judged rates still needed to rise 'significantly' and 'at a steady pace'. This was a stronger tone than expected, helping to push the euro higher. There was also further guidance on balance sheet reduction, which will begin at a 'measured' pace from March via organic runoff of securities. The pace will be €15bn/month until Q3 2023. The decision also came with an updated set of staff economic projections. For the first time, ECB forecasts now envisage a recession, albeit a 'short-lived and shallow' one. Once again, inflation forecasts were lifted, with core price growth now seen at 4.2% in 2023 (prior: 3.4%). No dot plot is available from the ECB, but futures markets expect rates to peak around 3.25% in mid-2023. On the same day there were rate rises delivered also in Norway (+0.25% to 2.75%) and Switzerland (+0.5% to 1%), not forgetting the Philippines (+0.5% to 5.5%) and Taiwan (+0.125% to 1.75%).

China’s main monthly data disappointed, with both industrial production and retail sales much weaker than expected. The former rose by only 2.2% at an annual rate, much slower than the 5% year-on-year recorded in October and the 3.5% consensus forecast, while the latter fell sharply by 5.9% year-on-year compared with the annual decline of 0.5% in October. This weakness gave the authorities another motive to loosen Covid restrictions. Meanwhile the exit from zero-Covid is proving predictably difficult, with reports of the virus ripping through a population lacking in herd immunity. Even those uninfected are exercising more caution, with real-time data such as subway journeys showing a sharp drop in passenger numbers. The fact that the government has stopped publishing infections and fatality numbers is unhelpful, but probably a sign that they are not good.

The information in this document is for private circulation and is believed to be correct but cannot be guaranteed. Opinions, interpretations and conclusions represent our judgement as of this date and are subject to change. The Company and its related Companies, directors, employees and clients may have positions or engage in transactions in any of the securities mentioned. Past performance is not necessarily a guide to future performance. The value of shares, and the income derived from them, may fall as well as rise. The information contained in this publication does not constitute a personal recommendation and the investment or investment services referred to may not be suitable for all investors. Copyright Investec Wealth & Investment Limited. Reproduction prohibited without permission.

Member firm of the London Stock Exchange. Authorised and regulated by the Financial Conduct Authority.

Investec Wealth & Investment Limited is registered in England.

Registered No. 2122340. Registered Office: 30 Gresham Street, London EC2V 7QN.