The positive impact myth

13 June 2022

Why buying the shares of companies that ‘do good’ is not enough.

4 min read

13 Jun 2022

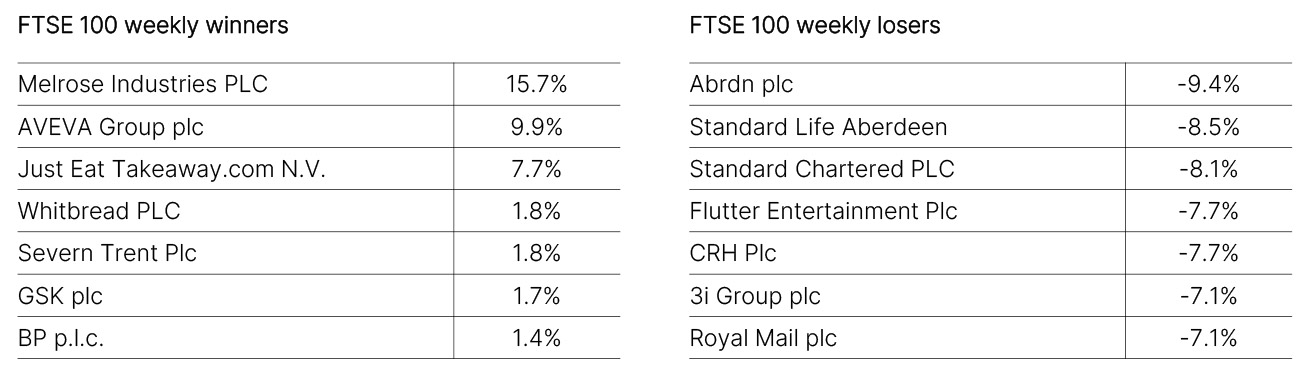

Welcome to our Economic Highlights, bringing you market updates from across the UK, US, Europe and China, as well as the FTSE weekly winners and losers.

UK GDP in April contracted by -0.3%, which was weaker than the consensus figure of 0.1%. Looking at the breakdown, the ending of the NHS Test & Trace scheme caused a -5.6% drop in human health and social work activity, which led to the broader service sector contracting by -0.3% in the month. Retail sales were 1.4% higher in the month, however it is uncertain how more growth is likely in the near term given the high inflation prints. Manufacturing output contracted by 1% in April as companies faced higher costs and difficulty in sourcing material.

The market waited all week for the latest US inflation data and it did not make comfortable reading when delivered on Friday. The headline Consumer Price Index rose 8.6% in May from a year earlier. This was above expectations and constituted a new cycle high for annual inflation. Food and Energy prices were the main drivers, meaning there was some consolation in the fact that the core rate (which excludes those elements) fell back from 6.2% to 5.9% (although was still higher than forecast). But used car and clothing prices, which had declined in April, were on the rise again, illustrating the worrying stickiness of this bout of inflation. Price calculations based on housing costs also look set to contribute to higher inflation in the months ahead. This was the last major data release ahead of the Federal Reserve’s meeting this week. Although markets had been expecting rate rises of 0.5% in both June and July, the prospect of a more aggressive 0.75% rise this week is no longer out of the question as inflation is currently public enemy number one. The influence of inflation on consumer sentiment was visible in the latest University of Michigan sentiment survey, which fell to a 50-year low. Worryingly, longer-term inflation expectations started creeping up again too, from 3% to 3.3% on a five-year horizon.

As unanimously expected by all economists polled, the European Central Bank Governing Council kept policy rates on hold at last week’s meeting, with the Deposit rate remaining at -0.50%, the Main Refinancing rate at 0% and the Marginal Lending rate at +0.25%. Also in line with what was previously flagged, the ECB announced the end of asset purchases under the APP programme, originally initiated in 2014, as of 1 July. Finally, the ECB was explicit in its guidance that it intends to raise its key policy rates by 0.25% at its next meeting on 21 July and that it anticipates following this up with a further rate rise in September. The size of the second rise remains under debate, but the Governing Council appears to be leaning towards more than 0.25%: the guidance stresses that ‘if the medium-term inflation outlook persists or deteriorates, a larger increment will be appropriate at the September meeting’. Beyond that, the ECB anticipates a ‘gradual but sustained path of further increases in interest rates’. Optionality, data dependence, gradualism and flexibility, however, remain key guiding principles.

May total social financing, RMB loans and M2 money supply all came in above market expectations following the weak broad credit growth in April. The sequential growth of TSF stock accelerated to 14.4% month-on-month annualised in May, after 5.1% in April. The rebound of May credit data likely reflected a combination of growth and credit demand recovery on easing Covid restrictions, and the strong push by policymakers two fronts: first increasing credit support and accelerating loan extensions; second, accelerating major infrastructure projects. The composition of loans suggests that both household and corporate loan growth rebounded in May. More interest rate cuts are expected in the coming weeks as China continues to try to turn around its economy, although the ongoing effects of the country’s zero-Covid policy will continue to create obstacles.

The information in this document is for private circulation and is believed to be correct but cannot be guaranteed. Opinions, interpretations and conclusions represent our judgement as of this date and are subject to change. The Company and its related Companies, directors, employees and clients may have positions or engage in transactions in any of the securities mentioned. Past performance is not necessarily a guide to future performance. The value of shares, and the income derived from them, may fall as well as rise. The information contained in this publication does not constitute a personal recommendation and the investment or investment services referred to may not be suitable for all investors. Copyright Investec Wealth & Investment Limited. Reproduction prohibited without permission.

Member firm of the London Stock Exchange. Authorised and regulated by the Financial Conduct Authority.

Investec Wealth & Investment Limited is registered in England.

Registered No. 2122340. Registered Office: 30 Gresham Street, London EC2V 7QN.